SAFRY - Safran: A Good Company But 'Hold' Due To Valuation

2023-11-10 22:57:08 ET

Summary

- Safran was a significant investment in the arms/industrial sector in 2022, with me shifting my rating in early 2023.

- I sold my position in Safran after achieving an initial outperformance of more than 6x compared to the market.

- The overall return on investment (RoR) on Safran since my article in March 19th, 1.5 years ago, is discussed.

- I consider the company to be a "HOLD" here.

Dear readers/followers,

Safran ( SAFRY ) was one of my significant investments in the arms/industrial sector in 2022, with my latest buys in September 2022 and my last article in early 2023. I shifted my rating at this time, and this is an updated article for that piece. For the SAFRF ticker, my latest article can be found here , and the company was at a "BUY" then, for the same reasons SAFRY was at a "BUY" in September of 2022 - the valuation at the time was compelling enough to still give it a "BUY" for the ADR ticker, even if the upside was materializing then.

My initial outperformance to the market of more than 6x was more than enough to make me sell my position, except a watchlist one, in Safran, with the last shares I intended to sell about two weeks after my last article.

Here is my overall RoR on Safran since my article back in September over 1 year ago.

SeekingAlpha Safran RoR (SeekingAlpha Safran )

With the company up over 80% since my lowest level, the company is now at a relatively high valuation and position. The question becomes if you can now, based on new results expectations, pay more for the company, and where this could be a profitable investment.

Let's see exactly what we have here, and what the results and upside could be.

Safran - Plenty to like, but maybe not enough at this valuation.

Safran is a play on the aerospace industry. The aerospace industry, if you spend any amount of time researching this fascinating sector, is set to see a very good few decades until the 2040s.

Why is this the case?

Because air traffic is growing faster than GDP, for one. The companies in the sector, including Safran as well as Rolls-Royce ( RYCEF ) which I also cover -as well as others -are seeing very good order flow and demand trends. The company records 38,200 new aircraft deliveries, of which 70% of those are single-aisle planes. The new demand for engines is driven by the airframer build rates, which in turn is somewhat driven by the current ESG and decarbonization of the entire aviation sector.

Also, added to this, and relevant for either pure-play defense players or partial defense players like Safran, is the ongoing increasing spending for the defense sector. This is happening for obvious reasons, but it's also part of what's driving Safran forward.

{kind=link}

Safran is, without a doubt, a good company. When I say that a business is a good business, I'm speaking, as always, of the business fundamentals, things like gross, operating, and net margins, things like returns on assets or equity or invested capital. The company is doing very well across these KPIs, with special highlights in the net margin, where the company's results are among the best in the entire sector. The company's business model is a well-working one. The same is true for fundamentals. With an interest coverage of over 24x, a cash/debt of over 1x, and other great basics, the company is one of the more solid players in the peer group.

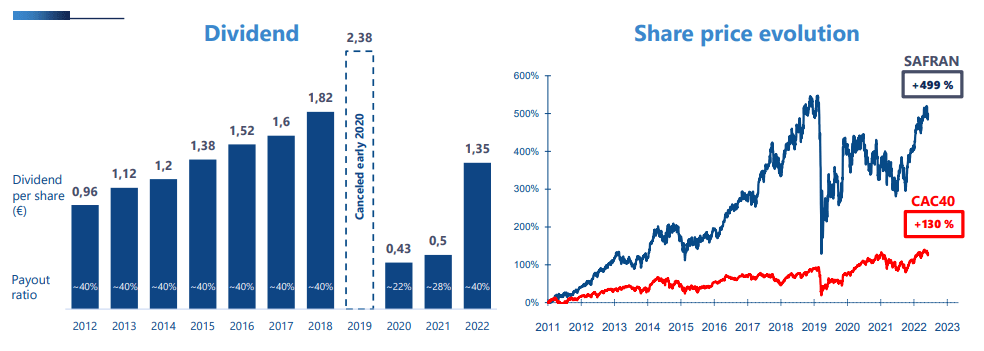

The one drawback to Safran is its dividend. At the current level, we're at less than 0.9% yield, which is sub-par in the segment and to company peers. And this dividend is very unlikely, based on company trends, to significantly improve over the next few years unless the company changes its dividend policy - again, unlikely.

The company's business model took a significant hit during COVID-19 and the resulting downturn in demand, revenue, earnings, margins, and FCF. It troughed in 2020, with FCF at close to "only" €1B, with the forward expectation for more than 2.5x that level. (Source: 3Q23 Safran results )

The advantage of Safran is having over a 70% market share for the worldwide single-aisle market, with a backlog of 10,000+ engines at this time, and a win rate for the A320neo of over 70% in 2022. The company is heading to a production level of over 2,000 engines per year to start to work through some of the backlog - and the aftermarket segment is recovering as well.

Safran IR (Safran IR)

Decarbonizing aviation comes in a few ways - it comes from more lightweight equipment, sustainable aviation fuels (which I by the way also invest in), and also the somewhat more ethereal factor (at least comparatively), of hybrid and EV flight. Safran is a market leader in these three sectors - because over 75% of the company's R&D spending is aimed exactly at these sectors.

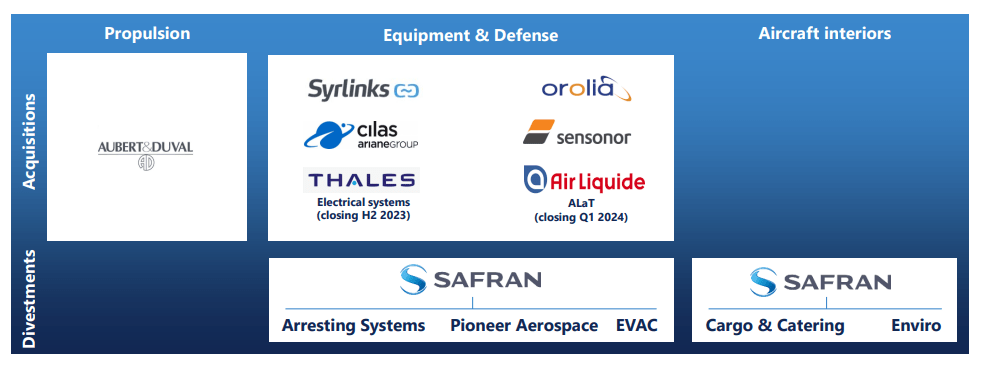

Let's remind ourselves, for a moment, of the company's successful transactions since 2021 and where the company is today.

{kind=link}

Even with the cancellation of the early 2010 dividend due to COVID, and the recovery since which has not gone back to the €1.82 level of 2018, the company has still managed a CAGR of 17.6% for shareholders between 2012 to 2023. This is well above the market average, and it's well above the CAC40, the comparable index that's relevant here.

{kind=link}

The current priorities for the company are a ramp-up in OE deliveries, reducing supply chain congestion through a better mix (and also delivering improved inflation effects for the company), and accelerating the investment pace for decarbonization technologies. These trends are expected to deliver earnings growth going forward in the next few years. (Source: 3Q23 Safran results )

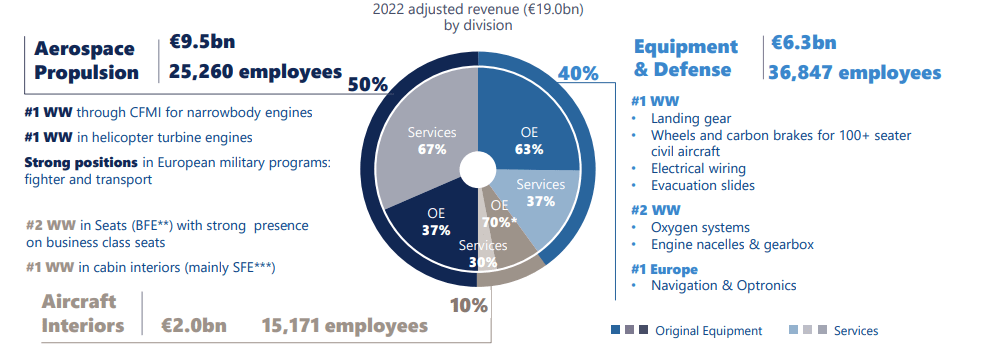

Sounds good, but is it a likely development? Maybe not exactly - but the company is a world leader in the aerospace and propulsion segment, as well as a strong player in other segments. While not a full defense contractor at over 50% of the mix, a 40% E&D exposure is still strong.

{kind=link}

Remember, Safran also has its aircraft interior business, and this is also up with new contracts from Asia, Europe, and the Middle East for seats, retrofitting, and business class interiors. (Source: 3Q23 Safran results )

3Q23 results were good. Top-line results are continuing to improve. The company's revenue went up 26%, which continues the recovery that's been ongoing. Propulsion alone went up even more, 28.4%, and aircraft interiors were even better at over 30%, despite my belief that the E&D segment would have been the best here.

As a result of this, the company increased its full-year outlook even further, reaffirming the latest increase back in July. The overall trend is really seeing expectations for more and more improvements here.

The aftermarket demand for Safran's services continues to be significant. The company continues to see actual, significant tailwinds with the narrowbody traffic now well above pre-crisis levels, resulting in very strong demand for spare parts - particularly for the CFM56. The company is trying to ramp up production to meet demand, but the clear trend-break of top-line results going above the 2019 levels is the strong positive indicator here.

Safran now expects annual revenues for the year of at least €23B, with recurring operating income of €3.1B and FCF above the €2.5B level that was expected, at €2.7B currently. This set of assumptions is based on no further major disruptions to the world economy (such as new COVID), with narrowbody volumes and trends continuing to move upward and LEAP engine deliveries increasing by around 40-45%, narrowed from around 50%. (Source: 3Q23 Safran results )

The company has hedged the USD exchange rate at about 1.13 at an exposure of about $10B.

Let me show you what these numbers mean for valuation and upside, and whether you should, as I see it, consider buying here.

Safran - Still expensive now, despite it being a quality business

The main problem with Safran at this time is simple. We're talking about an A-rated aerospace and defense business, yes - but we're also talking about this company trading at over 31x P/E, in a market with a risk-free rate of upwards of 5%, while Safran only yields 0.89%.

My previous PT was €115/share and the company now trades at €152/share, marking a clear overvaluation to at least my previous price target.

I view it as dangerous to estimate the company at a near-term historical average, such as a 3 or 5-year average. The reason is that the company went through a high valuation due to low earnings, but not a significantly declining share price.

On a 20-year average, Safran is trading closer to a 23x P/E. If you forecast Safran at 23x forward P/E assuming a double-digit EPS growth rate, you're still getting less than 15% annualized RoR, around 12.9%. While good, it's not a level that I am willing to invest in - not when considering what's available on the market today.

Even with all the fundamental advantages of the company - long-term debt at below 33% among them, the company requires some heavy premiums in order to outperform from this level on and onward. When you consider the potential downturn if the defense spending goes the other way, allowing for French dividend withholding taxes, and the potential FX risk if you're not a native EUR investor, you can see why I'm more comfortable at €115/share than I am at €150/share.

I'm willing to bump my target for the company here - but not as much as you might believe. Street targets have been massively raised since my last article. We're talking up almost €50/share on average, with current averages starting at lows of €145 to highs of €200/share with averages of €177/share. That's compared to a 2022 September low of €62/share, which is less than half , and a high of around €150/share, with an average of €125/share.

I'm raising my target to €125/share, implying a 15% annualized upside to an upside of 23-24x P/E, which is where I'd see the company for the long term. I realize that suddenly I'm among the more conservative analysts for Safran, but that's something I'm fine with. For the respective ADR's of Safran here, both SAFRY and SAFRF, that's a PT of around $130/share for SAFRF, which is a 1:1 ADR equivalent, and a $32.5/share PT for SAFRY, which is a 1:4 equivalent ADR for the native ticker.

Why?

Because I use conservative valuation metrics - and don't let myself be easily charmed by too-positive forecasts. At a projected FCF, the company is worth no more than €80-€90/share, even using very optimistic numbers, and based on a median sales multiple for the segment, Safran is currently significantly above the average. Couple this with a somewhat declining operating margin, close to a 10-year high price, a 10-year high P/S ratio, and an ROIC that's still less than WACC, there are many positives, but also some negatives on Safran. More conservative analysts consider the company currently to be fairly valued. Despite the average of €176/share here, only 9 out of 20 analysts have the company at a "BUY" here. (Source: Tikr.com/S&P Global)

So - I say again, €125/share, or $130/$32.5, and not higher, depending on if you go for the native or the ADR's. I'm keeping my very small watchlist position, but I am not adding more.

Thesis

- Safran isn't the most immediately profitable or exciting investment opportunity with what's happened in Russia, but it's a solid aerospace company with a market-leading position in appealing segments. The delayed earnings growth will likely materialize in 2023-2025.

- If the company becomes cheap enough - then I'm interested, and at the current price either for the ADR or for the native share. I invest in the native French shares.

- I give the company a PT of €125/share, and it's a "HOLD" here.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is no longer cheap and also doesn't have a significant enough upside for me to go "BUY" here. For that reason, I'm out and on a "HOLD". I'm rotating part of my Safran investment and looking for greener pastures/more value elsewhere.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Safran: A Good Company, But 'Hold' Due To Valuation