RYLD - RYLD: The History Has Shown That The Structure Does Not Function

2023-09-25 07:50:07 ET

Summary

- The Global X Russell 2000 Covered Call ETF applies a covered call strategy against the Russell 2000 Index and Vanguard Russell 2000 ETF.

- RYLD has a low net fee expense ratio of 0.6% and holds about 2000 companies, with the largest exposure being VTWO at 34% of the portfolio.

- Since its inception, RYLD has underperformed the Russell 2000 and other covered call strategy ETFs, which track popular indices.

- On a go-forward basis, RYLD is most likely set to deliver still inferior returns considering the bias towards small-cap stocks, which tend to perform badly in the contracting economy.

- The constrained access to financing renders more difficult conditions to outperform large-cap alternatives.

The Global X Russell 2000 Covered Call ETF ( RYLD ) applies a covered call strategy against Russell 2000 Index and / or Vanguard Russell 2000 ETF (VTWO). This means that RYLD goes long the underlying constituents of Russell 2000 and in the same time sells call options against these positions. As a result there is a capped upside with a fully open downside, which is somewhat protected by the collected premium.

All in all, the investment objective of RYLD is to generate high current income to provide investors with monthly distributions without any manual trading work.

Typically, ETFs with embedded option strategies are relatively expensive, but in RYLD's case the net fee expense ratio is very low at 0.6%, which creates less of a drag on the return potential.

In terms of the portfolio holdings, there are about 2000 companies included in the list. The largest exposure is VTWO accounting for ~ 34% of the total portfolio. Such tactic is employed due to VTWO's liquidity profile, which allows RYLD to reduce the size of trades on all of the underlying Russell 2000 Index companies. This obviously comes in handy considering that in many cases the level of free float and secondary liquidity of these smaller cap stocks are weak, implying unfavourable bid / ask spreads.

Thesis

In my opinion, RYLD is a subpar investment with very specific offering that might benefit a rather tiny size of investor universe. While RYLD is well-structured and has a small fee, the exposure itself is suboptimal.

Let me elaborate on why I think RYLD should be viewed with an extra caution. In a nutshell, RYLD has structurally underperformed both its peers and, most importantly, the Russell 2000 benchmark.

{kind=link}

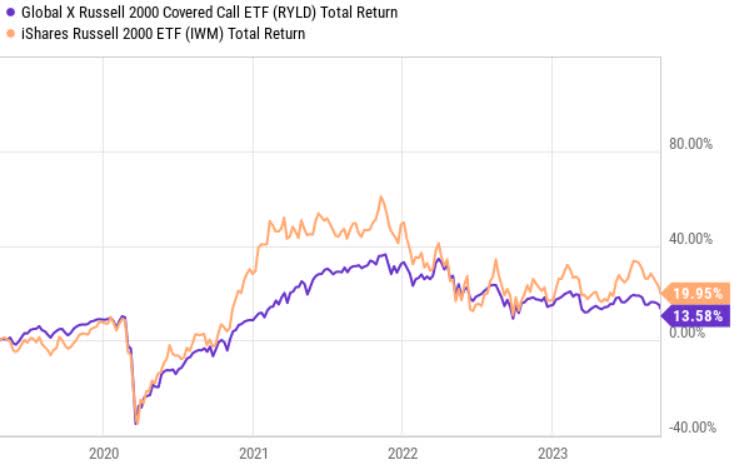

Since the inception, RYLD has underperformed Russell 2000 on a total return basis. In fact, there has been almost no single period in which RYLD has delivered greater returns than the index.

{kind=link}

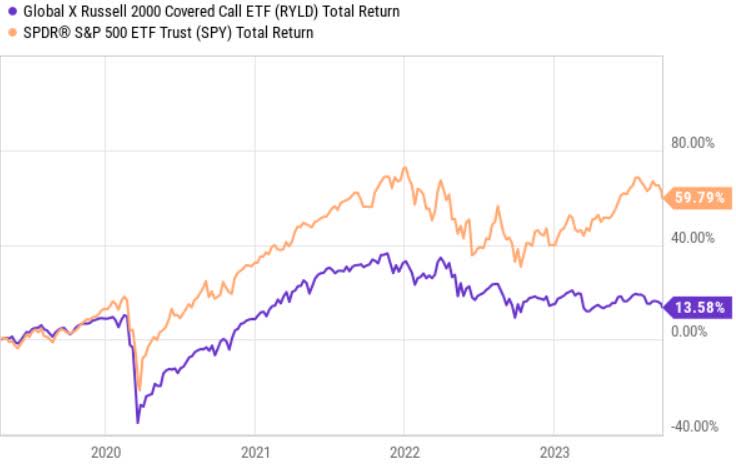

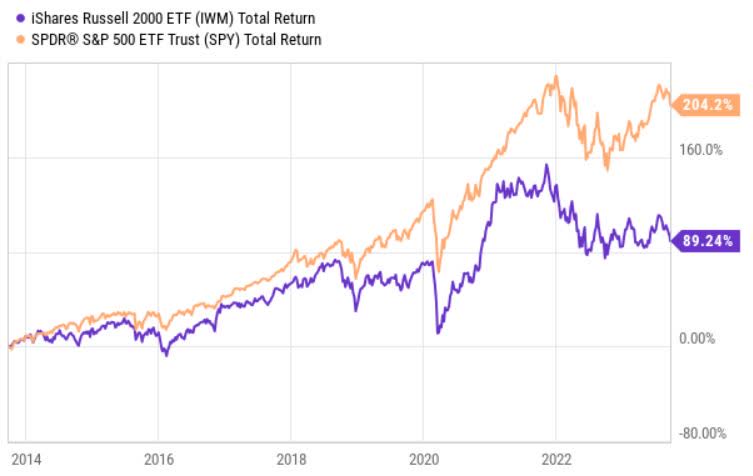

RYLD has also clearly underperformed the S&P 500 both when the COVID-19 broke out and when the FED started to aggressively increase the Fed Fund's rate.

{kind=link}

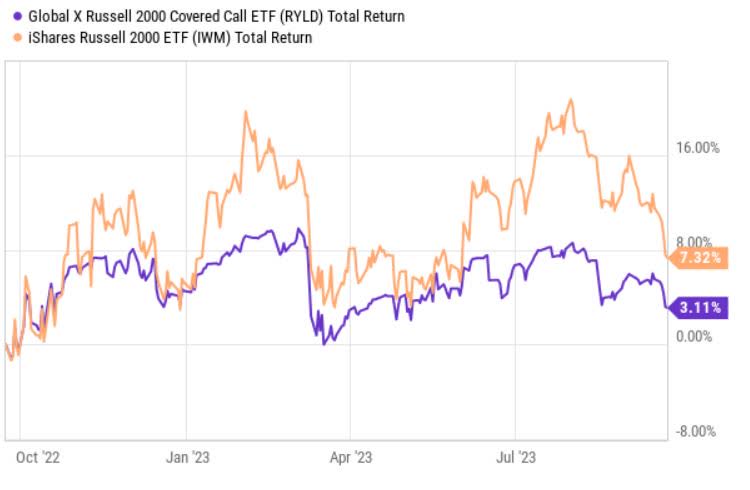

Even compared to some of its peers applying covered call strategies on other major indices, RYLD has lagged behind. Measuring this on a YTD basis, the divergence is very obvious.

There are two reasons for this.

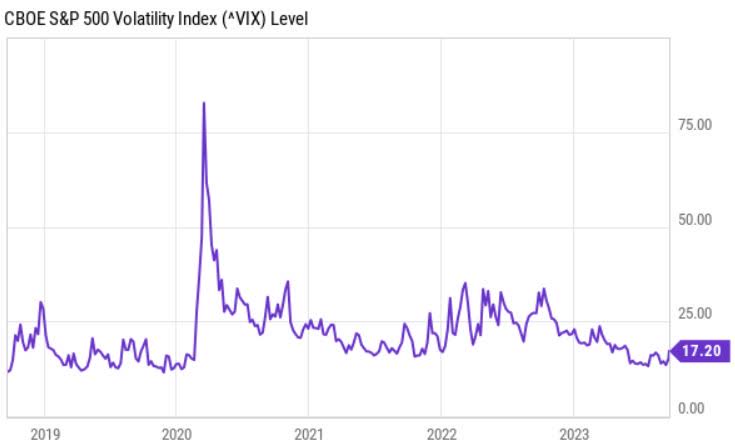

#1 Relatively muted VIX

The conditions under which covered call strategies thrive are typically associated with spiking volatility and an overall unpredictability in the market, where there is a huge uncertainty around the trajectory of capital markets over foreseeable future.

For RYLD and other covered call strategies the past couple of years have not been that favourable.

{kind=link}

We can see this through VIX level, where in the past 3 years, the index has been more or less stable and since Q3, 2022 has assumed a declining trend, which obviously does not help covered call strategies. Plus, the volatility of volatility, which tends to explain some part of the option premiums has been also stable.

In other words, what this means for RYLD is that the sold options have generated less attractive premiums. This, in turn, has forced RYLD to buy options at closer strikes to capture more meaningful premiums that has sacrificed the upside potential accordingly.

{kind=link}

The chart above captures this problem nicely. Whenever the Russell 2000 has gone up, RYLD has remained range bound (currently, the max price gain level is ~3.5%). Granted, during minor declines in the index, RYLD has been stable due to the sourced premiums. However, in instances of more significant declines, RYLD has followed accordingly because of the insufficient premium size.

#2 Poorly performing small cap stocks

Over the past decade, small cap stocks (represented by Russell 2000) have delivered inferior returns relative to the S&P 500. The gap in the total returns have widened since the pandemic years and higher interest rate environment.

{kind=link}

Going forward there are several fundamentals elements (except the valuations), which indicate that the relative underperformance of small cap stocks should continue.

The most critical element is the "higher for longer" interest rate environment, which imposes negative consequences on both the access and cost of financing. Since small cap stocks have per definition more limited flexibility to tap into wide range of financing sources, the combination of more constrained financing conditions should introduce more pronounced headwinds. For larger cap stocks, this issue is obviously less relevant.

Furthermore, during recessionary environment, small cap stocks tend to register worse results compare to better capitalized and more diversified companies. Against the backdrop of depressed manufacturing and consumption sentiment levels and the increased probability of a near-term recession, the return prospects of the Russell 2000 does not look promising.

The bottom line

Since its inception, RYLD has underperformed the Russell 2000 and other covered call strategy peers. The explanation of this lies in the combination of relatively stable VIX levels and poorly performing small caps.

Currently, given the macroeconomic backdrop, I do not see how RYLD could in a foreseeable future enjoy tailwinds stemming from its bias towards small cap universe. Granted, in such case the VIX would increase providing some momentum to the RYLD (sold option premiums). Yet, under such circumstances, I would bet on covered call ETFs, which track large cap stocks.

In my humble opinion, RYLD could be considered by investors, who think that VIX is set to increase due to the looming recession and that in the declining economic period, small caps should deliver better returns than those companies, which are embedded in the S&P 500 or other large cap indices.

For further details see:

RYLD: The History Has Shown That The Structure Does Not Function