RNMBF - Rheinmetall: Why The Company Is Not Bound For Market Outperformance

2023-11-02 06:53:34 ET

Summary

- I had a successful investment in Rheinmetall but regret not investing more when the stock was cheap.

- Rheinmetall is currently trading at a high valuation with a low yield, making it difficult to see further upside.

- The company is focused on becoming the top choice for the German defense industry and has seen growth in sales and orders.

- I give Rheinmetall a "HOLD" at this time.

Dear readers/followers,

My coverage on Rheinmetall (RNMBF) (RNMBY) has been almost long-term here, and I have been a successful investor in the company, my position being up more than 60% RoR in less than 2 years. Unfortunately, the totality of this upside was limited by the fact that I did not invest "enough" capital when the business was cheap. It's always tricky - you want to invest in a new company, but at what pace? Do you buy a full percent of your portfolio value at once? I do not. I size up carefully - and sometimes this means I miss out on significant growth in the business. This, unfortunately, was a good example of this.

What could have been returned in nominal cash values in five or six digits are instead much smaller, because I size my positions carefully, and only sit on a relatively small position in Rheinmetall at this particular point.

I even sold off most of my position, realizing this profit after the company went to valuation heights that I do not consider to be valid to any extent here.

I downgraded to "HOLD" in my last article - I won't change my stance in this article, but I will show you what I expect from the company.

Rheinmetall - The upside is very difficult to see here

The company, at this time, trades at a normalized P/E of 20x with a yield of less than 1.6%. It's hard to imagine a situation where this business traded at less than 5x P/E, but this has been the case more than once during the last 20 years. In fact, during most of the company's trading history between 2004 and 2020, you'd have underperformed the market by investing in Rheinmetall. Between 2006, prior to the GFC, and 2020, the company's return is less than 2% per year, which is abysmal compared to most indexes.

Frankly, if the Russian invasion of Ukraine hadn't occurred, I believe that Rheinmetall would be trading at the lower valuations we're used to seeing. Thanks to these new defense trends though, the entire industry has been changing for the past 2 years, and Rheinmetall is a very good example of a cyclical gone into overdrive.

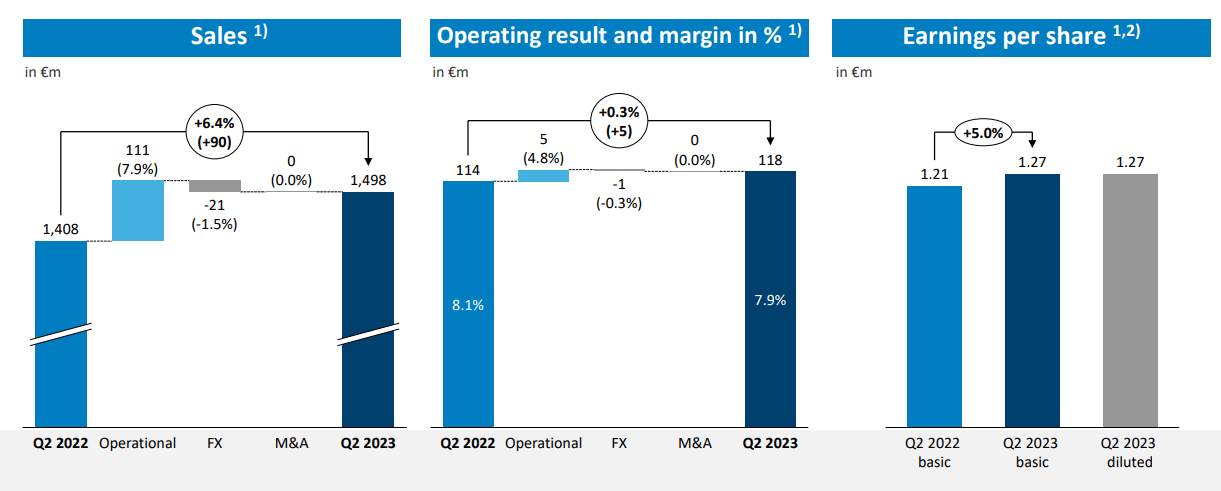

And despite this "overdrive" already being done in 2022, the 2023E period seems to be going well also. We have 2Q results of 6% sales increase, an even higher operating environment, and a very solid backlog that for the first time in a very long time is above €30B for the company.

The company also recently closed its important EXPAL deal, at a €1.2B valuation for pre-closing adjustment, which further grows the core of the business for the company.

The one disadvantage for the company here is a softening margin , which is never good, but can be expected in the current environment.

Rheinmetall's goal is currently simple.

{kind=link}

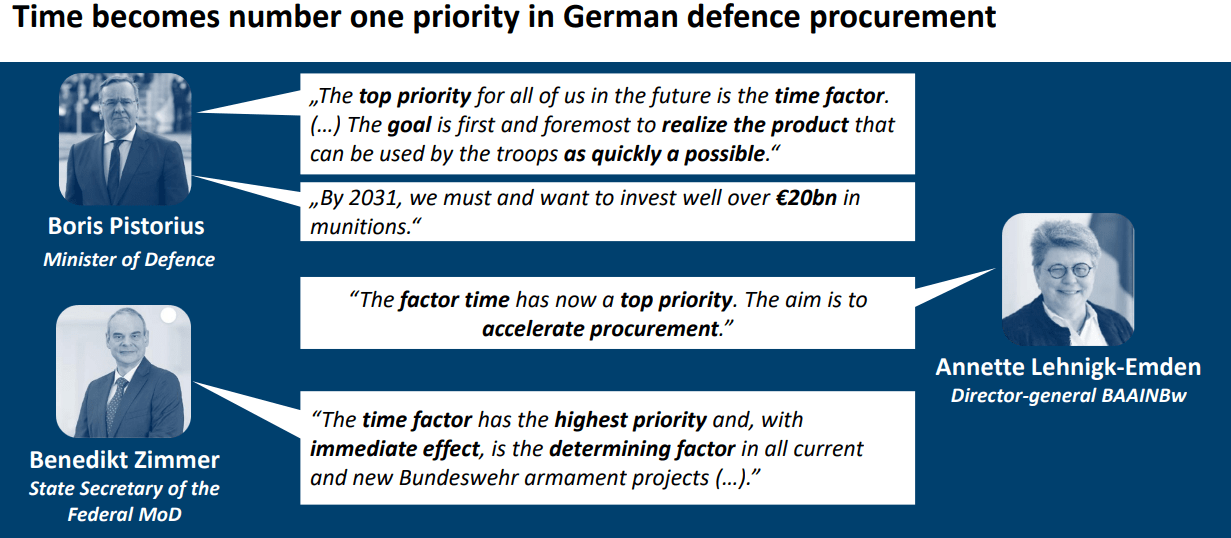

It wants to be the number #1 choice for the Bundeswehr and the German defense industry. Obviously, the company is already enjoying significant advantages from increased defense spending, not just NATO but including NATO, with Germany already closing in on that 2% target. Procurements are already signed, and the 2024E contracts are expected to drive this even higher.

Rheinmetall offers what the nation is looking for, including ordinance for Tanks, Artillery and Medium Calibers, tactical and logistical vehicles, Digital systems for Soldiers such as the Gladius Soldier System and D-LBO, and Air defense systems, both stationary and mobile variants.

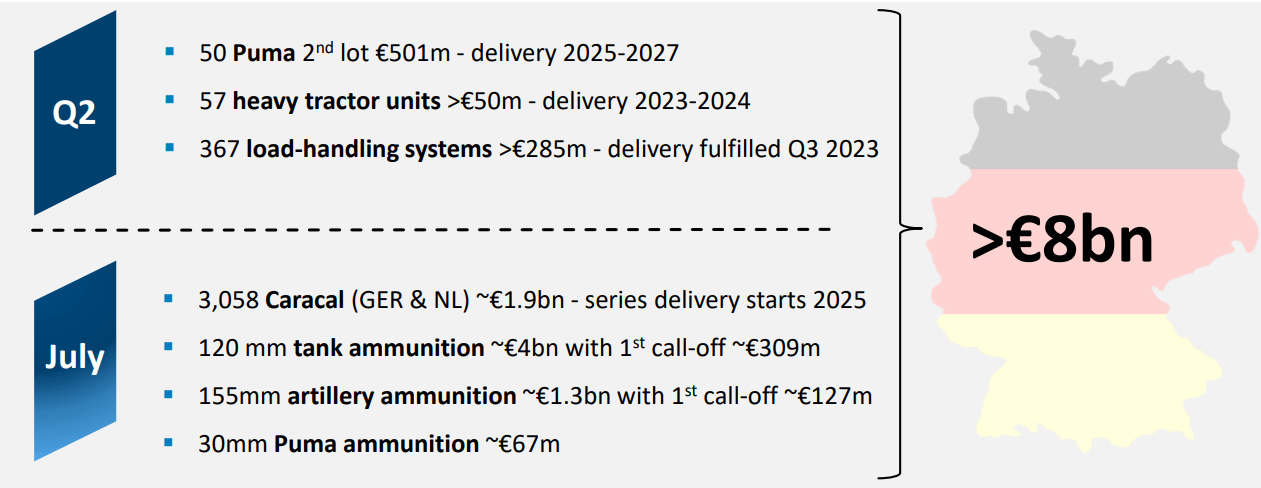

The company was able to record significant order increases in 2Q, with expected sales increases in 3Q as well.

{kind=link}

Rheinmetall is also an XM30 finalist for the US market, with a $700M order value for the company, from a program size of over $45B. This is a long procurement with a long process to the decision. The winner is not expected until the end of 2027, but it's still an interesting process to follow - given that the company has been downselected with funding of $100M for Rheinmetall.

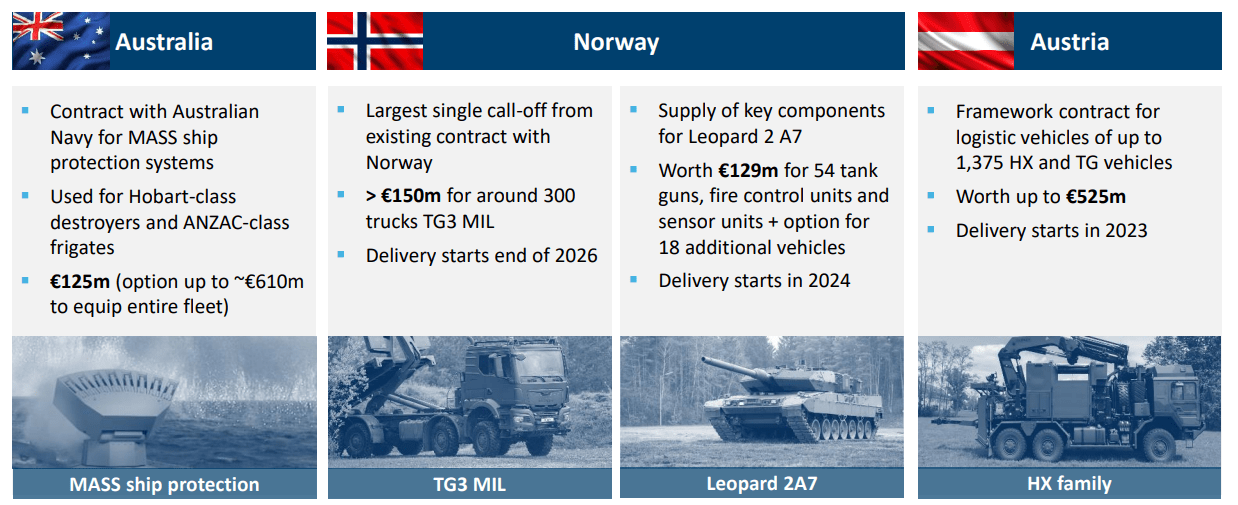

It's not just the German segment, but the international segment as well - with solid wins in Australia, Norway and in Austria.

{kind=link}

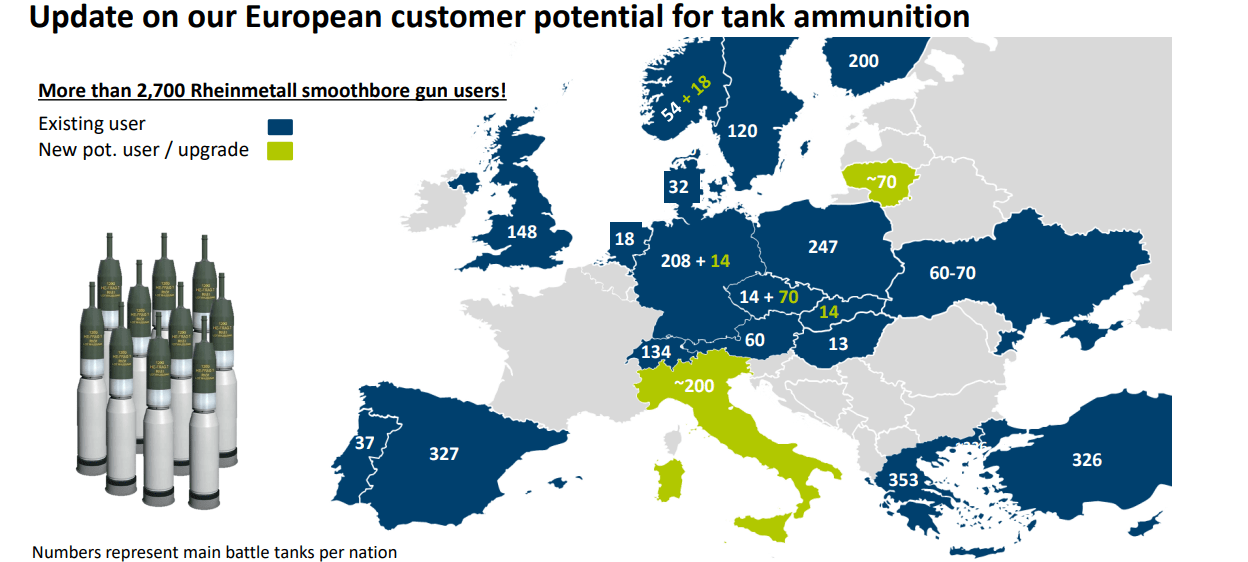

The company is also a major player in the segment of tank munition. Rheinmetall already has a continental market dominance - but in the last few years, we've seeing the company expand into Italy and into the Baltics as well.

{kind=link}

The company is using its proceeds and profit from its various wins and significant increases to R&D into emission reductions, alternative powertrains, innovations, and an overall overhaul and transformation of the Civil market segment.

However, the overall picture that we're seeing is that the company is now facing margin pressure from price increases and inflation, where sales increases are no longer enough to drive earnings significantly higher. This still means that the company is recording its best 2Q ever, in history , but YoY, it's only a slight improvement in EPS and a flat/slight softening in margins.

{kind=link}

This also has to do with that the company is significantly increasing its inventories to react to expected, rising customer demands - we're talking munitions, we're talking vehicle systems and we're talking weapons. Prepayments somewhat mitigated higher WC, but the company still saw increased working capital.

EXPAL is really worth mentioning, and the resulting company finances following this. Following the transaction, the company still has undrawn credit of almost a billion euros, as well as a Baa2 from Moody's with a stable outlook. The company has a stable debt, with a net debt/EBITDA of 0.9x, but it's important to note that this is in the context of the current "upcycle" EBITDA. If there is a downturn in defense, then the company's net debt/EBITDA would rise in reaction to this.

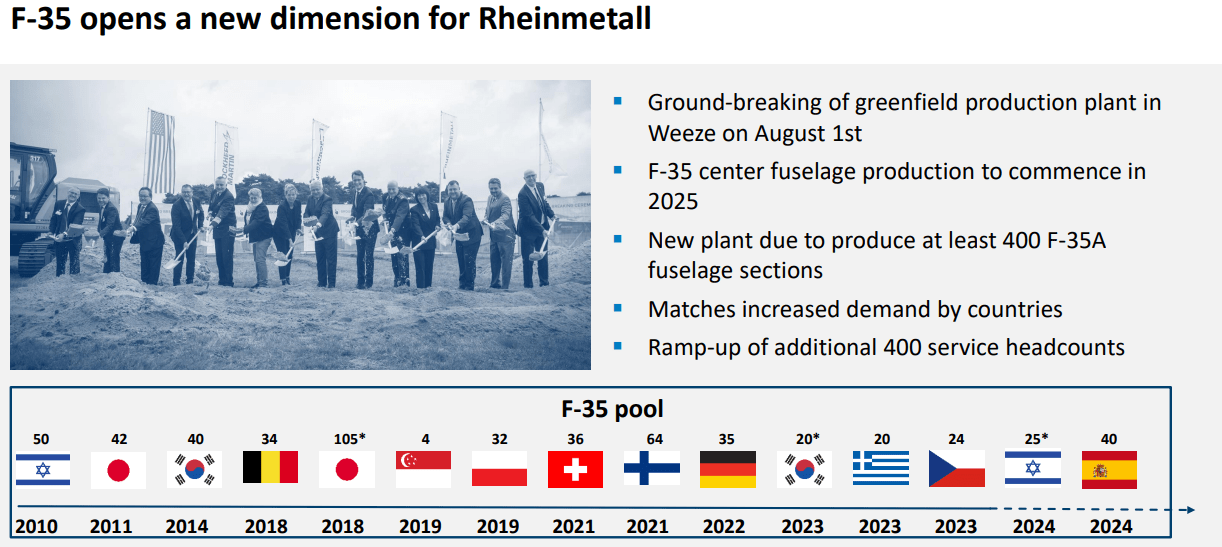

Going forward, I see a few potential catalysts for an upswing. F-35 is one of those. The company is also heavily investing its earnings into new production, new R&D, and other avenues - the CapEx is up €100M for this year alone, which for a company this size is significant.

{kind=link}

I expect 3Q to be a similar quarter to 2Q - as long as the current macro persists, I don't expect a significant downturn for the company at this time - but I do expect this upswing to eventually fade. The current estimates include continued growth, significant growth even, for the next few years. 31% in 2023, another 37% in 2024 and 23% 2025E. I believe this is far too optimistic - unless you believe that the current conflict-filled macro persists for those years, and the current demand stays at current or higher levels. That's where I believe we'll see an evening out eventually.

Let's see how this influences the company's valuation.

Rheinmetall's valuation - Things only have an upside if you expect 20-30% EPS growth per year

The trouble with Rheinmetall is valuation expectation. The company quite often misses analyst expectations. Statistically speaking, company earnings miss estimates over 35% of the time even with a 20% margin of error, which is well above average, with several misses of over 100%, highlighting the cyclicality of this particular business and this business segment.

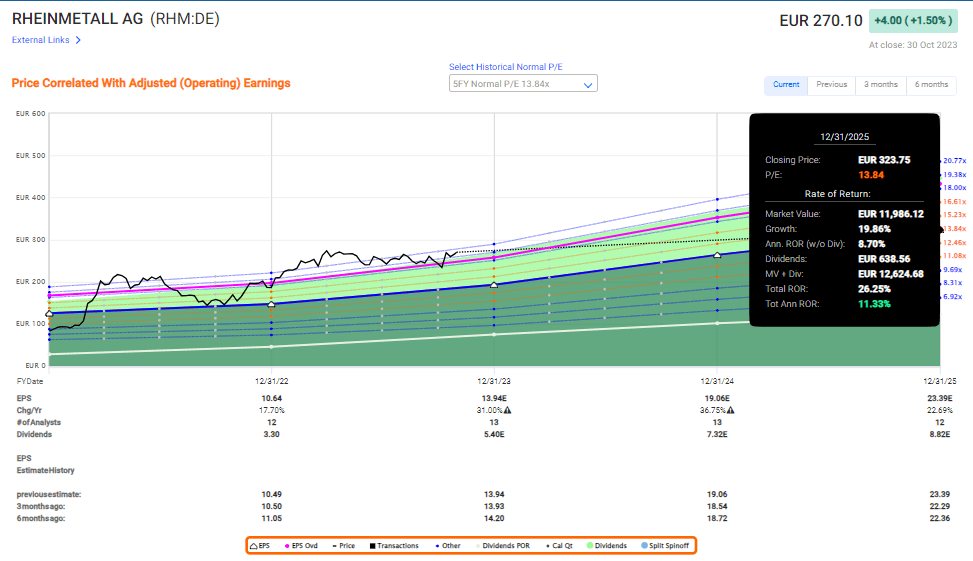

Remember, Rheinmetall typically trades cheaply. We're talking 10-15x P/E - compared to the 20x P/E it is at currently. A 5-year average of 13.8x means that you're currently in the market for a sub-15% return per year, even if these estimates actually materialize and the historical averages are in any way likely.

{kind=link}

The company broke through my initial price target of above €200, above €225, and even beyond this. As of today, it's at €270, which is well above where I believe it should be trading over the long term.

I am as of this article maintaining my share price, but I'm also saying that this company is not worth €250 conservatively. This environment is really coloring and affecting how Rheinmetall is being traded, but I would be very careful here.

This is despite the analyst averages. S&P Global analysts are giving the company a target range starting at €233 and going to €320/share, with average of $298. However, despite this only 5 of the 12 analysts are at a "BUY", and several are at "underperform" here.

This implies an upside of 9% from the current price - but I would call this very exuberant. Rheinmetall seeks to differentiate its appeal primarily from the current European military situation and look beyond Ukraine . This is a very good thing because it's something they must do. I think, however, that this process is as of yet far from done - and I believe these to be very closely linked to a degree where I do not think you should be buying the company.

I would forecast Rheinmetall at around 10-13x P/E over the long term, which to me would imply the highest possible annualized RoR of barely double digits, and even this is, I believe, based on continued growth in the military segment.

Coupled with the company's sub-par and relatively unattractive yield, I do not believe this to be good enough to invest in. I have sold most of my shares of Rheinmetall at a very good profit, and I do not believe in an upswing materially above €275/share for this company - unless something fundamental in the macro changes and this company's earnings go even higher than is currently expected.

But at this time, this company is not a "BUY", and going into 3Q23, it's a definite "HOLD". If the 3Q report we see in over a week changes things, I'll update things here, but for now, I'm happy with my thesis and target.

Thesis

My thesis for Rheinmetall is as follows:

- Rheinmetall is one of the significantly important German arms and civil production companies, with an appealing sales mix, great margins, and exposure to the current flows when it comes to orders and spending that makes it one of the most attractive plays on the German market.

- At a cheap valuation, I continue to believe you can generate a significant alpha here, and you could be looking at 20-30% annual RoR if the company reaches some of the heights that seem to be implied. But at this time, the upside is too limited to be considered, due to the sheer pricing we're looking at for the company.

- I consider the company a "HOLD" with a PT of €200/share, downgrading my former target since my last article.

Remember, I'm all about :1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

An upside, yes. Enough upside, no. I say "HOLD" here.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Rheinmetall: Why The Company Is Not Bound For Market Outperformance