TJX - Ross Stores: Great Business But Valuation Is Not Attractive

2023-12-19 06:32:47 ET

Summary

- I recommended a hold as I believe the market has already priced-in growth potential over the next 3 years.

- ROST has shown strong growth momentum and has room for further expansion in the Midwest and Northeast regions.

- Gross margins are expected to rebound to historical levels as the business recovers from the impacts of COVID-19.

Investment overview

I am recommending a hold rating for Ross Stores (ROST) as I believe the market has already priced in the potential growth over the next 3 years. However, that is not to say that I am negative about the business. I am just waiting for the right time to purchase the stock, as I believe ROST growth momentum should persist for the long term and margins will revert back to historical levels.

Business description

ROST is a big name in the off-price retail industry in the US and is one of the three big boys: Burlington Stores (BURL) and TJX Companies (TJX) being the direct competitors. The key product lines that ROST focuses on are apparel and home fashion. The concept of off-price retail has been well received by US consumers, as evident from the strong expansion in the number of stores over the past decade. For ROST, the business has grown the number of stores from 1,055 to 2,112 as of 3Q23. Strong expansion has led to net sales growing from $7.9 billion in FY10 to $19.6 billion over the trailing 12 months [TTM].

Growth momentum showing no signs of slowdown

As mentioned, ROST has demonstrated very strong growth performance over the past decade, and I believe the growth runway remains long and clear for ROST. ROST's growth is essentially a function of store growth and same-store-sales [SSS] growth. The major growth driver ahead is likely to come from store growth, as ROST still has plenty of whitespaces in the Midwest and Northeast parts of the country. Relative to ROST, TJX is more well penetrated across the entire US, which I believe sets a precedent that ROST can do the same too. For size reference, TJX has 4,934 stores as of 3Q23 across the entire nation, which is more than 2x the size of ROST, suggesting significant room for store expansion.

As for the near-term growth drivers, aside from store growth, I see the current macro environment as a growth tailwind for SSS growth. The logic is straightforward, in that the high inflationary environment has resulted in low consumer confidence and reduced disposable income. This essentially forces consumers to be more cost-conscious and look for more value alternatives, which is ROST's strong point. This pressure is not only true for the low-income consumer; it appears to be impacting the higher-income group as well, also known as a trade-down. In my opinion, the off-price channel, such as ROST, has a great chance to capitalize on trade-down behavior in the current consumer climate. Especially as consumers continue to look for trendy branded goods at affordable prices. This movement was evident in ROST's 3Q23 performance , which saw 5% SSS growth due to traffic. Management noticed widespread momentum across geographies and income cohorts, indicating that customers were positively engaged with the value offerings of the company. Importantly, the sales trend has been fairly consistent throughout the quarter, suggesting the underlying demand behavior has not seen major changes yet.

I might be reading too much into management FY23 guidance, but it seems to hint that quarter-to-date trends continue to be stable as they reiterated SSS growth guidance at 1-2% for 4Q23. Also, if we adjust for the headwinds that management mentioned, it seems like like-for-like growth will be higher than the low-single digits guided. Some of the headwinds that were called out were:

- Tough y/y comparison. In my opinion, this is just optics, nothing to do with fundamentals. I would note that winter is expected to be much warmer this year and that Christmas falls on a Monday, both of which should drive additional traffic this year vs. last year.

- Promotional retail environment. This is a fair point, but it should impact all retailers given the festive season.

- Macroeconomic uncertainty. While I cannot forecast how the world is going to evolve, I would place my bets that consumers will continue to prefer value products (i.e., cheaper-priced goods) if the macro backdrop continues to stay at this level (high inflation and rates).

All in all, I am positive that ROST growth momentum can continue at a historical pace for the foreseeable future.

Gross margin to expand back to historical level

Historically, ROST has had pretty stable gross margins in the high 20%, but margins have deteriorated to mid-20% post-covid due to the freight situation. As we continue to move past the impacts of COVID and the world becomes more normalized, I see no reason for the ROST margin to not recover back to pre-COVID levels. Indeed, 3Q23 has shown that margin can expand and is not structurally impaired. Gross margin expanded 260bps to 27.6% (from 25% in 3Q22), primarily driven by increased merchandise margins benefiting from ocean freight tailwinds. I expect ROST merchandise margins to benefit from ocean freight in 4Q, albeit to a lesser extent vs. prior quarters as tailwinds moderate, along with ongoing decreases in distribution and domestic freight more than offsetting increased incentive compensation. Based on my management insights, ROST should be able to recapture almost all ocean freight headwinds relative to 2019 by FY23, which means FY24 is likely to see normalized gross margins. In fact, I think there is a good chance for gross margin to further improve if the labor environment improves, which should ease the ongoing pressures from higher trucking wages.

Balance sheet remains strong to support growth investments

ROST has a very strong balance sheet that can support continuous investment in Capex to drive store growth. As of 3Q23, the business has a cash position of $4.5 billion and a debt position of $2.5 billion (excluding operating leases), which translates to a net cash position of $2 billion. ROST has continuously generated positive FCF over the past decade, and even in the worst of times (subprime), ROST generated positive FCF. As such, I don't see any issues with ROST servicing its debt levels or paying them down if it needs to.

Valuation

{kind=link}

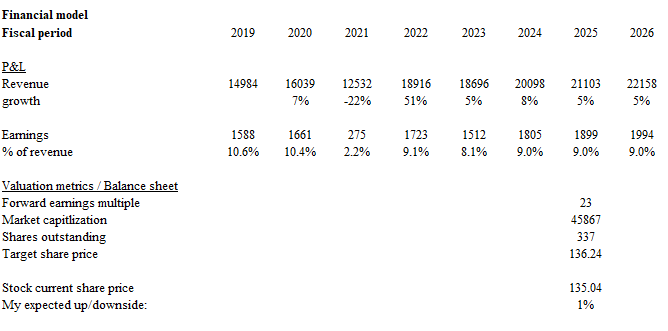

My model assumes FY24 to be a year of elevated growth (8%) as ROST continues to benefit from the trade-down impact. However, as the economy normalizes, ROST growth should revert back to its historical growth of mid-single digits. The same is for margins, which I expect to revert back to 9% (similar to the high single-digit range in the past). The issue I have with ROST is that the valuation appears to have priced in the next 3 years of growth. Valuation has also recovered back to its 5-year average of 23x, making the case for further valuation upside less convincing as there is no major catalyst in sight. At 23x, my target price is $136, which is close to the current price of $135. Even on a relative basis, ROST multiple is also where I think it should be, below BURL (26x forward PE) and in line with TJX (22x forward PE), given the expected growth rates. BURL is expected to grow faster at 10%, while TJX is expected to grow at similar rates to ROST.

Risk

The key risk is that the economy sees prolonged pressure on low-income consumers' spending power, which could bring down the overall industry growth potential as price declines outpace volume growth. In layman terms, the decline in average basket pricing could outweigh traffic growth, translating to declining sales growth.

Conclusion

I recommend a hold rating for ROST. With ample whitespace for store expansion, particularly in the Midwest and Northeast regions, ROST's growth seems promising. Moreover, the current macroeconomic climate favoring cost-conscious consumers presents a favorable environment for ROST's value offerings. Gross margins should also continue to rebound back to historical levels as the business showed signs of margin improvement in 3Q23. However, my concern lies in ROST's current valuation, which appears to have already priced in its projected growth. At a multiple of 23x, my target price aligns closely with the current market price.

For further details see:

Ross Stores: Great Business But Valuation Is Not Attractive