RPAR - RPAR: Should Likely Perform Well In A Recessionary Environment

2023-05-03 07:41:23 ET

Summary

- The RPAR ETF is a convenient way to access risk-parity strategies.

- The RPAR ETF's design was flawed, as it had a heavy weight in TIPS bonds that was expected to go up in inflationary environments.

- Instead, TIPS bonds were the worst performing asset class in 2022 as inflation soared due to the bonds' duration risk.

- Going forward, I believe the RPAR ETF should do well in a recessionary environment as expectations for interest rate cuts build due to the fund's heavy bond exposures.

The RPAR Risk Parity ETF ( RPAR ) applies risk-parity concepts to construct a portfolio that is expected to perform well in all economic scenarios. Unfortunately, the fund placed a heavy weight in TIPS bonds, which failed to protect the fund during 2022's inflation episode.

Despite my misgivings on the strategy's design, I believe the current portfolio allocation should do well if the economy falls into a recession/stagflation, as expectations build for interest rate cuts which should benefit the fund's heavy fixed income allocations.

Fund Overview

The RPAR Risk Parity ETF gives retail investors access to risk-parity strategies in a liquid ETF structure. The RPAR has over $1 billion in net assets and charges a reasonable 0.51% net expense ratio.

Strategy

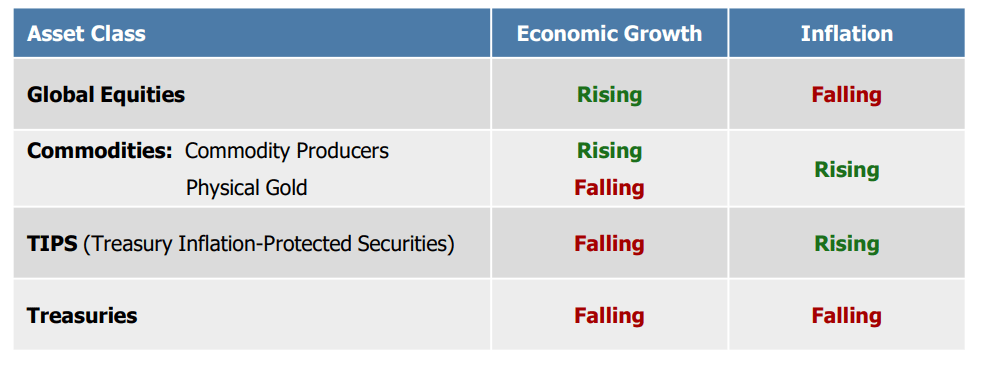

Whenever I hear 'risk-parity' I am always reminded of Ray Dalio and Bridgewater , one of the pioneers of 'risk-parity' investing. The basic idea behind 'risk-parity' is to design a portfolio with various assets that will work in different economic scenarios. For example, RPAR chooses to invest in 4 asset classes: Global Equities, Commodities, TIPS, and Treasuries with different performance profiles shown in Figure 1.

Figure 1 - RPAR invests in diversified asset classes (RPAR investor presentation)

{kind=link}

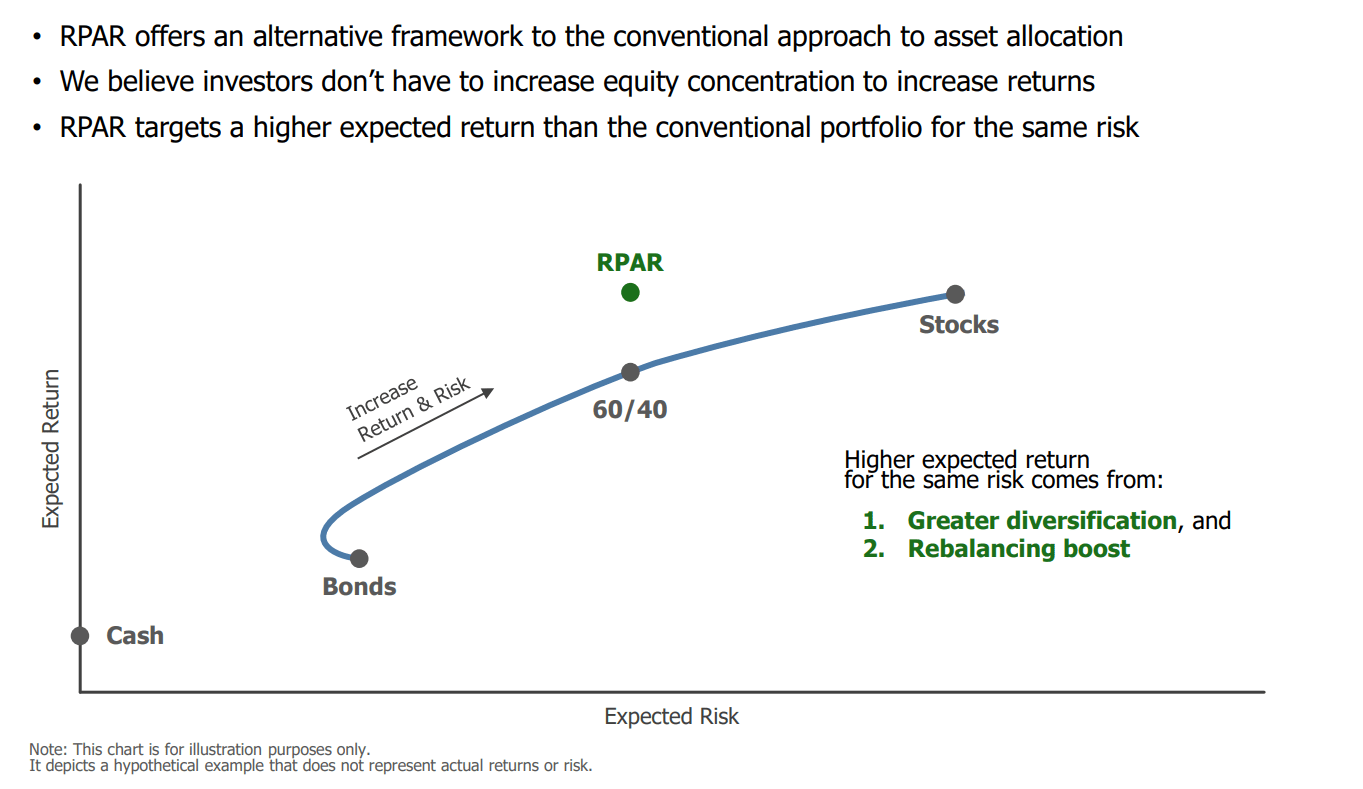

In combination, the manager believe these asset classes will produce returns similar to equities, but with lower expected risk (Figure 2).

Figure 2 - Manager believes combined portfolio will producer returns similar to equities but with lower risk (RPAR investor presentation)

{kind=link}

Portfolio Holdings

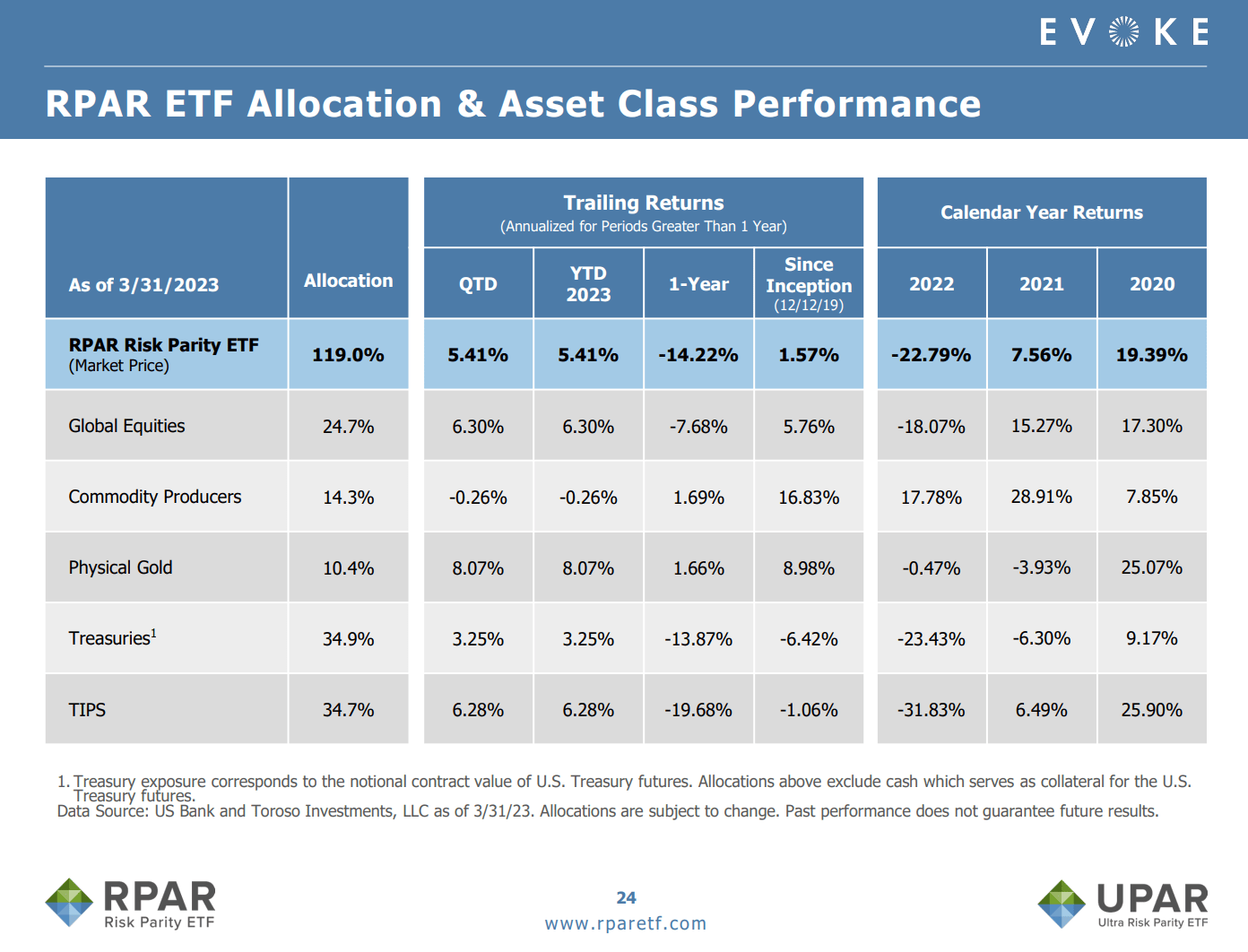

Figure 3 shows the RPAR ETF's asset class allocation as of March 31, 2023. The fund is currently 25% invested in global equities, 25% invested in commodities (14% commodity producers and 10% gold), 35% in treasuries, and 35% in TIPS.

Figure 3 - RPAR current allocation and historical returns (RPAR investor presentation)

{kind=link}

Distribution & Yield

The RPAR ETF pays a modest quarterly distribution with trailing 12 month distribution of $0.69 or 3.6% (Figure 4).

Figure 4 - RPAR pays a modest distribution yield distribution (Seeking Alpha)

{kind=link}

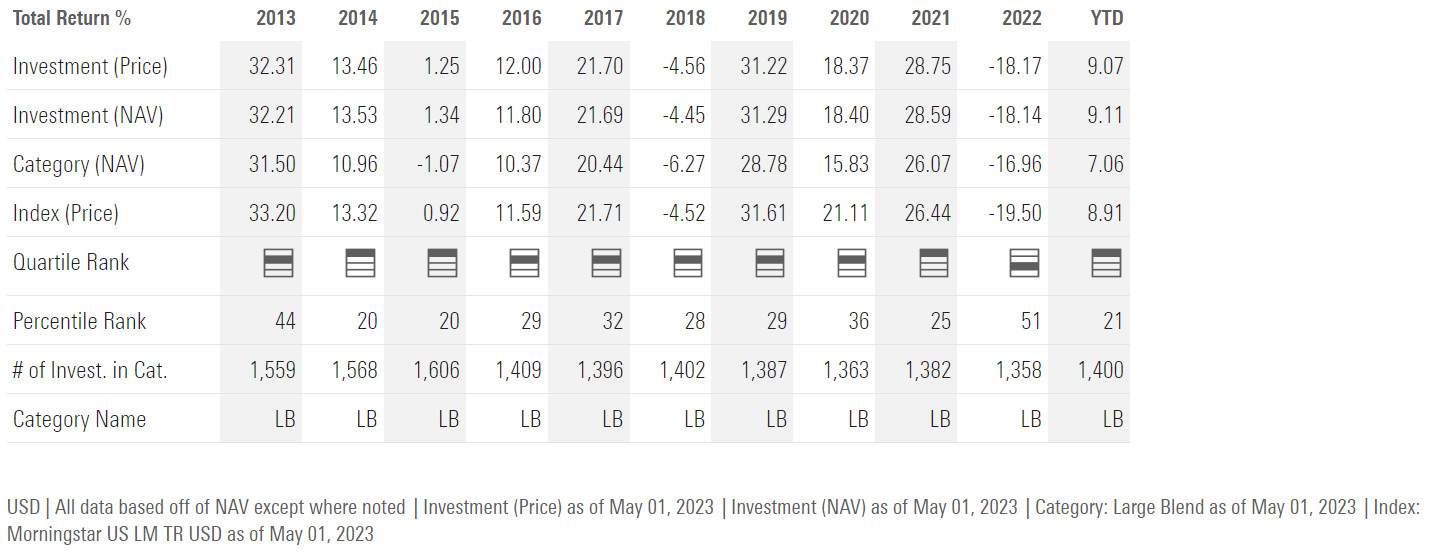

Returns Have Been Disappointing

While the RPAR ETF has a great marketing pitch , the actual performance for the fund has been disappointing since its launch in late 2019. As seen from figure 3 above, the fund had a good 2020, returning 19.4%, but 2021 returns were modest at 7.6%, and 2022 returns were abysmal at -22.8%.

Since RPAR is marketed as having equity-like performance with lower risk, I believe a fair comparison would be against the SPDR S&P 500 ETF Trust ( SPY ), whose annual returns are shown in Figure 5.

{kind=link}

Notice in 2020, RPAR delivered roughly similar returns to SPY; however, 2021 was a huge underperformer (7.6% vs. 28.6% for SPY), and RPAR lagged in 2022 as well (-22.8% vs. -18.1%).

Rate Tightening Caused Underperformance

According to RPAR's marketing materials, RPAR's poor performance in 2022 was due to the Federal Reserve aggressively tightening monetary policy to fight inflation.

"A material tightening versus expectations poses a headwind for all assets at the same time because they all compete with the risk-free yield ? When the risk-free yield suddenly becomes more attractive, all assets reprice lower to offer a higher forward-looking return so their expected return above the risk-free yield is competitive ? This is why both stocks and bonds experienced major declines at the same time."

While the statement above is factually correct, it sounds like the manager was trying to explain why their black box did not work as intended rather than offering any insight.

I believe the key weakness of the strategy's design was the heavy weight towards TIPS bonds. Recall from figure 1, RPAR's strategy expects TIPS bonds to rise during inflationary environments. In fact, we know from figure 3 above that TIPS bonds was the worst asset class in 2022 when inflation was soaring, declining by 31.8%.

TIPS Bonds Have Duration Risk

Treasury Inflation-Protected Securities ("TIPS") are bonds issued by the U.S. Treasury Department that provide protection against inflation. The principal of a TIPS bond increases with inflation as measured by the Consumer Price Index ("CPI"), and decreases with deflation. When a TIPS bond matures, investors are paid the greater of the adjusted principal or original principal.

TIPS bonds also pay fixed rate bi-annual interest that is calculated on the adjusted principal, so the interest payments increase with inflation.

While an individual TIPS bond protects the bondholder from inflation with adjustments to their principal and interest payments, that is not necessarily true for portfolios of TIPS bonds.

In fact, as I have detailed in numerous articles regarding TIPS ETFs like the Schwab U.S. TIPS ETF ( SCHP ), portfolios of TIPS bonds, being fixed income instruments, have duration risk. So it was naive for the manager to expect TIPS bonds to benefit from inflation without expecting a response from the Fed in terms of interest rate increases that would negatively impact TIPS bonds due to duration.

What Is RPAR's Outlook?

Putting aside my misgivings on the strategy's design, what do I think about RPAR's prospects now given my views on the macro-economic environment?

My current view is that the global economy is headed for a recession/stagflation. For example, the recently released Q1/2023 GDP report showed real GDP grew at only 1.1%, below analysts' 2.0% estimate (Figure 6).

Figure 6 - Real GDP for Q1/23 was 1.1% (BEA)

Combined with core Personal Consumption Expenditures ("PCE") inflation averaging 4.6% in Q1, one gets the picture that the U.S. economy is in a serious bout of 'stagflation'. In fact, the Fed's own staff economists are projecting "a mild recession starting later this year, with a recovery over the subsequent two years," as they wrote in the FOMC Minutes.

Referring back to figure 1, in a period of low to negative economic growth and high inflation, Global equities should perform poorly. Commodity producers should do poorly as well, as they are equities at the end of the day. Gold should do well as expectations for interest rate cuts start to build, as should Treasuries and TIPS. Given Gold/Treasuries/TIPS account for 80% of net assets, I believe the RPAR ETF should do well in the environment I envision (Figure 7).

Figure 7 - RPAR should do well in a bad economy (RPAR investor presentation)

{kind=link}

Risk To RPAR

The biggest risk to RPAR is if I am wrong on the macroeconomic outlook and the economy actually muddles along while the Fed continues to keep interest rates 'higher for longer'. If that were the case, we could see another year of poor performance from the fixed income allocations, which could weigh on overall portfolio returns.

Conclusion

The RPAR ETF applies risk-parity concepts to construct a portfolio that is expected to perform well in all economic scenarios. Unfortunately, the fund placed a heavy weight in TIPS bonds, which failed to protect the fund during 2022's inflation episode.

Despite my misgivings on the strategy's design, I believe the portfolio allocations should do well if the economy falls into a recession/stagflation, as expectations build for interest rate cuts.

For further details see:

RPAR: Should Likely Perform Well In A Recessionary Environment