IAUX - Royal Gold: Penasquito Strike To Weigh On Q3 Sales

2023-08-07 06:14:16 ET

Summary

- Royal Gold released its Q2 results last week, reporting softer than expected results with lower revenue from Andacollo, Penasquito, and Mount Milligan offsetting full production from Khoemacau.

- While Penasquito stung a little in Q2, it's expected to sting more in Q3, with a strike ongoing which could result in an FY23 guidance miss for RGLD.

- We've seen multiple positive developments across the portfolio, and Royal Gold's diversification more than offsets some short-term noise from the Penasquito strike.

- While we could see an FY2023 guidance miss if Penasquito isn't restarted soon, I would view any weakness below US$109.25 resulting from this as a buying opportunity.

It's been a mixed Q2 Earnings Season for the Gold Miners Index ( GDX ) with the higher average realized gold price mostly being offset by higher operating costs and many producers suffering from one-time headwinds such as power outages, impacts from wildfires, and severe weather. In the case of the largest gold miner in the sector, Newmont ( NEM ), it was a tough quarter due to the June strike at Penasquito which has remained in place. However, this impact has been felt across several other names, with Wheaton PM ( WPM ) holding a silver stream at Penasquito, and Royal Gold ( RGLD ) holding a 2.0% NSR on all metals at this massive asset. Unfortunately, this has contributed to weaker Q2 results for RGLD, and dampened its FY2023 outlook with the potential it could miss guidance of 320,000 to 345,000 gold-equivalent ounces. Let's take a closer look below:

Penasquito Operations (Newmont Presentation)

{kind=link}

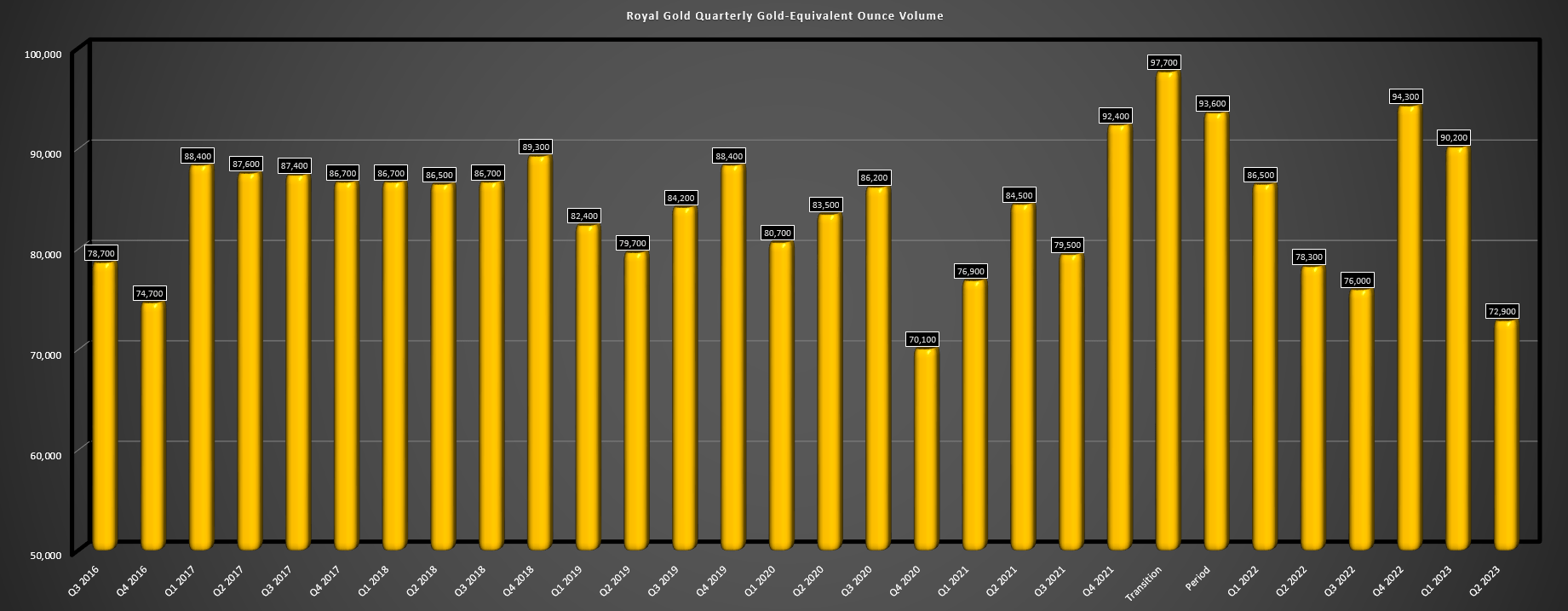

Q2 Results

Royal Gold released its Q2 results last week, reporting quarterly production of ~72,900 GEOs, its weakest quarter in over two years. The softer results were attributed to lower revenue at Mount Milligan, Voisey's Bay, Andacollo, Robinson, Marigold, Goldstrike, El Limon, Gwalia Deeps, and Penasquito, with the latter set to have an even weaker Q3 with the strike in place for nearly half of the current quarter without any resolution. Meanwhile, although Pueblo Viejo had a better quarter in Q2 2023 ($23.5 million vs. $19.8 million), the asset was lapping very easy year-over-year comps, and revenue was down ~15% on a two-year basis, with lower silver deliveries related to lower silver recovery which led to an 89,300 ounces of silver deliveries being deferred in the period. The result is that there are now over 607,000 ounces of silver that have been deferred, and while the Expansion Project to 14.0 million tonnes per annum is nearly complete, we could see a softer Q3 depending on the timing of deliveries at this asset as tie-ins and the finishing touches on the much-awaited expansion are completed.

Royal Gold Quarterly GEO Volume (Company Filings, Author's Chart)

{kind=link}

The good news is that the Pueblo Viejo Expansion once commissioned will provide a lift to attributable sales for Royal Gold, with the expansion set to result in annual production ( Pueblo Viejo 60% basis ) averaging ~540,000 ounces of gold from 2024 to 2027 and closer to 600,000 ounces next year. This should translate to upwards of 55,000 GEOs next year for Royal Gold attributable to this asset, a major step up from what we've seen in H1 2023 to date. And at other key assets, although Mount Milligan had a softer Q2 (~$41.2 million in attributable revenue vs. ~$45.6 million in Q2 2022) due to lower grades and recoveries (mine sequencing), the asset will benefit from higher grade copper and gold ore from Phase 7 and 9 in H2, helping Royal Gold to finish the year stronger at this asset depending on the timing of deliveries. That said, the one question mark remains Penasquito, where we will see a sharp drop in attributable revenue in Q3 vs. the $9.0 million reported in Q3 2022 unless the strike is ended immediately.

Pueblo Viejo Operations (Company Presentation)

{kind=link}

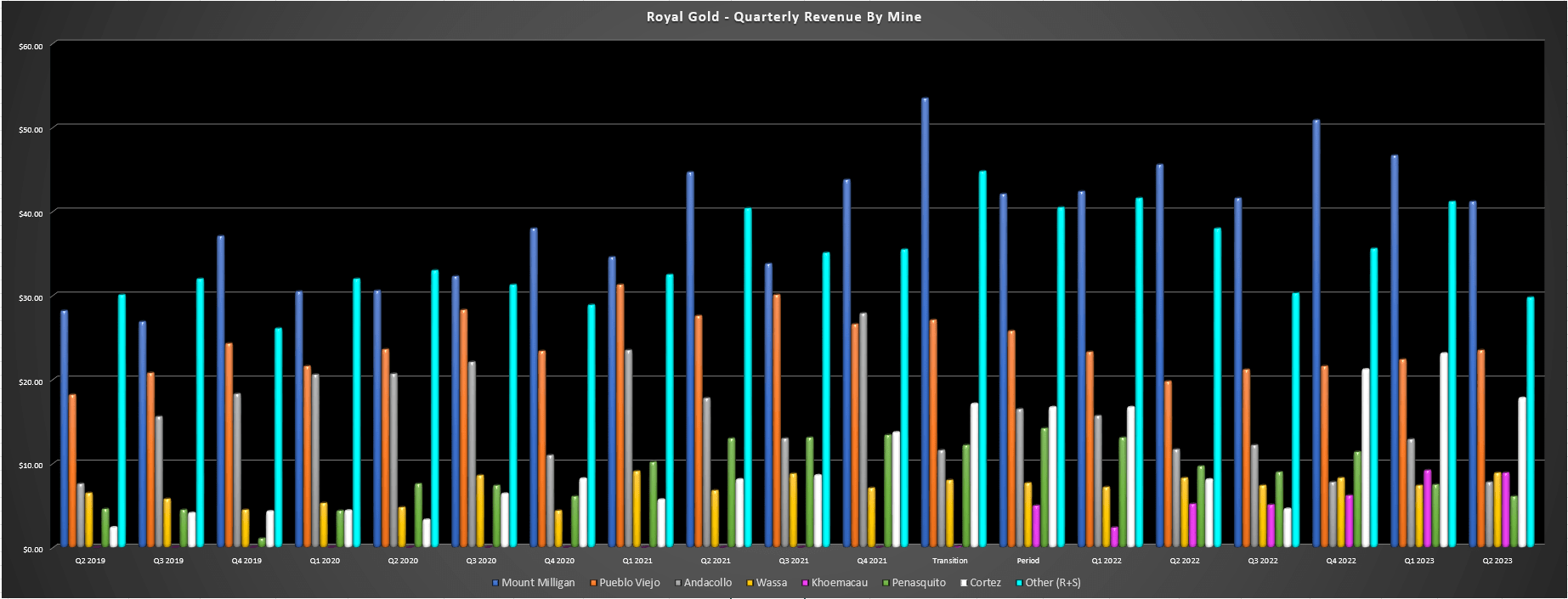

On a positive note, the ounces are staying in the ground at Penasquito and are simply deferred, a resolution is likely even if it drags on and creates some noise in Royal Gold's short-term results, and the company did see some assets help to pick up slack in Q2. This included higher revenue from Rainy River where the transition to underground is progressing well, higher revenue from Pueblo Viejo despite a soft start to the year with a focus on tie-ins and commissioning for the massive PV Expansion, higher revenue from Wharf and Khoemacau, with the latter ramping up to full production earlier this year, and higher contributions from Cortez ($17.8 million total) with increased revenue from the Legacy Zone and new contributions from the CC Zone. Finally, while a small asset, King of the Hills contributed ~$1.1 million in revenue from its 1.5% NSR with the start of commercial production just over six months ago vs. no contribution in the year-ago period.

Royal Gold - Quarterly Revenue by Mine (Company Filings, Author's Chart)

{kind=link}

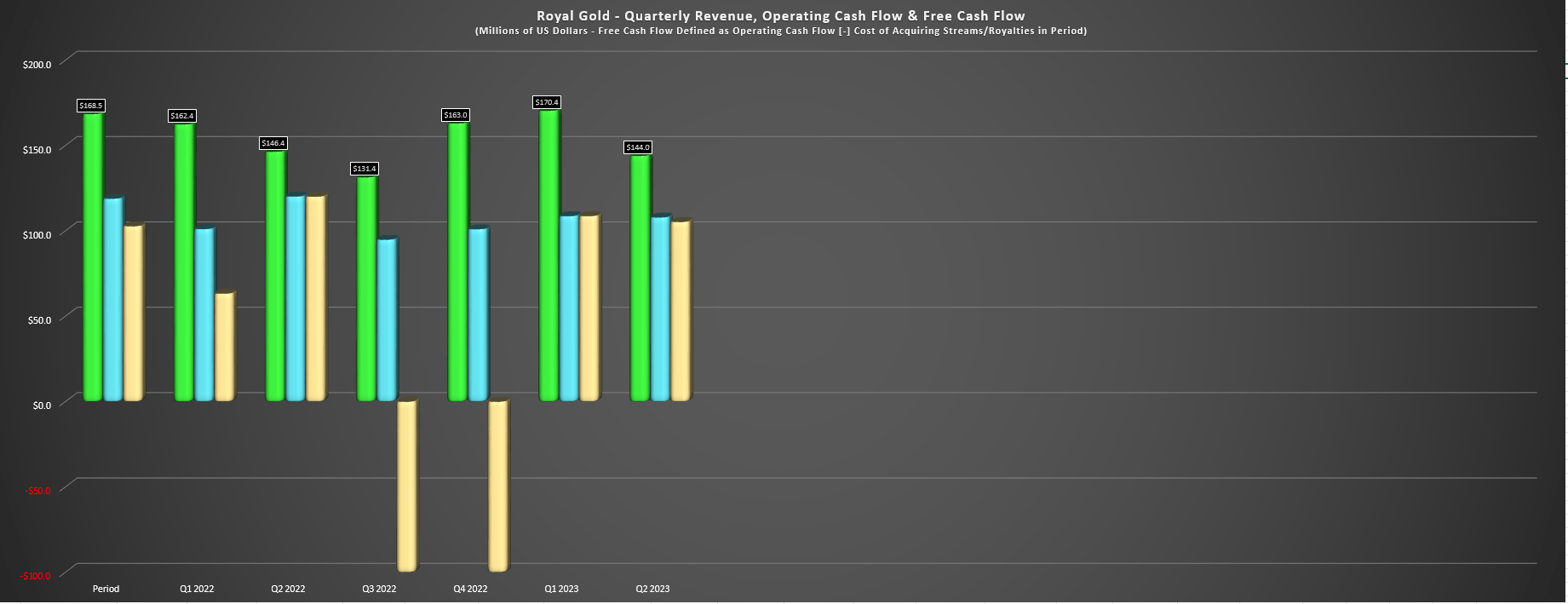

Looking at Royal Gold's financial results, the company also got some help from higher average realized gold and silver prices that offset the pullback in copper prices, with an average gold and silver of $1,976/oz and $24.13/oz in the period, respectively. This increase in precious metals prices partially offset the lower GEO volume, but Royal Gold still saw decline in revenue to $144.0 million (Q2 2022: $146.4 million), a disappointing result given the significant increase in royalty exposure to Cortez. That said, several growth opportunities at Cortez have yet to kick in, with the Goldrush Record of Decision expected by year-end at this massive high-grade project, and the potential for Robertson and Fourmile to contribute by 2028 and 2030, respectively. This should translate to meaningful growth at Cortez, and I'll discuss later, there appears to be material elsewhere in Nevada later this decade.

Royal Gold - Revenue, Operating Cash Flow & Free Cash Flow (Company Filings, Author's Chart)

{kind=link}

Finally, if we look at Royal Gold's operating cash flow and free cash flow, these came in at $107.9 million (down 10% year-over-year), while free cash flow fell to $105.3 million. That said, Royal Gold still finished the quarter with over $700 million in liquidity ($102 million in working capital and $600 million on RCF) after making a $100 million payment on its RCF balance, placing the company in a position to take advantage of sector-wide weakness and continuing growing with debt and cash flow to further improve its per share metrics. And this is despite a busy two years from an acquisition standpoint. So, assuming the new deal in Brazil goes through on the producing Serrote (GSR on 85% of payable gold until $250 million in revenue and 45% thereafter) and Santa Rita (GSR of 64 ounces of gold, 135 ounces of platinum and 100 ounces of palladium per 1 million pounds of payable nickel production with step downs), Royal Gold will still be in a healthy financial position to complete mid-sized deals over the next 12 months.

In addition to the gold, platinum, and palladium royalties, Royal Gold will pay $35 million for a 0.50% GSR on payable copper and nickel at a rate of 0.5)% for 2023 and 2024, 0.75% during 2025, 1.1% thereafter, and then a step down to 0.55% after a revenue threshold of $90 million is reached.

Recent Developments

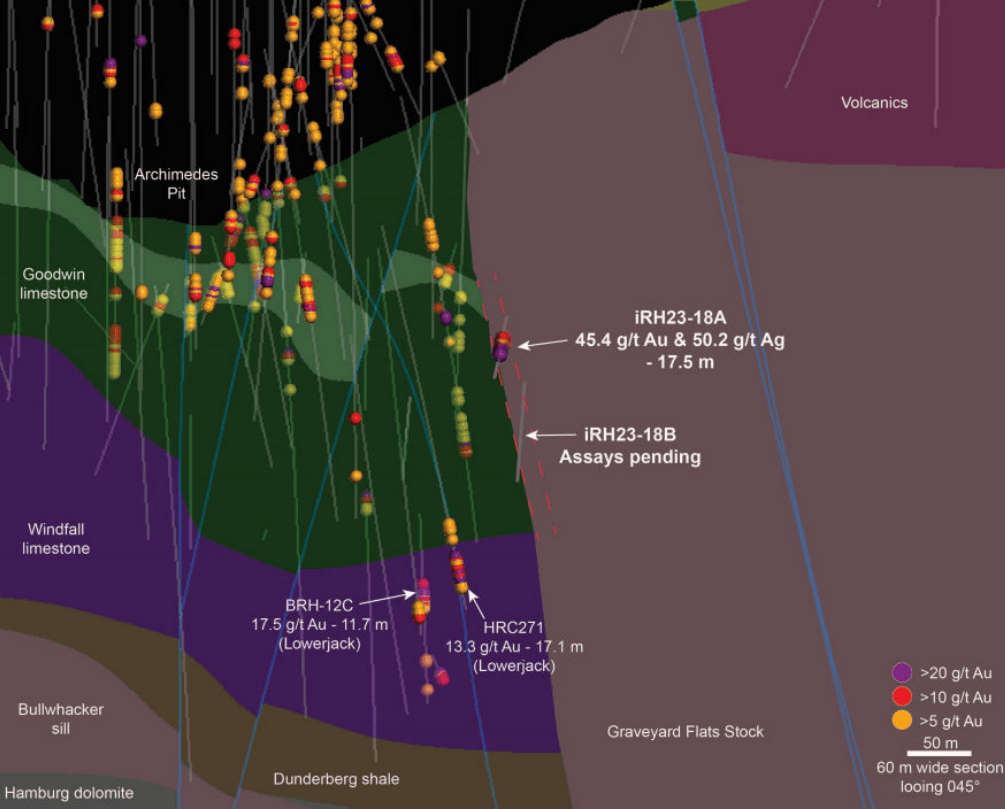

Moving over to recent developments, there have been several, but one of the most recent ones comes from Nevada. For those unfamiliar, Royal Gold holds a 3.0% NSR on all metals at i-80 Gold's ( IAUX ) Ruby Hill Project near Eureka, but this was a sleeper asset that didn't get any airtime since Watertown acquired it in 2015 and sat on it for years. However, since i-80 Gold has begun exploration here, we've seen multiple new gold and polymetallic discoveries, with the seventh made last week in a span of just 18 months. And while all of these discoveries have been quite impressive and point to significant resource growth at this asset and the potential for a 13.0+ million ounce resource base property-wide (Mineral Point, Hilltop, Blackjack, Ruby Deeps/426 and new zones), the most recent discovery is arguably the most exciting, with i-80 Gold announcing one of the best intercepts drilled in Nevada in the past three years last week.

i-80 Gold - New Tyche Zone Discovery (Company Website)

{kind=link}

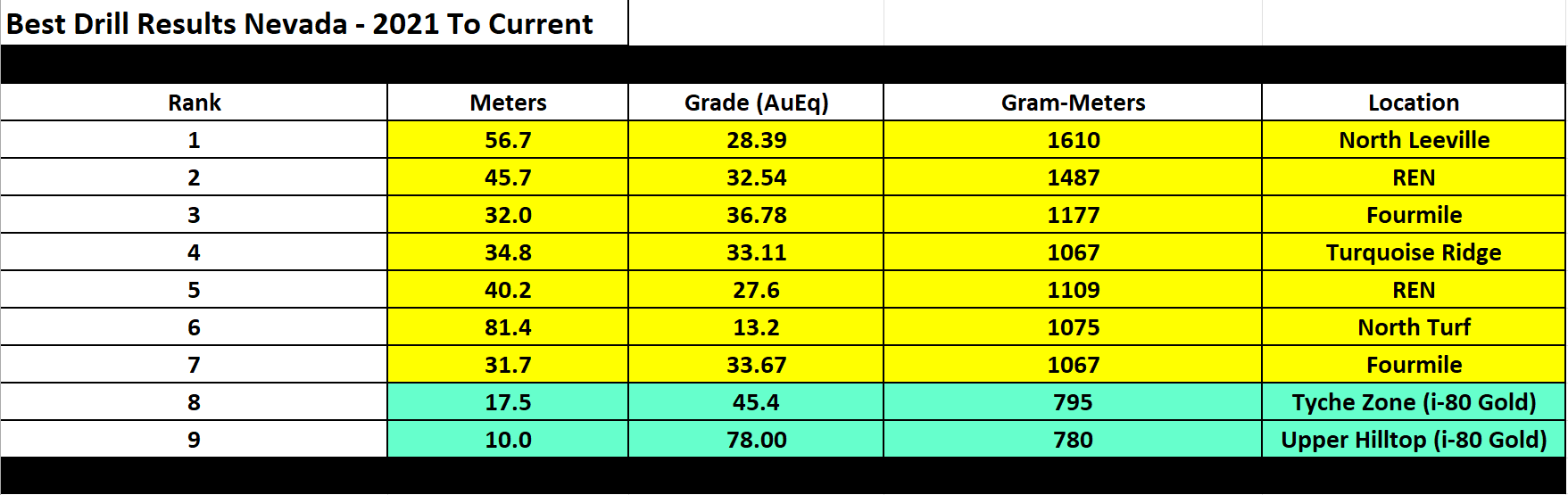

As shown above, i-80 Gold's drill hole iRH23-18A was drilled just east of its skarn deposit (Blackjack) at Ruby Hill in the Graveyard Flats Stock in what is the first intercept of this style of mineralization on the property. The grades were off the charts with 17.5 meters at 45.4 grams per ton of gold and 50.2 grams per ton of silver (46.1 grams per ton gold-equivalent), translating to 800+ gram-meters and beat out its previous best hole of ~780 gram-meters when it hit 10.0 meters of 60.2 grams per ton of gold, 908 grams per ton of silver and 16.8% lead and zinc. To put these intercepts in context, these are now the #8 and #9 ranked intercepts drilled in Nevada over the past 30 months, and they are only behind that of Nevada Gold Mines, a joint-venture between the two largest gold companies in the world that own multiple mining complexes with a combined resource base (reserves, measured, indicated, and inferred ounces) of ~100 million ounces of gold.

Best Drill Results In Nevada Ranked (2021 To Current) (Company Filings, Author's Table)

{kind=link}

The fact that i-80 Gold has hit two of the best intercepts Nevada-wide in the past 30 months is even more impressive given that it has a modest exploration budget relative to Nevada Gold Mines, and with multiple discoveries that include Upper Hilltop, Lower Hilltop, East Hilltop (carbonate replacement mineralization), and more recent discoveries of the 428 and Tyche zones (high-grade sulfide gold), this is certainly an asset that could become a meaningful contributor for Royal Gold long-term, with the potential for ~250,000 GEOs per annum of production property-wide post-2028 or 400,000+ ounces with longer-term optionality from Mineral Point. Hence, I see this new discovery as very positive for i-80 Gold but also the royalty holder at Ruby Hill, Royal Gold, that holds a large royalty on the asset that was collecting dust in its portfolio and is now finally beginning to surface some value.

{kind=link}

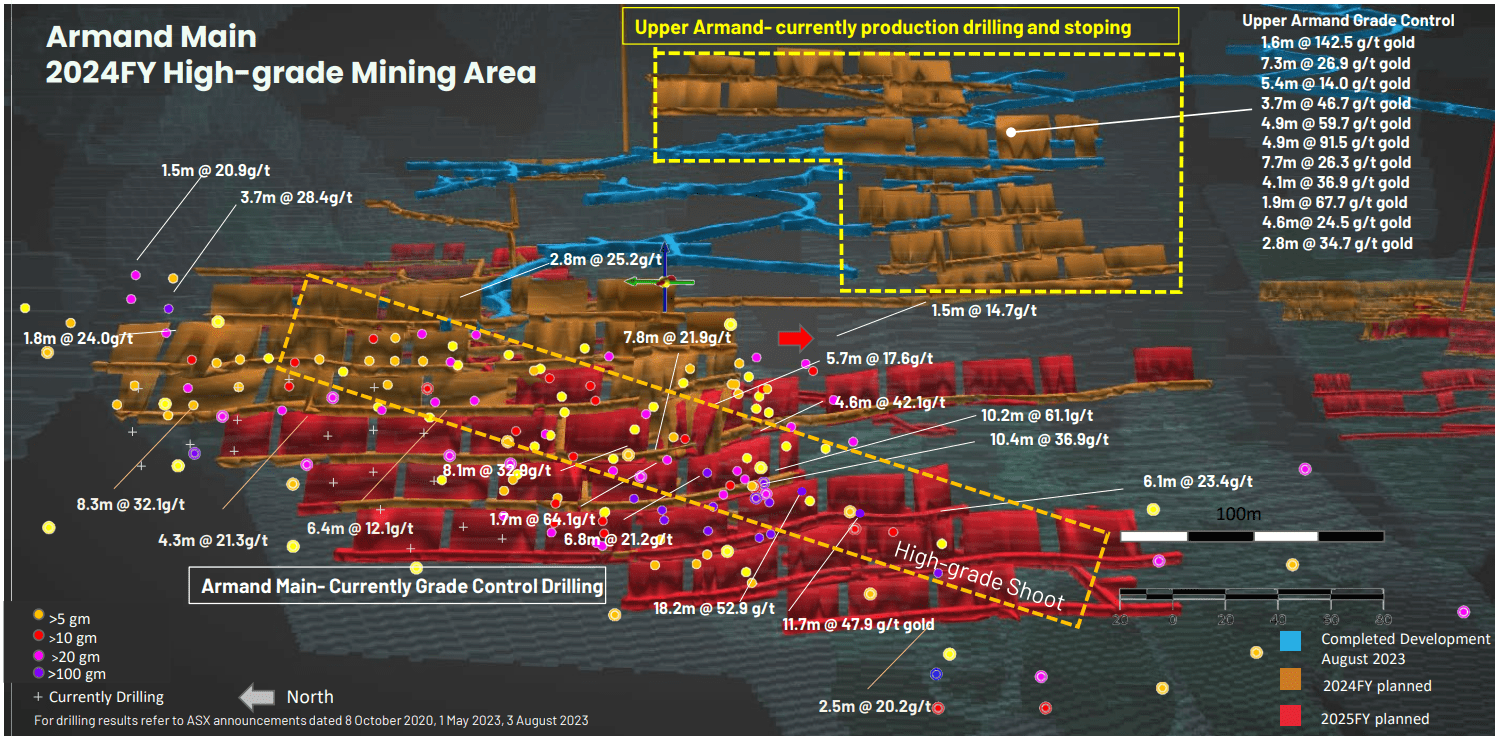

And speaking of high-grade projects, Bellevue Gold's ( OTCPK:BELGF ) Bellevue Gold Project is nearing the finish line, with first production expected by year-end. In addition, the company continues to release incredible infill drilling intercepts with recent drill highlights, with a sample of these including:

- 18.4 meters at 52.9 grams per tonne of gold

- 10.2 meters at 61.1 grams per tonne of gold

- 10.4 meters at 36.9 grams per tonne of gold

In addition, Bellevue is delineating a new easterly dipping discovery outside of the Armand Main resource, with a highlight intercept of 5.7 meters at 36.3 grams per tonne of gold. These hits are well above the average reserve grade at Bellevue of 6.1 grams per tonne of gold, suggesting the potential for positive grade reconciliation like we've seen in other high-grade assets in Australia (Fosterville) and potential resource expansion at better grades, with grade control drilling showing positive grade reconciliation with the block model to date. For those unfamiliar, Royal Gold holds a 2.0% NSR at Bellevue with the asset expected to produce ~160,000 ounces on average in its first five years, translating to annual revenue of ~$3.0 million to Royal Gold. However, assuming half a gram per tonne of positive reconciliation relative to reserve grades, production would increase by ~11,500 ounces for Bellevue, or the equivalent of an additional ~$440,000 to Royal Gold per year at a $1,900/oz gold price assumption.

{kind=link}

Elsewhere, solid progress continues to be made at the Goose Project in Nunavut (Royal Gold: 1.95% GSR above 400,000 GEOs), with the updated outlook being mill completion in Q1 2025, with first five-year production averaging 300,000 ounces. And in Ontario at Cote Gold (Royal Gold: 1.0% NSR), commercial production is set to begin next year with this asset also being a significant contributor in a Tier-1 ranked jurisdiction (490,000+ ounces per annum in the first six years). Finally, Mara Rosa is also progressing well in Brazil, and while it's a smaller asset than the former two, Royal Gold holds a 1.0% NSR royalty and a 1.75% NSR royalty on gold on Hochschild's ( OTCQX:HCHDF ) new mine, making this a solid contributor as well, with first production expected in H1 2024.

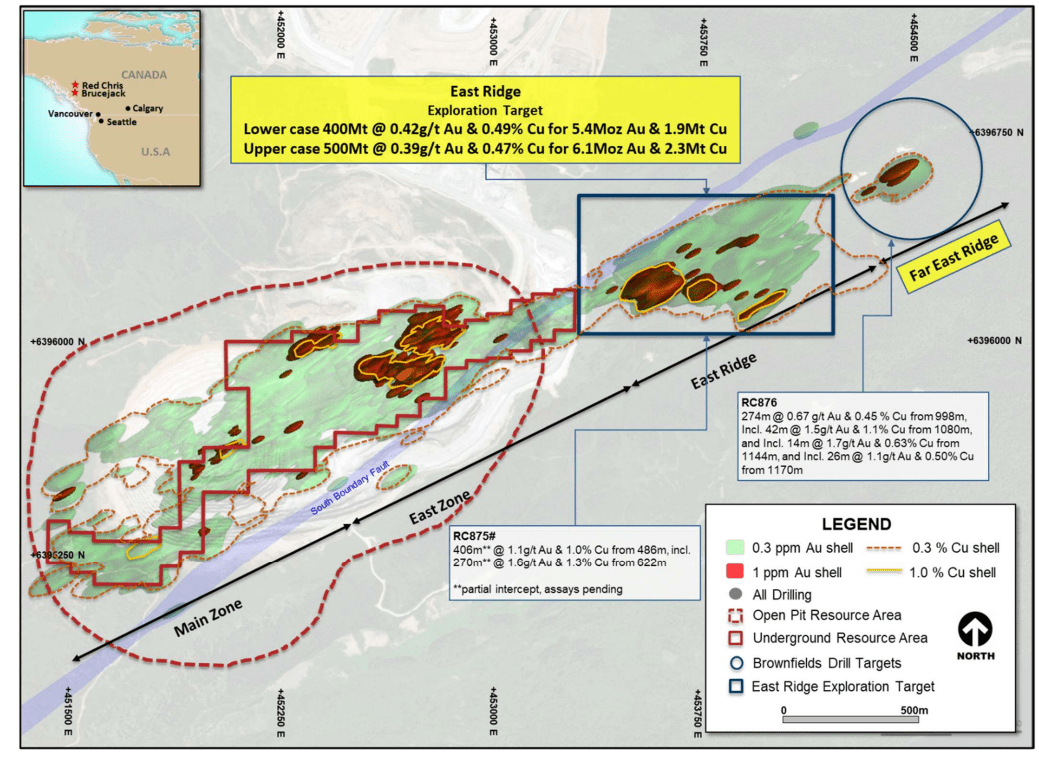

Lastly, I'd be remiss not to briefly discuss East Ridge at the Red Chris Mine in British Columbia, with Royal Gold holding a 1.0% NSR on all metals at Red Chris. As shown below, the East Ridge Exploration target (separate from resources and reserves) has been increased to ~500 million tonnes at 0.39 grams per tonne of gold and 0.47% copper or 6.1 million ounces of gold 2.3 million tonnes of copper. This is a massive upgrade from ~300 million tonnes at 0.40 grams per tonne of gold and 0.40% copper last year. Plus, if we compare this potential resource to the current M&I resource base at Red Chris of ~12 million ounces of gold and ~3.5 million tonnes of copper, this would significantly increase Red Chris' resource base at similar gold grades but higher copper grades, with a current resource grade of ~0.42 grams per tonne of gold and ~0.39% copper.

Red Chris Drilling Highlights & East Ridge (Company Presentation)

{kind=link}

And the upgrade to tonnes in the exploration target is certainly positive, the even more exciting news is that Newcrest ( OTCPK:NCMGF ) stated that it has "confirmed continuity of the higher-grade mineralization across the vertical extent of the deposit" at the East Ridge Exploration Target. As highlighted in its Q2 report, a partial intercept in drill hole 875 hit 406 meters at 1.1 grams per tonne of gold and 1.0% copper from 486 meters, with grades well above its current reserve grades and East Ridge Exploration Target grades. Meanwhile, drilling at Far East Ridge (a new discovery) intersected 274 meters at 0.67 grams per tonne of gold and 0.45% copper, opening up the potential for a fifth porphyry center along the Red Chris Corridor. This intercept was drilled 100 meters east of hole 860 which hit 66 meters at 0.53 grams per tonne of gold and 0.46% copper, a meaningful step-out that has confirmed elevated grades east of East Ridge. So, with East Ridge open to the east and at depth and a 30+ year mine life even without East Ridge or Far East Ridge, this is certainly looking like a brilliant acquisition by Royal Gold for $165 million, with the potential for it to produce into the 2060s.

To summarize, while Royal Gold may have a softer quarter in Q2 relative to expectations because of factors outside of its control, the company certainly has an impressive development pipeline that will contribute from 2024 through the end of the decade, with several of these contributors set to be high-grade assets in Tier-1 ranked jurisdictions, which could contribute to a higher multiple for Royal Gold. Hence, with Royal Gold having its tentacles in several of the highest-grade opportunities sector-wide and certainly having significant exposure to the best discoveries of the past decade in Nevada (Hilltop, Goldrush, Fourmile, South Pacific Zone, Tyche?), Royal Gold is certainly one of the best ways to get exposure to the gold sector with discovery optionality whole benefiting from the low risk of the royalty/streaming model.

Valuation

Based on ~66 million fully diluted shares and a share price of $113.40, Royal Gold trades at a market cap of ~$7.48 billion and an enterprise value of ~$7.77 billion. This is down from a peak market cap of ~$9.76 billion earlier this year ahead of the strike announcement at Penasquito and the pullback we've seen in precious metals and copper prices since April. From a valuation standpoint, this has left Royal Gold trading at just ~17.5x conservative FY2023 cash flow per share estimates of $6.50, a discount to its historical multiple of ~21.8x cash flow (15-year average). And if we apply what I believe to be a premium multiple of 24.0x cash flow given its increased scale, diversification, and addition of several world-class and long-life Tier-1 jurisdiction royalties (Red Chris, increased exposure to Cortez, Great Bear, Cote Gold), this translates to a fair value for RGLD of $156.00 - 38% upside from current levels.

{kind=link}

While this is an attractive upside case and investors get exposure to a consistent dividend grower by owning RGLD (22 consecutive years of dividend increases), I prefer a minimum 30% discount to fair value to justify starting new positions. If we apply this discount to Royal Gold's conservative fair value estimate of $156.00, this translates to an ideal buy zone of $109.25 or lower, suggesting RGLD has yet to dip into a low-risk buy zone despite its recent sharp correction. So, while I see Royal Gold as a sleep well at night sector leader that offers exposure to gold, silver, and copper without the headaches that can come with some producers, I remain on the sidelines for now unless we see a deeper correction materialize.

Summary

Royal Gold had a softer Q2 than I anticipated with a softer quarter from Mount Milligan and Pueblo Viejo and the surprise strike at the massive Penasquito Mine in Zacatecas, Mexico. And with the Penasquito strike still not seeing a resolution, it's not clear whether the company will meet its FY2023 guidance. That said, Royal Gold continues to operate business as usual, has multiple bought and paid for irons in the fire (exploration/development pipeline) that will provide further diversification and growth in the coming years. Just as importantly, many of these assets sit in Tier-1 jurisdictions in a sector where jurisdiction is becoming even more important, and several of them are among the best discoveries and assets sector-wide. So, while we have seen some short-term turbulence in RGLD's share price and the possibility of a miss in FY2023, the stock is finally approaching another low-risk buy zone below US$109.25 if its weakness persists.

For further details see:

Royal Gold: Penasquito Strike To Weigh On Q3 Sales