SCCD - Sachem Capital: Selling Overpriced Baby Bonds To Secure A 9-11% Yield

2023-09-08 10:30:00 ET

Summary

- Sachem Capital baby bonds offer a level of comfort as they rank senior to shareholders and preferred shareholders.

- The article discusses the different options in the Sachem baby bond spectrum, including their coupons, prices, and maturity dates.

- The author recommends considering selling SCCB and reinvesting in higher-yielding securities like SCCD or SACC.

Introduction

About a month ago, I published an article on Sachem Capital ( SACH ) where I highlighted some of the publicly traded debt securities issued by Sachem. Those baby bonds can be quite attractive in certain scenarios. And although you would give up potential capital gains in case Sachem's performance is exceeding expectations, it provides a certain level of comfort to know you are ranked senior to all shareholders and preferred shareholders in case the business does not perform as expected or anticipated.

There is not 'one right investment' when it comes to the notes

As I discussed the financial results of Sachem Capital in my previous article, I don't think there's any need to just copy that analysis verbatim. I'd urge you to read or re-read the August article , as I still stand by what I wrote.

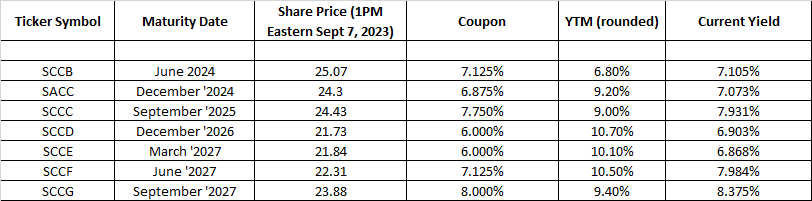

In this article, I wanted to discuss the different options in the Sachem baby bond spectrum. In the table below, you can find all outstanding baby bonds with their coupons, prices on the market, and the maturity dates. The maturity is always on the final day of the month mentioned below.

Some commenters on my previous article were also wondering what the 'current yield' is, as there is a type of investor mainly interested in generating income right off the bat without necessarily wanting to maximize the yield to maturity. While I personally don't consider that to be a relevant metric that I would use, I am happy to accommodate and have included the current yield as well, as that's easy enough to calculate.

I also took the liberty to round the yield-to-maturity results for the simple reason the YTM changes every single day. Every day you get closer to maturity, even if the baby bond price does not move, will constitute a (small) change in the yield to maturity. Therefore, readers are warned to perhaps run the numbers on the YTM again themselves when they are looking at these baby bonds. My yield to maturity is merely meant to be 'indicative'.

{kind=link}

My personal perspective on bonds, baby bonds, and debt securities in general is that I mainly care about the yield to maturity. In the article published in August, I mentioned I was still happily buying ( SCCG ) for its 9.75% yield to maturity.

Since that article was published, I sold about three-quarters of my SCCG as the yield to maturity continued to drop (I sold a portion above $24, so the yield to maturity was even lower at that point). I am leaning towards reinvesting the proceeds in ( SCCD ). Not only because the yield to maturity is the highest but also to take advantage of the maturity date which comes several years earlier than the SCCG maturity date.

But there are a few other potential trades investors should consider. The difference between SCCB and SCCC, for instance. For some reason, the SCCB securities are trading at a premium to par, which means the yield to maturity is even lower than the 7.125% coupon. Meanwhile, the SCCC securities, which mature just fifteen months, are trading at a discount of more than 2% to par while the coupon is 62.5 bp higher. The discount to par is important in this case, as the relatively short period until maturity means the yield to maturity is a stunning 220 bp higher than SCCB. Additionally, even buying the SACC securities would result in a substantially higher YTM and an even bigger bump compared to what a switch to SCCC would yield.

The only reason one could consider SCCB is for the 'seniority by maturity' rule: SCCB matures first and, therefore, should be the least 'risky' security when it comes to repayment. That's a fair assumption, but it does not explain the massive difference in yield to maturity. But apart from that, investors should consider selling their SCCB position and redeploy the cash in a higher-yielding security.

Investment thesis

I am still convinced owning debt securities issued by Sachem Capital is the right strategy for my personal portfolio, but I also have to be somewhat agnostic when selecting the baby bonds. While I obviously need to take elements like transaction fees into account, it does make sense to keep an eye on the respective yield-to-maturity results and switch positions where necessary.

I currently have a position in SCCG, SCCB (which I am now intending to sell and switch over to SCCD), and SACC. I may add to existing positions or acquire new positions depending on their respective bond price fluctuations.

For further details see:

Sachem Capital: Selling Overpriced Baby Bonds To Secure A 9-11% Yield