CFRHF - Richemont: Resilience In The Luxury Sector Buy Confirmed

2024-01-20 01:52:44 ET

Summary

- Richemont's Q3 results show a 4% growth in top-line sales, with strong performance in Asia.

- We remain optimistic about Richemont's medium-term earnings opportunity, particularly in the Jewellery Maison division.

- Concerns over the termination of the YNAP agreement and potential write-downs impact Richemont's equity story, but the underlying business strength is solid. Our buy rating is then confirmed.

Compagnie Financière Richemont ( OTCPK:CFRHF ) ( OTCPK:CFRUY ) just release its Q3 2024 release. Following our last update with a rating upgrade called Time To Enter , we believe we had good timing. In early 2023, we were waiting for an entry point, providing two analyses with a neutral rating; however, we were optimistic about a stock price rebound (1. Richemont Could Benefit From A China Restart and 2. Another Set Of Solid Results ). Looking at the Q3 results, we were right, and the company's share is up by >10%. Before commenting on Richemont's performance, it is important to report our buy case recap: 1) a compelling valuation with a P/E in the 12/13x area (excluding the cash component) compared to a sector average at >20x, 2) M&A optionality, and 3) pricing power to show for the next year, given the fact that Richemont had less aggressive product price increase versus its closest peers.

{kind=link}

Mare Evidence Lab's past analysis

Q3 Results Analysis

Richemont's top-line sales grow 4% in the third quarter. The Swiss group based in Geneva, which controls luxury brands such as Cartier, Van Cleef & Arpels, and Piaget, closed the period with a turnover of €5.6 billion, showing stability despite the ongoing luxury slowdown.

All markets except Europe, where sales fell by 3%, reported an improving performance. In particular, Asia's results stand out, with China closing at +25% and Japan growing by 18%. On a channel level, retail leads the company with a plus 11% compared to last year's results and +6% on actual exchange rates. Looking at the business areas, the Jewellery Maisons division continues to generate the most robust results. On a nine-month basis, the group revenues increased by 5%, slowing down compared to the double-digit growth achieved in the last financial year. On a positive note, Richemont’s net cash increased to €6.8 billion. This is also key in our valuation and reflects the strong business performance.

Upside on the Horizon

Our last update emphasized how Q3 performance " will be decisive to understand what the 2024 prospects and visibility are ." After analyzing the update, we remain constructive on the company's medium-term earnings opportunity, particularly for the Jewellery Maison. This is based on a differentiated brand offering and an attractive valuation. Richemont is one of our top picks for 2024. Our target price is set at CHF 147 per share; we believe the following will likely unlock further shareholders' value:

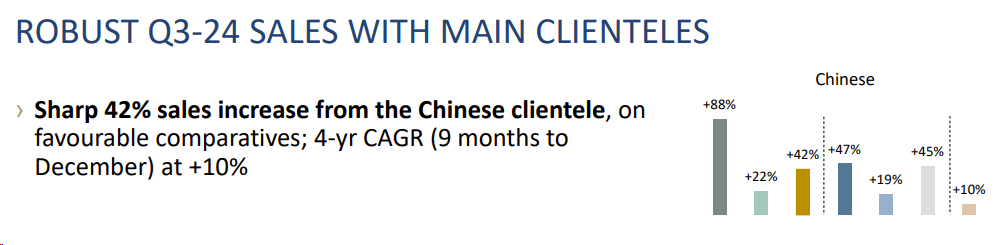

- China's cooling economy and challenging real estate crisis have worried the company, which has relied on the country for organic growth in the last few years. In Q3, supported by a rebound from strict COVID lockdowns (easy comps), the company enjoyed a surge in sales (Fig 1). This is a supportive signal for the sector and shows resilience in the luxury market. Chinese luxury spending signed a plus 50% in 2023, representing 30% of the entire market. Here at the Lab, based on McKinsey's latest State of Fashion report , we see a plus 5/6% in 2024 and account for approximately 80% of incremental sector sales. On the other hand, we see American and European luxury growth demand on pause;

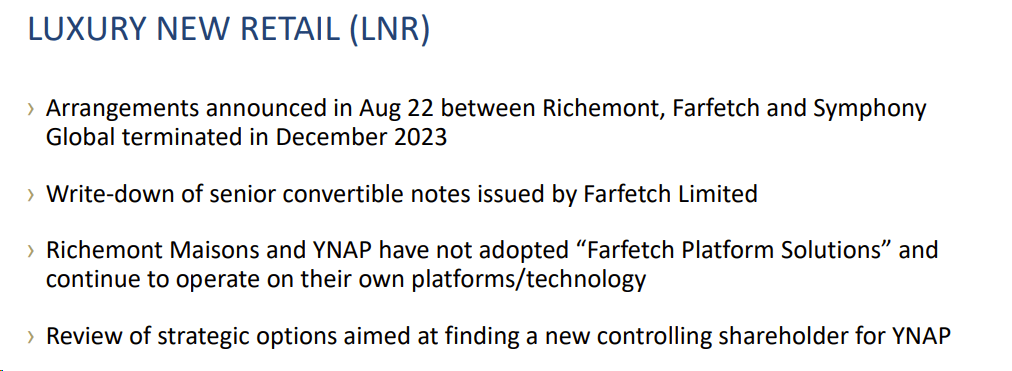

- Here at the Lab, we believe the YNAP termination transaction was largely expected. Before Q3, the company communicated the termination of the agreement with Symphony Global and Farfetch. Following Coupang's announcement of the Farfetch acquisition, Richemont will not adopt Farfetch Platform Solutions or use the open concessions on its marketplace (Fig 2). In the Q3 analyst call, the CFO stated that the YNAP option is going to be re-evaluated. That said, other assets write-downs are expected. Looking at the press release, the company stated that " it is reasonable to expect that the USD 300 million convertible senior notes issued by Farfetch Limited to Richemont in November 2020 will not be repaid " and that " the carrying value of these notes in Richemont's accounts amounted to EUR 218 million as at 30 November 2023 ." Therefore, we anticipate a €218 million write-down of an additional EUR 218 million. In addition, we should also report that the company invested $250 million in a Chinese Farfetch JV in 2020. Currently, it is not clear what is next, but we believe a further write-down is to be expected. Richemont reports YNAP business as an asset held for disposal until another buyer is found. Our team believes that YNAP value continues to cast a disproportionate shadow over the company's compelling equity story, and we are confident in the underlying business strength;

- Our Q3 results were supported by robust Jewellery demand over Christmas, but we still expect a more challenging environment in Q4. Despite that, the company has pricing optionality, and we expect a mid-single-digit price increase starting from April;

- As a reminder, the company closed its financials at the end of March. After the Q3 results, we now project Richemont's yearly top-line sales of €20.4 billion with an EBITDA of €4.7 billion. Our Q4 estimates are cautious for both divisions and below consensus expectations. This is due to a challenging Chinese consumer comparative from last year's reopening and European consumer demand weakness.

{kind=link}

Chinese sales evolution

Source: Richemont Q3 results presentation - Fig 1

{kind=link}

YNAP strategic options

Fig 2

Conclusion and Valuation

That said, luxury demand is normalizing post-COVID-19, but is still ahead of its historical trend. In addition, Richemont has solid business fundamentals, and we project higher sales compared to the luxury sector (5.8% vs. 4%). As a reminder, the luxury sector trades on 21x 2024E P/E, with a 5% discount versus its 10-year history. Being patient was a crucial advantage in Richemont, and today, continuing to apply a 2024 sector average P/E multiple of 21x, we derive an unchanged valuation of CHF 147 per share based on an EPS of CHF 6.8. Therefore, we maintain our overweight on Richemont. Following the recent developments in the Farfetch-YNAP, we expect Wall Street uncertainties around the next step for YNAP will ease. Downside risks include a lower-than-expected Chinese demand recovery and a persistent slowdown in the USA and EU areas. In addition, the company might be impacted by lower volumes due to additional price increases. In our last analysis, we slightly cut Richemont's target price on negative currency development.

For further details see:

Richemont: Resilience In The Luxury Sector, Buy Confirmed