WFCNP - Richie Capital Group Q1 2023 Letter To Investors

2023-04-11 22:00:00 ET

Summary

- Richie Capital Group invests on behalf of clients using an established investment process leveraging decades of investment experience. Our investment goal is to provide superior returns over time through the active management of long-only investment strategies.

- The year started in a bullish fashion only to see the banking crisis hit the brakes on market momentum.

- In our 2023 first quarter letter, we provide updates on our portfolios and discuss the potential long-term impacts of Silicon Valley Bank's demise.

Q4 2022 Performance Update

{kind=link}

Dear Partner,

The news moving markets this quarter was, again, the continued rise in interest rates, but also a minor earthquake in the financial sector: the collapse of Silicon Valley Bank ( SVB ), Signature Bank ( SBNY ), Silvergate Bank, and Credit Suisse ( CS ). In the aftermath of these events, we believe the most compelling question is: who will fill the void that Silicon Valley Bank leaves behind?

Who was Silicon Valley Bank?

Silicon Valley Bank was founded in the 1980s with the mission of addressing the specific needs of startup companies. At the time, the banking industry did not have a good understanding of startups and how to service companies that had promising futures but no revenue. SVB offered comprehensive banking services to founders with an understanding of the failure risks inherent in the world of startups. SVB managed this risk through their unique business model: offering loans in exchange for equity in the companies. Initially, founders seeking a loan from SVB had to pledge up to 50% of their equity as collateral. Over time, this rate fell to roughly 7% which reflected both a low failure rate and founders’ incentive to pay off the loans to maintain control of their companies [4] .

With this business model and a willingness to step in where other banks would not, SVB became the go-to bank for founders by offering products that were purpose-built for the industry. SVB provided a one stop solution so that founders could focus on developing their new technology instead of managing working capital. It was common for a venture capital firm’s term sheet to require that startups open a bank account at Silicon Valley Bank. Initially, SVB’s strategy was to simply manage bank deposits, but they eventually expanded their offerings to include services that would allow SVB to support these companies as they matured beyond their startup phase. When a new company received fresh funding from a VC, the startup would typically have many other needs. SVB opened its rolodex to connect these customers to its network of venture capital, legal and accounting expertise. They provided founders with credit cards and access to mortgages. SVB sponsored technology conferences and funded networking dinners and happy hours where entrepreneurs could connect with peers. SVB built an M&A arm to broker a deal if the startup needed to be sold. If a startup failed, SVB would assist in the orderly wind up of the business. SVB played the long game and became enmeshed in the VC community. Their absence will leave a gaping hole in the heart of Silicon Valley.

Who will step in?

With SVB’s demise, the question remains, who will provide these much-needed resources to startups that don’t fit the traditional banking model? SVB is credited by many founders and VCs as being more willing to lend to startups than larger banks. Even as startups flocked to the larger banks during the recent crisis, the larger banks have no need (and are now disincentivized) to take the same risks. Wells Fargo ( WFC ) and JP Morgan ( JPM ) have always had specialist teams of bankers in Silicon Valley and can fill some of the gaps, but their services will not match those of a bank that spent 40 years honing a specialty business model. Without SVB, early-stage companies will be met with higher borrowing rates and more hurdles securing venture debt. It is notable that even SVB prioritized supporting companies that received funding from the top-tier VC firms such as Kleiner Perkins, Sequoia, and NEA to reduce risk. With SVB gone, only the blue blood startups will have access to resources.

Who do you trust?

The entire banking industry (and the value of the U.S. Dollar itself) is built upon trust. We trust that our financial institutions will have our money when we want it. In exchange for making our deposits, the bank takes our money, loans it elsewhere and pays us a portion of that interest spread. The entire system is predicated on all depositors not asking for their money back at the same time. At the beginning of March, news that SVB needed to quickly raise capital by selling some of its investments at a loss sent the stock into a freefall. VCs and founders rushed to their phones to encourage their portfolio companies to get their money out of the bank as quickly as possible, the very definition of a bank run. Because social media fueled the panic and withdrawals could be made via smartphone apps, this was likely one of the quickest bank runs in history.

An interesting correlation is that as these banks collapsed, the crypto economy rose. The value of Bitcoin was up 70% through Q1, and the value of Coinbase ( COIN ) rose nearly 80%. This would seem to imply that cryptocurrency investors view crypto as a safer alternative to the banking system. However, if over the past few years, a significant portion of the U.S. banking system had been offloaded to cryptocurrency and there had been a similar failure within the crypto ecosystem, who would have bailed out the system? Who do you trust?

There are long-term implications for public markets and our investments. SVB’s collapse, combined with an already slowing macroeconomy, will likely slow deal flow among VCs and in some ways stifle the “innovation economy.” The real effects of the demise of SVB may not be felt for many years. For public equities, venture capital is the “farm team” for the universe of public equities. Venture capital supports the innovation economy by providing funding to promising startups which will hopefully grow large enough to become public companies. According to an updated 2021 research paper [5] , venture capital-backed companies account for 41% of total U.S. market capitalization and half of all public companies founded within the last 50 years. Our largest tech companies, and arguably the crown jewels of our economy (Apple, Alphabet/Google, Amazon, Microsoft, etc.) were all birthed from VC investment. Without the farm system, the U.S. loses its innovation engine: prior to the 1970s (when the VC industry was spawned), the U.S. did not create top public companies at a higher rate than other developed countries. But since the development of the VC ecosystem, the U.S. now produces twice as many top public companies as other developed nations [6] .

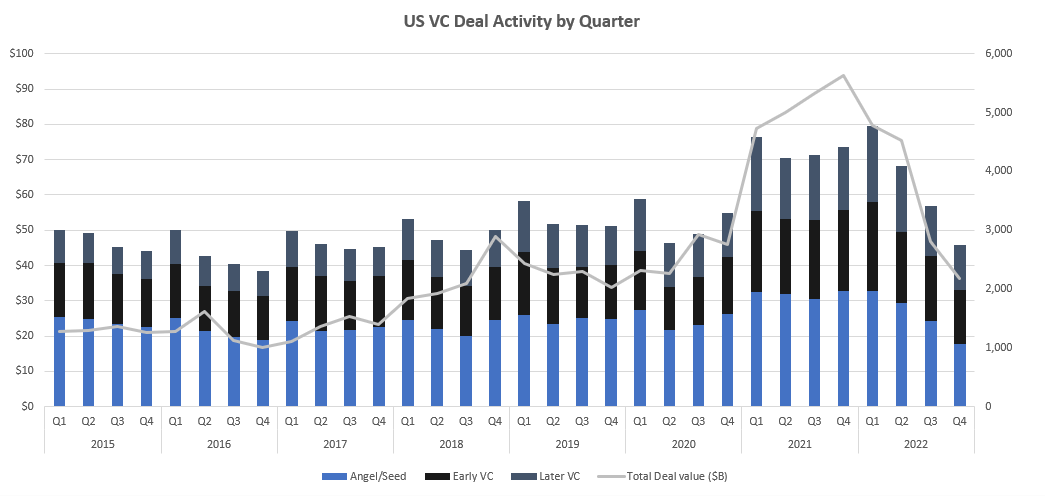

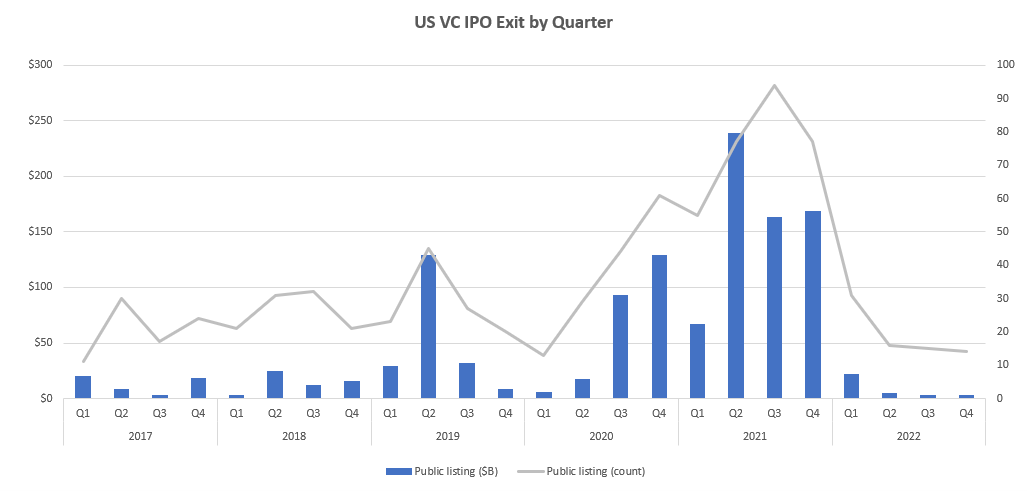

Even prior to the recent banking crisis, there were clear negative trends within the industry:

Slowing deal flow

{kind=link}

Fewer IPO exits

{kind=link}

These would appear to be natural cyclical drop-offs in activity after periods of inflated (bubble?) levels of activity. However, the loss of a key cog in the system leaves questions, and a void. The events will likely put a damper on innovation and, at a minimum, squeeze long-term growth from the economy. We continue to align our client portfolios to this new reality.

S ELECTED P ORTFOLIO D ISCUSSION

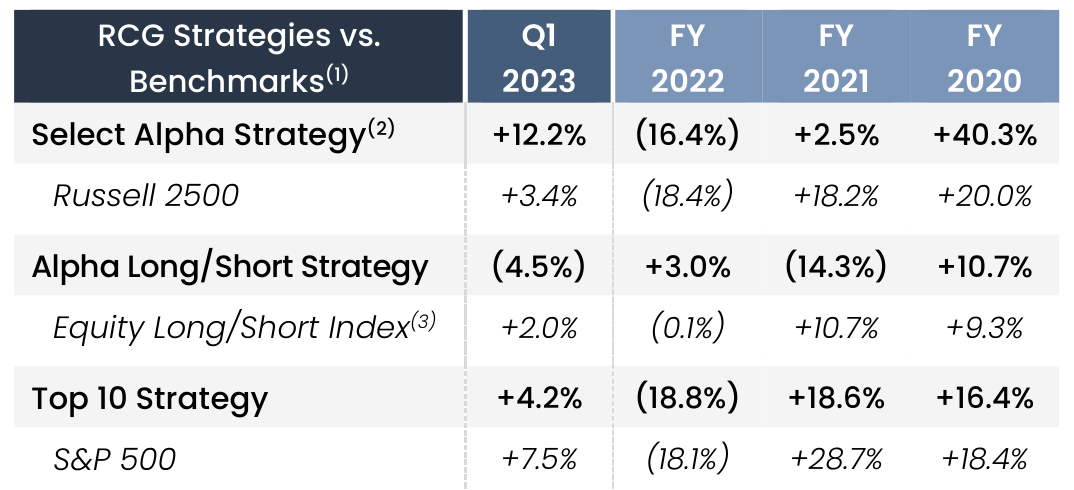

For the first quarter of 2023, the RCG Select Alpha strategy gained 12% while the RCG Long Short strategy declined 4%. Their respective benchmarks the Russell 2500 Index gained 3% and the Equity Long Short Index gained 2%. In the first quarter, the market suffered from whiplash. Stocks rose in an upbeat fashion in January driven by better than feared Q4 earnings results and signs of easing inflation. The Fed raised rates twice, and the markets began to expect that hiking would soon come to an end. The collapse of SVB and further financial sector contagion throughout the U.S. and Europe pulled stocks in reverse. The brunt of the impact was felt in the world of small and midcap (R2000 and R2500) with volatility rising 30%+ while the broader market remained relatively stable.

Q1 2023 Biggest Contributors :

Perion Network ( PERI up +56.4%) – Our investment in the Israeli based ad-tech company has now been a top performer for two quarters in a row. In February, Perion announced full year 2022 earnings which included guidance for 14% revenue and EBITDA growth in 2023. This implies meaningful growth in a challenging environment where their peers continue to struggle. Despite the stock’s strong performance, Perion is still trading at a modest 19x earnings.

In addition to the optimistic growth outlook, Perion seems to be benefiting from anticipation of Bing’s new ChatGPT driven search engine. Bing is Perion’s largest customer. We, along with Perion’s management, believe that the “new Bing” offers a meaningful growth opportunity. The more users convert to Bing, the more publishers will advertise on the platform and drive Perion revenue. On Microsoft’s Q4 earnings call, CFO Amy Hood discussed the impact of growing Bing market share: “every percentage point of share it gains in search equals roughly $2 billion in additional advertising revenue.” It is difficult to envision a scenario where Perion is not a direct beneficiary of Bing’s success.

A notable announcement during the quarter was the departure of CEO Doron Gerstel who will step down on July 31 st . Gerstel has served as the CEO for six years and was initially recruited to turn the company around. He has exceeded expectations. Gerstel stated he “needed time to re-energize” after having been CEO of five different companies since 1999. Gerstel is certainly a big loss, but we believe his successor, Tal Jacobson, is a credible and proven replacement.

Jacobson was recruited from Similar Web in 2018 to help revamp Perion’s search business. As the General Manager of CodeFuel, Tal transformed Perion's search advertising from a fledgling business unit in decline into a significant driver of Perion's soaring market share by cementing the strategic relationship with Microsoft and winning Microsoft Advertising Global supply partner of the year award. We believe Tal is an ideal successor. Hiring internally is the right decision and Jacobson is the obvious internal candidate.

Long term growth remains attractive as Perion continues to incubate new products and technologies in what they call the “explore execution model”. Perion continues to be an exciting growth story at a great price.

Comfort Systems ( FIX up 26.9%) – The national provider of HVAC installation, maintenance, and repair services, had an outstanding quarter. Driven by positive tailwinds from the trends in modular construction and American business reshoring, the company finds itself with more business than it can accommodate. Management highlighted that Comfort Systems has an order backlog that will keep them busy well into 2024. Their order book is completely full for 2023 and they are now booking projects for 2024. The reported jump in backlog was primarily due to a large order from a single customer in the modular construction business. The commitment is to support a large customer project where the company is seeking to get ahead of other businesses and the coming reshoring trends. One of the traits we most admire about Comfort Systems is their deep relationships with their customers. Comfort System’s believes that this is only the beginning of the movement towards reshoring and, in the coming years, more businesses will develop new buildings and facilities in the U.S. to overcome recent global supply chain challenges.

Finally, Comfort Systems announced the acquisition of South Carolina-based Eldeco. Edelco performs electrical design and construction services in the Southeast and is expected to contribute annualized revenue of $130 to $140M. The acquisition will be accretive to earnings in 2023 and 2024.

MSCI ( MSCI Inc up +20.6%) – MSCI was a top performer in the first quarter supported by a strong Q4 earnings report, an optimistic outlook for 2023, and a flurry of bullish sell-side analyst reports. MSCI has proved to be a diversified all-weather franchise, increasing organic revenue by 9% in 2022 despite a volatile year that saw the S&P 500 closing down -18% after reaching depths as low as -25%. MSCI management appears optimistic based on their projected 4% to 10% increase in free cash flow for 2023.

Growth in the ESG and climate segment is a major growth lever for MSCI and will be a focus for investors in 2023 and beyond. Longer-term, management believes this segment will grow at a mid to high 20% rate. This is an ambitious target for a segment that is already generating $228 million in revenue, but we believe it to be achievable. MSCI is an underappreciated ESG beneficiary and is positioned to benefit from the ESG movement. There is a growing trend for companies such as EV manufacturers and alternative energy providers to market themselves as ESG. They will rely on MSCI to assist them in providing measurable and concrete ESG characteristics and data to support these claims.

We believe MSCI is a proven compounder with leading offerings in both the lucrative index data field and the emergent ESG data industry. This “compounder” quality is reflected in that approximately 97% of revenue is recurring, they have an attractive cash flow generation profile, and a history of creating value for shareholders with double digit annual EPS growth since 2014.

Q1 2023 Biggest Detractors:

A10 Networks ( ATEN down -11.1%) – The provider of cybersecurity and infrastructure solutions for on-premises, cloud and edge environments traded down during the quarter despite recording a record fourth quarter and full year revenue. The company still faces some challenges as they transition from a hardware focus to becoming software centric. Investors were likely concerned with ATEN’s negative growth in their enterprise segment. Despite near term headwinds, we view the company as an attractively priced cybersecurity market leader with attractive margins and high returns on capital. The company continues to outpace their peers in the Application Delivery Controller ( ADC ) market and expects double digit earnings growth for the full year 2023.

AMT (American Tower Corp down -3.6%) – Shares of American Tower lagged in the quarter after a lackluster earnings report and a broader sell-off of in REIT’s. Rising interest rates have hampered the REIT sector as 1) income investors can now find comparable yields from U.S. treasuries, and 2) debt financing for real estate has become considerably more expensive.

In the fourth quarter earnings report, American Tower recorded a -$642 million impairment charge when VIL, American Tower’s largest customer in India, was unable to make their scheduled payments. Management views India as more of an opportunistic growth driver and commented that they are open to all possibilities, including a partial equity sale of the India business. India is a very attractive market long term due to favorable demographics and a growing need for data, but it is encouraging to see that management is clear eyed in assessing this new market.

Despite these temporary headwinds, American Tower’s core business is strong. Management anticipates double digit AFFO growth in 2023 driven by solid organic leasing trends across the global portfolio including a meaningful step up in U.S. and Canadaian organic tenant billings in 2023. Longer term, we believe the ever-expanding need for data will drive more tower demand and density. American Tower has an incredibly attractive business model supported by long-term contracts with large communications companies which include annual price escalators.

Conclusion

Our portfolios have had a great start to the year despite fears of an economic slowdown. As a firm with aspirations to become a world class institutional investment firm, we view 2023 as an exciting new phase in the growth of our business and the RCG story. To commemorate our development, we have updated our website www.richiecapital.com with a shiny new look and feel. We have some exciting developments on the horizon and look forward to sharing them with you in the coming quarters. Until then, we are always open to investor questions and feedback. And, as always, we thank you for entrusting us with your valuable investment assets.

Khadir Richie

Founder & CIO, Richie Capital Group

|

Footnotes[1] All portfolio and index returns mentioned are presented net of expenses and maximum management fees paid by any account within the composite. All performance is estimated pending year-end performance audit. Completed audit numbers available upon request. Please refer to the end notes at the end of this letter for additional information on the benchmarks provided. [2] The RCG Long Only strategy has been rebranded the “RCG Select Alpha Strategy” as we continue to expand our client offerings. [3] Represents the BarclayHedge Equity Long/Short Index. [4] Silicon Valley Bank - Wikipedia [5] The Economic Impact of Venture Capital: Evidence from Public Companies [6] https://www.aei.org/economics/americas - greatest - economic - assets - the - venture - capital - industry - has - to - be - near - the - top - of any - list/ |

DisclosureThe information contained herein reflects the opinions and projections of Richie Capital Group, LLC and its affiliates as of the date of publication, which are subject to change without notice at any time subsequent to the date of issue. Richie Capital Group does not represent that any opinion or projection will be realized. All information provided is for informational purposes only and should not be deemed as investment advice or a recommendation to purchase or sell any specific security. This shall not constitute an offer to sell or the solicitation of an offer to buy any interests in any fund managed by Richie Capital Group or any of its affiliates. Richie Capital Group has an economic interest in the price movement of the securities discussed in this presentation, but Richie Capital Group's economic interest is subject to change without notice. While the information presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy of any data presented. This communication is confidential, and all content contained herein is protected by U.S. and international copyright laws. You may not copy, reproduce, distribute, transmit, modify, create derivative works, or in any way exploit any part of copyrighted material without the prior written permission from Richie Capital Group. Performance returns are estimated pending year-end audit. Past performance is not indicative of future results. Actual returns may differ from the returns presented. Factors that could result in a difference between composite returns and client account returns include, but are not limited to, account asset size, asset allocation, timing of transactions, commissions, management fees and specific client mandates relative to individual investment objectives. Estimated returns are presented net of expenses and maximum management fees. All dividends are assumed to be reinvested. References to market or composite indices, benchmarks, or other measures of relative market performance over a specified period are provided for information only. The composition of a benchmark index may not reflect the manner in which a Richie Capital Group portfolio is constructed in relation to expected or achieved returns, investment holdings, portfolio guidelines, restrictions, sectors, or concentrations, all of which are subject to change over time. Each client will receive individual returns from their respective custodian. Positions reflected in this letter do not represent all the positions held, purchased, or sold, and in the aggregate, the information may represent a small percentage of activity. The information presented is intended to provide insight into the noteworthy events affecting returns for clients. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Richie Capital Group Q1 2023 Letter To Investors