SSRM - Sandstorm Gold: Higher Prices Likely Ahead

2023-11-09 10:00:49 ET

Summary

- Sandstorm Gold Ltd. released Q3 results, reporting a satisfactory quarter with revenue up on the back of stronger metals prices.

- However, the real story was the positive developments across the portfolio which many on the sidelines appear to be missing due to focusing too much on the short term.

- In this update, we'll dig into the recent results, and progress on key assets, and see whether Sandstorm is a turnaround story worth betting on after its violent correction.

We're more than halfway through the Q3 Earnings Season for the Gold Miners Index ( GDX ) and one of the most recent companies to report its results was Sandstorm Gold Ltd. ( SAND , SSL:CA). Overall, the company had a satisfactory Q3 , with revenue up 6% year-over-year helped by higher metals prices. However, the overall quality of its revenue, cash flow, and portfolio has improved materially since its two major acquisitions last year (Nomad/Basecore), with a more diversified royalty/streaming portfolio and multiple new royalties/streams on impressive and in some cases world-class assets. In this update, we'll dig into the Q3 results , the stock's updated valuation, and whether this pullback below US$4.50 is worth buying.

All figures are in United States Dollars unless otherwise noted.

Platreef Project Construction Progress - Ivanhoe Mines

{kind=link}

Q3 Results

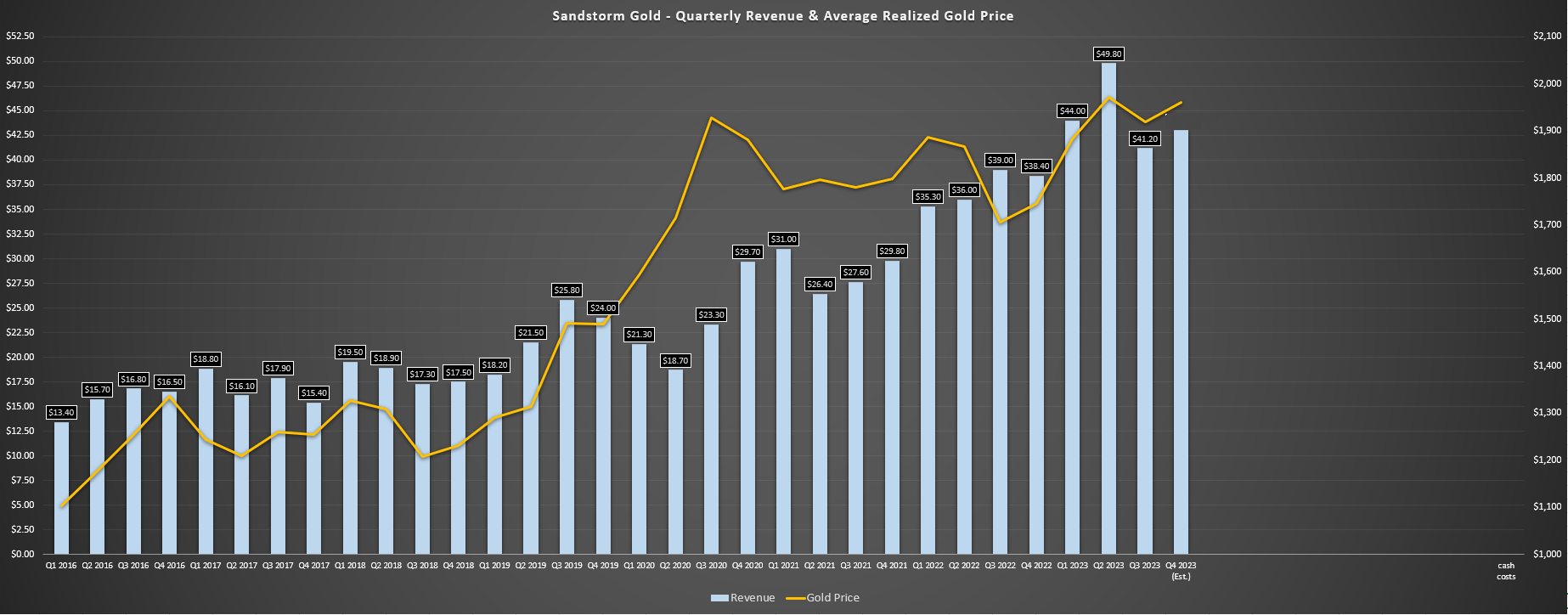

Sandstorm Gold Royalties ("Sandstorm") released its Q3 results this week, reporting quarterly revenue of $41.3 million and operating cash flow of $31.9 million, translating to a 6% and 27% increase from the year-ago period, respectively. The increase in sales can be attributed to the higher average realized gold price ($1,919/oz vs. $1,706/oz). Meanwhile, attributable gold-equivalent ounce [GEO] sales may have declined year-over-year, but they were up sharply on a year-to-date basis, with Sandstorm reporting record sales of 74,000 GEOs following its acquisitions. This has placed the company well on track to deliver into its annual guidance of 90,000 to 100,000 GEOs, and the recent strength in metals prices will certainly help with cash flow generation to allow the company to continue de-leveraging.

Sandstorm Quarterly Revenue & Average Realized Gold Price - Company Filings, Author's Chart

{kind=link}

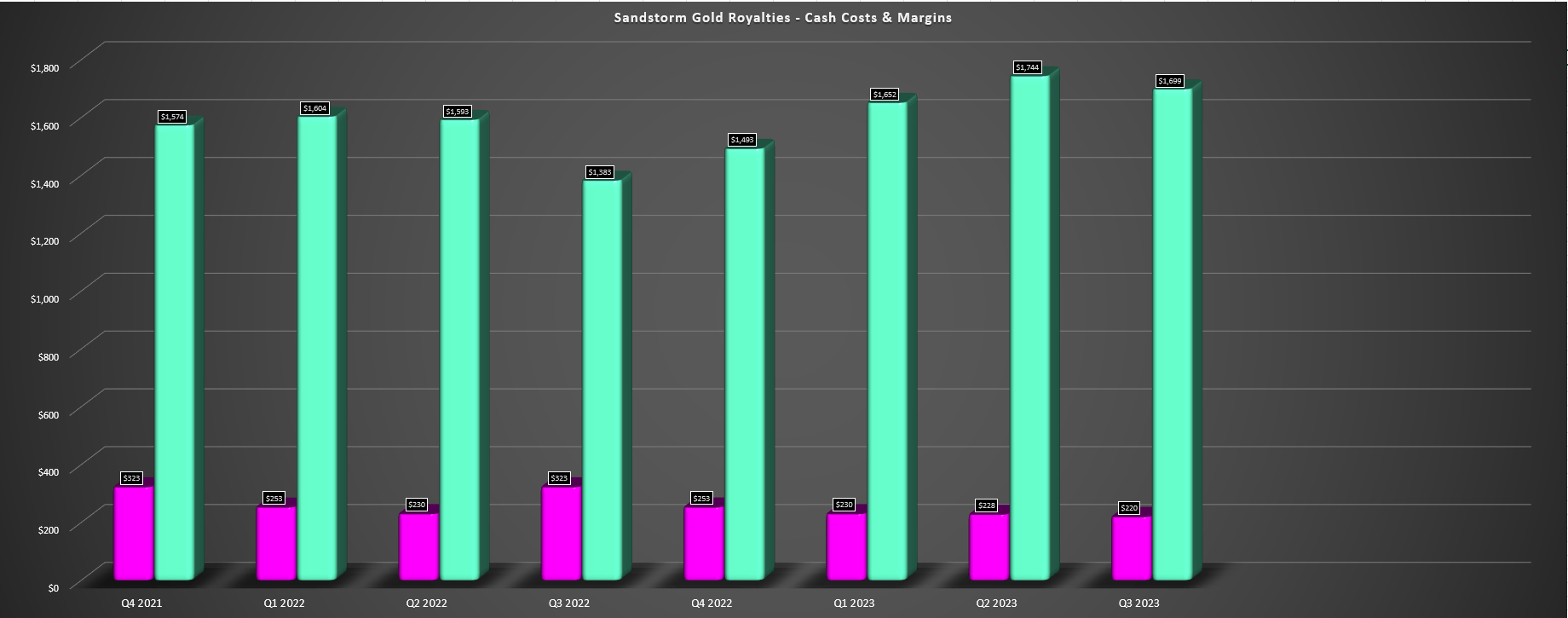

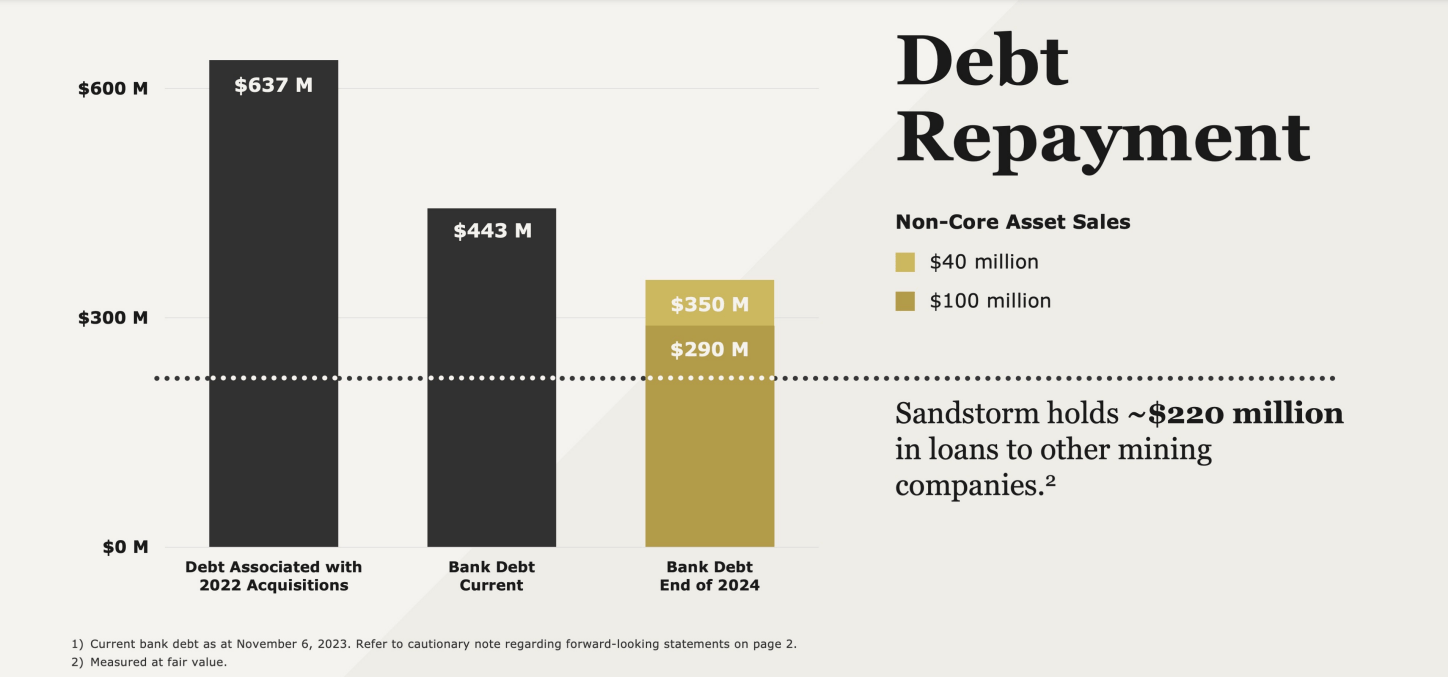

Looking at the company's margins, it was another solid quarter, with Sandstorm reporting cash margins of ~88.5% ($1,699/oz), up from $1,383/oz in the year-ago period. This was related to lower cash costs and the much higher average realized gold price, and while this did not translate to higher net income, this was largely because of lapping difficult comparisons ($24.9 million gain recorded in Q3 2022 on Hod Maden sale) as well as much higher interest expense ($9.8 million vs. $6.5 million) because of higher interest rates. On a positive note, the company repaid $11.0 million in debt on its RCF in Q3, and has reduced debt further post quarter-end (current debt: $443 million), following the sale of royalties to Sandbox. These included a relatively small royalty on a portion of the pit at Blackwater in British Columbia, Canada (0.21% NSR) and a 1.0% GRR at El Pilar in Sonora, Mexico, where the production timeline was recently pushed out to 2025.

Sandstorm Cash Costs & Margins - Company Filings, Author's Chart Sandstorm Gold Debt & Debt Target - Company Presentation

{kind=link}

{kind=link}

Understandably, some investors might not be elated with Sandstorm's decision to engage in non-core asset sales to help de-lever. And while the company has stated it's focused on non-cash flowing assets, the two first deals across the plate may not have been cash-flowing (and weren't paid out entirely in cash), but they were certainly inching closer to first production. That said, Sandstorm's CEO Nolan Watson stated on the call that the recent deal had been in the works for a while already ($10 million in cash, $15 million in Sandbox shares) which may explain why somewhat of an exception was made here. In addition, Sandstorm's CEO stated new deals would prioritize cash, and he reaffirmed that the $40 to $100 million of proceeds from non-core asset sales references cash only and not any other proceeds from these transactions, meaning that we should see at least $50 million of these proceeds applied to the debt load over the next year.

Obviously, selling non-core assets for a royalty/streaming company is a bit of a strange move given that the model for royalty/streamers is to sit on non-cash flowing assets and benefit from optionality (one never knows which will yield a huge discovery), like the surprise Corvette lithium discovery which was a sleeper until 2022. However, there's no question that Sandstorm bit off a little more than it could chew last year in hindsight given the interest rate environment, and I think selling off assets vs. selling equity is the right move with SAND shares trading at their lowest multiple in years. Plus, it has nearly 250 total royalty/streaming assets (of which 42 are producing), and there are dozens that are unlikely to head into production by 2035, so letting them go for some value makes sense when the company is sitting on high-cost debt (SOFR + 1.9% to 3.5%). In summary, while I don't love the move, I think it's the lesser evil, and this isn't a case where it's dumping cash-flowing assets or core assets like Iamgold (IAG) did with Rosebel, Boto Diakha-Sirabaya and Karita.

Recent Developments

Overall, the recent financial results and relatively heavy debt load might spook some investors, especially when compared to the pristine balance sheets of some of its larger royalty/streaming peers (net cash positions). However, Sandstorm's debt levels are very reasonable considering it has a diversified and "recurring" business model. Another criticism of Sandstorm is that its per share metrics are not trending in the right direction, and this is also a valid point. That said, a significant chunk of the value in its recent acquisitions were related to development-stage assets, so this is not going to show up in GEO sales, cash flow, and or revenue per share immediately. Therefore, judging the company on per share metrics following a major acquisition (and an unfortunate follow-on equity raise) is a little fair, just as it would be unfair to judge Orla Mining ( ORLA ) on its per share growth for its Gold Standard acquisition while the asset is still awaiting final permitting ahead of eventual production by 2027.

Plus, if one is willing to take a deeper look at Sandstorm's portfolio, there are several positive developments worth discussing which I will highlight below:

Greenstone

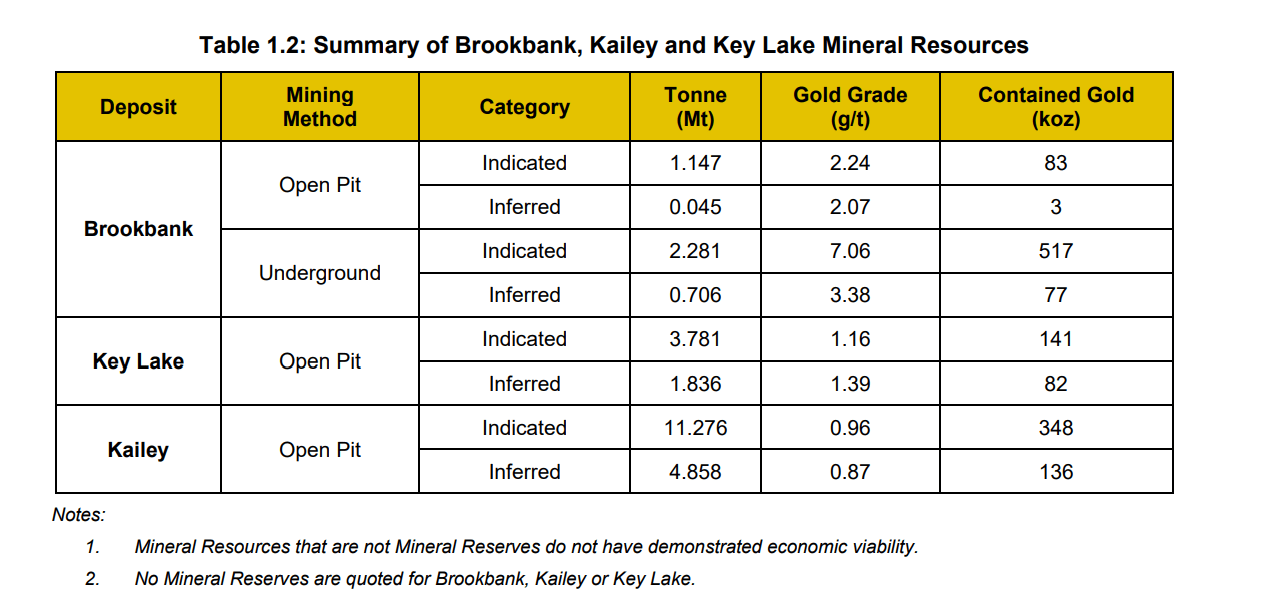

Beginning with Greenstone (SAND holds a 2.375% gold stream on first ~120,300 ounces, stepping down to ~1.58% after), Equinox Gold ( EQX ) continues to make solid progress at the asset (over 90% complete with pre-commissioning activities underway), with the company remaining on budget and schedule against all odds after massive capex blowouts at Cote Gold and Magino. This is great news for Sandstorm given that this is a 400,000+ ounce gold producer in its first five years with a payment of 20% of spot per ounce, and this should contribute ~8,500 ounces in its five first full years of production to Sandstorm, translating to over $12 million in cash flow per year starting in 2025 (full year of commercial production) from this one asset alone. Plus, it's worth noting that the stream covers Greenstone, Brookbank, Kailey and Key Lake (other deposits) and there is the project is permitted for 30,000 tonnes per day vs. a planned throughput rate of ~27,000 tonnes per day, suggesting the potential to lift throughput and potentially pull forward ounces.

Greenstone Resources ex-Reserves - 2020 TR

{kind=link}

Platreef

Moving over to Platreef which is majority owned by Ivanhoe ( IVPAF ), the asset is a monster that lies in elephant country for PGM projects on the Northern Limb of the Bushveld Igneous Complex in South Africa (Limpopo Province). For those unfamiliar, over 70% of the world's platinum is mined, with other projects/mines including Waterberg to the far north and Mogalakwena (largest open-pit platinum mine) to the north of Platreef. And digging into Platreef, the project is home to over 850 million tonnes of resources (indicated & inferred) or ~125 million tonnes of reserves, with an average reserve grade of 1.94 grams per tonne of platinum, 1.99 grams per tonne of palladium, 0.30 grams per tonne of gold, 0.13 grams per tonne of rhodium, plus additional nickel and copper credits.

Platreef High-Grade Mineralization - Ivanhoe Mines

{kind=link}

Sandstorm holds a 37.5% payable gold stream on Platreef until ~131,300 ounces have been delivered, stepping down to 80% until ~257,000 ounces have been delivered, plus 5% thereafter.

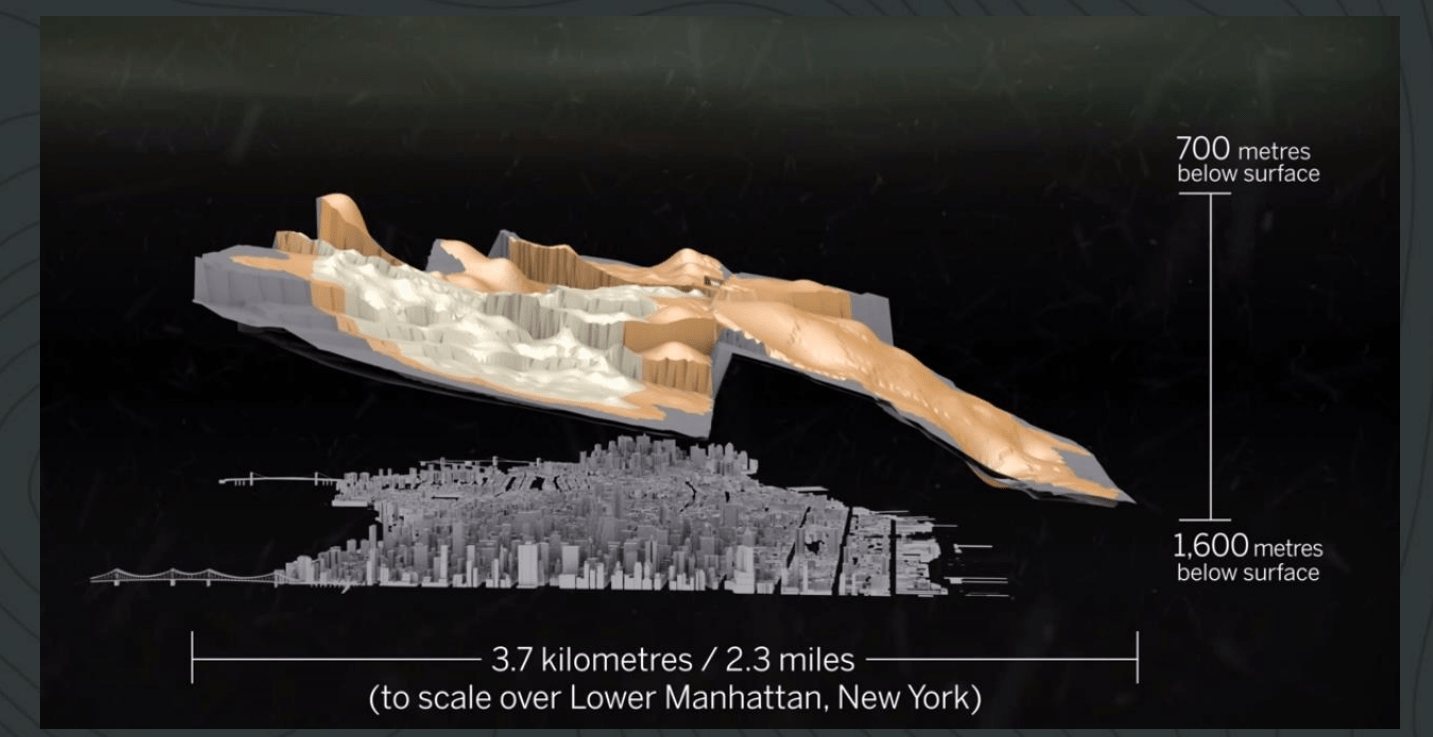

This translates to a 3P3+gold grade of 4.37 grams per tonne, and the mine is expected to be one of the lowest-cost mines globally, with total cash costs after credits of less than $550/oz even adjusting for inflationary pressures. As for the mine life, it sits at 29 years, providing a material boost to Sandstorm's weighted average mine life, especially when factoring in other assets like Greenstone, Caserones, Hugo North Extension, and MARA. And to put the sheer size of Platreef in perspective, the below image shows the ore body overlaid against Lower Manhattan in New York, with the Platreef deposit being a flat-lying reef that is 26 meters thick on average and up to 60 meters thick in some areas. The current plan is to develop Platreef in phases (~800,000 tonnes to 5.0+ million tonnes per annum), and according to Ivanhoe, Phase 2 is being accelerated and pulled forward from a previously envisioned timeline of 2030.

Platreef Deposit vs. Lower Manhattan - Nomad Royalty Presentation

{kind=link}

As highlighted in Ivanhoe Mines' Q3 results , Shaft 3 (previously expected to be a vent and secondary escape shaft) is now being equipped for hoisting, providing additional capacity to remove ore and waste. Not only will this de-risk the Phase 1 ramp-up but it will also pull Phase 2 forward from a previous outlook of 2030, with the potential for Phase 2 at significantly higher throughput rates (3.0+ million tonnes per annum) to commence by 2028. In fact, as highlighted by Ivanhoe in its Q3 results, we should see an accelerated ramp-up of underground mining for Phase 2 before Shaft 2 completion in 2027. And while Ivanhoe certainly has ambitious plans at Platreef to more than quadruple throughput with Phase 2, it's important to note that this is a very experienced operator, with the company having considerable experience with massive projects/mines, with it producing ~330,000 tonnes of copper from its world-class Kamoa-Kakula Complex in DRC last year, and working towards a Phase 3 expansion to increase production to 600,000+ tonnes per year with the construction of a new 5.0 million tonne per year concentrator.

So, what does this mean for Sandstorm?

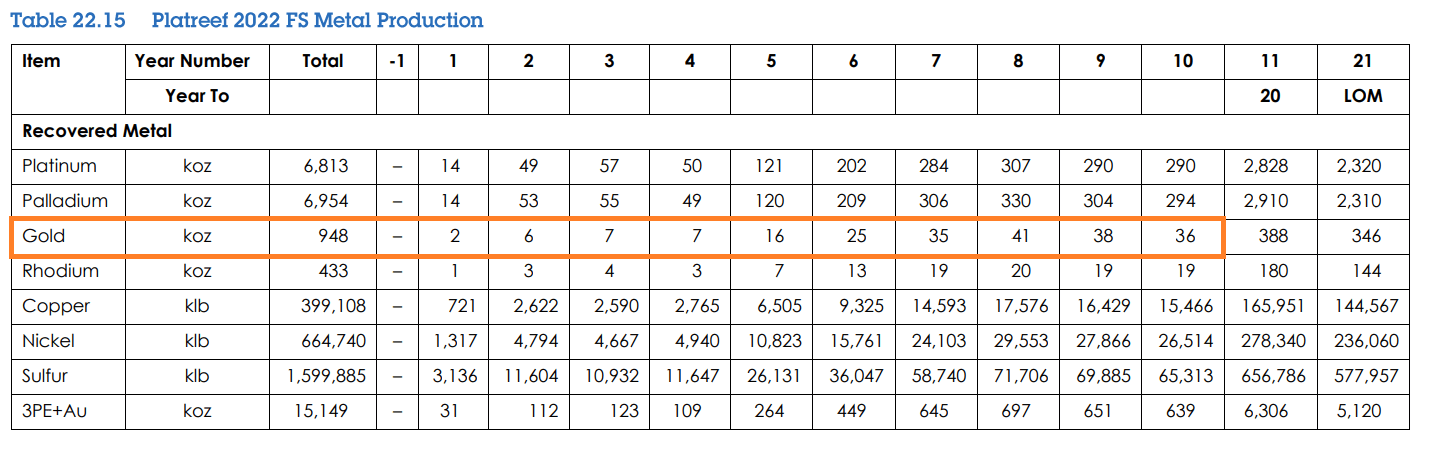

As it stands, Platreef is expected to begin first concentrate production in Q3 2024, with minimal contribution expected next year to Sandstorm based on its 37.5% gold stream. However, attributable production should average over 3,000+ GEOs for its first three years, ramping up to 8,000+ GEOs potentially as early as 2028, and ultimately over 12,000 GEOs in Phase 3 post-2030. Based on a $100/oz payment per ounce, this should translate to upwards of $26 million per annum in cash flow for Sandstorm post-2030 once in Phase 3 until the step down is hit post-2037, which to put in perspective is roughly one-fourth of the cash flow it's generating today from over 40 producing assets. Hence, this is a game-changer for Sandstorm like Greenstone, and will be a meaningful contributor on a per ounce basis.

Platreef 2022 FS Metal Production - 2022 TR Ivanhoe

{kind=link}

Hod Maden & Robertson

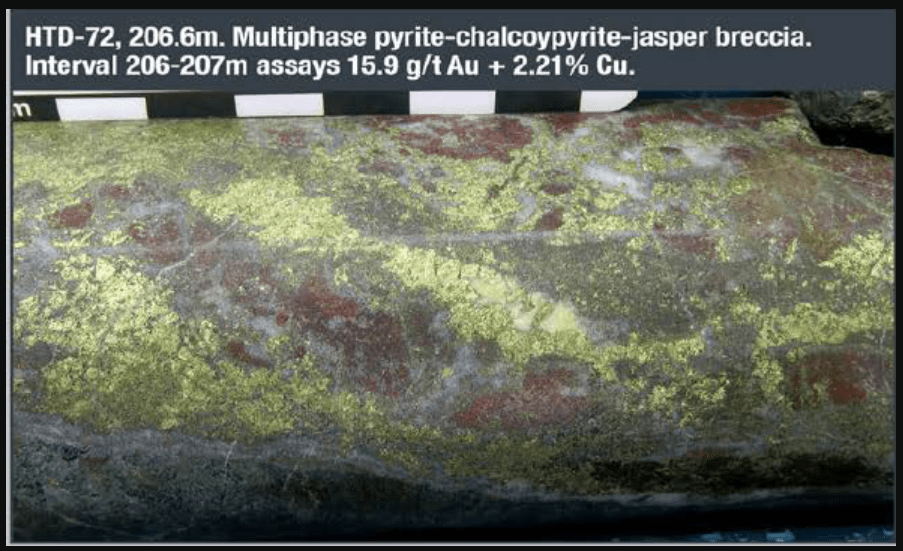

While neither Hod Maden or Robertson have begun construction yet, both assets are certainly worthy of discussion, with both held by experienced and well capitalized operators in Barrick ( GOLD ) and SSR Mining ( SSRM ) with ~$8.0 billion in combined liquidity. Starting with Hod Maden, SSR Mining reported blockbuster infill drilling results from the mine that included 26 meters at 18.5 grams per tonne of gold and 3.24% copper, 61 meters at 18.8 grams per tonne of gold and 2.26 % copper, and 90 meters at 16.5 grams per tonne of gold and 1.56% copper. These grades may not match the Aurelian-like intercept in HTG-002 of 85.3 meters at 84.3 grams per tonne of gold and 6.8% copper released in 2020 from Hod Maden, but these results and still world-class and are well above the reserve grade of 8.8 grams per tonne of gold and 1.5% copper.

Aurelian Resources hit 158.4 meters at 25.21 grams per tonne of gold in 2007 in hole 139 ahead of eventually being acquired by Kinross ( KGC ), and few if any projects have matched these grades in the gold space except Hod Maden.

Hod Maden Mineralization - Hole 72 - Mariana Resources

{kind=link}

Like Greenstone and Platreef, Hod Maden is also a game-changer for Sandstorm based on its 2.0% NSR and 20% gold stream, but it's actually far more impactful from a GEO standpoint. This is because it's expected to contribute over 36,000 GEOs on average in its first four full years of production (albeit at a higher cost of 50% of spot), making it a very chunky asset that will translate to over 40% growth vs. Sandstorm's current attributable production profile. Hence, for investors that want exposure to one of the highest-grade future gold mines with significant exploration upside with inflation protection (streaming interest vs. developer or producer) Sandstorm is one way to get this exposure at a very attractive valuation. And assuming SSR Mining delivers on its plans (2024 FS, 2027 commercial production), we will see a meaningful boost in Sandstorm's annual sales and cash flow in 2027, as shown in the below chart.

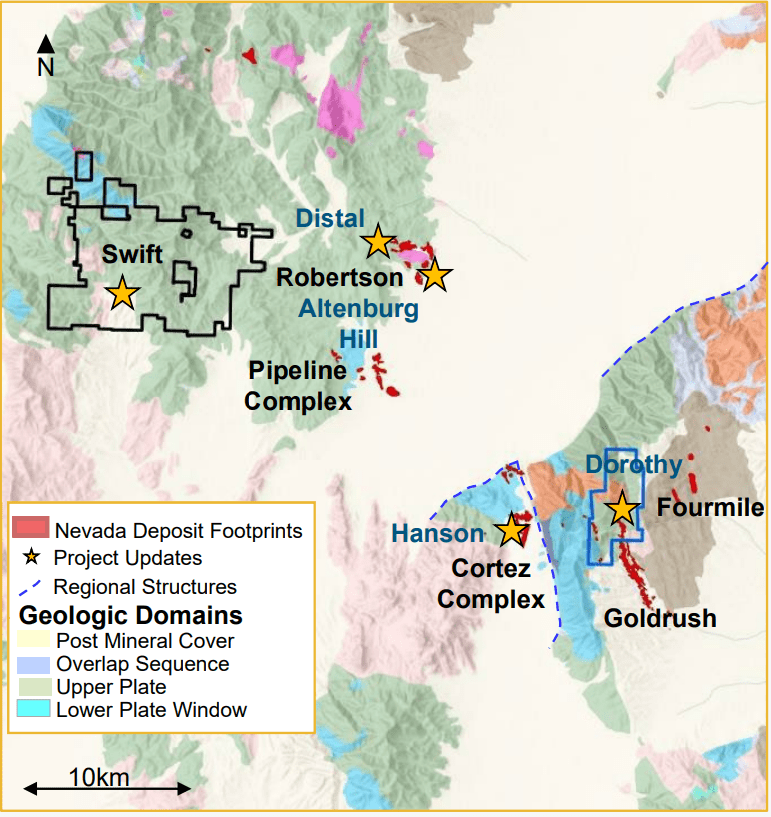

Elsewhere, Barrick's Robertson Project (an important future oxide feed for the Cortez Complex) reported maiden reserves of ~1.6 million ounces last year, but there looks to be considerable upside here. This is because the company shared that it's seeing geological continuity between the Gold Pan and Porphyry targets (shown below), and results from the Distal target have been very encouraging, with a highlight hole of 13.9 meters at 15.6 grams per tonne of gold that absolutely dwarfs the ~0.50 gram per tonne reserve grade. For those unfamiliar with Robertson, it's expected to be a 250,000 ounce per annum producer at a 2.25% royalty above $2,000/oz gold which will likely be the floor for gold post-2026 when the asset goes into production (2.0% NSR from $1,800/oz to $2,000/oz), and this will contribute another 6,000 GEOs per annum in its early years.

Robertson Exploration - Barrick Website

{kind=link}

However, given the exploration success, Barrick has outlined an exploration target of ~110 million tonnes at 0.50 grams per tonne of gold at the mid-point (~1.8 million ounces), suggesting the asset could get much bigger and potentially support a 300,000 ounce per annum production profile and or a longer mine life, pushing Sandstorm's attributable GEOs north of 7,000 per annum. Obviously, there are no guarantees here, but with the success Barrick has had to the southeast at Fourmile and the fact that this is a very important complex for Nevada Gold Mines as the Pipeline/Cortez open pits wind down, I would expect Barrick to drill this asset hard to try and grow open-pit reserves here.

MARA

Last, but certainly not least, Sandstorm has an option to purchase a 20% gold stream on the MARA Project that's been consolidated by Glencore (GLCNF) after the company purchased the majority interest earlier this year. For those unfamiliar with the asset, it is one of the largest and highest-grade undeveloped copper projects globally in Argentina (530+ million copper equivalent pounds in first 10 years) and is expected to benefit from existing infrastructure with a plan to convey ore to the existing Alumbrera processing plant. At first glance, $225 million might seem like a steep price to pay for a 20% gold stream, but there are three benefits worth pointing out here:

1) Sandstorm forks over this cash when a construction decision has been made

2) These payments are staged and shouldn't kick in until at least H2 2025, giving Sandstorm ample time to pay down its debt

3) If exercised, Sandstorm will get ~520,000 ounces in return (20% of ~2.6 million ounces of recovered gold based on reserves) at 30% of spot, translating to ~$730 million in total cash flow at $2,000/oz gold or ~$800 million at $2,200/oz gold.

It's also worth noting that the previous study highlighted the potential to fully utilize installed capacity at Alumbrera due to the softer Agua Rica ore, which would bring forward ounces and increase Sandstorm's attributable production further. Obviously, we still don't have a positive construction decision here yet so there's no reason to jump for joy just yet as a Sandstorm investor. However, if exercised, Sandstorm would enjoy ~131,000 ounces in its first six years of ~26,000 ounces per annum, translating to over $38 million in annual cash flow (this uses a $2,100/oz gold price assumption from 2028-2032), and that assumes the base case 110,000 tonne per day processing rate and not a potential ~9% expansion to 120,000 tonnes per day.

So, why is all of this important?

Putting It All Together

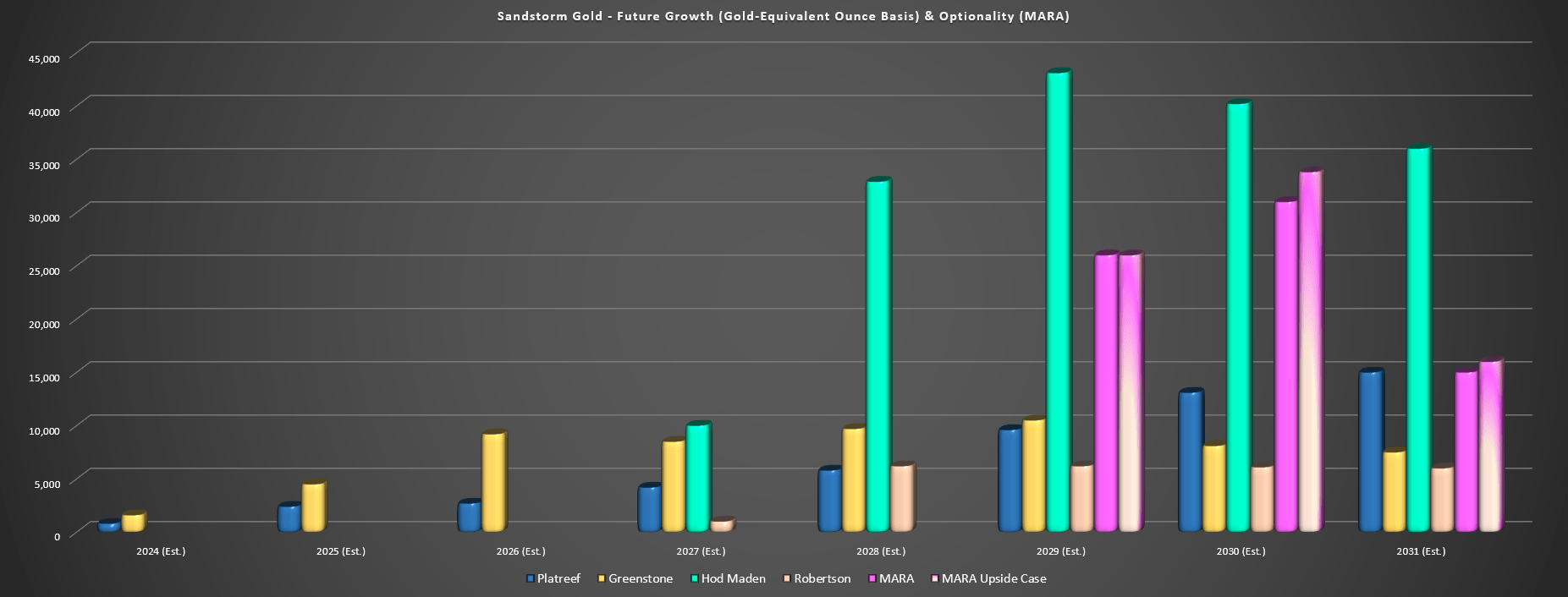

It's easy to a Sandstorm critic today and in fairness the execution the past year has been poor with a follow-on financing post M&A at depressed prices and now a plan to sell non-core assets to improve the balance sheet. And while I think Sandstorm got a great price for the assets it purchased, it's clear that other M&A was more graceful with less leverage and less share dilution so the underperformance in the stock is partially justified. However, most critics focus on the current quarter, the current year, the next twelve months or the most distressed assets (Mercedes) that make up a miniscule portion of total NAV but spend little time talking about the positives. And when it comes to the positives, two charts are worth 1,000 words.

Sandstorm Gold - Future Growth (GEO Basis) & Optionality (MARA/MARA 120k TPD) - Author's Chart, Company Filings, Author's Estimates

{kind=link}

The first is shown above, and it shows that assets that are not currently in production could contribute over 50,000 incremental GEOs per annum in 2028 and 90,000+ GEOs with peak production from Hod Maden and if MARA comes online. Importantly, this chart excludes smaller assets and another 10,000+ GEOs combined from other assets like Lobo Marte, Woodlawn, and Hugo North Extension which could kick in by 2030 or earlier, as well as other assets like Horne 5, Suruca, Troilus Gold, and Gualcamayo Deep Carbonates (which includes $30 million on commercial production). So, while Sandstorm may have flat to down production next year, it's quite clear that any step downs within its portfolio will be more than offset by considerable growth from high-quality assets over the next several years and several of these assets have very long mine lives.

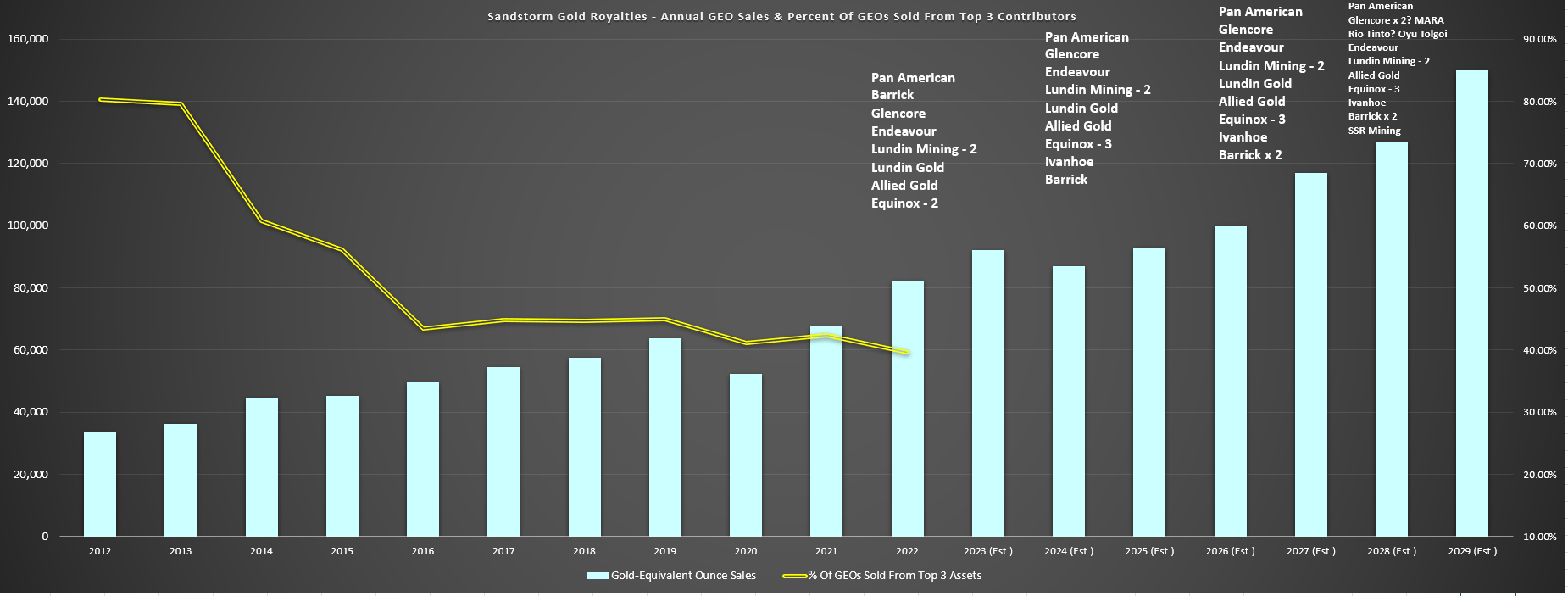

Sandstorm Gold - Annual GEO Sales + Estimates, Percentage of GEOs from Top 3 Assets & Operators/Future Operators - Company Filings, Author's Chart & Estimates

{kind=link}

The second chart is also quite important because it shows the potential progression of production, and how Sandstorm has made significant progress reducing its reliance on any one asset (yellow line = percentage of GEO sales from top-3 assets and continues to trend lower). However, the other major take-away from this chart is its suite of operating partners which continues to grow, with several of these partners being experienced and multi-asset operators with the capital to drill aggressively and potentially expand operations if they see success at the drill bit. As shown above, new partners as of the recent acquisitions include Glencore and a second asset held by Lundin Mining ( LUNMF ) in Caserones and post-2027 will include Barrick (minor partner at South Arturo, but a second mine in Robertson), potentially a second asset held by Glencore (the MARA project), and an asset operated by SSR Mining (Hod Maden).

Hence, Sandstorm will be more diversified, larger scale to start funding its assets with cash flow and accelerating growth, and also higher-quality with better partners. However, despite this positive outlook, the stock remains in the bargain bin with sentiment the worst it's been in my recollection outside of the secular bear market where the whole sector was hated (2012-2015).

Valuation

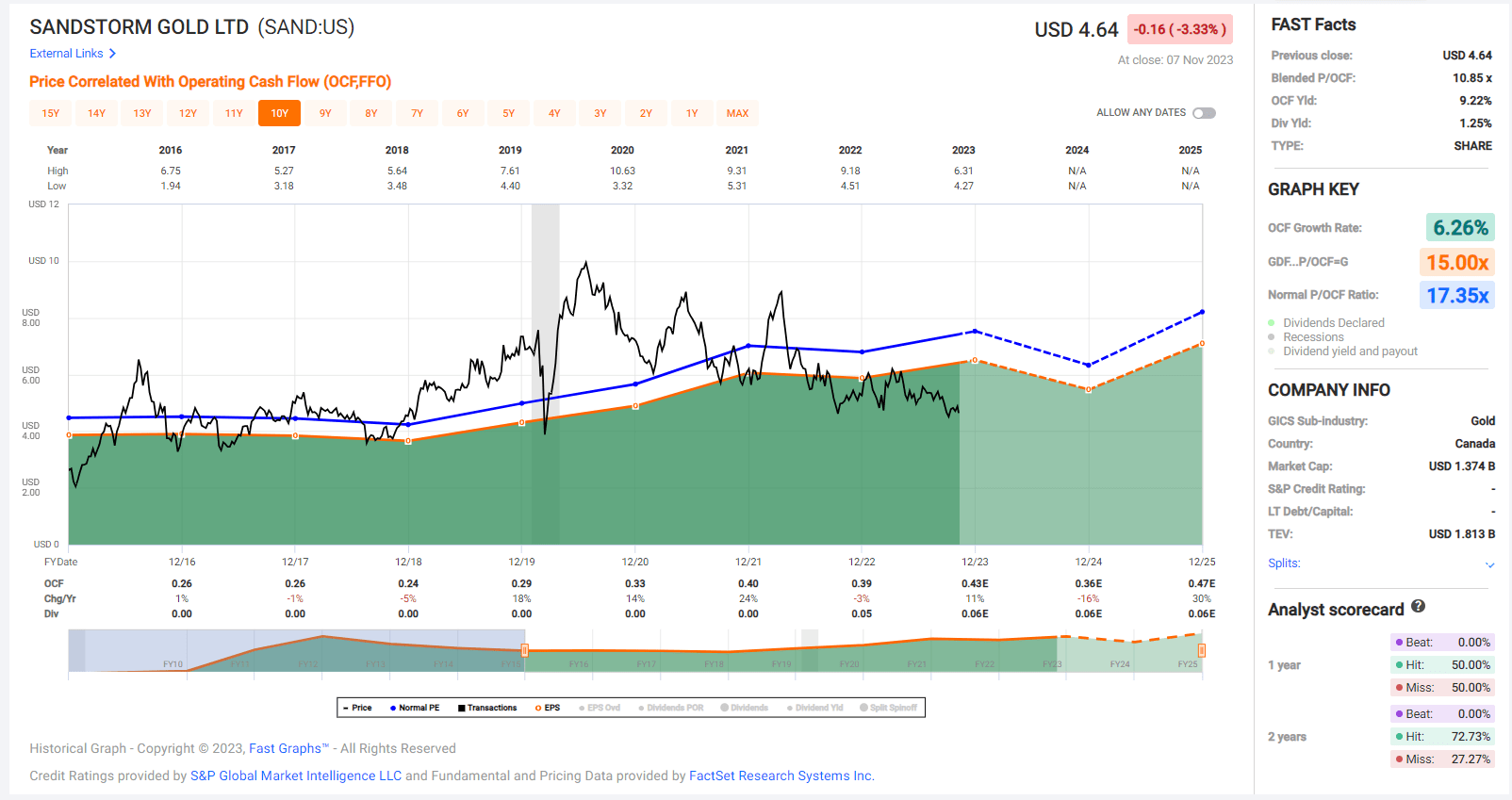

Based on ~296 million shares and a share price of US$4.50, Sandstorm trades at a market cap of ~$1.33 billion and an enterprise value of ~$1.77 billion or closer to $1.55 billion if one places any value on its loans to other companies. This is a dirt cheap valuation for a company with an estimated net asset value ($1,875/oz gold, $24.00/oz silver) of ~$1.81 billion and one capable of generating over $140 million in operating cash flow in 2025 at current metals prices. In fact, Sandstorm now trades at barely 11x P/CF (FY2025 estimates) vs. a historical multiple of ~17.4x cash flow and is currently sitting at just 0.73x P/NAV. Typically, this is a valuation reserved for a producer, not a royalty/streaming company with 85%+ cash margins.

Sandstorm Gold - Historical Cash Flow Multiple - FASTGraphs.com

{kind=link}

Using what I believe to be relatively conservative multiples of 1.30x P/NAV and 14.0x cash flow (~20% below its historical multiple) and a 65/35 weighting on P/NAV vs. P/CF, I see a fair value for the stock of US$7.50 per share or a 66% upside from current levels. And if we choose to value Sandstorm solely on P/NAV, which would be how a potential suitor would be more likely to value the company and use the same conservative multiple of 1.30x, Sandstorm's fair value comes in at US$7.95 (76% upside from current levels). So, no matter how one slices it, Sandstorm continues to trade at a massive discount to fair value, and I would expect a steady re-rating higher in the stock as it continues to pay down debt and as key boxes are checked. These include commercial production at Platreef and Greenstone, a construction decision at Hod Maden, and the real game-changer, a potential construction decision at MARA, which would translate to a similar attributable ounce profile to Greenstone and Platreef combined (~22,000 GEOs average in first six years).

Summary

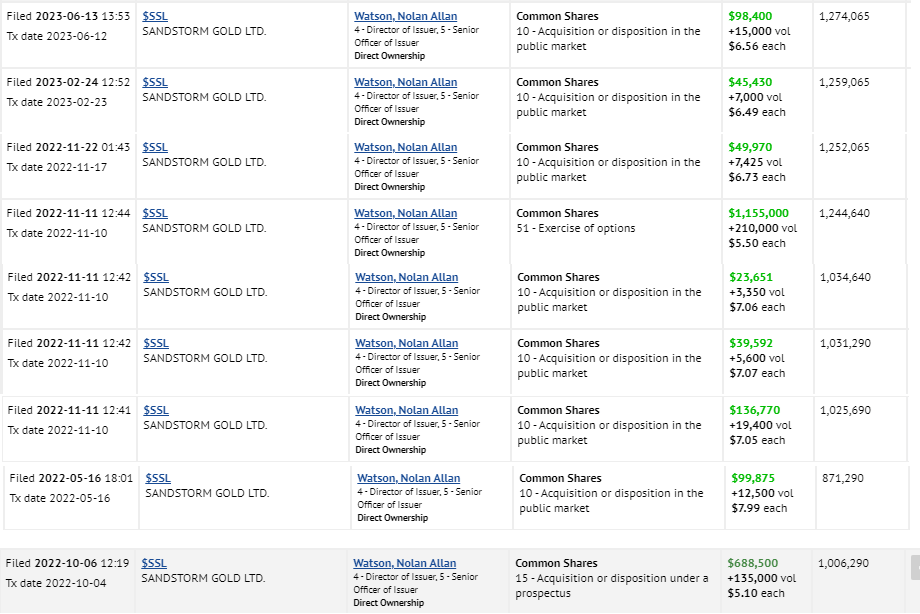

There's no question that it's been a rough year for investors in Sandstorm Gold and I was certainly quite early in my view that the stock had bottomed last year at US$5.20 per share. That said, outside of rising interest rates, the fundamentals have continued to improve, and the stock's relative valuation is now arguably the most compelling that it's been since its March 2020 lows. The improving fundamental picture includes a stronger operator at Hod Maden, the consolidation of MARA by Glencore, and two of its key streaming assets barely six months from first production, besides continued exploration success at multiple assets. So, while the share price performance is disappointing, I think this is providing an opportunity, hence why I recently added to my position again below US$4.40.

Sandstorm Gold CEO Insider Buying - SEDI Insider Filings

{kind=link}

Obviously, I could end up being wrong about the favorable reward/risk setup on Sandstorm here, and I'm wrong all the time. However, I'm happy to be overweight when a stock is the most hated it's been in years, and especially when they are sporting near negative 5-year returns (SAND: +6%) despite a solid business model. In summary, I see this violent correction in SAND as a buying opportunity, and it would not surprise me to see the stock trade back above US$7.00 within 18 months, translating to an attractive return for patient investors. Lastly, it's encouraging to see Sandstorm's CEO continuing to purchase shares at a pace well above insiders at other companies, with over $1.0 million worth of shares purchased over the last 18 months alone.

For further details see:

Sandstorm Gold: Higher Prices Likely Ahead