RUTH - Ruth's Hospitality Group: Upside Is Still On The Table

Summary

- Ruth's Hospitality Group continues to report climbing sales, but profits and cash flows have been mixed lately.

- This has been instrumental in pushing shares down more than what the market has seen, but this doesn't mean investors should stay away.

- Shares are still attractively priced and will likely appreciate in the future.

In an ideal world, investment opportunities would pay off shortly after we make them. Unfortunately, that's not how things work most of the time. It can take patience and time for things to work out. And in between the time we make an investment and the time we realize the upside that we wanted, there can be a great deal of volatility to contend with. One company that has exhibited precisely that is Ruth's Hospitality Group ( RUTH ), an enterprise that's focused on developing and operating fine dining restaurants in the markets in which it operates. Lately, sales from the company have been growing at a decent rate. But its profits and cash flows have taken a slight step back. Even though this is the case, the stock looks attractively priced at this time and likely offers additional upside for investors moving forward. So although shares have fallen over the past few months, I would make the case that it still makes for an attractive 'buy' prospect at this time.

Fine dining woes

Back in August of 2022, I wrote an article detailing whether or not it made sense for investors to consider Ruth's Hospitality Group for their portfolios. Leading up to that point, the company had done quite well to grow its operations, including its revenue and cash flows. On top of this, I was drawn by how cheap shares were. This combination of factors led me to rate the company a 'buy', a rating that reflected my view at that time that shares should generate upside that would exceed what the broader market would experience over the same period of time. So far, the market has not exactly agreed with my assessment. While the S&P 500 is down 4.8%, shares of Ruth's Hospitality Group have seen downside of 6.9%.

{kind=link}

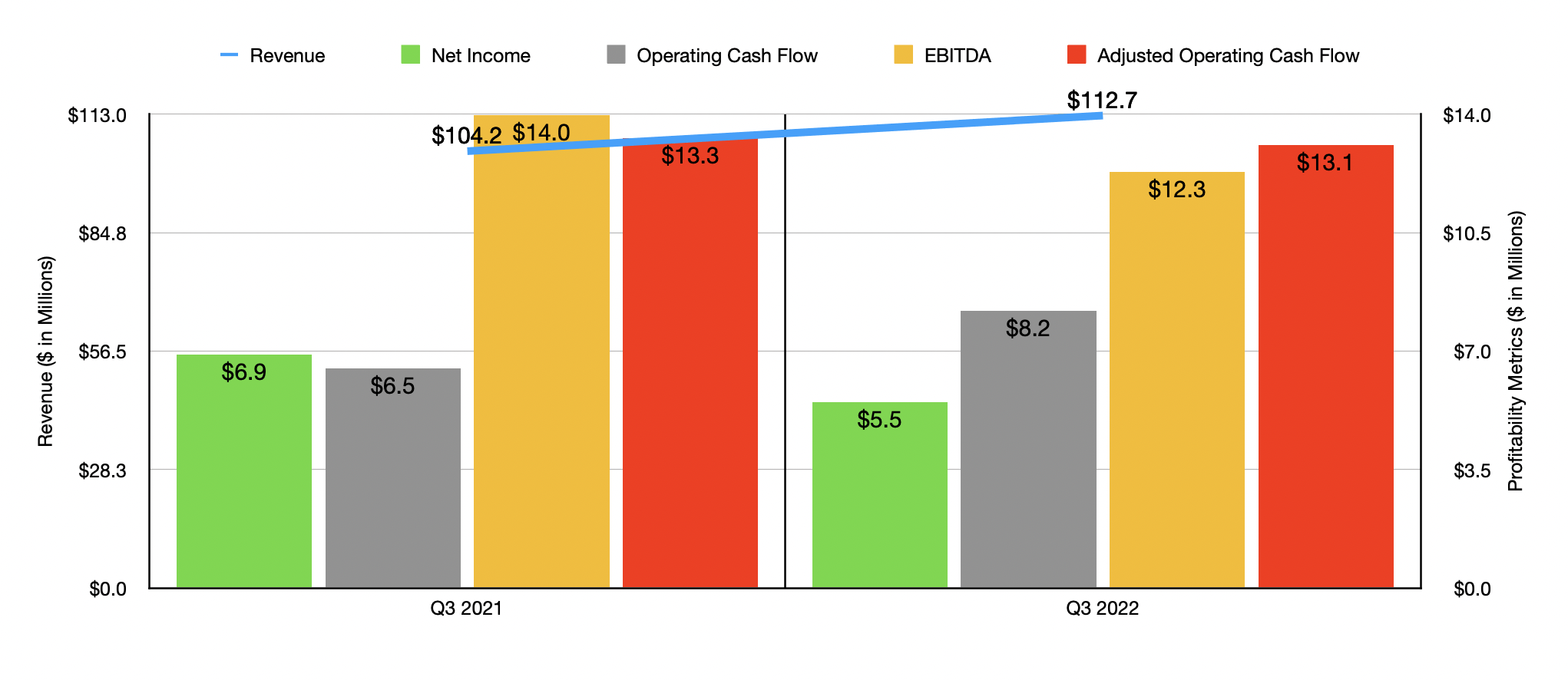

This return disparity, while not necessarily significant, is still disappointing to say the least. I would also make the case that it is largely unwarranted. For starters, if we look at data covering the third quarter of the company's 2022 fiscal year, the only quarter for which new data is available that was not available when I last wrote about the business, we would see that sales continue to climb. Revenue of $112.7 million in the third quarter was 8.2% higher than the $104.2 million generated the same time one year earlier. The company benefited from multiple factors on this end. Company-owned comparable restaurant sales, for instance, expanded by 2.9% year over year. Franchise income was up 3.5%. And other operating income jumped by 7%, driven primarily by an increase in breakage income thanks to an increase in gift card redemptions and a rise in income from restaurants operating under contractual agreements with the enterprise.

Although it was great to see revenue increase, profits did take a small step back. Net income, for instance, dipped from $6.9 million to $5.5 million. Even as food and beverage costs fell from 34.2% of sales to 31.7%. Instead, the company dealt with increased restaurant operating expenses totaling 50.2% of sales compared to the 47.2% reported one year earlier. That was due to higher labor costs from adding staff to its locations. Marketing and advertising costs also rose thanks to a $1.2 million increase in digital and data transformation expenses. Other profitability metrics followed a similar trajectory. Operating cash flow did increase year over year, climbing from $6.5 million to $8.2 million. But if we adjust for changes in working capital, it would have ticked down from $13.3 million to $13.1 million. Over that same window of time, EBITDA decreased from $14 million to $12.3 million.

{kind=link}

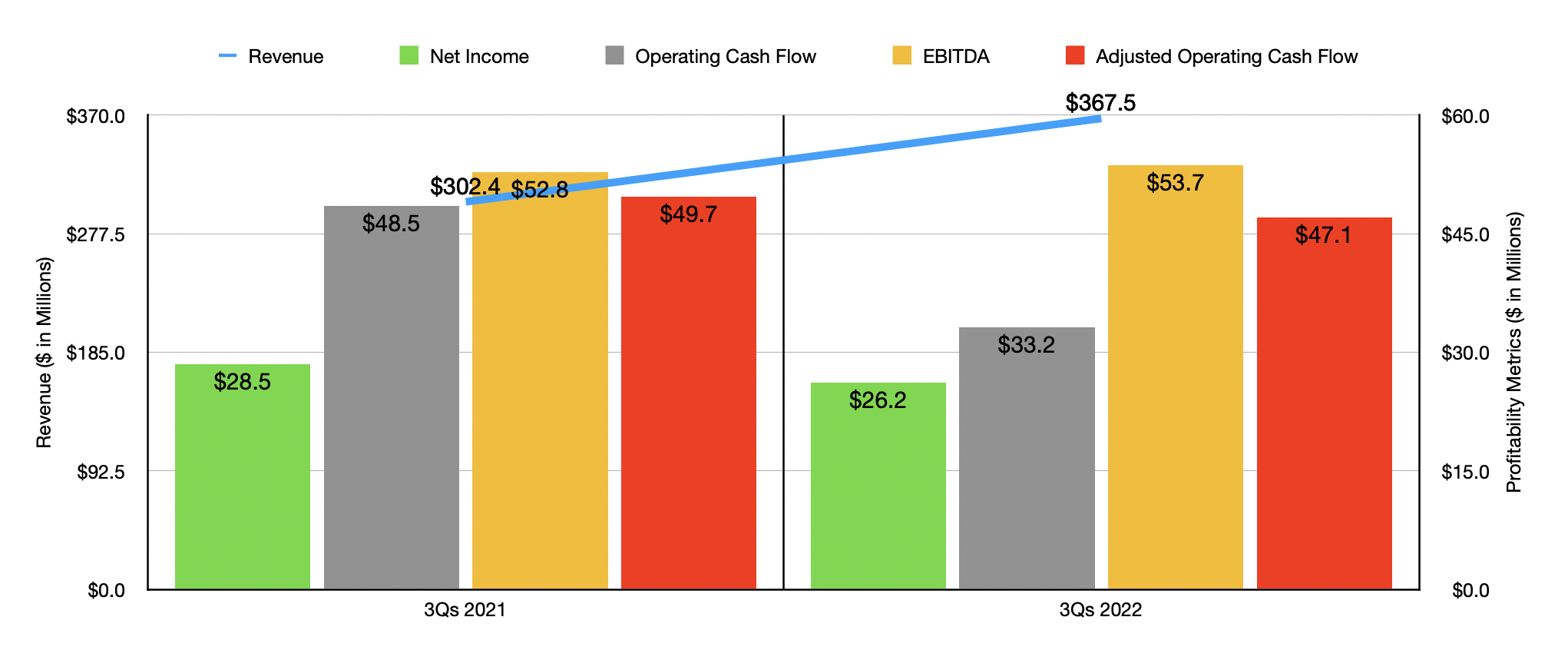

Because of how the third quarter turned out, results for the first nine months of 2022 as a whole have been somewhat mixed. Revenue was up nicely, totaling $367.5 million compared to the $302.4 million reported one year earlier. Despite this, profits dipped from $28.5 million to $26.2 million. Operating cash flow fell from $48.5 million to $33.2 million, while the adjusted figure for this trimmed from $49.7 million to $47.1 million. In fact, the only profitability metric to improve year over year for the first nine months relative to the same time one year earlier was EBITDA. This came in at $53.7 million in 2022, up from the $52.8 million reported one year earlier.

{kind=link}

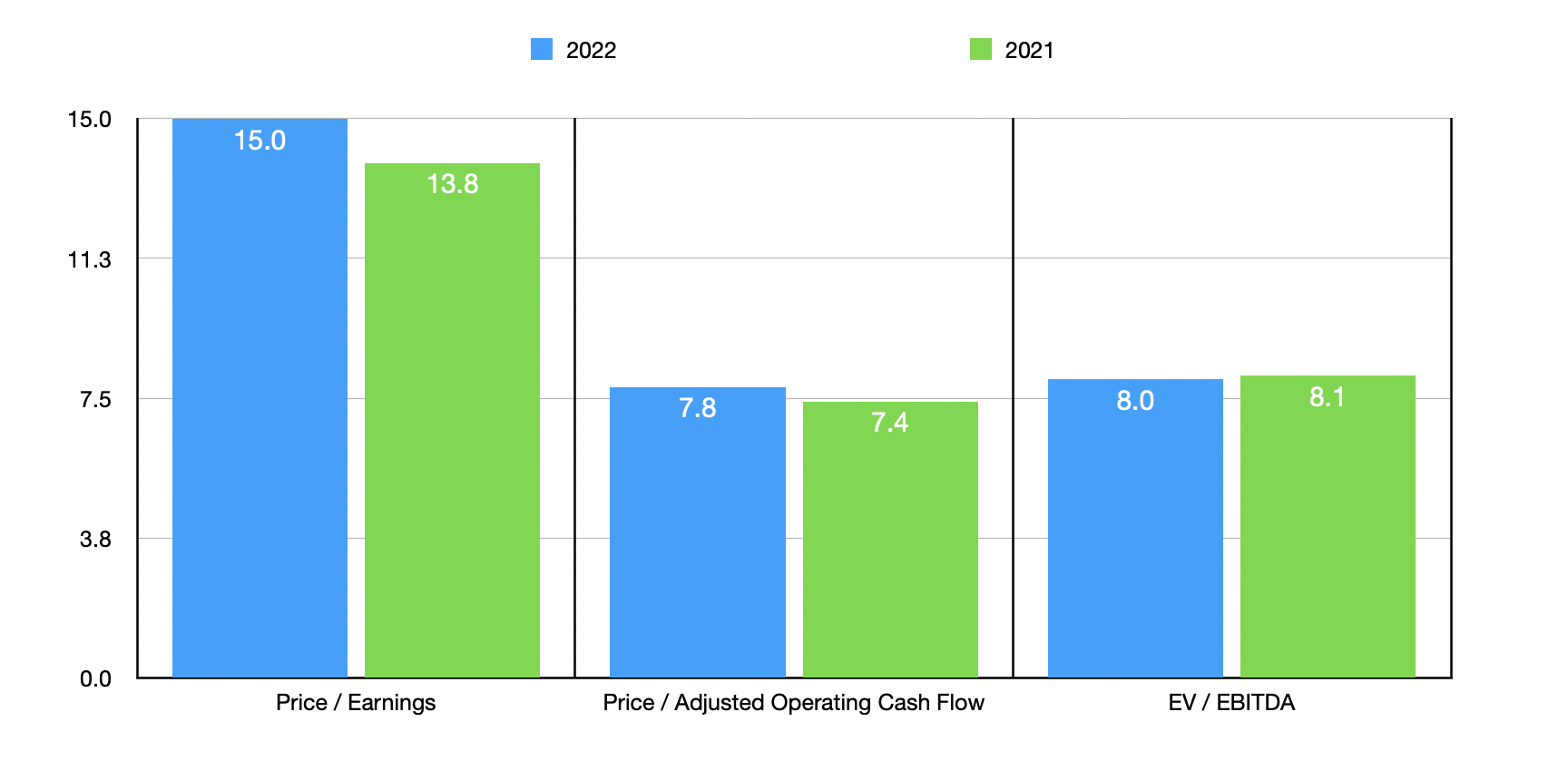

If we annualize results experienced so far for 2022, we would get anticipated net income of $38.9 million, adjusted operating cash flow of $74.8 million, and EBITDA of $74.3 million. Based on these figures, the company is trading at a forward price to earnings multiple of 15, a forward price to adjusted operating cash flow multiple of 7.8, and a forward EV to EBITDA multiple of 8. By comparison, if we were to use the data from the 2021 fiscal year instead, the multiples would be 13.8, 7.4, and 8.1, respectively. I also, as part of my analysis, compared the company to five similar enterprises. On a price-to-earnings basis, these companies ranged from a low of 7.3 to a high of 745.7. And when it comes to the EV to EBITDA approach, the range was from 5.7 to 116.8. In both cases, only one of the five companies was cheaper than Ruth's Hospitality Group. Meanwhile, using the price to operating cash flow approach, the range was from 12.6 to 41.4. In this scenario, our prospect was the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Ruth's Hospitality Group |

| 15.0 |

| 7.8 |

| 8.0 |

| BJ's Restaurants ( BJRI ) |

| 745.7 |

| 13.7 |

| 13.8 |

| Denny's ( DENN ) |

| 7.3 |

| 20.0 |

| 5.7 |

| Kura Sushi USA ( KRUS ) |

| N/A |

| 41.4 |

| 116.8 |

| Chuy's Holdings ( CHUY ) |

| 25.7 |

| 13.8 |

| 9.8 |

| El Pollo Loco Holdings ( LOCO ) |

| 19.3 |

| 12.6 |

| 9.3 |

Takeaway

Fundamentally speaking, Ruth's Hospitality Group is still doing well from a sales perspective but it's clear that margins have been harmed a little bit by rising prices. This may put a damper on the company's upside. But at the same time, cash flows are still appealing and shares are trading at levels that make the company look cheap. Investors should naturally continue to keep an eye on bottom line results because we don't know how the picture could change moving forward. But if we don't see any further deterioration in its bottom line results, I believe a 'buy' rating would still be appropriate.

For further details see:

Ruth's Hospitality Group: Upside Is Still On The Table