BBRYF - Richemont: Fairly Valued After Earnings Update

2023-11-11 04:56:21 ET

Summary

- Richemont's stock price has declined by almost 12% YTD following disappointing sales growth in H1 FY24, as the European market slowed down in Q2 FY24 and exchange rates were unfavourable.

- Despite the sales slowdown, profits remain stable and there is potential for continued profit growth, if margins continue to sustain.

- The stock is now however fairly valued, and with little impetus for demand growth for now, it doesn't have a Buy case for the short-to-medium term.

Since I last wrote about the Cartier owner Compagnie Financière Richemont ( CFRUY ) in late September, its price was up by 3.5% when I started writing this article. But as I finish writing, the release of its interim results for its current financial year (H1 FY24, full-year ending March 31, 2024) today hasn't gone down well with investors, knocking 3.85% from the price. It's now down by almost 12% YTD.

Is the decline justified, is what I explore here. And whether there's still upside to the stock and its ADRs or not.

Sharp sales slowdown

There's indeed some disappointing news in the latest update. The company’s sales growth for H1 FY24 has slowed down to 6% year-on-year (YoY) at actual exchange rates [AER], down from 19% for the full year FY23.

Weaker performance in the second quarter (Q2 FY24) drove this softening, as sales shrank by 2% in the quarter, compared to a healthy 14% increase in Q1 FY24. At constant exchange rates [CER], the numbers look somewhat better with a 5% sales growth in Q2 FY24, but even this is a sharp decline from the 19% increase seen in Q1 FY24.

This was to be expected, though. The company’s Chairman Johann Rupert had recently warned of weakening demand in Europe, which is a significant market for Richemont. This has played out, with a contraction in the market by 2% at AER (Q1 FY24: 10% growth) and a 1% decline at CER (Q1 FY24: 11%).

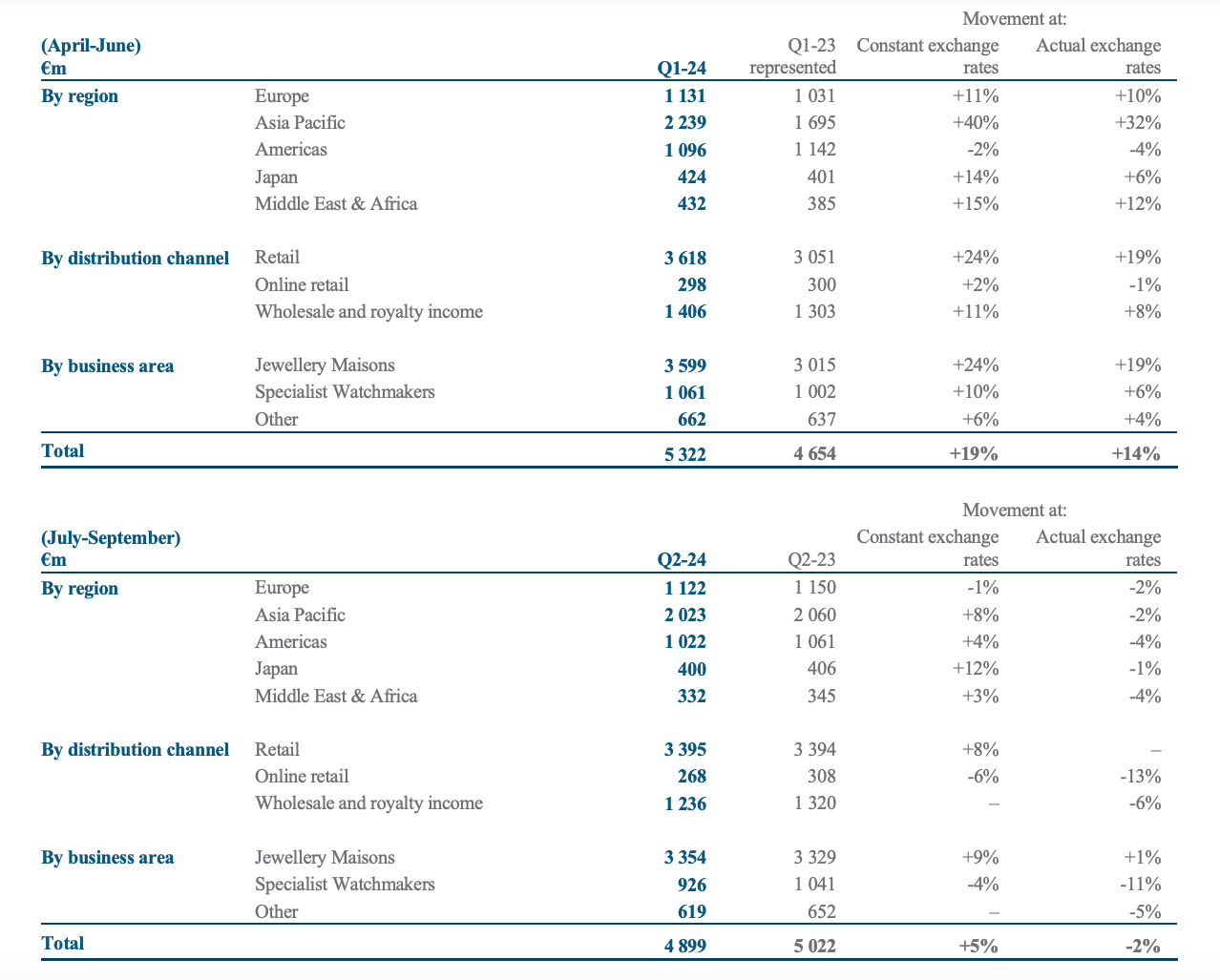

Sales by Region (Source: Compagnie Financière Richemont)

{kind=link}

It's worth noting, that at AER, all other markets have suffered too (see table above), indicating the adverse impact of unfavourable exchange rates during the latest quarter. Growth has slowed down in CER as well, to be sure, particularly for the big Asia Pacific market. But the silver lining is the surprising pickup in Americas’ growth after shrinking last quarter, which is encouraging for the remainder of the year even if Europe continues to slow down.

Profits look alright

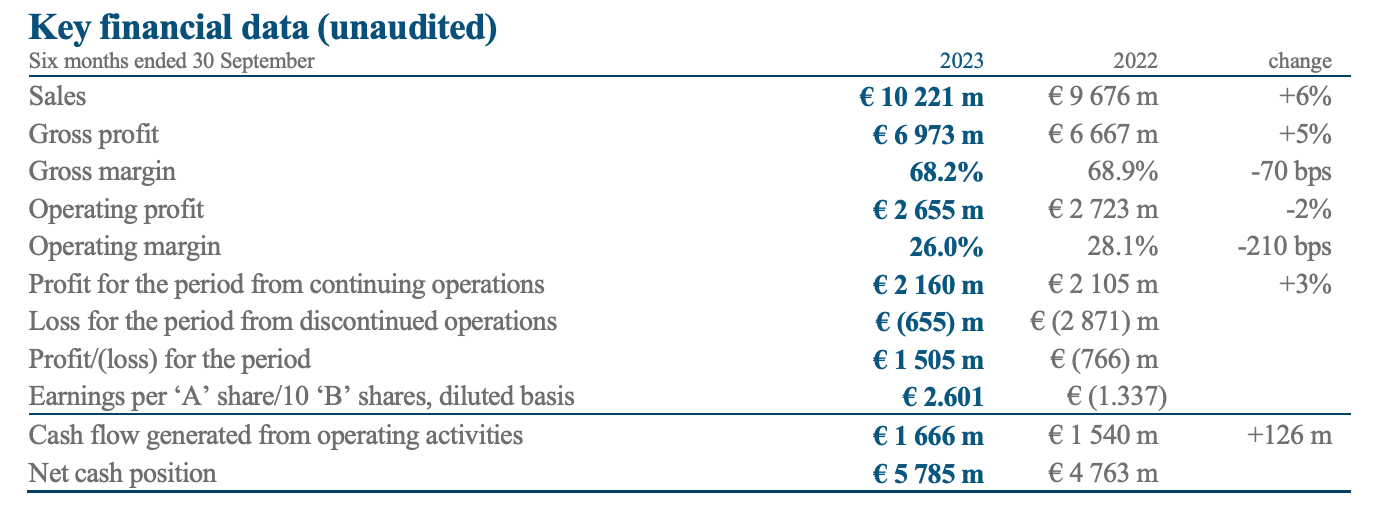

The profits picture isn't bad, however. While gross profits and profits for continuing operations saw an increase at AER (see table below), operating profit saw a small decline in H1 FY24.

Both gross and operating margin have seen a softening to 68.2% and 26% respectively as well. In themselves these margins aren’t bad at all, just that they have come off from the same time last year. The company attributes this to unfavourable exchange rates though, indicating that there’s nothing going on fundamentally with Richemont to impact margins.

The net profits however, look significantly improved from last year, when Richemont clocked a loss due to discontinued operations, which refers to the sale of the online portal YNAP to Farfetch ( FTCH ).

Source: Compagnie Financière Richemont

{kind=link}

The outlook

Still, the outlook for the company based on the latest trends isn't entirely a washout. Here's why.

If sales continue to shrink by 2% as seen in Q2 FY24, the company would still end up with a small growth of a little under 3% at AER for the full year FY24, however. Further, assuming that the margin for profits from continuing operations remains unchanged from H1 FY24 at 21.1%, there’s a chance for better profit growth of 10.7% for the full year, compared with the 3% in H1 FY24.

Also, net profits would likely be significantly higher considering that the company saw a small net profit figure of EUR 301 million in FY23 due to the loss from discontinued operations last year.

The market multiples

Based on this outlook, the forward GAAP price-to-earnings (P/E) ratio comes in at 22.1x. Richemont’s forward P/E is lower only compared to Prada ( PRDSY ), which according to my recent estimates was at 24.9x, among luxury peers.

It's comparable to LVMH ( LVMUY ) which is trading at 22.2x. And trades higher than the likes of Swatch ( SWGAY ) and Burberry ( BURBY ). SWGAY was at 11.7x when I last did the estimates in September and BURBY is at 14.2x as per analysts’ estimates.

When comparing the trailing twelve months [TTM] GAAP P/E, however, Richemont looks better. Its ratio at 16.8x is higher only than those for SWAY and BURBY, with the average of the luxury set at 18.3x. Essentially, the TTM P/E still looks competitive, but the forward P/E, not so much. On balance, it’s fairly valued though.

Consider the dividends

I do think, however, that it’s worth considering Richemont’s dividends for four reasons. One, with its earnings still growing, there’s potential for dividends to continue rising, as they have for the past three years. Two, the dividend payout ratio was at a comfortable 51.4% of earnings per share from continuing operations in FY23. This earnings measure is considered instead of the net income because the number was skewed to the downside on the losses from discontinued operations.

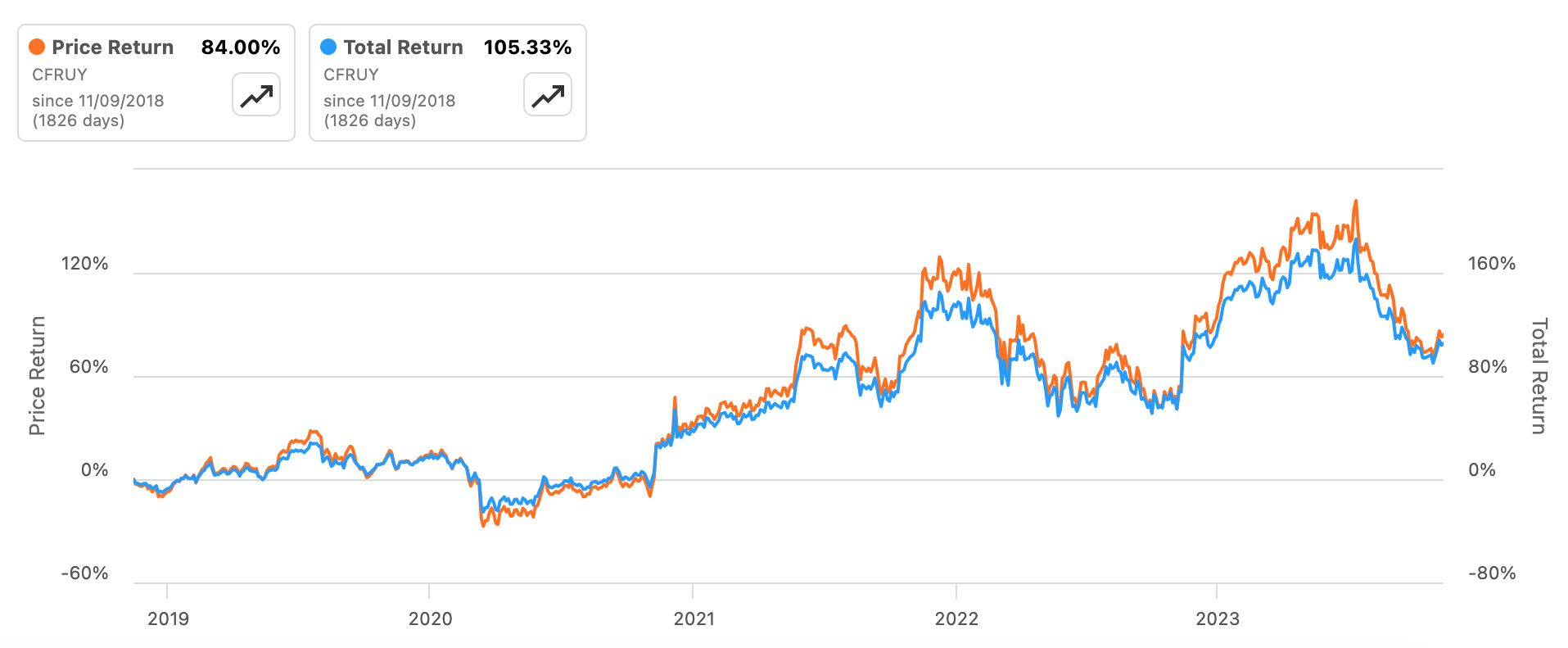

Three, the TTM dividend yield at 2.2% isn’t the best, but it isn’t bad either, at just a bit below the 2.5% for the consumer discretionary sector. Over time, dividends add up, impacting total returns positively (see chart below). And finally, Richemont’s dividends are stable, with the company having paid them consecutively for the past 13 years.

Price and Total Returns (Source: Seeking Alpha)

{kind=link}

What next?

The Richemont story effectively shows that while sales are softening, the profits are still doing alright. The drop in demand in Europe is concerning, but at the same time, some pickup in demand from the Americas in the latest quarter is encouraging. In any case, the profits continue to see some uptick, and if the margins remains constant, there’s potential for continued profit growth.

However, Richemont now looks fairly valued based on the market multiples. Though for investors already holding the stock, the passive income can keep trickling in, which is a good reason to consider buying it for the long-term anyway. But for short to medium term investors, I’d wait for another update to see how its financials evolve. I’m going with a Hold rating now.

For further details see:

Richemont: Fairly Valued After Earnings Update