RMGNF - RHI Magnesita: Recession Fears Hide The Underlying Value

Summary

- Recession expectations have pushed the stock price of RHI Magnesita below its intrinsic value.

- The company's margins are more stable than what the market expects.

- In my view, RHIM is a buy for a patient long-term value investor.

Theses

RHI Magnesita N.V. (RMGNF) is a dull but necessary niche business currently trading at 14% long-term average free cash flow yield based on my estimates. The market is selling the stock due to recession fears; however, it is already trading below its intrinsic value and is also less cyclical than the market expects. I can't see an immediate catalyst to push the stock price higher; perhaps that is why the stock is trading so low. However, if you are happy to hold value, it will likely lead to double-digit returns over time, and meanwhile, you can take advantage of the stock volatility.

Overview

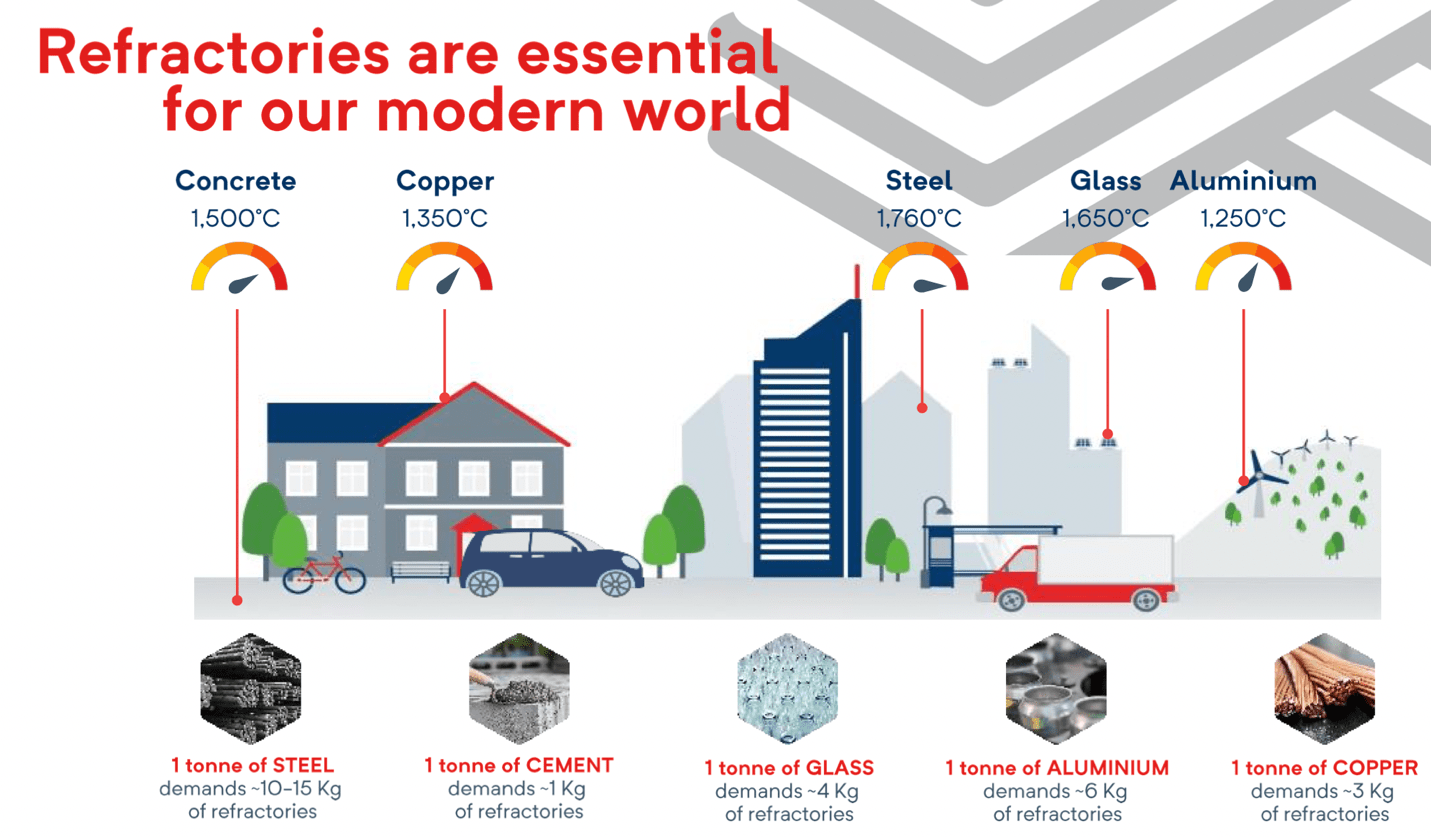

RHI Magnesita is a global refractory producer. Refractory products are used as heat shields mostly in steel production and in the production of cement, glass, aluminum and copper as well. Steel manufacturing consumes the most significant number of refractory products, and steel producers account for 70% of RHI Magnesita’s revenues.

{kind=link}

RHIM investor presentation

For international investors, they are listed on the London and Vienna stock exchanges. In case you only have access to the US stock market, there is an OTC listing ( OTC:RMGNF ), but because of the low liquidity, it may take time for you to buy and sell positions, or you may not be able to do so at all. Also, trading the OTC stock rather than on the London exchange will often result in less favorable bid and ask prices.

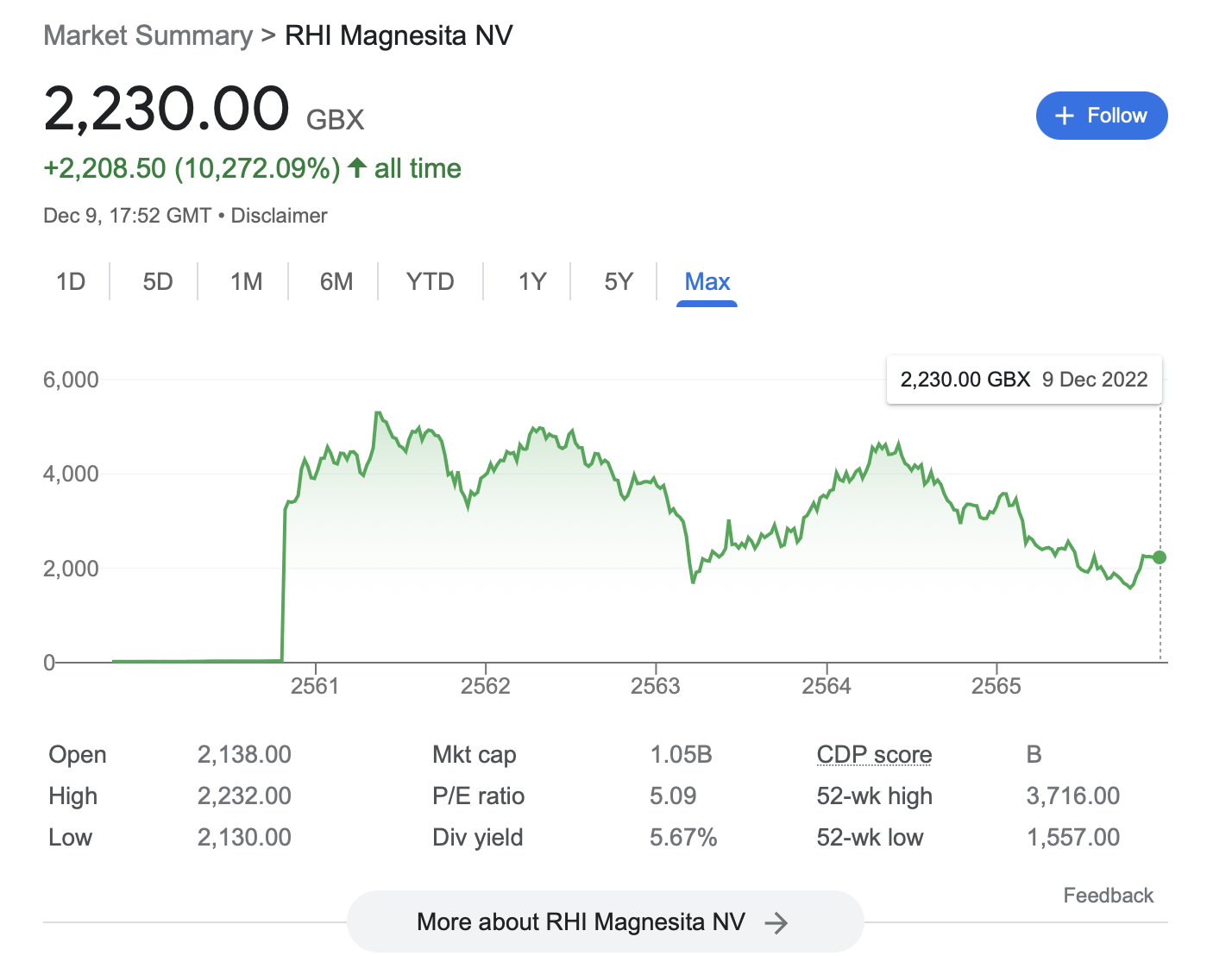

At the moment of writing, this article the market cap is £1.05 billion or €1.22 billion. It is a relatively small business in a quite unknown industry, so there are likely not too many people following the stock. I will use euros for the stock valuation as their financial statements are translated into euros.

{kind=link}

Google Finance

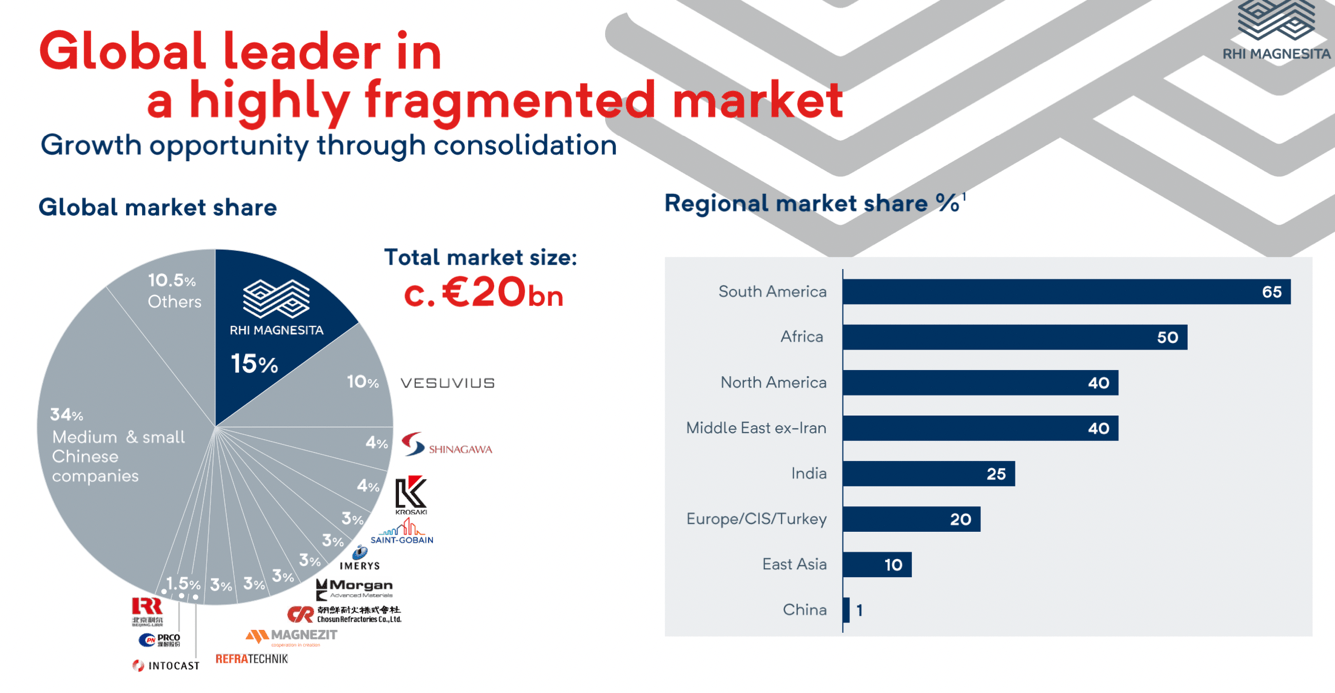

The entire refractory sector’s annual revenues are €20 billion. In 2017 RHI merged with South American refractory producer Magnesita , and they became the market leader with a 15% market share or 30% when excluding China. Overall, the sector is very fragmented and full of small producers. Part of their strategy is to acquire the smaller companies and, as the industry consolidates over time, they can hopefully increase profit margins.

{kind=link}

RHIM investor presentation

RHI Magnesita's revenue mix is global from all around the world.

{kind=link}

RHIM investor presentation

Competitive advantage

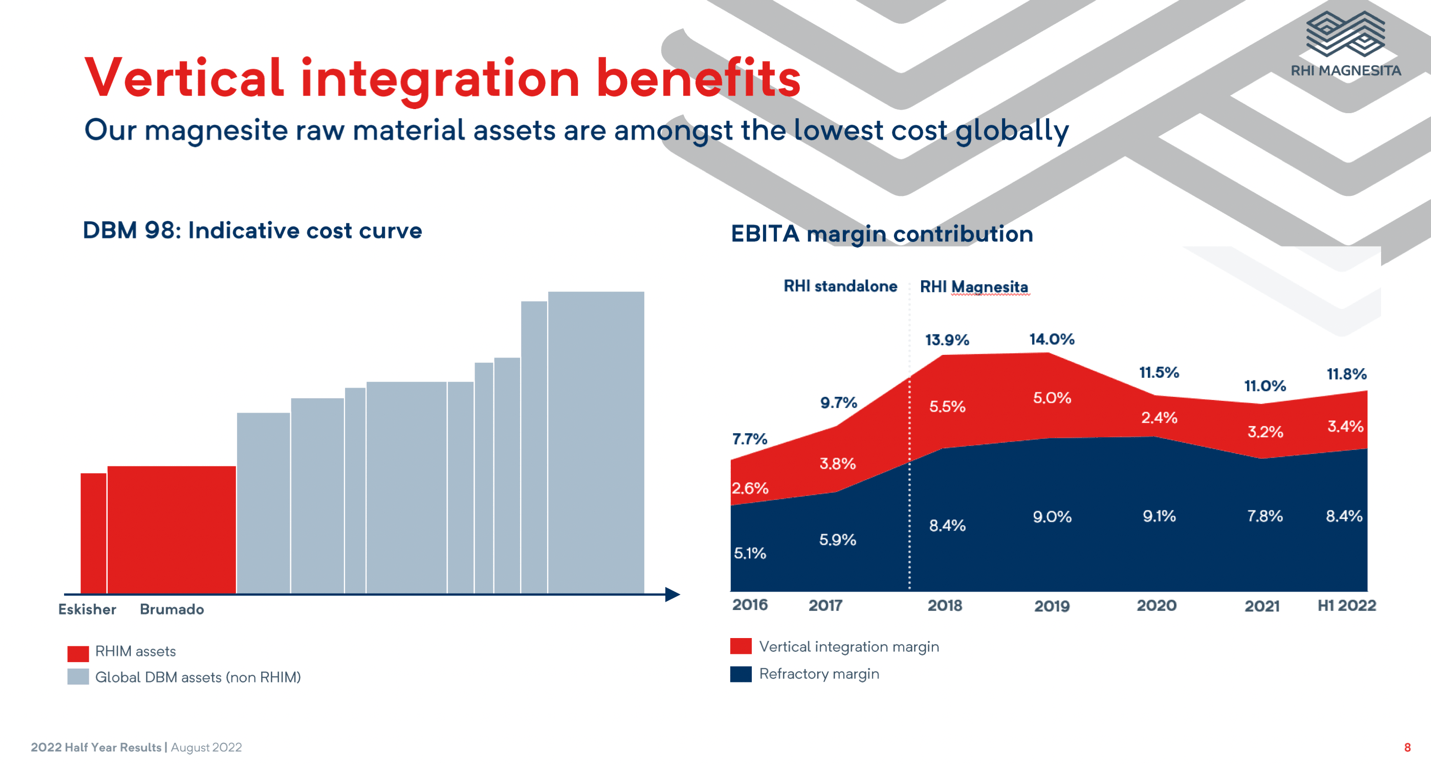

RHI Magnesita is vertically integrated, meaning they own low-cost magnesite and dolomite mines that cover approximately 50% of their raw material needs. The raw material production on top of the market size gives them a competitive advantage, especially during times when raw material prices are high, like in 2018 when raw material production contributed an additional 5.5% EBITDA margin.

{kind=link}

RHIM investor presentation

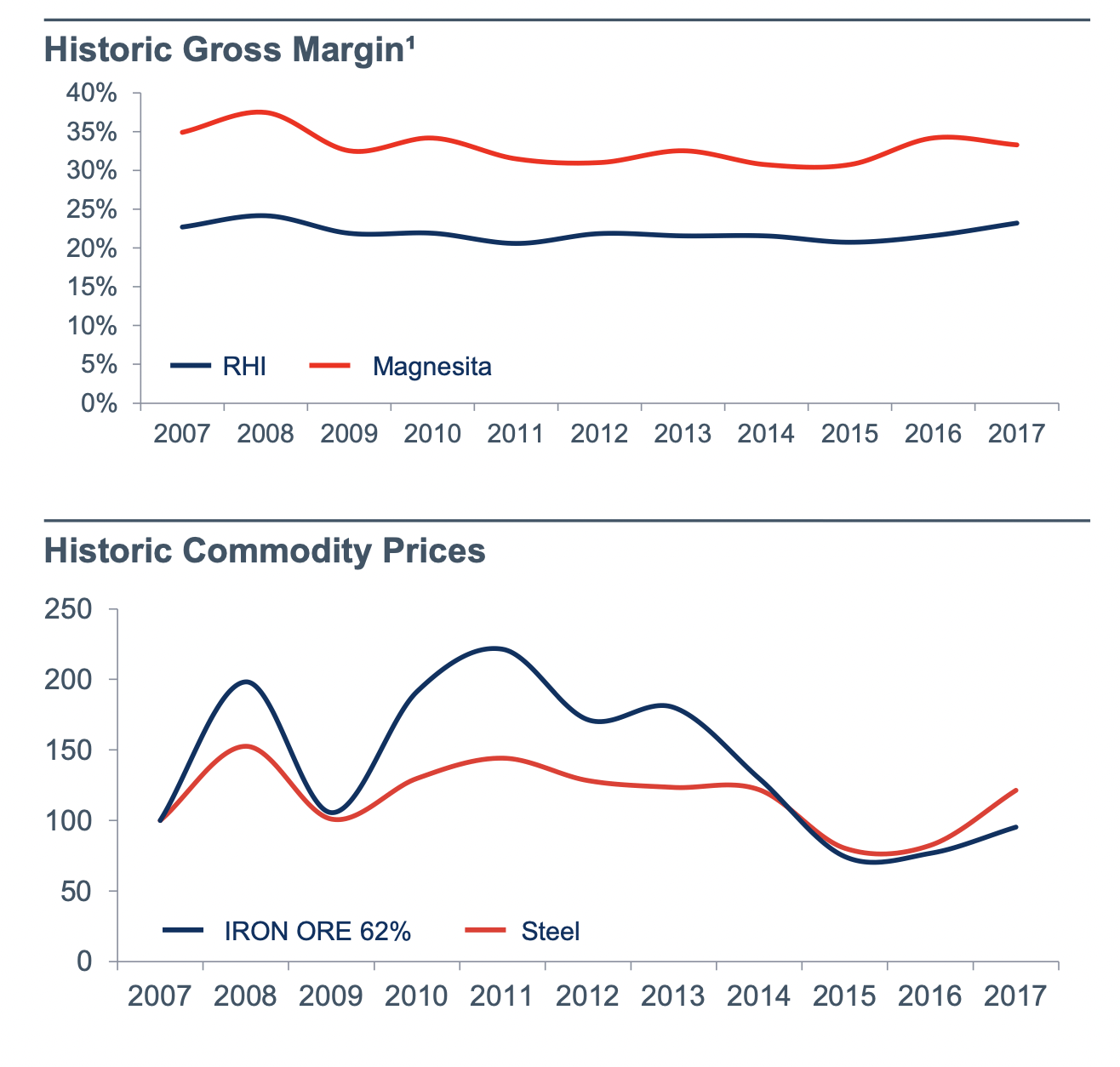

Cyclicality

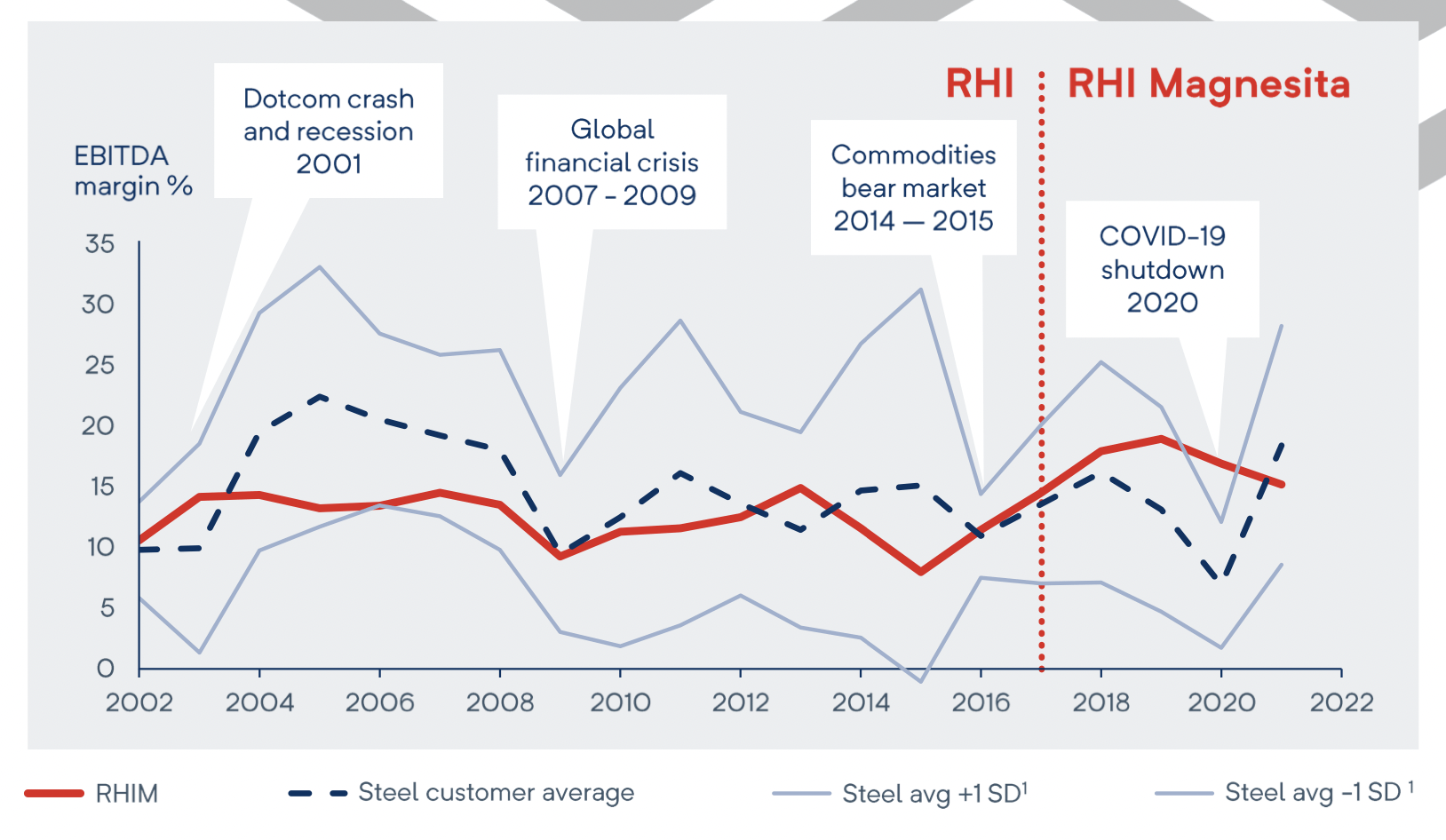

While steel manufacturers and iron ore miners are extremely cyclical businesses, refractory manufacturers' EBITDA margins are much more stable.

{kind=link}

RHIM investor presentation

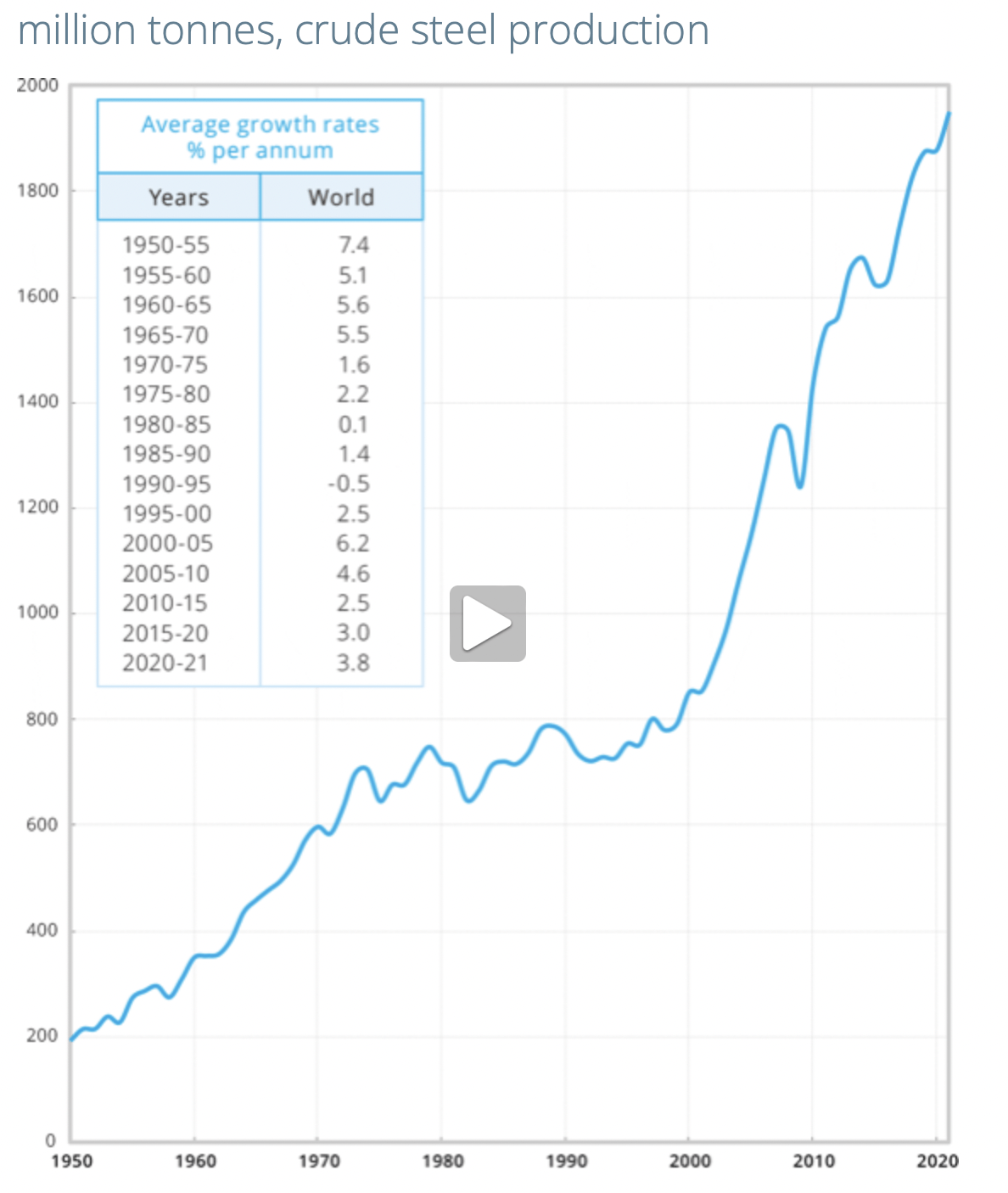

During recessions, steel production doesn’t usually fall that significantly. Only a few percent drop in demand will crash the iron ore and stainless steel prices, but the total production volumes are more stable, so the refractory product manufacturers can still make decent profits even during recessions.

{kind=link}

worldsteel.org

Chinese demand risk

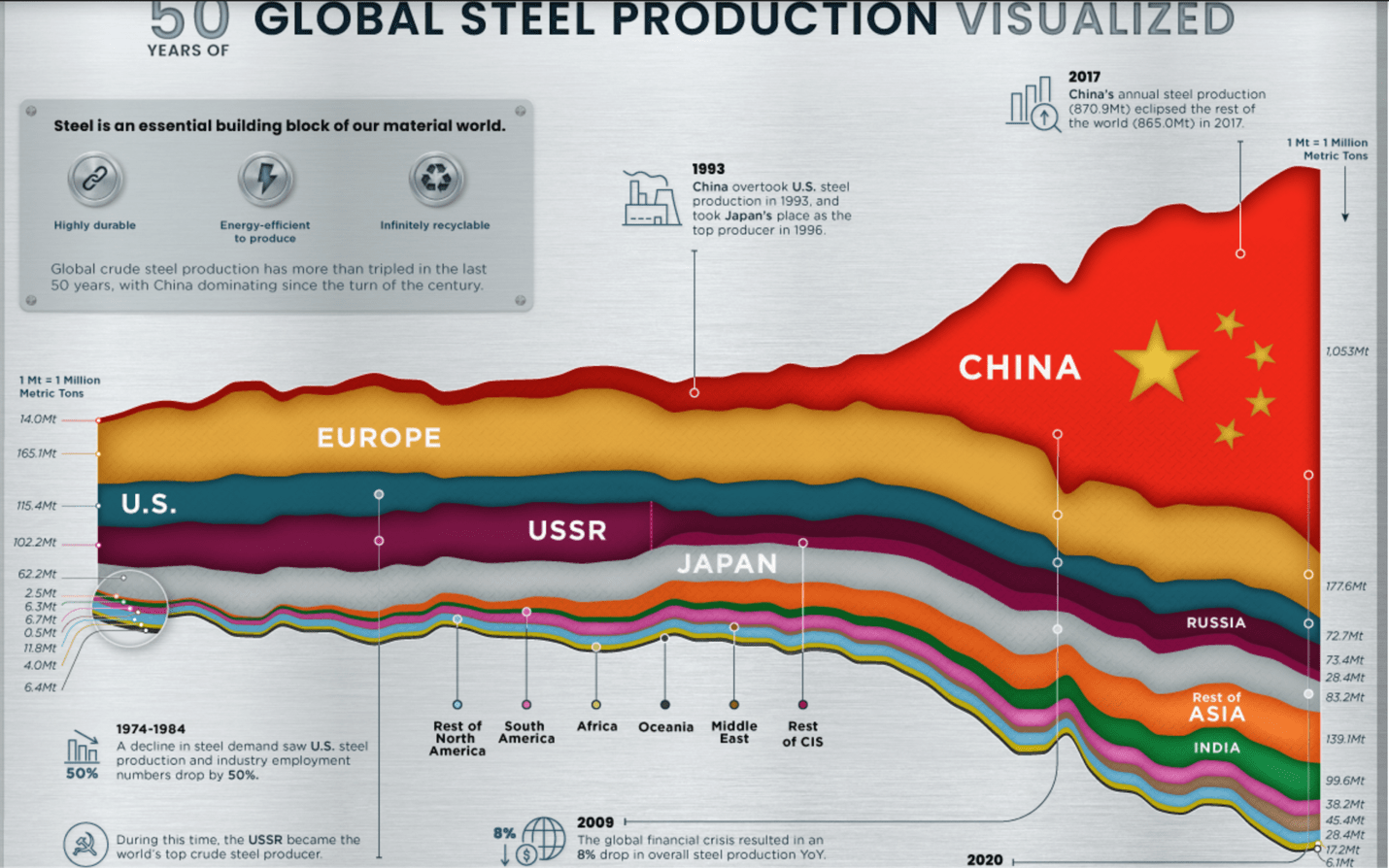

In the past 20 years, all the additional steel demand has grown from China. However, after two decades of rise in real estate prices fueled by speculation, Chinese real estate prices are currently way above their intrinsic values and it will be just a matter of time before the sector collapses (property price to income ratios) . On top of that, the Chinese communist party has invested heavily in infrastructure projects that don’t make any economic sense just to boost the GDP numbers. So if they end the crazy infrastructure investments at some point, it will lead to a massive demand gap in steel consumption.

{kind=link}

visualcapitalist.com

But then only 6% of RHI Magnesita’s sales are going to China and in the refractory industry, you want to manufacture locally, near the customers because otherwise transportation costs and tariffs make your products quickly uncompetitive. So, in case the Chinese steel demand falls, it would cause many local refractory producers’ bankruptcies, but I don’t think those Chinese producers could flood the global market and also crash the global refractory products prices.

Financials

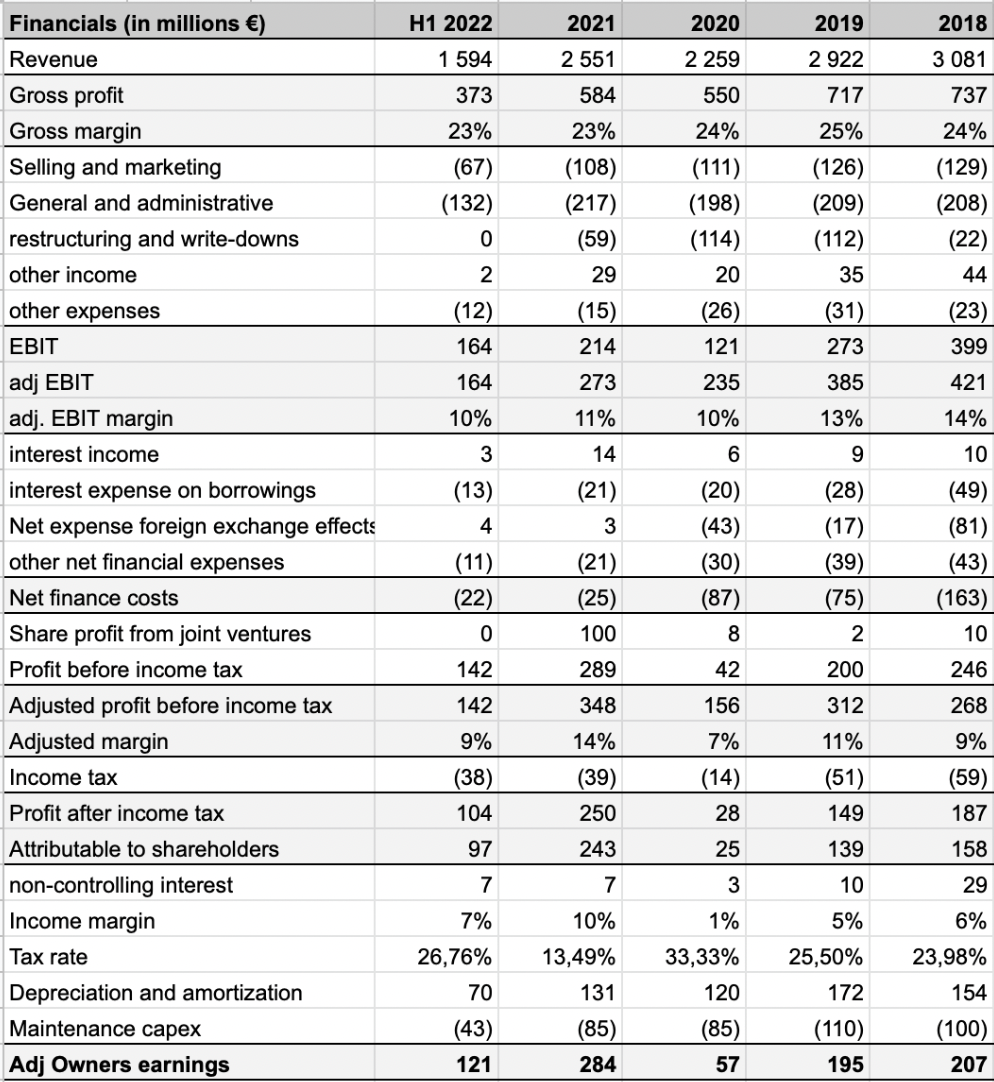

In 2018 and 2019 , they made around €3 billion in revenues. They made €158 million and €139 million net incomes for their shareholders during those years even though they had €22 million and €112 million restructuring charges and €81 million and €17 million foreign exchange losses. Without the restructuring and forex losses, they would have made something around €300 million in net income for both of those years. However, in 2020 when steel prices fell, revenues also fell about 30% and margins narrowed because of the lower sales volumes and lower commodity prices which meant that RHI Magnesita's magnesite and dolomite production didn’t give them so great cost advantage.

{kind=link}

Author's excel sourced from RHIM financial statements

Also, the management claims that their sustaining capex is around €85 million annually, while depreciation and amortization expense was between €120 million to €150 million annually. So, if that is true, actual owners’ earnings should be around €35-€65 million more than reported accounting earnings. However, I can't just take management word for it because I can’t see how they separate the growth capex from the maintenance capex.

In the first half of 2022 , they made €1.6 billion in revenues leading to a €3.2 billion annualized rate if the second half is like the first half. In the first half of 2022, steel prices were high, and the steel industry was very profitable. However, in the second half, steel prices started significantly falling as there seemed to be a slowdown in demand. So next year, revenues will likely fall again, and the profitability will take a hit.

Also, when looking at the 2022 adjusted EBIT margin, which excludes restructuring costs and write-offs, margins are still well below the 2018 and 2019 levels as in those years, they benefited from extremely high magnesite prices, but that kind of profitability is not expected going forward.

{kind=link}

RHIM investor presentation

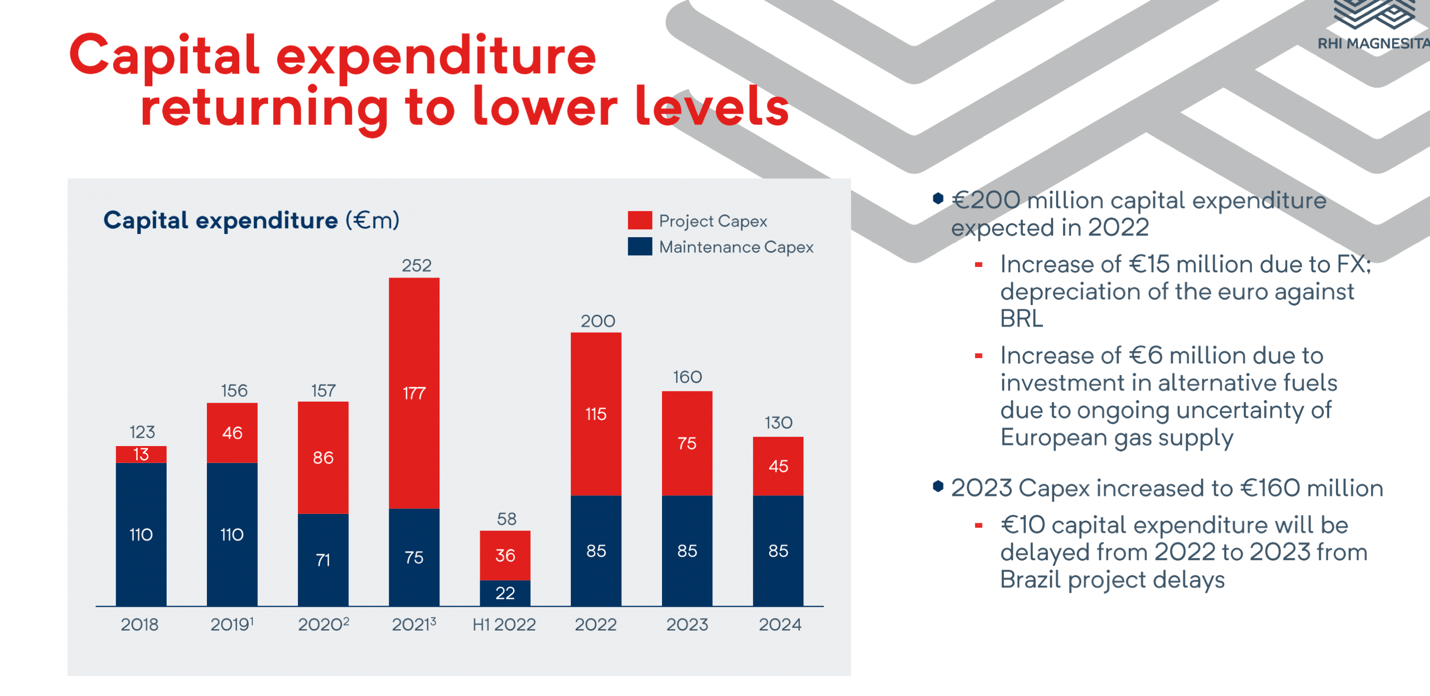

Capex peaked in 2021, so from now on, they will have more free cash flows to either pay dividends, do buybacks or make business acquisitions.

{kind=link}

RHIM investor presentation

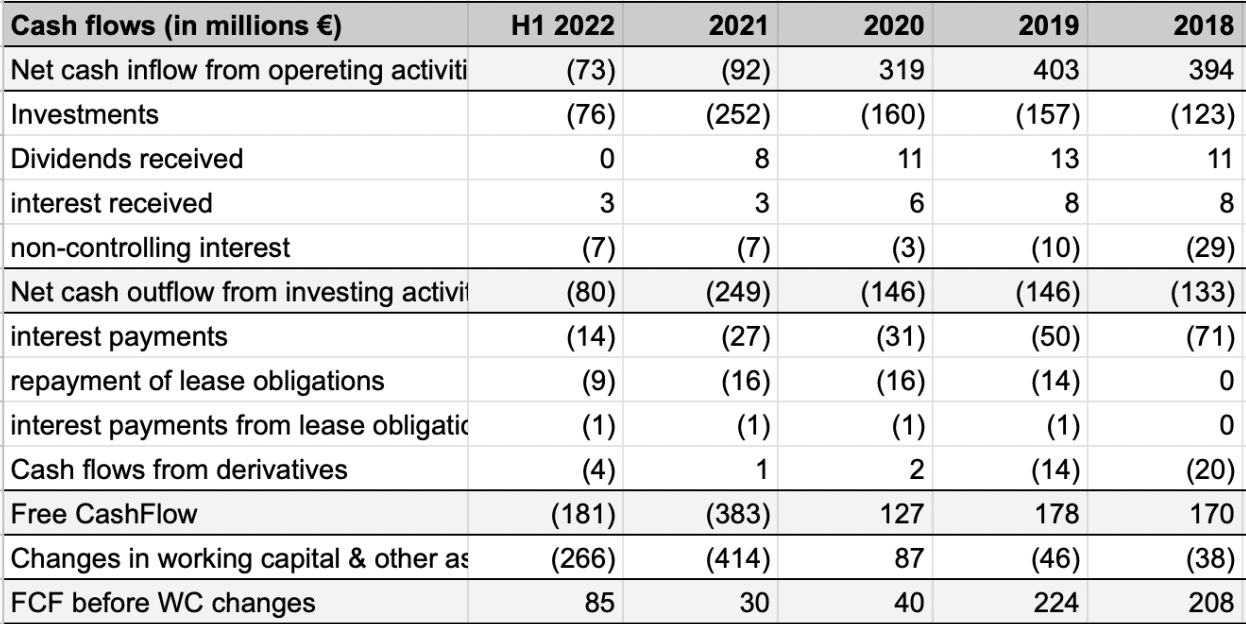

In 2021 and 2022, the cashflows were massively negative firstly because of high capex but more importantly because of working capital increase as raw material prices went up and they accumulated more inventory to combat the global supply chain challenges. If you adjust the free cash flows before working capital changes, the 2021 and 2022 free cash flows were still positive. From now on, they will start reducing inventory levels, and capex is also decreasing.

{kind=link}

Author's excel sourced from RHIM financial statements

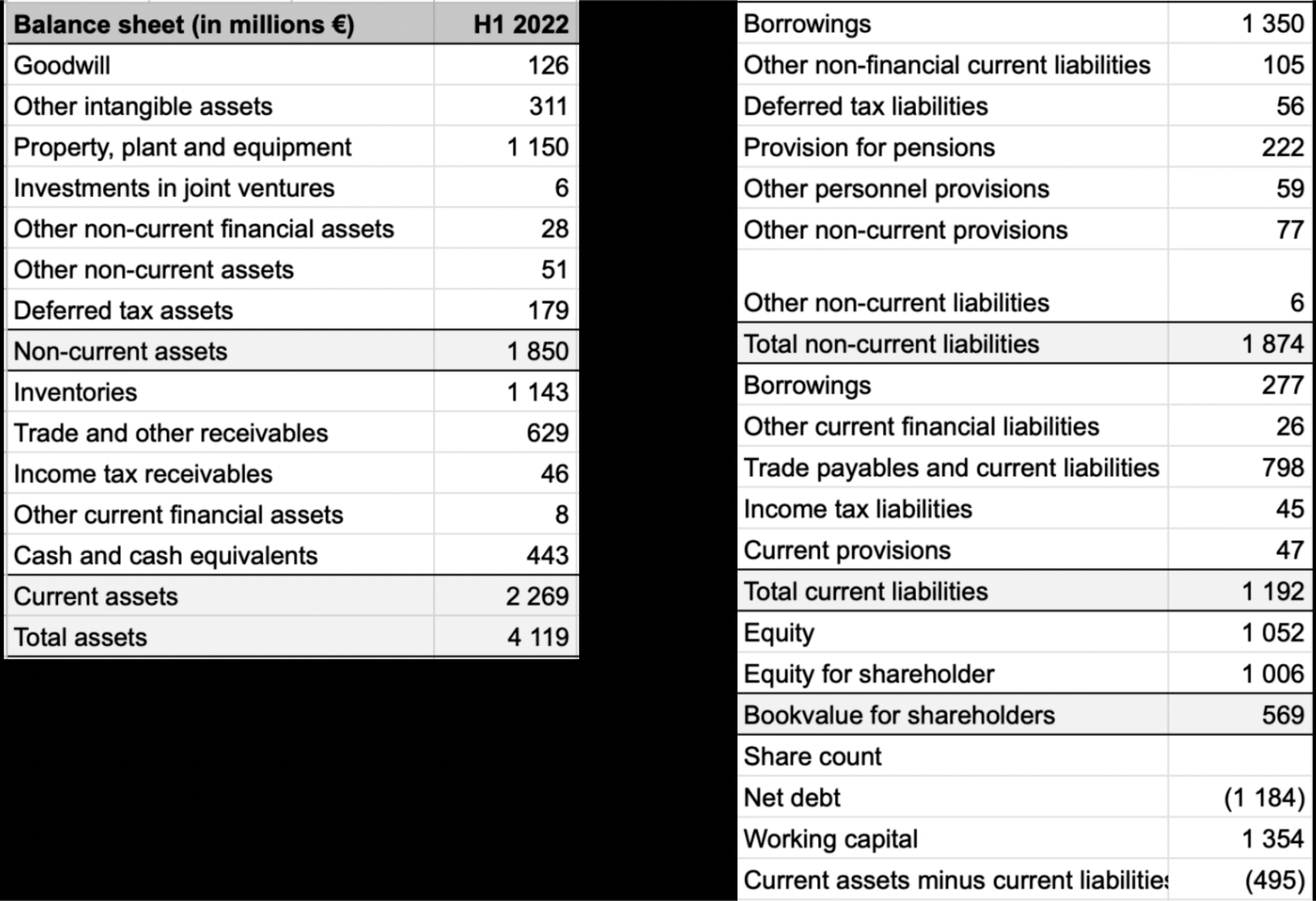

Shareholders' equity is €1 billion which isn’t far below the current market cap. However, more than €400 million of that equity is goodwill and intangible assets. Net debt is almost €1.2 billion which is quite high. However, most of it is used to finance inventory and the net debt levels went temporarily up as they increased inventory levels in recent years and the current working capital is €1.35 billion positive. If I deduct the current assets from current liabilities, long-term interest debt and pension obligations, that will lead to a negative balance of €500 million which isn’t that much anymore. So, yes, this business does have high debt levels, there is no way around that, but most of it is used to finance their inventories as it is simply a business where you need a good amount of working capital.

{kind=link}

Author's excel sourced from RHIM financial statements

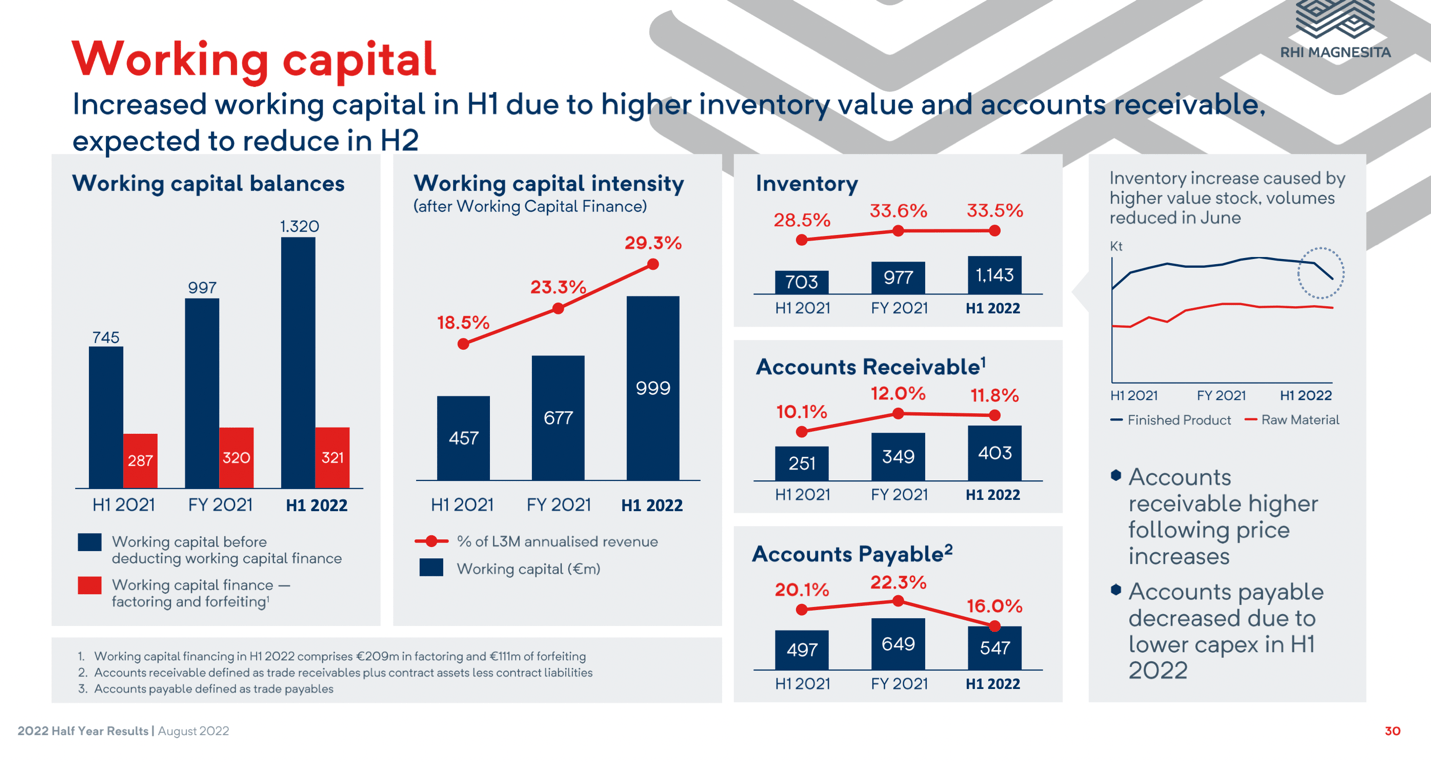

Working capital increased by almost €600 million in the past year, so after they scale down the inventory, the balance sheet will also look a bit healthier.

{kind=link}

RHIM investor presentation

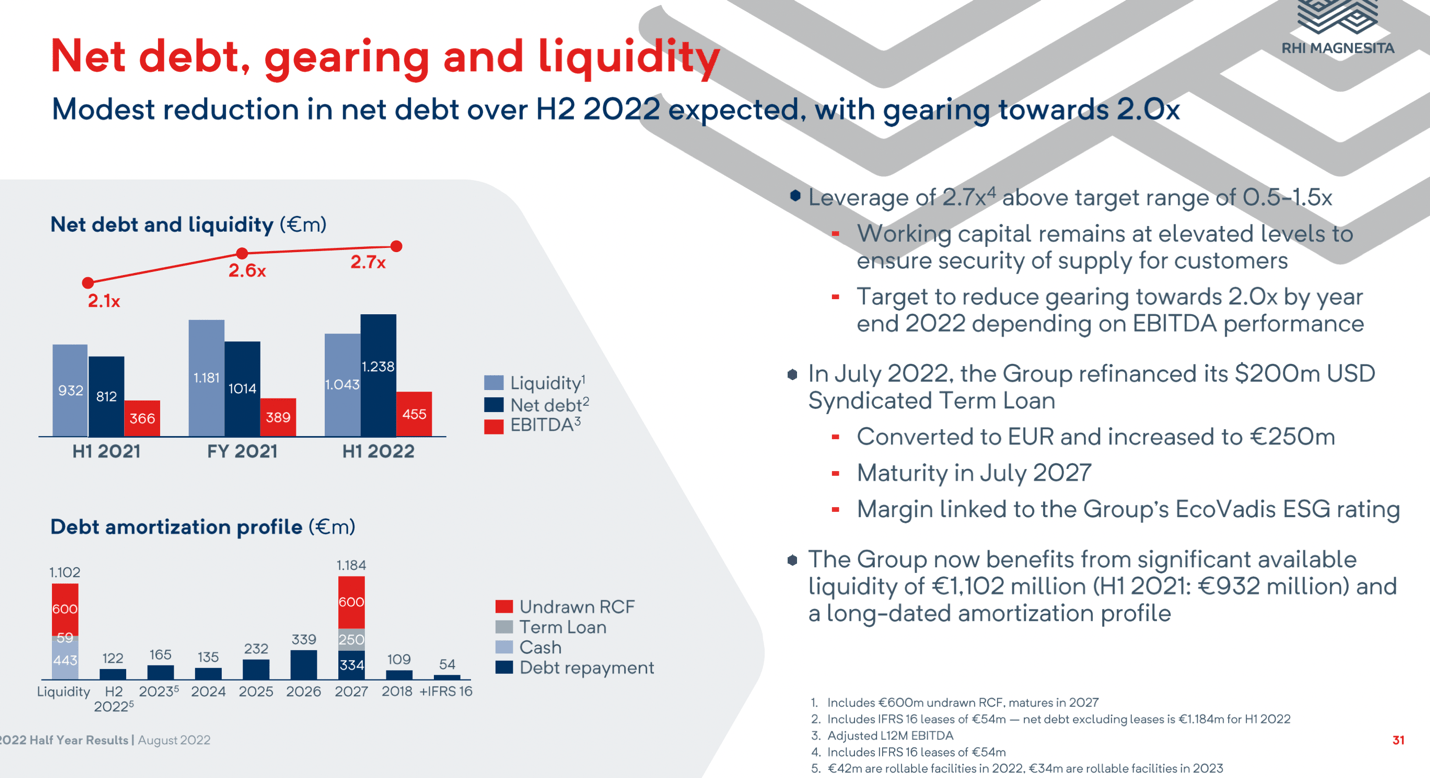

When looking at debt profile, most of the debt is fixed interest rate debt and no major maturities in the near future. Also, they got plenty of liquidity, so there are no problems on the financing side.

{kind=link}

RHIM investor presentation

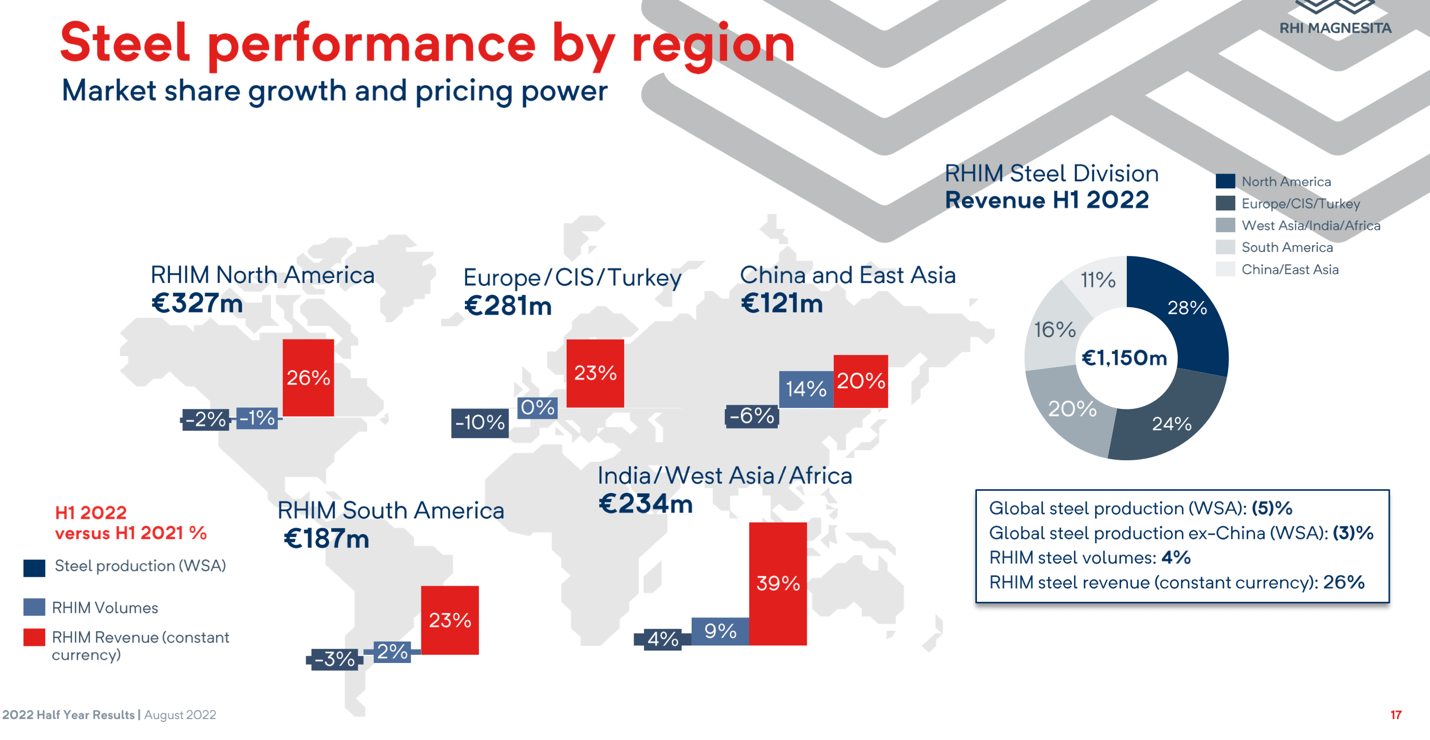

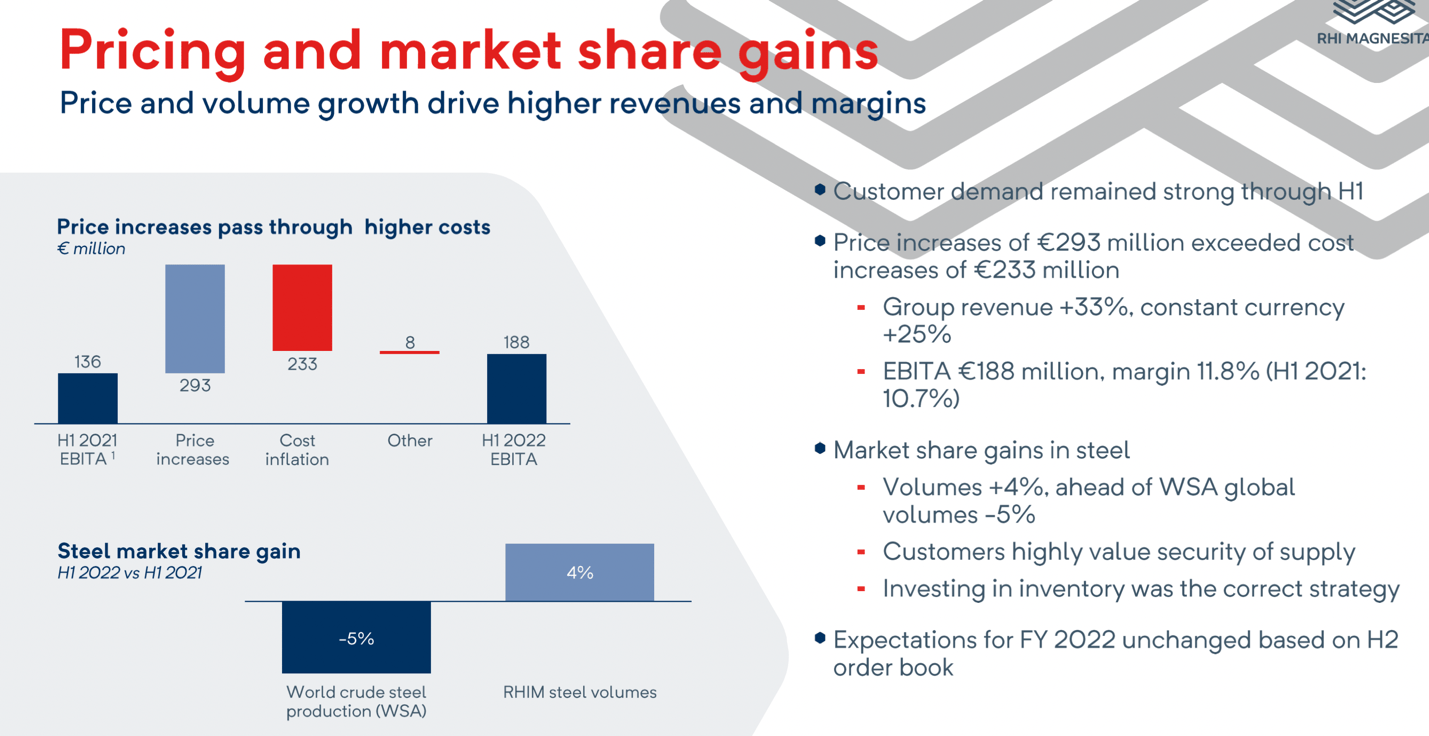

In the first half of 2022, they did more than offset the inflation with price increases, leading to a highly profitable first half. Also, while global steel production fell by 5%, RHI Magnesita increased its volume by 4% and gained additional market share. It shows that they have a competitive advantage over the small producers.

{kind=link}

RHIM investor presentation

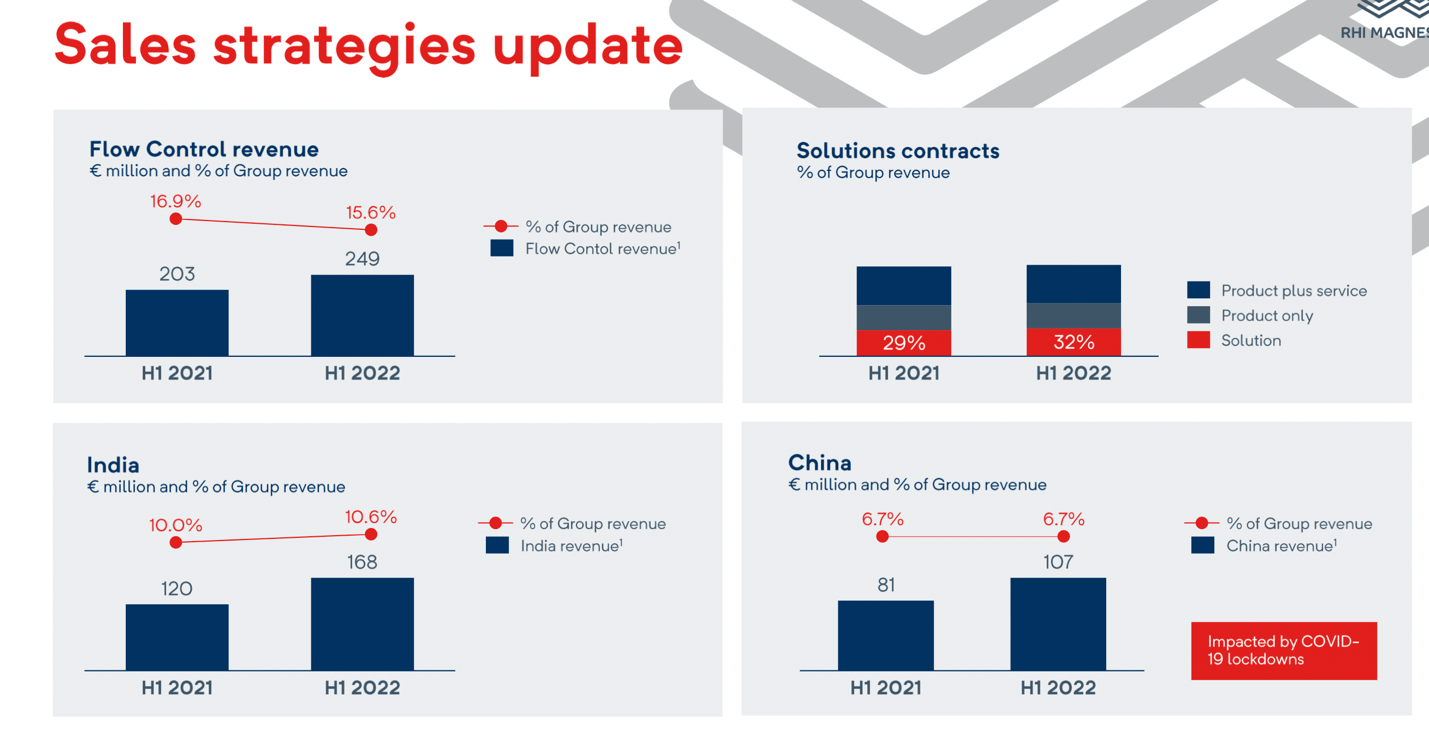

Solutions revenue

They also keep increasing the solutions revenue mix each year, already making 32% of total revenue in the first half of 2022. With solutions business, they are trying to optimize customers' refractory usage so that both parties save money. I don’t quite understand how that solutions business works and what is the competitive advantage there, but it is something that not all of their competition is offering, and they keep increasing market share, so it seems to be working.

{kind=link}

RHIM investor presentation

Indian business

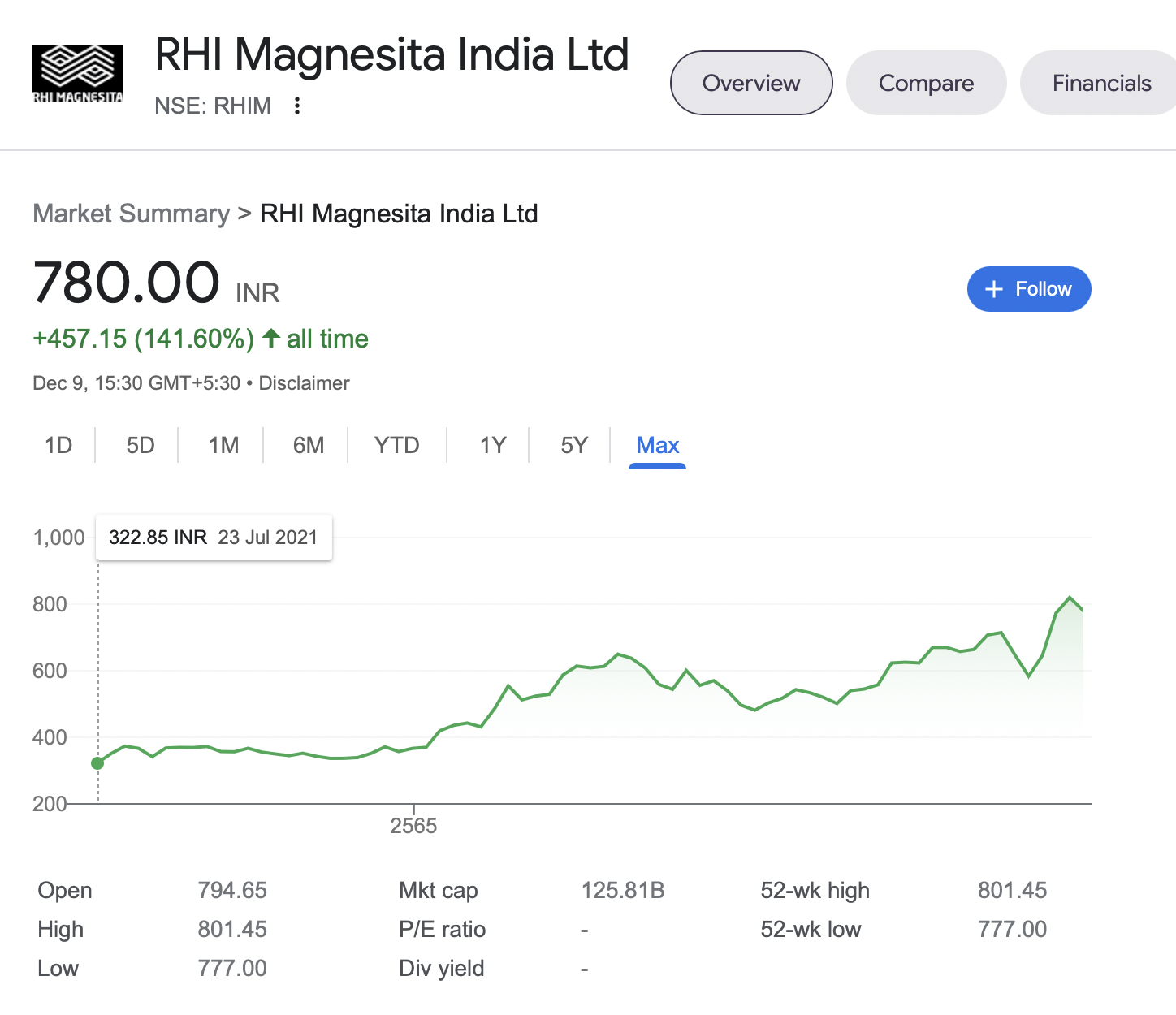

About 10% of RHI Magnesita's revenues are from India. I discovered that their Indian subsidiary, which they own 70%, is also listed on the Indian stock exchange. So, remember RHI Magnesita, the entire company listed on the London stock exchange, is valued at €1.22 billion and the Indian subsidiary, of which they own 70% and account only for 10% of the total revenues, is valued at ? 125 billion (Indian rupees) or €1.45 billion. So, RHI Magnesita's 70% stake in that €1.45 billion market cap is worth more than €1 billion. If I deduct the Indian business from RHI Magnesita's valuation, you can buy the rest 90% of the company for just €200 million or with a price to earnings ratio of one.

{kind=link}

Google Finance

Of course, I think the Indian subsidiary valuation is crazy and wrong, so I can’t use the market cap when valuing the Indian business. It just shows more how inefficient and lazy the stock market can be, which is excellent news if you are a value investor. I wonder if there would be anyone in India actually willing to pay that price for the entire Indian business if they tried selling it, or would the management be ready even to sell the Indian business as lately it’s been their focus growing in that region. If they found a buyer for that business with the current market price, that would be a quick way to double the stock valuation, but I don’t see it happening.

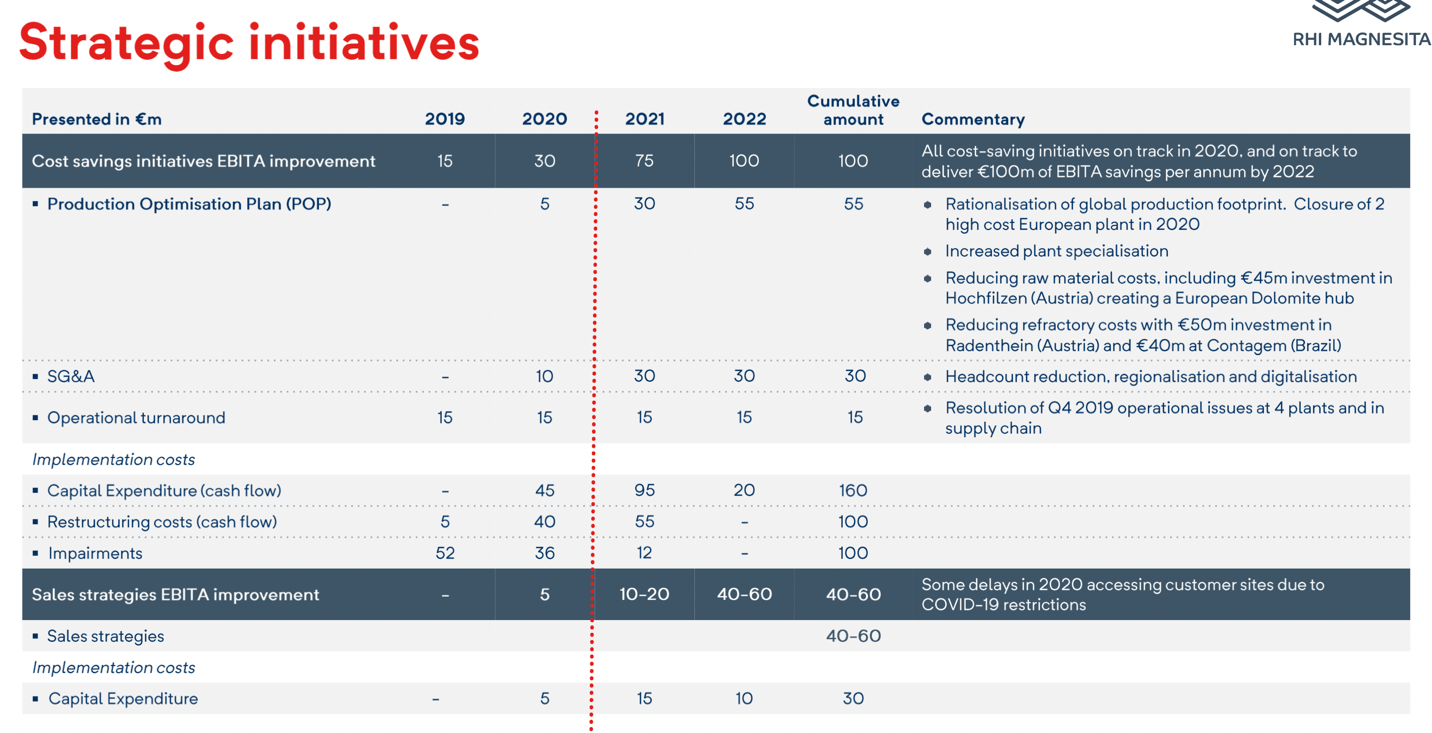

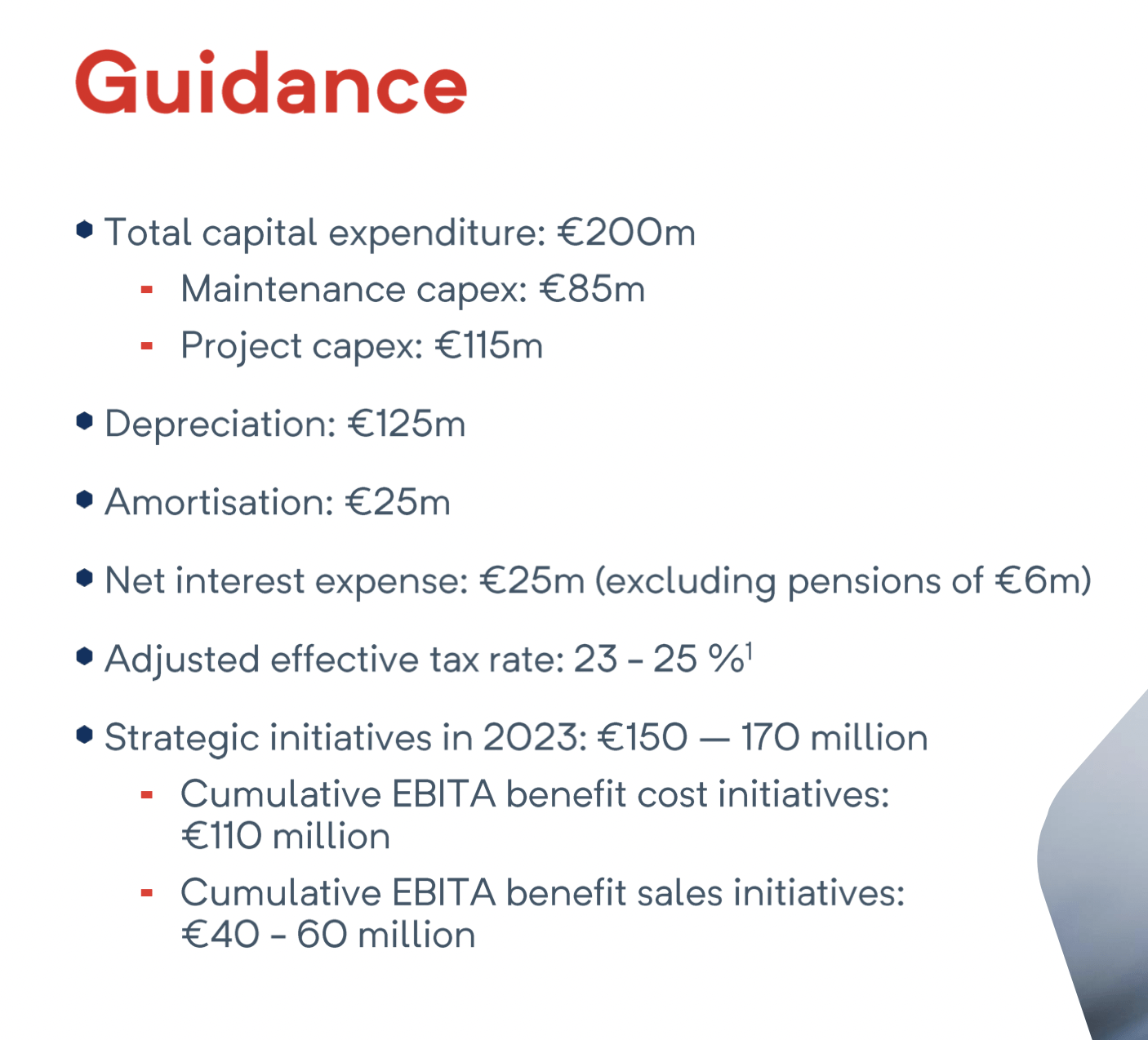

Strategic initiatives to boost profitability

In 2019 they started a strategic initiatives plan to achieve €100 million cumulative EBITA improvement by 2022 from cost savings plans and an additional €40-€60 million EBITA from the sales strategy plan.

{kind=link}

RHIM investor presentation

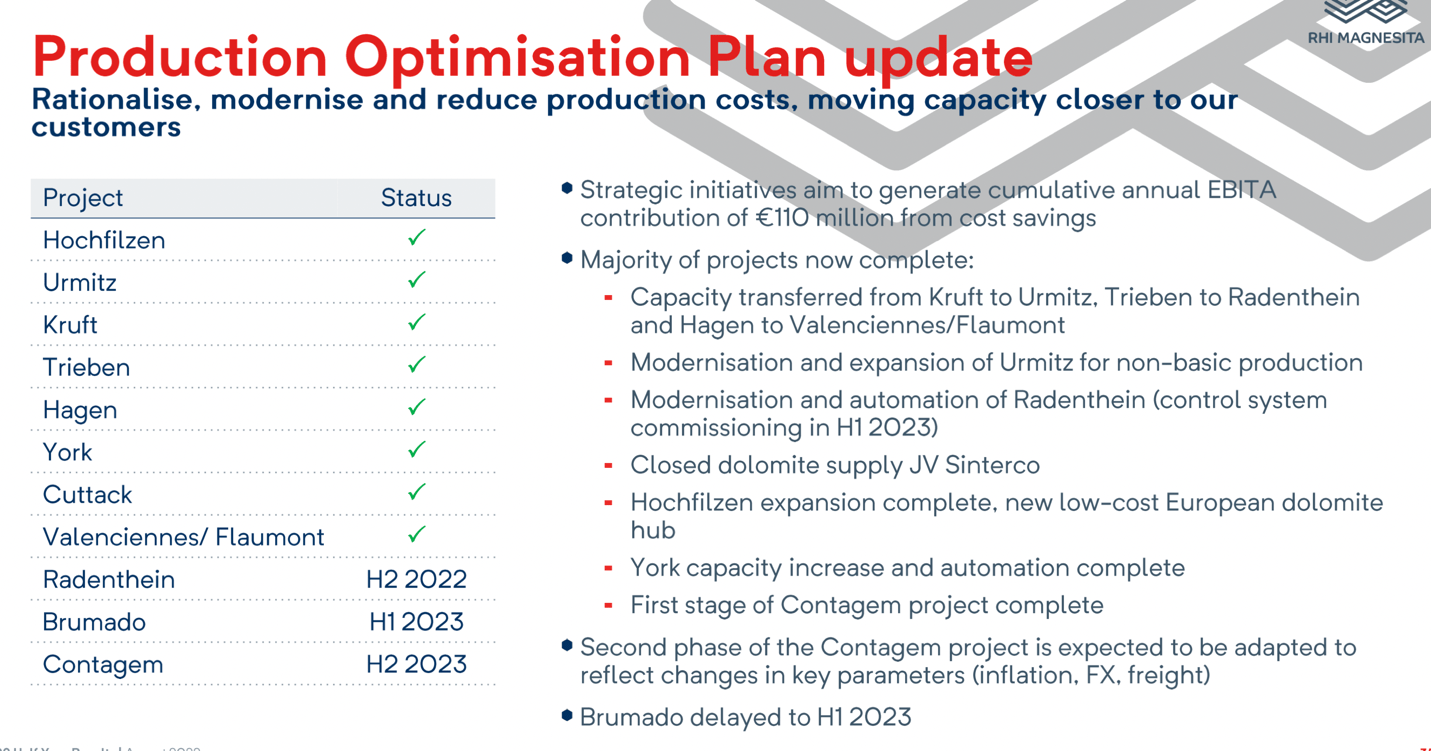

The strategic initiatives plan is almost finished, except for a few delays in Brazil that will be completed by 2023.

{kind=link}

RHIM investor presentation

So, they plan to capture €150-€170 million EBITA benefit by 2023 from this strategic initiatives plan.

{kind=link}

RHIM investor presentation

However, they should have already captured the majority of the EBITA improvement in 2022, but when I’m looking at 2022 financial statements, RHI Magnesita's underlying profitability, excluding the vertical integration margin from raw materials sites, isn’t any better than what it was in 2018 or 2019. So, as they should have already captured more than €100 million EBITA savings run rate in 2022, I'm wondering where all the benefits disappeared as margins haven’t improved. And it’s not like the overall industry margins went down because when I’m looking at the competition, they are all currently making large profits.

RHIM investor presentation

Competition

Shinagawa is Japanese refractory manufacturer primarily active in Asia. For them, FY 2022 was a very profitable year.

{kind=link}

Google Finance

{kind=link}

Google Finance

Vesuvius, the second biggest refractory producer, also made large profits so far in FY22.

{kind=link}

Google Finance

{kind=link}

Google Finance

Zaklady Magnezytowe, a tiny refractory manufacturer in Poland, is about to make record profits in FY22.

{kind=link}

Google Finance

{kind=link}

Google Finance

So, let’s see if RHI Magnesita can get some additional EBITA benefit as they finish the strategic initiatives plan by 2023, but take management's promises with a grain of salt.

Capital allocation

Regarding capital allocation, they pay around 30% of the net income in dividends. Then they use the rest for organic investments, acquisitions, or share buybacks. For the investments, they aim to achieve double-digit returns on invested capital.

Valuation

So, I think this company will make around €2.7 billion to €3 billion in revenues on average. Let’s say the average revenue is €2.8 billion. Then RHI’s historical EBITDA margins were, on average, around 12%.

RHIM investor presentation

However, in 2017 they merged with Magnesita, which was always a more profitable company and the merger increased group revenues by around 25%.

{kind=link}

RHIM investor presentation

So, let’s say that after the merge, RHI Magnesita's average EBITDA margin rose to 13%, and then as they achieved synergies and executed the strategic initiatives plan, let’s add one more percentage to long-term average EBITDA margin, making it 14%.

Depreciation and amortization expense is going to be €150 million. However, the management team says that maintenance capex will be just €85 million annually. I’m not going to blindly trust the management maintenance capex assumptions, but then I believe it is lower than their current depreciation and amortization expenses, as this is not a growth industry anymore but a stable cashflow business. So, I’ll meet somewhere in the middle and assume maintenance capex to be €120 million annually to be a bit more conservative.

The interest cost is currently €20 million annually and much of the debt is fixed. However, over time it will go up significantly, so I’ll calculate it with €40 million annual interest expense.

The average tax rate is around 25%.

Based on these assumptions, the average earnings over cycles should be around €174 million. As the market cap is €1.2 billion, RHIM is currently trading at a long-term average price to earnings ratio of 7 if these earnings assumptions are correct.

Author's excel

So, I’ll assume average earnings to be €174 million in my valuation model. They’ll pay out 30% of the earnings in dividends. The holding company is a Dutch holding entity, so it does have pretty good tax treaties with most jurisdictions. I would have to study all of the tax laws to be more precise, but I think from most jurisdictions, they should be able to distribute profits to the parent company without paying additional withholding taxes and in some jurisdictions, they may have to pay like 5 or 10% withholding tax, but overall, it is quite tax efficient corporate structure.

So, they’ll pay 30% in dividends and then invest the rest of the earnings achieving a 10% return on invested capital. It’s 50 years valuation model without any terminal multiple and the discount rate used in it is 10%. Based on this model, I’m getting a valuation of €1.6 billion compared to the current market cap of €1.2 billion. Then depending on whether your dividends are taxed or not, you have to deduct your dividend tax rate from the valuation to make the valuation model correct to you.

{kind=link}

Author's valuation model

Why is the stock trading so cheaply?

That is the biggest question I struggle to figure out. Maybe because the stock is a small cap in a relatively unknown industry, so people just haven’t figured it out. Or perhaps it is because everyone is expecting a global recession, so we know that earnings will likely fall in the next couple of years and as earnings are expected to fall, people expect the stock price also to go even lower, even though it is already cheap. Maybe also, many investors are currently more attracted to investing in iron ore miners or steel producers as many of those are currently trading at price to earnings ratios between 2 to 5, while they fail to recognize that iron ore miners and steel producers are much much more cyclical businesses than refractory producers.

I don’t know, these are the reasons I’m thinking, but maybe I’m missing something. If the Chinese construction sector collapses, perhaps the Chinese refractory producers will flood the global market so that nobody won’t make any money over the next five years until there are enough bankruptcies and the demand recovers. I don’t think the Chinese manufacturers could compete with all the extra transportation and tariff costs, but maybe I’m wrong.

Conclusion

To me, this already seems like a good investment and I think the market only sees the likely upcoming recession and a couple of years lower profits, so why bother investing now as there is no catalyst to immediately shoot the stock price up, right? But maybe it’s the key to buy it before no one sees the catalyst to push the stock price up because when people know the catalyst, the stock will already be priced higher.

If you are happy to own value for the long term, this will likely lead to double-digit returns over time. Will there be an even better entry point for the stock in the future? Who knows. It is already offering value and if the price keeps falling, it's an opportunity to buy more.

For further details see:

RHI Magnesita: Recession Fears Hide The Underlying Value