RBBN - Ribbon Communications: Likely No Value For Long-Term Investors

2023-05-23 15:02:24 ET

Summary

- A friend of mine wanted me to look into the company that he was interested in.

- The company has seen erratic revenue growth and is consistently unprofitable.

- There is very little to like in terms of its financials.

- Fundamentally, this is a stock to avoid until it can be consistently profitable.

Investment Thesis

With choppy, unprofitable years in the past, a friend of mine wanted me to look into Ribbon Communications ( RBBN ) to see if there is potential for it to outperform in the future as he feels very optimistic about the company. Unfortunately for him, I look for companies that have already proved themselves to be good money makers, rewarding their shareholders, having a strong competitive advantage, and a decent moat. RBBN misses all of these points, and I don't see it changing anytime soon unless the company figures out a way to improve margins significantly. Until then, I will give the company a hold rating.

I will touch briefly on what the company is doing right now but focus mostly on the company’s financial history and financial health, coupled with the metrics that I think are the most important to look at when considering investing in a company.

Briefly on the Company and Latest Quarter Results

Ribbon Communications makes software, IP, and optical networking solutions for many service providers around the world. It helps modernize its clients' networks by offering cloud-to-edge communications solutions like optical IP systems for 5G connectivity.

Quarterly Report - Mixed

I do not like companies using non-GAAP figures on their quarterly results, especially when the companies highlight these instead of GAAP. Q1 '23 earnings were not very good even on non-GAAP. The company reported -$0.02 of non-GAAP EPS, which still beat estimates by a penny. Revenue grew 7.5% y-o-y, which missed estimates by around $1.3m. Furthermore, the company's margins did not improve at all and were around 200bps (basis points) worse compared to the previous year.

The management is still maintaining a positive outlook and guidance for 2023.

I modeled the financials of the company and there is nothing impressive about how the company has performed since 2018, and I do not know why my friend is excited about the company in its current state, however, I am keeping an open mind.

Outlook

The management is guiding a double-digit growth for itself in the future, which usually means low double-digit whenever the management is using this sort of terminology. If it was over 20%, companies usually say the number.

The company has a lot of potential to keep growing and scaling its operations in India and the management seems excited about the direction that this is going. India is a huge region, and their services will be needed there for sure. Airtel is one of their biggest clients in the region and sales grew around 18% there. In my opinion, that is not a very strong growth y-o-y, and I would like to see somewhere closer to 30%-40%.

Optical IP sales in the US grew by around 78% y-o-y, however, it is not a significant figure in terms of total revenues. It is promising though.

The company is in a very intensive industry where margins are very tight and RBBN, by the looks of it, has to operate unprofitably until efficiencies start to kick in. R&D Sales and Marketing eat up all of the gross revenues and then some more. It has improved y-o-y; however, it is still delivering negative returns to shareholders.

I think the company should focus more on its Cloud and Edge segment which has much healthier margins than its Optical Networks segment or at least find a way to improve its efficiency.

Financials

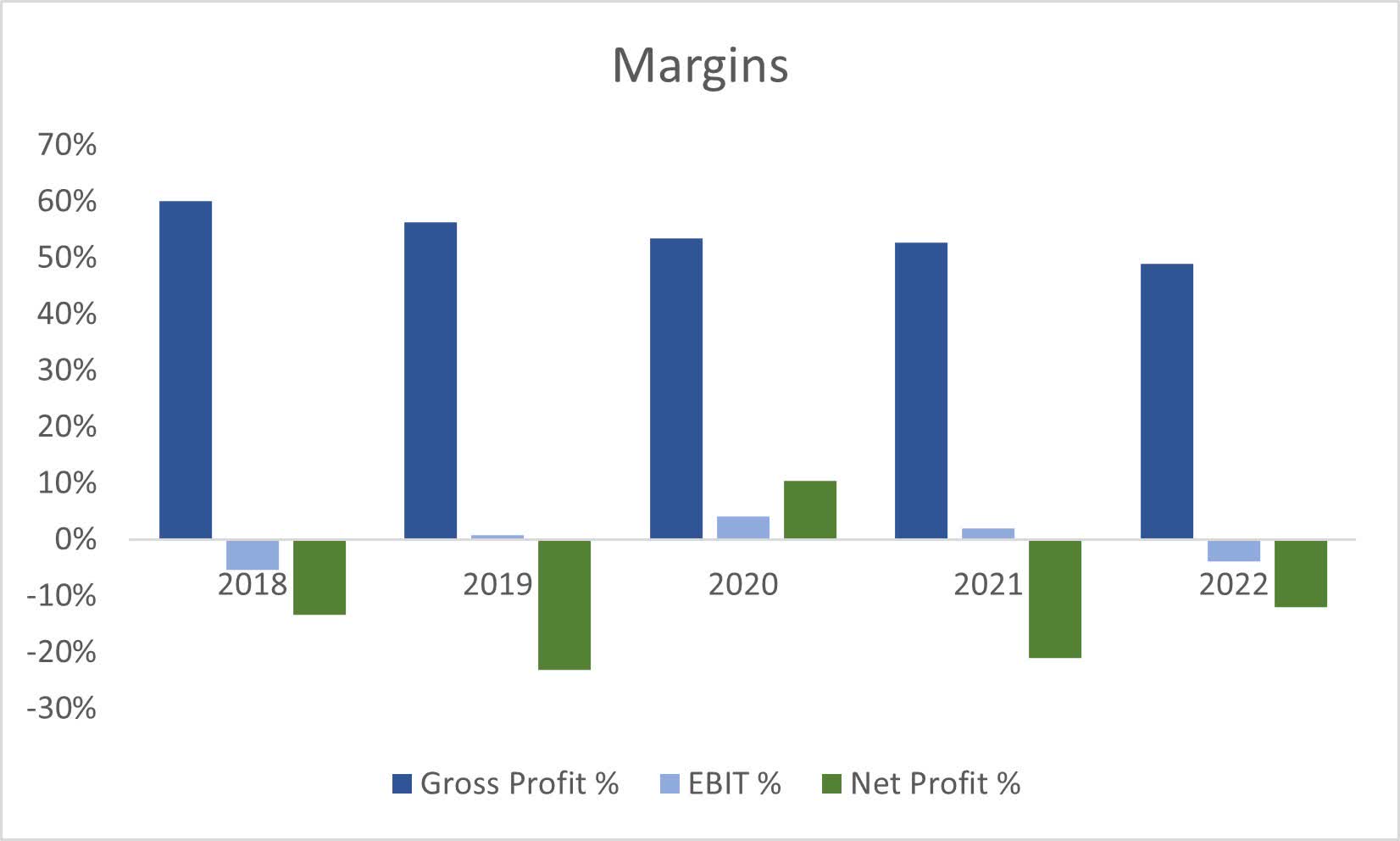

Speaking of margins, when I modeled the company's financials, I saw a company that has not been improving in at least the last 5 years.

Gross margins seem to be heading down since 2018, while EBIT and net margins have seen only one positive year out of the last 5, which is not a company I like to invest in.

{kind=link}

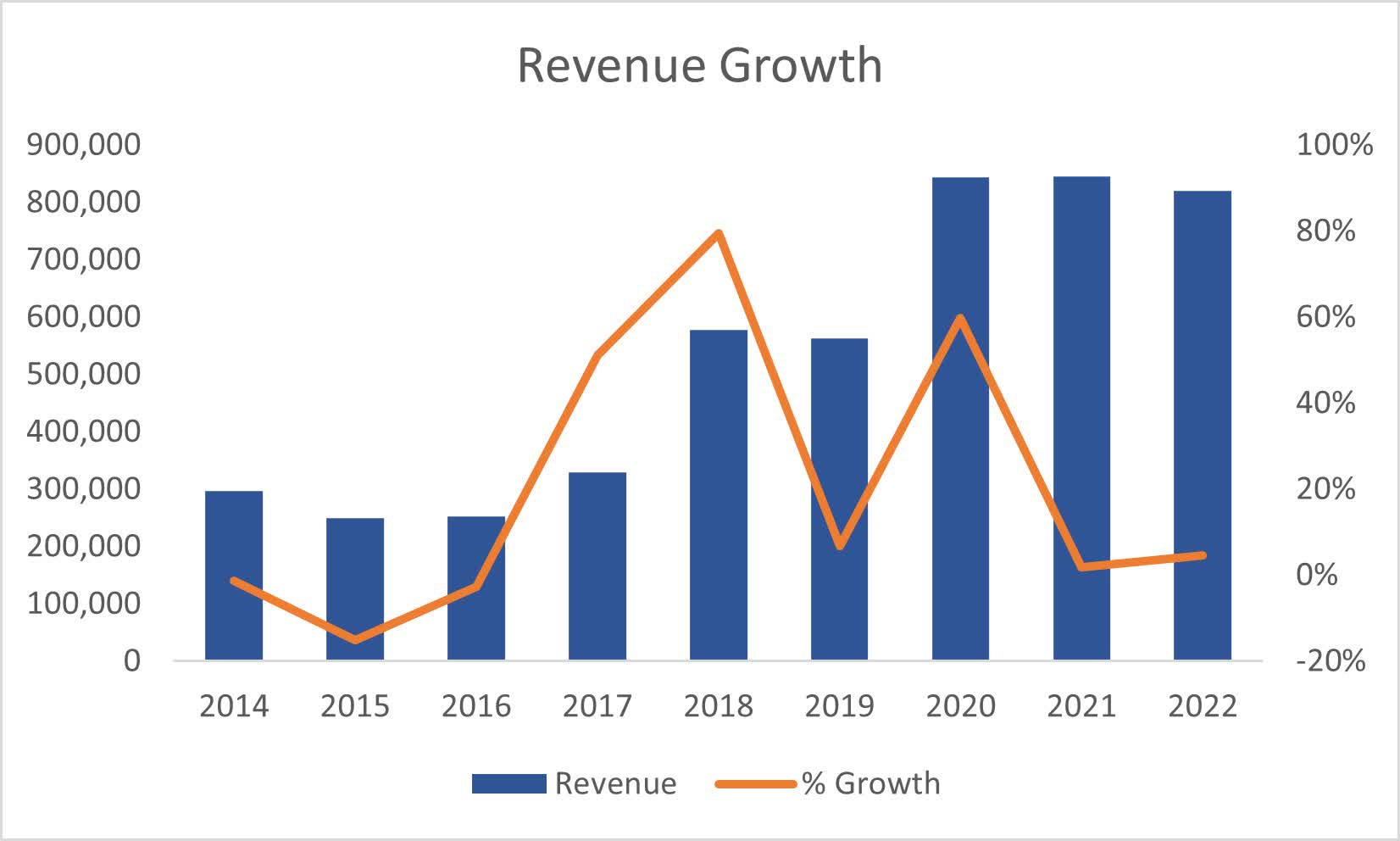

Then I thought maybe the company is still in the early stages of growth which would explain why it is losing money left and right. The company has been around since ’97 according to Seeking Alpha, so it’s not a new company any longer. Looking at their revenue growth, it shows some massive spikes in y-o-y growth followed by subpar growth. Looks like the company is very inconsistent.

{kind=link}

Turning over to the balance sheet, the company had $46m in cash and $225m in long-term debt which improved by around $80m since the end of FY22, which is a good sign. The company is somewhat prioritizing getting the leverage down. How harmful is this long-term debt? Well, interest expense is around $6.4m which increased from $4m the year before in the same quarter, even with less debt on the books. The company already experienced an operating loss, which means the company is not able to cover its interest expenses. That is a big red flag for me. This leaves the company in a tough situation. It will have to either come up with a good plan to reduce costs, so EBIT is at least covering the interest expense but preferably covers more than that. The company would have to issue more shares to raise capital, which is not going to benefit any current shareholders. For now, the cash on hand does cover the interest expense but not for long.

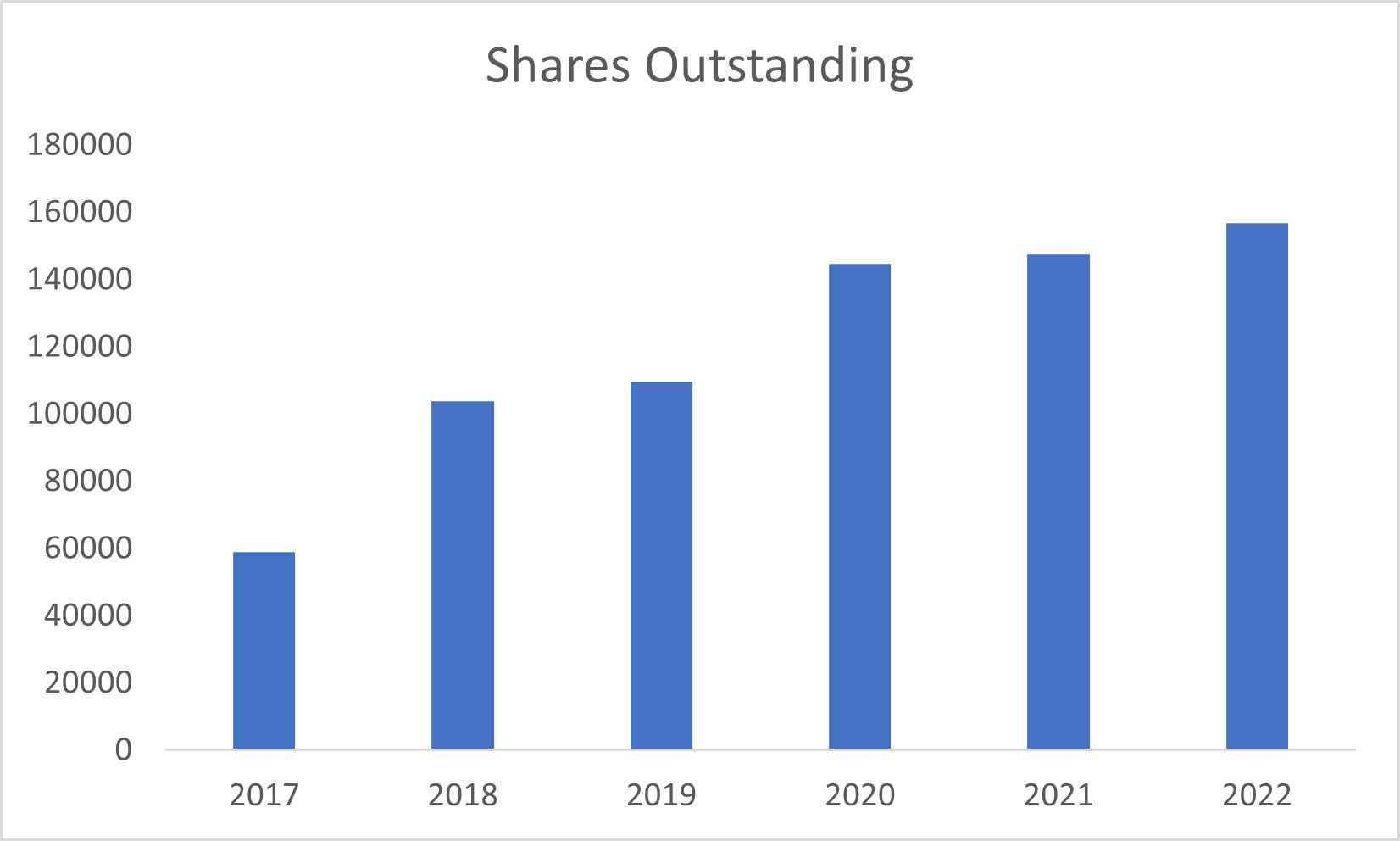

We can see that the company went the share dilution way to raise capital. The company’s share count has increased by 166% in the last 6 years.

{kind=link}

No value has been generated for current shareholders during these years. The company might continue to dilute further if the management is not able to operate it more efficiently.

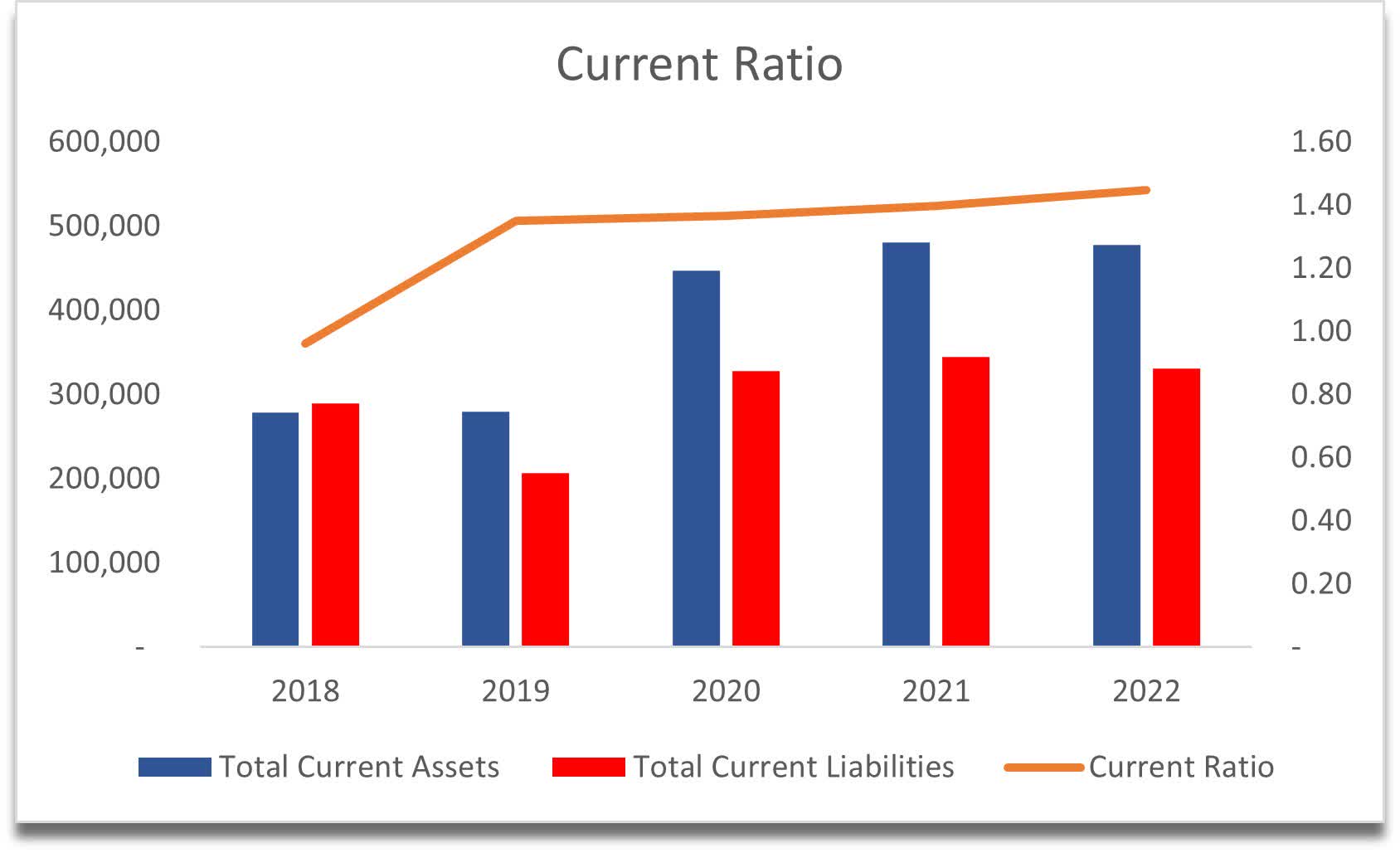

The company's current ratio is acceptable; however, I would like to see it be around 2.0. At the moment the company is not facing urgent liquidity issues.

{kind=link}

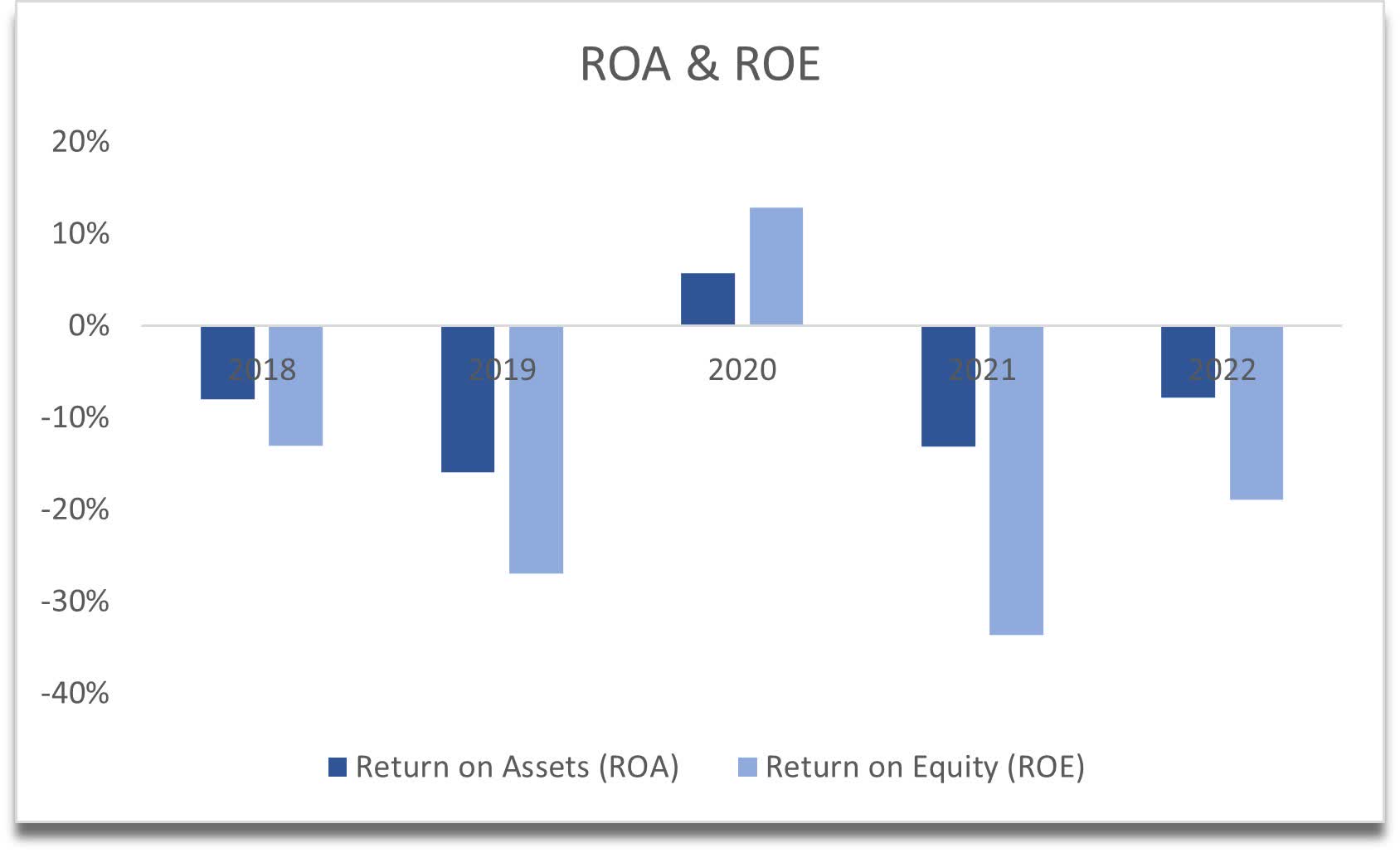

The next metric is where the company has lost me completely. ROA and ROE are not good at all. The company is not being very efficient with its assets and not creating value for its shareholders in my view.

{kind=link}

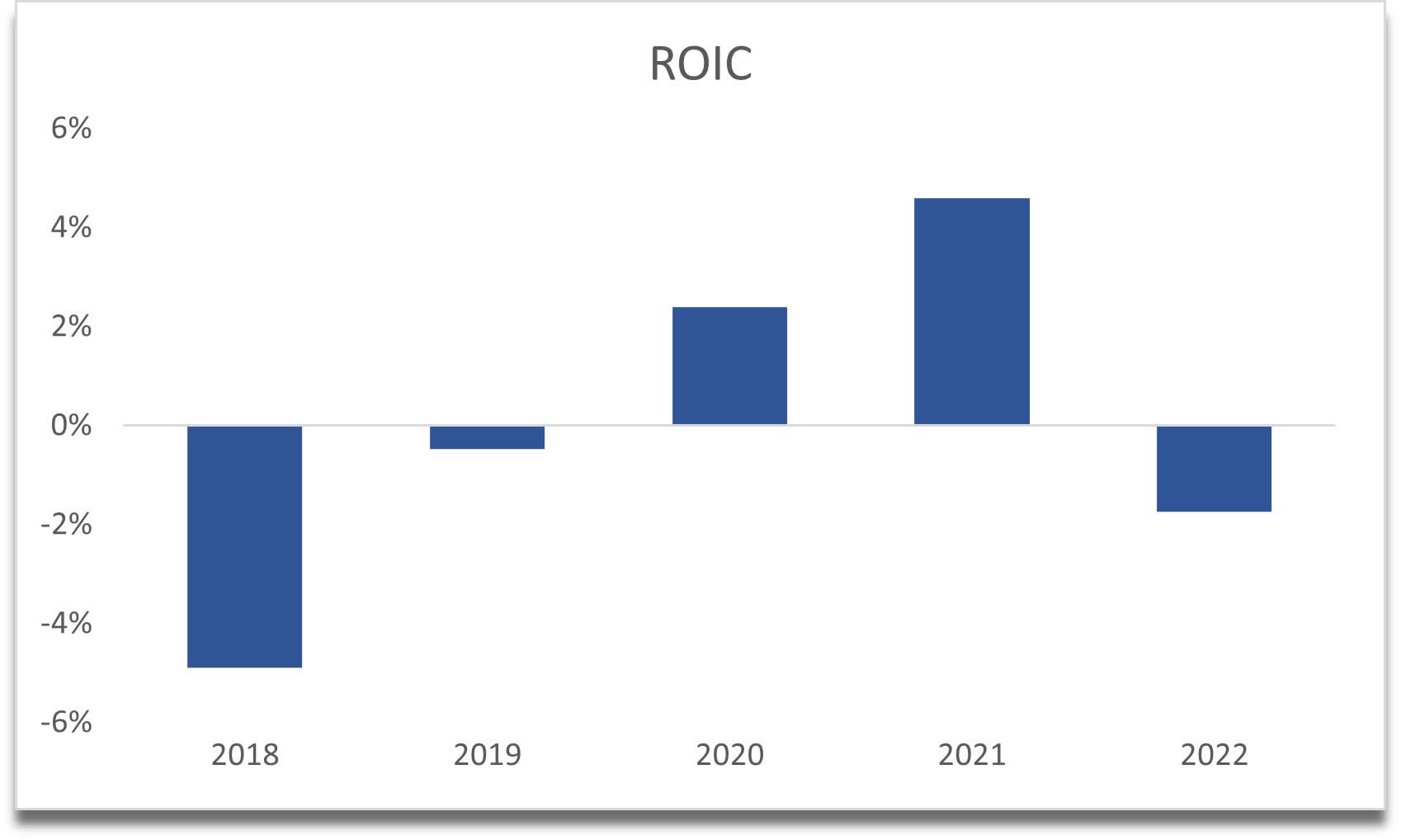

The same can be said about the return on invested capital. It is not good, which indicates the company does not have a competitive advantage in the industry and no competitive moat. Even in the years it was positive it was still not great.

{kind=link}

Overall, looking at the company in this kind of detail reveals a company that is struggling to create value. Constant dilution is not good for anyone except for getting capital to pay off interest expenses and keep afloat a little longer. If the company doesn't manage to become consistently profitable, I believe the company's share price will continue to deteriorate, and will be a long time before it becomes a good investment in the long run.

Closing Comments

I usually give a valuation in all of my articles, however this time, it would be a big speculation on the company’s prospects. It is hard to model margin improvements when the management hasn’t given any guidance on when they would achieve consistent profitability by cutting costs and further digitization efforts to streamline its operations. Sometimes I do find a company that had a turnaround just by looking at the above metrics like ROIC, ROA, and ROE, however, I do not see a positive turnaround story for the company here. The fundamentals are not great right now and I will stay clear.

I think one can still make money on this company just because the company is down bad just from the recent highs in February of '23. In the last 10 years, the company is down 75%. It may continue on this path of plummeting, but we may also see a few bounces, however, fundamentally in terms of value, the company is not creating any in my view and has not created any for its shareholders in a long while, especially the long-term investors. I would not be happy with how the company has been performing and I will tell my friend my thoughts and he can decide what he would like to do.

For further details see:

Ribbon Communications: Likely No Value For Long-Term Investors