RNMBF - Rheinmetall: I Wish I Had Bought More In 2021/2022 (Rating Downgrade)

2023-08-22 05:44:44 ET

Summary

- I regret not buying more shares of Rheinmetall when they were cheap, limiting my potential returns.

- I'm considering selling my position in Rheinmetall due to the company's high valuation and the need to rotate my capital.

- Rheinmetall's growth is driven by the re-arming and military focus in Germany, Europe, and globally, which supports positive trends and targets.

- It is now growing too expensive, and I believe the time has come to change my rating.

Dear readers/followers,

There are certain companies where I can kick myself for not buying more when they were cheap. One of the rare drawbacks of diversification and position limiting and investing approaches is that it limits you from going "all in", or even "a lot in" when you see a significant opportunity on the market.

Rheinmetall ( RNMBF ) ( RNMBY )was such an opportunity, and while I did "BUY", and while my recommendations have generated outsized returns relative to the market...

Seeking Alpha Rheinmetall (Seeking Alpha)

...the simple fact is, I could have bought a lot more, but didn't. What could have been returned in nominal cash values in five or six digits are instead much smaller, because I size my positions carefully, and only sit on a relatively small position in Rheinmetall at this particular point.

The time has even come to, despite the company's significant upside over time, look to sell off my position with the purpose of rotation of capital. The company trading at over €200/share is unheard of, and the business has long since left behind any claim to valuation logic.

In this article, I'll update you on the company, why I consider current analyst averages of over €300/share to be difficult to justify, and why I may rotate my position in the company on a forward basis, taking home a very good profit despite not investing early enough.

Rheinmetall - A valuation downgrade may be necessary as we see if some of these lofty targets materialize

So, whenever a company with cyclicality and that has essentially, at least prior to 2021, gone absolutely nowhere since 2005, sees this sort of demand growth, the question always becomes if this growth is in any way sustainable over the long term.

Current S&P Global analysts and FactSet analyst estimates, as well as company expectations, would say that "yes, it's indeed possible". I would tread a bit more carefully. Rheinmetall, which tends closer to 12-15x P/E, is currently trading at almost 20x P/E due to a growth in adjusted EPS of over 1,600% in 2021, another 18% in 2022, and more double-digit growth rates expected all the way to 2025E and beyond.

This growth is, of course, largely based on the re-arming and refocus on the military we see not only in its home country Germany, but across Europe and the world. It's also the reason I haven't yet sold my shares - the trends still point in a pretty positive direction - as do overall targets and concrete results.

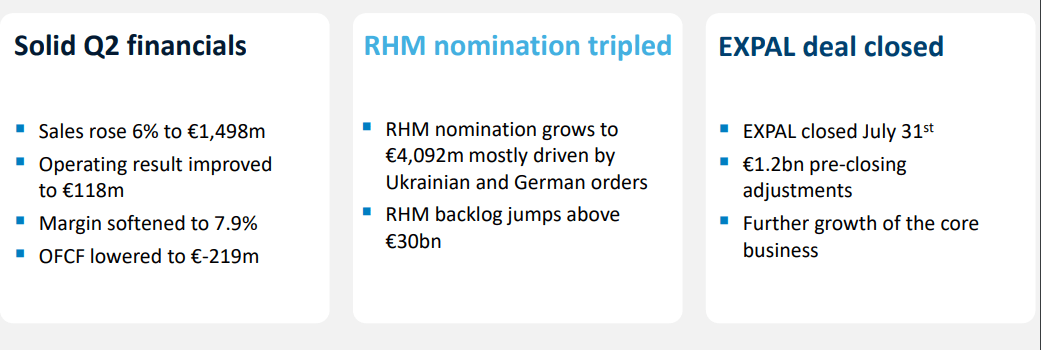

We have the 6-month results for this year - less than 15 days old. So data is fresh. And trends are encouraging, justifying the confidence and upside in the company.

Rheinmetall IR (Rheinmetall IR)

{kind=link}

The company has both a military and automotive appeal. Prior to the Ukraine war, the company's appeal was extremely limited, due to the very underdeveloped nature of most of the European militaries at the time. This has obviously reversed now. This is followed and presented very clearly by the company.

Rheinmetall IR (Rheinmetall IR)

{kind=link}

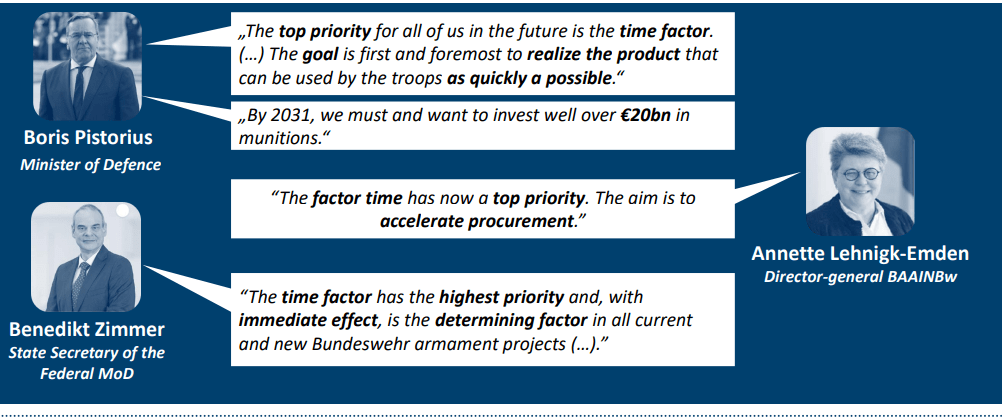

And obviously, Germany has a long way to go here. A long, long way - but they've now begun this journey - with Rheinmetall continuing to be a net beneficiary of such trends. The company offers almost everything that the army is looking for in key segments, and with NATO spending now going to and above 2% of the GDP, the company is in for significant gains.

We're talking Tank, Artillery, and Med-Cal munitions, we're talking both tactical and logistical vehicles, we're talking digitization systems , and we're talking air defense systems - both stationary and mobile systems.

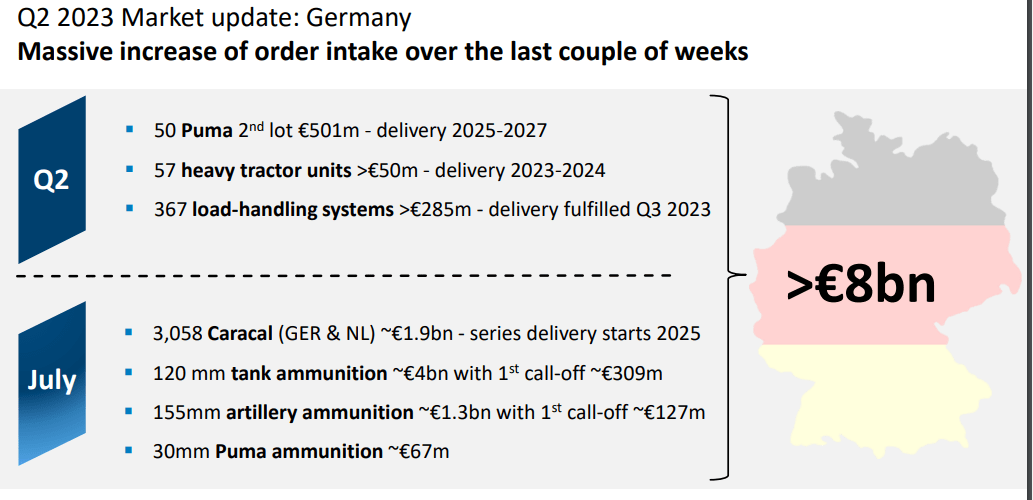

Take a look at this market update.

Rheinmetall IR (Rheinmetall IR)

{kind=link}

The company also has market appeal in the US, with Rheinmetall securing almost $700M in order value, of an overall program size of $45B. International markets overall continue to be a significant positive for this company, with contracts from Norway, Australia, and Austria, worth around €1B in total for 2Q.

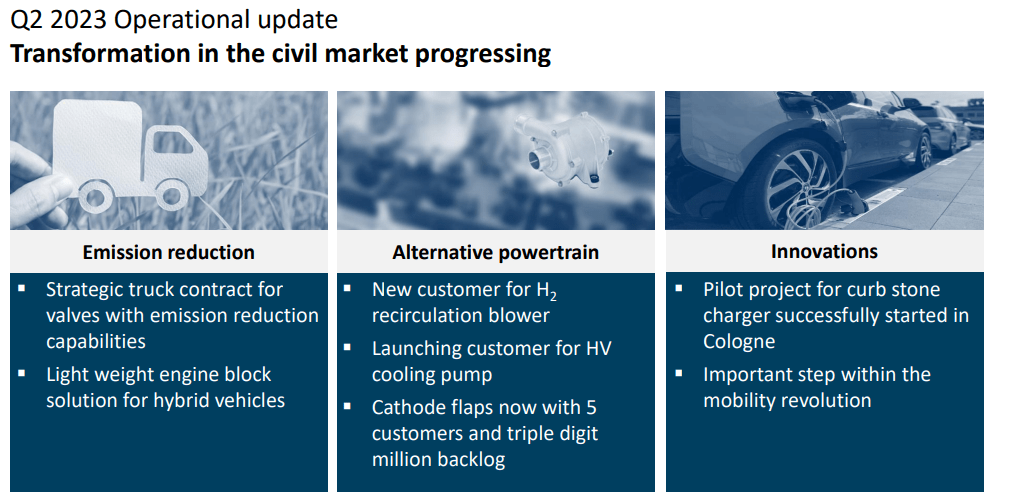

While the company of course wants to highlight its military market, what was once the selling point for Rheinmetall continues to develop as well - the civil market is working with alternative powertrains, ESG, and other innovations.

Rheinmetall IR (Rheinmetall IR)

{kind=link}

In short, we have continued sales growth, we continued stable operating results, and margins. We have continued growing EPS. The company is increasing inventory in anticipation of demand. The company is also strengthening liquidity, issuing bonds, but with an overall cash position of well over €1.3B and undrawn credit of nearly €1B. The company has BBB from Moody's and currently stands at a 0.9x net debt/EBITDA.

The company remains exposed to main vehicles, Weapons/munitions, and Sensors - all very appealing sectors. The company's backlog now stands at over €30B, a YoY increase of almost 17%.

As geopolitical tensions increase, there have been talks and decisions about an F-35 production plant in Weeze. The plant will produce center fuselages, set to commence in 2 years, with a capacity of at least 400 sections per year, with demand increase possible over time. The F-35 has a substantial pool of countries using it, from Greece back in 2010, to Spain having agreed with 40 planes by 2024. This increases Rheinmetall appeal as well.

The company is taking advantage of very strong top-line and profit trends, delivering significant CapEx on the investment side (up 15% to €700M for the full year), to ensure future growth.

The sales load is arriving as the company expected - backend-loaded, with significant amounts of more sales towards the end of the year.

In short, Rheinmetall looks ready to take on the world, and results and forecast are looking better than they have for over 20 years, all due to a worsened geopolitical macro and overall security situation in Europe - and the world. What could possibly derail this?

A few points, because I do want to be a voice of caution here.

First of all, many of these positives are due to Ukraine and the situation there. If we move towards a ceasefire or pause in hostilities, I am almost 100% convinced that this will cause a significant hit to the company's share price. While I am unwilling to speculate at this point when such a development will come, I am almost certain that it will come, as both the Russian and Ukrainian public is starting to get war-weary. Ukraine will, I believe, fight as need be - but there will be stronger voicing for talks as we move forward in 2023 and into 2024. Any decline in hostilities, if formal, will serve to start to deflate some of these military beneficiaries somewhat.

In short, I believe that if you missed out on military companies when they were cheap, and prior to becoming as highly valued as they are now, you should be careful in entering.

It's always hard being the one lone guy (or few) that takes the contrarian view. In this case, that means saying "What if we go down?". Order trends are solid. I believe things are safe for the near future. But the potential for a downturn is there, and if we do see a softening of demand or even just a slowdown, I believe the company may see some normalization to around 14-16x P/E.

Just what would this mean for you or me?

Rheinmetall - The valuation is lofty

Since my last article, the company has broken through my PT of €180, and moved well beyond €200/share to a current level of €249. I am as of this article increasing my share price, but I'm also saying that this company is not worth €250 conservatively. Furthermore, it does not have an annualized 15% upside on a conservative forward basis from this point onward.

That means that I am shifting my thesis to a "HOLD". And I am holding here - I'm not selling, but I'm also not adding more at this price.

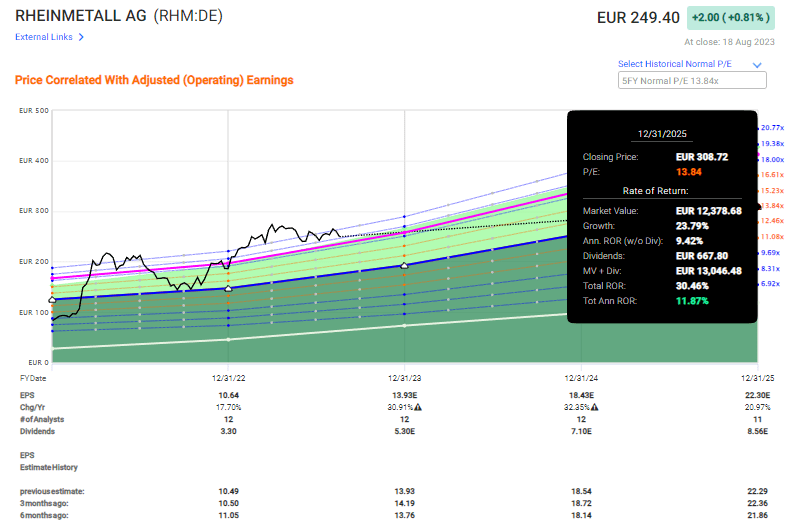

Rheinmetall valuation and forecasts work off the assumption that growth is going to be double-digit and seemingly unending here. That is not a thesis I agree with - not even remotely. However, even if you were to expect that, and forecast it at 14x P/E on a forward basis, which would be conservative, the meager 1.7% yield means that your rates of return would look something like this.

Rheinmetall upside (F.A.S.T graphs)

{kind=link}

12% isn't enough to interest me - not if bought at valuations well above the company's historical average. I am not saying that the company will drop down here, though I am saying that I believe that if we are at €300/share in 2-3 years, we should consider ourselves lucky - and investors who still hold their shares might be considered having seen a good return.

Rheinmetall seeks to differentiate its appeal primarily from the current European military situation and look beyond Ukraine. This is a very good thing because it's something they must do. But I still believe things to be linked enough for there to be a significant decline in share price if and when we see a move towards peace, which would see the company trade closer to 13-15x as opposed to 20x P/E.

I cannot find specific operational risks I would keep a specific eye on here. This is all macro. S&P Global analysts give the company lofty share price targets We start at €233 and go all the way up to €322. That's compared to less than €100/share price targets less than 2-3 years ago. Some of this makes sense. But the lofty valuations are, as I see things, clearly going a few steps too far here. I believe the company has already "tried" for a higher valuation and we're down slightly from ATH's.

Out of 12 analysts, 7 still have the company at a "BUY". I believe people are still being blinded by much of the growth we've seen in less than 3 years here. I would put the company closer to a 13-15x P/E for the 2023E results. 14.5x P/E comes to around €200/share, and that's where I end up with my current share price target at this time.

I would also remind over-positive investors in Rheinmetall, that historically the company has a 40%+ negative miss chance even with a 20% margin of error on the analyst side. Rheinmetall is not known for being predictable, so a 20-30% annualized upside for the next few years, that's something I find a bit hard to swallow.

I'm not selling yet - but if we see trends going back towards the €275 mark, then I will start cutting loose some of the company's shares here, and do so very happily with over 60% in profit inclusive of FX.

This means I am now changing my target for Rheinmetall, and saying "HOLD".

Questions? Let me know!

Thesis

My thesis for Rheinmetall is as follows:

- Rheinmetall is one of the significantly important German arms and civil production companies, with an appealing sales mix, great margins, and exposure to the current flows when it comes to orders and spending that makes it one of the most attractive plays on the German market.

- At a cheap valuation, I continue to believe you can generate a significant alpha here, and you could be looking at 20-30% annual RoR if the company reaches some of the heights that seem to be implied. But at this time, the upside is too limited to be considered, due to the sheer pricing we're looking at for the company.

- I consider the company a "HOLD" with a PT of €200/share, downgrading my former target since my last article.

Remember, I'm all about :1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Upside, yes. Enough upside, no. I say "HOLD" here.

For further details see:

Rheinmetall: I Wish I Had Bought More In 2021/2022 (Rating Downgrade)