RELL - Richardson Electronics: Betting On Green Energy

2024-01-14 20:28:03 ET

Summary

- Richardson Electronics missed EPS and revenue expectations in Q2 2024, with a significant decline in sales.

- The company remains confident in its pipeline of projects and global opportunities in the green energy solutions business.

- The demand for green energy solutions presents a significant market potential for Richardson Electronics, but actual demand may vary.

Richardson Electronics, Ltd. ( RELL ) is a small-cap stock that has been around for 75 years. Although most of their solutions were niche and limited in their scalability, the company has recently made significant strides in its Green Energy Solutions Business ((GES)). The GES segment is expected to produce 50% of the company’s total revenue in the near future. The company has at least two concrete solutions within its GES segment that could help double the company’s revenue to $500 million by 2027 and make it highly profitable: a plug-and-play replacement for wind turbine batteries and high-quality synthetic diamonds. Furthermore, the company has a strong revenue source within the cyclical semiconductor wafer fabrication industry due to its partnership with LAM Research.

Since my first article , the stock has lost significant value, and financials are likely to see a YoY decline in FY2024. Although the stock may appear to be a risky bet, it is important to note that the company’s solutions are project-based, depending on time and resources to complete these, which makes it difficult to get a clear picture of how the business is doing on a quarterly basis. The recent Q2 2024 earnings report and lowering of FY2024 revenue may have caused negative market sentiment, but the earnings call paints a bullish picture of progress within the GES segment, potential recovery within PMT, and long-term loss-making Healthcare. Based on this information, I maintain a hold rating for the stock, although there are reasons to be bullish about the company’s future prospects.

{kind=link}

Company updates

Last year, Richardson Electronics benefited from several large projects, including electric locomotive development and major owner-operators of GE wind turbines such as Nextera, Enel, and Invenergy. The FH 2024 paints a financially weak picture, impacted by economic conditions, declining sales to semiconductor wafer fab customers, and delays in the company's GES business. In contrast, the company emphasizes that projects are lengthy and disruptive and remains confident in its existing project pipeline and new global opportunities within its GES business, which it believes will drive substantial long-term value. While the company hasn't given concrete numbers on new orders, it expects some of these larger customers to place new orders this year. The company expects to see sequential revenue growth in Q3 and Q4 within its GES business, driven by new products, customers, and technology partners, all supported by the forecast and backlog from these project-based customers. In Q2 2024, the company added major new customers such as BP Energy, EDF Energy, and EDP Renewables. Furthermore, 90% of its ULTRA3000 sales in Q2 were with new wind customers.

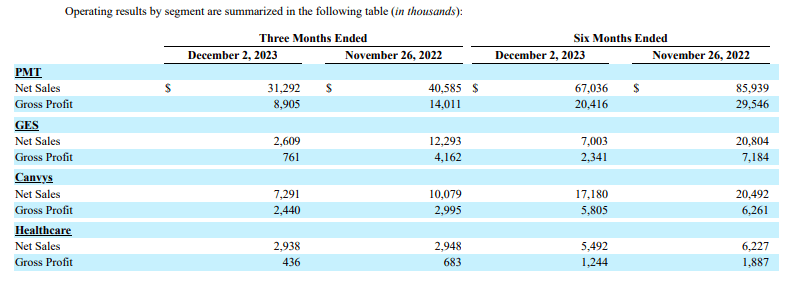

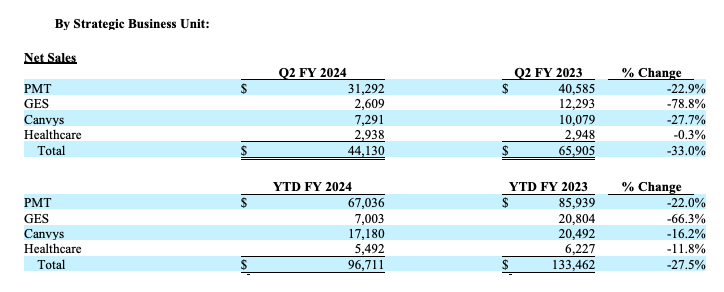

Revenue and gross profit by segment Q2 2024 versus Q2 2023 (SEC)

{kind=link}

Research has also shown a growing demand for net-zero offerings, which could generate annual sales of $9 to $12 trillion by 2030 across various sectors, including transport, power, and consumer goods. This is in line with the company's expectation of growing its pipeline of green energy projects. The company expects to receive significant bookings in Q3 and Q4 of FY 2024. GES and PMT backlogs remain strong at over $100 million. The company's recent partnership with North America's Integrated Power Services ((IPS)) underscores its progress and could help increase the sales and installation rate. Furthermore, PMT has been the company's largest revenue driver through large customers such as LAM Research. It expects the cyclical semiconductor wafer fabrication industry to recover in the latter half of the year. Furthermore, within the electric locomotive side, there is a $100 million opportunity. The company has orders for over 25 trains. The management forecasts an annual growth of 15% to 20% to hit $500 million in revenue by 2027.

The ULTRA3000 and ULTRAPEM 3000

These products are designed for the ultracapacitor battery replacement market within wind turbine generators (WTG). The ULTRA3000 is a plug-and-play replacement for batteries within GE wind turbine pitch systems, designed to reduce installation time and labour costs and decrease downtime. The ULTRAPEM 3000 has been designed to support other wind turbine platforms such as Suzlon, Senvion, and Nordex, for which there is an opportunity for more than 7,000 turbines in India alone and several thousand more in North America. The ULTRA3000 is already in use with over 14,000 electric capacitor modules built for wind turbines, and there is about that much on the backlog with customers. The company is the exclusive supplier to the GE marketplace for the ULTRA3000, and as new products come out, the company should benefit from these.

ULTRA3000 overview in Q4 2022 (Investor Presentation 2022)

Financials and Q2 2024 Earnings updates

Over the last three financial years, we have seen the company increase its top and bottom line results. However, annual results over the last ten years show little consistency due to the nature of the engineered solutions the company provides, which are often niche with a small market. Furthermore, the company has disappointed in the FH 2024. In Q2 2024, we saw the company miss EPS and revenue expectations. The company has also seen a major decline YoY in its top and bottom lines.

In the second quarter of fiscal 2024, Richardson Electronics reported EPS of $-0.12 , which was $0.13 worse than the analyst estimates. The company's revenue for the quarter declined by 33% YoY to reach $44.13 million, falling short of the consensus estimate by $7.87 million. The company's net sales saw a sharp decline of 33.0% to $44.1 million in the second quarter of fiscal 2024, down from $65.9 million in the corresponding quarter of the previous year. This decrease was attributed to lower sales across all segments, particularly in the PMT and GES, with PMT sales dropping by 22.9% and GES sales plummeting by 78.8%.

{kind=link}

The company's gross margin deteriorated to 28.4% of net sales during the quarter, compared to 33.2% in the same period last year. The company reported an operating loss of $2.0 million in Q2 FY 2024, compared to an operating income of $7.2 million in Q2 FY 2023.

One of the strengths is a strong balance sheet with $23 million in cash and no debt. It also has a revolving line of credit of $30 million available. The company paid $0.8 million in cash dividends in the second quarter of fiscal year 2024. Furthermore, it declared a quarterly dividend of $0.06 per share, which will be paid in Q3 2024. One promising action to align the board with the company's progress is that it is requiring the board members to buy $150,000 worth of stock as part of their participation.

Valuation

We have observed a significant drop in the company's stock price by 19.04% in the last 24 hours due to a weak Q2 2024. This decline was expected as the net sales decreased by 33%. Additionally, there were unexpected project delays across the company's GES business, which further impacted the negative market sentiment.

{kind=link}

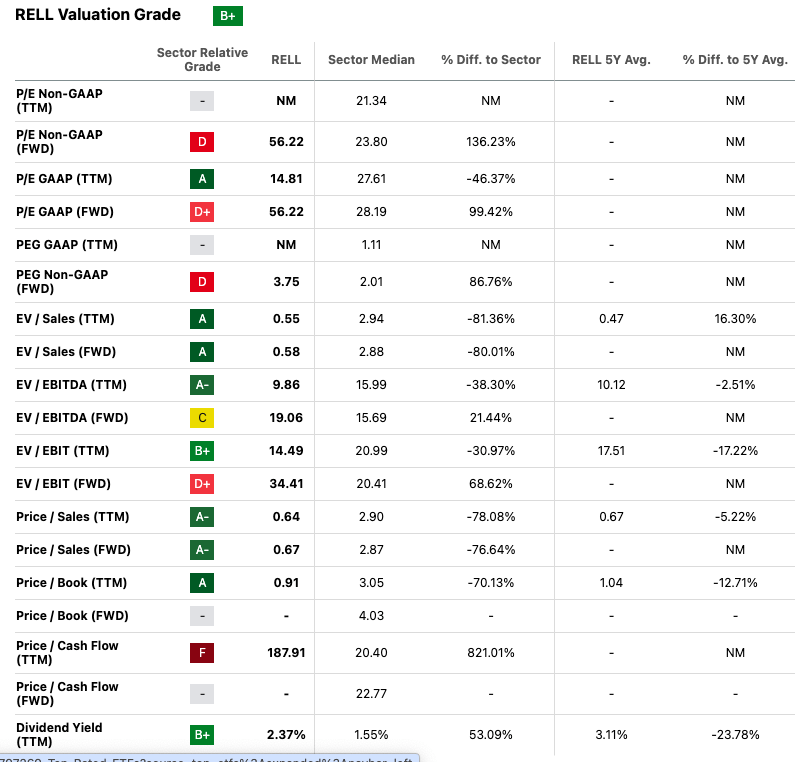

The company is facing some challenges, but it is hopeful about its growth potential, particularly in GES. It is expected to generate $500 million in revenue and have a good cash flow within the next five years. However, due to the lack of specific information regarding the size and scope of new contracts and the nature of the backlog, it is difficult to accurately assess future earnings. On the bright side, the stock is trading at an attractive price-to-sales ratio of 0.64, which means investors are paying less than a dollar for every dollar sold. Though the downward trend in financials is a concern, if it's only due to timing rather than bad business practices, this could be a very rewarding but equally risky stock.

{kind=link}

Final thoughts

Richardson Electronics’ Q2 2024 results have disappointed, with missed earnings and revenue estimates and significant declines in sales. The earnings call, on the contrary, paints a much brighter picture and reiterates the difficulty of evaluating this company on a quarterly basis due to its project-based solutions. Richardson Electronics continues to invest in its GES business, which could potentially drive significant long-term value. The company’s recent partnership with Integrated Power Services in North America and the growing global demand for its GES products suggest upside potential. The CEO has mentioned this is part two of the growth process. While enthusiastic about the potential, I maintain a wait-and-see-hold response while we get more concrete information on the amount of money and number of orders that new and existing customers are investing in the solutions.

For further details see:

Richardson Electronics: Betting On Green Energy