NTDOF - Right Tail Capital Q4 2022 Investor Letter

Summary

- Right Tail’s portfolio is nearly 90% invested (up from 74% last quarter).

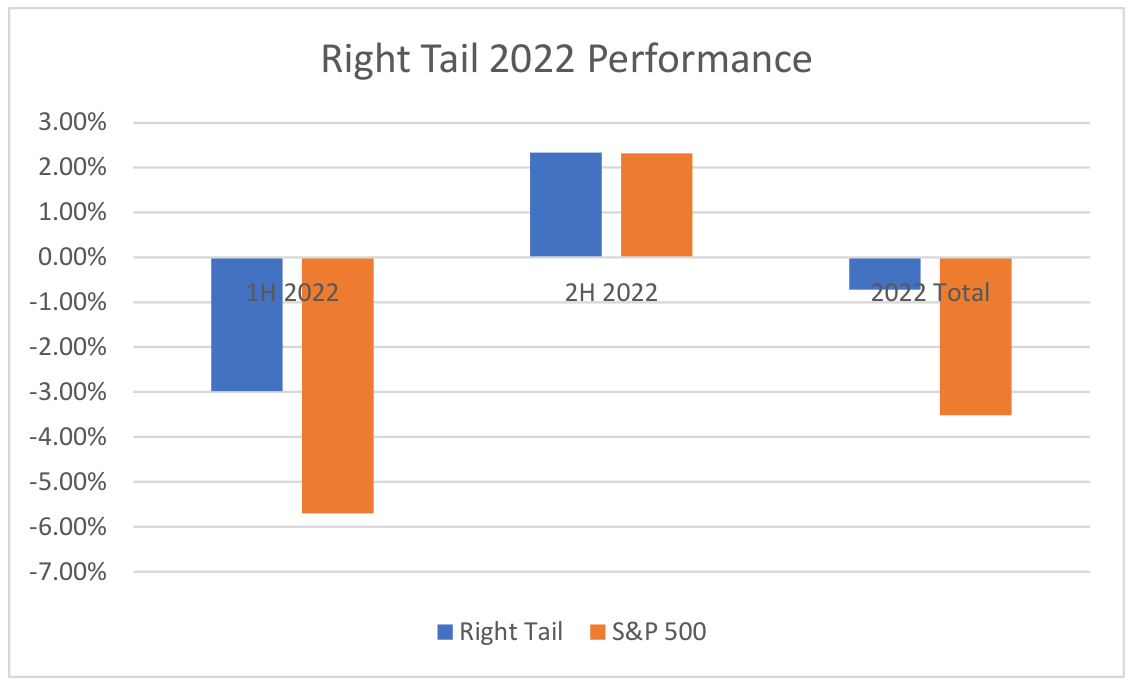

- 2022 performance is -0.7% while the total return of the S&P 500 was -3.5%.

- One of Right Tail’s investments is Ross Stores which I purchased at inception in May 2022.

When is the last time you made an Amazon ( AMZN ) purchase that only had 58 reviews? What if I told you the product was not brand new, but had been around 5 years?

Well, my favorite book this year fits this description. It is so unpopular that there is not even an audio edition. Do you want to buy it now?

Thinking independently is important in investing as well as not judging a book by its reviews or a stock by what the crowd thinks. A friend of mine recommended the book I’m referencing, and to me, it punched well above its accolades.

I read broadly to gather knowledge and become a better investor. At the University of Virginia, I explored various fields such as medicine, history, economics, and classics. Charlie Munger often describes the benefits of reading. He says, “As long as I have a book in my hand, I don’t feel like I’m wasting time.” He also suggests, “Develop into a lifelong self-learner through voracious reading. Cultivate curiosity and strive to become a little wiser every day.” Angel investor Naval Ravikant similarly extols reading. Like the power of other small habits compounded over time, he says “I probably read one to two hours a day. That puts me in the top .00001 percent. Eventually you will read enough things…that it will dramatically improve your life.”

The book is One Buck at a Time: An Insider's Account of How Dollar Tree Remade American Retail by cofounder Macon Brock and journalist Earl Swift. It is an undiscovered gem, rich with insights.

I do not know why this book is unknown. It could be that business biographies are less popular but Shoe Dog, the excellent tale of Nike’s ( NKE ) founding by Phil Knight, has over 25,000 reviews. Perhaps Dollar Tree ( DLTR ) is less of an exciting brand than Nike with a less well-known founder. The boutique Beachnut Publishing may not carry the same cache as larger publishers.

The authors trace Dollar Tree’s rise. From its roots within a company selling toys at shopping malls, Dollar Tree blossomed into a fabulous business that has delighted its stakeholders for decades. An initial investment of ~$50,000 sparked the creation of a company whose enterprise value is ~$40 billion today.

The inflection point was in the mid-1980s when management discovered a store called “Everything’s A Dollar.” They admired the unexpected, low-priced values and faster inventory turns, and they thought their existing expertise in sourcing product from Asia would be an advantage versus competitors.

They were right. Astoundingly, “Every store paid for itself in its first year…Some earned enough…to [almost] pay for a second store.” What a phenomenal return on investment to have a store pay for itself so quickly with many years of large future cash flows to come.

The willingness to significantly change the company as management pivoted to the dollar store model is very rare. In addition to their supply chain competency, the keys were good processes, a company culture of optimism and teamwork, and applying a lesson from their toy store days – that you should surprise and delight your customers every time they come in the store. As one executive put it:

“What simplicity to sell each product for only dollar. What bravado as well! Such are the deals that Dollar Tree provides its customers every day. They defy credulity…Yet the company's stores maintain one of the highest profit margins in the business.”

I love how this book speaks to the magic of great businesses. Capitalism competes away excess profits so businesses must be exceptional to stand the test of time. Dollar Tree has done it by sourcing great values that it sells at a low price (only $1 for most of its history). Other businesses that Right Tail has discussed in the past similarly delay, and sometimes defy, the gravity of capitalism.

The business insights and company story are intermingled with insightful historical anecdotes. The authors led me on a nostalgic trip through the retail landscape of my childhood. I was taken back to the 1980s with discussions of Toys’R’Us ( TOYRF ) and the early days of the video game industry led by Atari ( PONGF ) and Nintendo ( NTDOY ). We also learn about the evolution of discount retail, the challenges of dealing with union labor, and the 20th century history of Norfolk, Virginia, where the company was founded.

Despite Dollar Tree’s fantastic long term track record, Mr. Brock has a poor opinion of the short-term nature of the stock market. He says “Wall Street didn't give a damn then about long term performance (2000), and it doesn't now. It doesn't give a damn about the past or the future either. It focuses only on what's shiny and right under its nose. The market has a notoriously short attention span.” This insight is yet another reminder of the value of Right Tail Capital’s long-term perspective in finding high quality investments to generate strong long-term performance.

If you read this book, please let me know what you think. Meanwhile, I will continue to treasure hunt for fantastic businesses at reasonable prices that delight their investors the way Dollar Tree delights its customers. Stay tuned for a current investment discussion on another discount retailer later in this letter.

Portfolio and Performance Discussion

Speaking of our investments, Right Tail’s portfolio is nearly 90% invested (up from 74% last quarter). They are undervalued, high quality companies with durable competitive advantages, excellent management, and attractive return potential.

While I encourage us to judge Right Tail’s performance over multi-year periods, I wanted to provide an update on performance since mid-May. 2022 performance is -0.7% [1] while the total return of the S&P 500 was -3.5%. No one enjoys seeing their accounts decline in value. I do not want to overstate the significance of these results in this wealth-compounding marathon, but I am pleased that Right Tail has gotten off to a good start and outperformed the market [2] . Right Tail’s long-term perspective continues to be one of our greatest foundations, and I look forward to continuing to build Right Tail’s track record in the years to come.

{kind=link}

Investment spotlight: Ross Stores ( ROST )

One of Right Tail’s investments is Ross Stores which I purchased at inception in May 2022. I have also owned this business since the early onset of Covid in 2020, one occurrence when the market offered the shares at excellent value.

The company is headquartered in California and has an enterprise value of ~$41B. Like Dollar Tree, Ross Stores delights its customers with a treasure hunt experience. The company has ~2000 off-price retail stores around the country. Ross’ name-brand apparel and home fashions offer savings of 20% to 60% relative to typical retail prices.

Like many Right Tail investments, Ross provides value to several of its partners. Customers, who either want a bargain or possibly need a bargain, discover less expensive branded goods. Vendors rely on Ross to sell unwanted inventory discreetly. Rather than discounting the product at their own stores or website and training customers to expect and even wait for discounts, a vendor sells some of its product to Ross receives cash for its inventory and can move on.

Interestingly, Ross’ value proposition likely increases during tougher economic environments like the one we’re in today and the great financial crisis. Consumers know they can find a good deal. Vendors liquidate unwanted inventory and plan for the next selling season. Often, Ross Stores can establish new relationships with vendors who need them more during tougher times. This increases its ability to delight its customers. While vendors may prefer to partner with Ross only during tough times, I suspect Ross’ ability to generate additional sales keeps them coming back. These dynamics help perpetuate the company’s moat. More vendors likely lead to more customers.

This fantastic value proposition has helped Ross please its shareholders. The stock has risen >200x (not including dividends) since its IPO in 1985. Buffett’s retained earnings test also confirms the stellar returns – market cap has grown by $33B since 2010 while retained earnings have only grown $2.4B. This indicates that Ross Stores has created tremendous value per dollar of investment.

The opportunity to invest in Ross at a discount to intrinsic value likely exists for a few reasons. There are general worries about the health of the economy, stock market and consumers. Recent same store sales have been down low to mid-single digits after a strong 2021. These concerns also ignore that same store sales have increased low to mid-single digits over the last two decades. Additionally, Ross has faced margin pressures due to labor shortages and freight challenges, the latter of which continue to abate. It’s been a unique, challenging set of circumstances the last few years between Covid, stimulus and cost pressures that have affected all parts of Ross’ and its off-price competitors’ businesses.

In a typical year, Ross likely grows earnings low double digits or higher. They achieve this through same store sales and new stores each growing low to mid-single digits. From this base of 5-8% revenue growth, the company achieves some operating leverage and shrinks the share count to get to low double-digit earnings growth. The opportunity today is potentially sweetened assuming Ross can improve margins back to pre-pandemic levels. Combine it all and a mid-teens CAGR or 5-year double seems like a reasonable base case from today’s prices.

The short-term risks are questions around the economy. Certainly, if consumers have a tougher time, they may buy fewer goods in the short term. That said, I take comfort in knowing that Ross offers great, and potentially improving, values to its customers during a tougher economy. Longer term I worry about store count and a successful online treasure hunt experience. Ross increased its long-term count target last year and continues to enter less-penetrated geographies. The online experience strikes me as inferior to the in-person experience for consumers and vendors alike. Vendors do not want their closeout sales to be widely broadcasted. While consumers enjoy the convenience of online shopping and home delivery, they may not get the same treasure hunt experience of serendipity. Furthermore, the ability to see these items firsthand is important.

Thank you for your continued interest in Right Tail. Your long-term mindset, especially in more volatile stock markets like today, is one of our greatest advantages. Please reach out if you would like to discuss Ross Stores or Right Tail’s other investments in more detail.

May you all have a fantastic 2023,

Jeremy Kokemor, Right Tail Capital

DISCLAIMERThis review (the “Review”) is being furnished by Right Tail Capital LLC (“Right Tail” or the “Firm”) for informational purposes only. This Review does not constitute an offer to sell, or a solicitation, recommendation or offer to buy, any securities, investment products or investment advisory services offered by the Firm (the “Offering”). Any offer or solicitation may only be made to prospective eligible investors by means of an Investment Advisory Agreement and Form ADV, which contain a description of the material terms relating to the Offering, including the numerous risks involved. This Review is being provided for general informational purposes only. Right Tail Capital (“Right Tail”) is registered as an Investment Adviser with the states of Virginia and Louisiana. Interested parties should read Right Tail’s Forms ADV I and II, available at adviserinfo.sec.gov. Certain information set forth in this Review is based upon data, quotations, documentation and/or other information obtained from various sources believed by the Firm to be reliable. No representation or warranty, expressed or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. This report and others posted on www.RightTailCapital.com are issued without regard to the specific investment objectives, financial situation, or needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Company fundamentals and earnings may be mentioned occasionally but should not be construed as a recommendation to buy, sell, or hold a company’s stock. Predictions, forecasts, estimates for markets should not be construed as recommendations to buy, sell, or hold any security -- including common stocks, bonds, mutual funds, futures contracts, and exchange traded funds, or any similar instruments. Investment strategies managed by Right Tail involve a significant degree of risk, and there can be no assurance that the strategy’s investment objectives will be achieved or that significant or total losses will not be incurred. Nothing contained herein is or should be relied upon as a promise, representation or guarantee as to the future performance of Right Tail’s strategies. Past performance is not indicative of future results. Images, graphics, logos, and other designs used in the Review are believed to be in the public domain. A reasonable, but not exhaustive, effort has been made to verify that such images, graphics, logos, and designs are not protected under copyright. However, if any party feels that this Review is in breach of copyright law, it should immediately contact the Firm. Performance data for the Right Tail Portfolio is based on the advisor’s brokerage account which was invested beginning on May 16, 2022. This performance figure has not been audited by any third party. Individual account performance will vary depending on a variety of factors, including the initial date of investment, inflows/outflows, account size, fee class, and transaction costs. Please see your individual account statement(s) for actual account balances and performance. Performance comparisons to benchmarks such as the S&P 500 Index and the SPDR S&P 500 ETF Trust ("SPY Index ETF", "SPY", or "S&P 500 Index ETF") are provided for information purposes only. The SPY is an exchange-traded fund which seeks to provide the investment results that, before expenses, correspond generally to the price and yield performance of the S&P 500 Index. The S&P 500 Index is a diversified large cap U.S. index that holds companies across all 11 GICS sectors, and as such may differ materially from the securities managed by Right Tail in client accounts. Benchmarks such as the S&P 500 Index and the SPY may be of limited use in understanding the risks and uncertainties inherent in the investment strategies managed by Right Tail. The information in this Review is not intended to provide, and should not be relied upon for, accounting, legal, or tax advice or investment recommendations. The Recipient should consult the Recipient’s own tax, legal, accounting, financial, or other advisers about the issues discussed herein. Nothing in this Review regarding tax strategies, tax savings, tax rates, tax efficiency, or any other statements related to taxes should be relied upon as an indication of Right Tail’s suitability to give advice or make decisions with respect to taxes in any jurisdiction. |

Footnotes[1] Net performance for Right Tail’s performance fee structure. Management fee paying investors would be ~78 bps lower. [2] As judged by the S&P 500 total return. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Right Tail Capital Q4 2022 Investor Letter