SAFRY - RTX Stock: A Buy After Post-Earnings Rally

2023-11-22 12:06:56 ET

Summary

- RTX Corporation stock gained more than 8% since September, with changes to shareholder returns.

- The GTF turbofan program is facing difficulties, but the long-term value is expected to be significant.

- Collins Aerospace and Pratt & Whitney segments performed well, while the Raytheon segment had lower sales growth.

- The company has a massive backlog with positive demand trends in its end markets.

In September 2023, I analyzed RTX Corporation ( RTX ) stock and marked the stock a buy based on the significant plunge in stock price, which I believed was not proportionate to the issues faced on the GTF turbofan program. Indeed, the program is facing significant difficulties which will ground on average 350 airplanes per year through 2026. However, for the longer term, I believe this program will be a significant value driver for RTX due to a growing installed base and continued servicing required for engines which tend to have an escalating pricing nature for spare parts. Since my report in September, the stock has gained more than 8% with some changes to shareholder returns, and in this report, I will be discussing what this does to the valuation of the company as well as a brief look at the earnings to start.

A Brief Discussion Of RTX Geared Turbofan Costs

{kind=link}

In my previous report, I already did a sanity calculation to assess whether the revenue charge and cost charge were excessive because that's what was suggested. Back then my calculations showed that for the additional engines that were brought under the scope of inspection costs were not excessive.

| Estimate and recognized charges for GTF Turbofan Issue in $ millions |

| Year |

| Previous |

| New |

| Change |

| Change [%] |

| 2023 |

| $ 12,934 |

| $ 12,605 |

| $ -329 |

| -2.5% |

| 2024 |

| $ 14,155 |

| $ 13,696 |

| $ -459 |

| -3.2% |

| 2025 |

| $ 15,217 |

| $ 14,954 |

| $ -263 |

| -1.7% |

| Total |

| $ 29,372 |

| $ 28,650 |

| $ -722 |

| -2.5% |

In total, there's an expected pressure of 2.5% related to accrual expenses for the GTF program and the divestments based on analyst expectations compared to my previous expectations.

Changes to Free Cash Flow Estimates:

| Changes to FCF in $ millions |

| Year |

| Previous |

| New |

| Change |

| Change [%] |

| 2023 |

| 4284 |

| 4728 |

| $ 444 |

| 10.4% |

| 2024 |

| 5362 |

| 5253 |

| $ -109 |

| -2.0% |

| 2025 |

| 6894 |

| 6997 |

| $ 103 |

| 1.5% |

| Total |

| $ 12,256.0 |

| $ 12,250.0 |

| $ -6 |

| 0.0% |

Compared to the previous expectations. There is some variability in free cash flow per year, but overall my initial expectations fetch rather well with updated analyst estimates.

Perhaps a more prominent change to the valuation that could possibly offset any positive impact from the share repurchase program is the fact that we have upgraded the stock valuation tool that now more accurately follows cash flows.

{kind=link}

For those who followed my previous valuation of RTX Corporation stock, you might notice that despite the $10 billion share repurchase program the price target has not moved much. In fact, the stock price is roughly a dollar lower which I would attribute to the share repurchases being financed with debt and the stock valuation tool more accurately describing the cash flows. Beyond that, I foresee additional borrowing needs in the years to come.

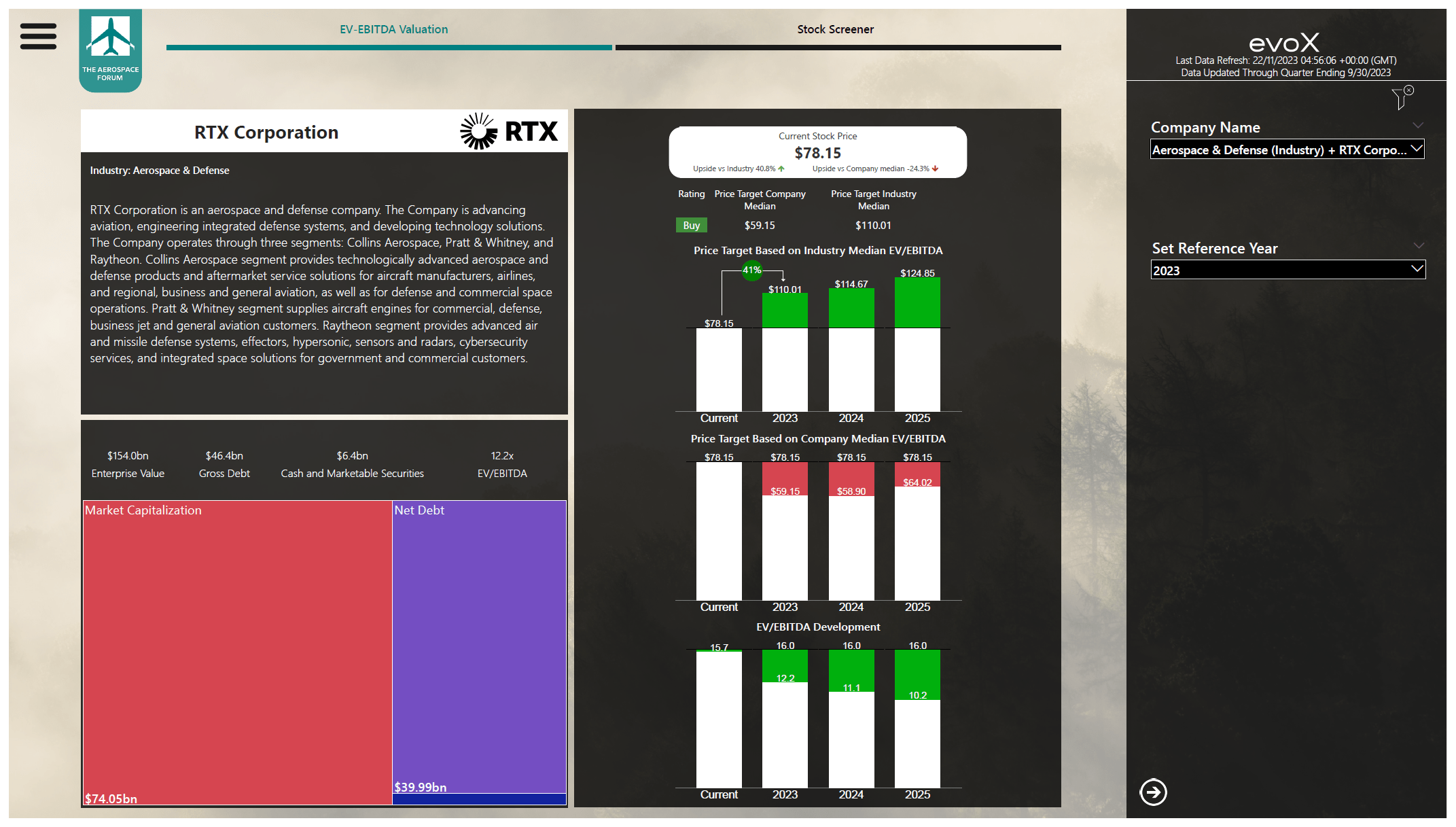

That, however, does not mean that I'm less optimistic about the stock. Valued in line with its peers there's 41% upside to $110 which closely coincides with the high target that Wall Street analysts have for the stock. As mentioned in my previous report, I'm not convinced that a 16x EV/EBITDA valuation that I use for aerospace and defense stocks is fully justified for a company that's going through its fair share of problems. At the same time, the 8.05x EV/EBITDA valuation is very low. Things are bad for RTX, but not that bad that we should value it in line with airlines. The company simply holds too many positive elements for that. So, using a multiple expansion that will close 50% of the valuation gap between the targeted industry multiple and the company median EV/EBITDA, I get to a $82.67 price target representing 5.7% upside. Generally, I'm looking for upside of at least 10%. However, I do believe that the longer-term trends warrant a buy and the automatically generated rating in the screenshot of the valuation tool is in agreement on that. The reason why I personally think the company is a buy is that the current repurchases, although financed with debt, allow for even better shareholder returns in the form of dividends, and once the company has sorted its issues and perhaps if a bull market of some sort we could see RTX trade closer to peers which would unlock double-digit upside from current levels. So, there are many moving items to be positive about.

Conclusion: RTX Stock Remains A Buy For Me

The GTF issues are of course ugly for RTX and it hurts the credibility of the platform and business, but the cost and sales charges have already occurred, and from here on we will see the cash flow pressures materialize but even with those cash flow pressures there's significant upside as the company's median EV/EBITDA is out of line with that of peers, and I think it insufficiently appreciates the long-term trends and demand drivers active in the end markets for RTX Corporation. So, by focusing too much on the near-term pressures and the pressures on the GTF program investors might be missing a golden opportunity. That's not to say that RTX is performing flawlessly because the Raytheon segment results in Q3 2023 for instance were not great, but the company overall showed strong results despite higher input costs and going forward the company will likely also be more diligent on accepting fixed price contracts which should make its future bookings and a significant part of its current $50 billion backlog more worthwhile.

For further details see:

RTX Stock: A Buy After Post-Earnings Rally