SASOF - Sasol Limited: A Potential Value Trap

2023-03-16 18:21:26 ET

Summary

- Be careful of Sasol Limited's price-to-book discount and 6.28% dividend yield.

- The company's asset base recently suffered from significant impairments, and its dividend payout ratio likely exceeds its sustainable amount.

- A structural break in the economy has caused oil, chemicals, coal, and gas prices to capitulate. Moreover, various indicators point toward heightened tail risk.

- Infrastructure issues persist in South Africa, lending the argument that Sasol might suffer from lagged mining production and deflated fuel demand.

- We are not bearish on Sasol's stock. Instead, we authored this article as a cautionary statement to value-seeking market participants.

I never enjoy writing bearish reports on high-quality companies for a few reasons. The first is that they possess a hint of unfairness to the firm's management team, and second, it is not easy to explain to investors that a company's recent operational performance and its stock's prospects are not always intertwined. However, somebody has to do it, so here we are.

For those unaware, Sasol Limited ( SSL ) is a South African multinational energy firm with an emphasis on fossil fuel and chemical activities such as coal mining, oil production, fuel retail, and chemical supply. Sasol is incredibly well-managed, and SSL stock currently trades at a price-to-book discount of approximately 1.51x. However, a prospective vantage point suggests that its stock possesses a potential value trap amid a structural break in the economy that has added pressure to the firm's top line. Moreover, the company has regional cost concerns, and its stock's market-based characteristics are not aligned to benefit from the current financial market environment.

Let us delve into a more detailed discussion about a few of Pearl Gray Equity and Research's latest findings on Sasol Limited's American Depositary Receipts.

Operational Update

Overview

Sasol's primary segments are chemicals and energy. The latter of the two is heavily reliant on fuel, which spans approximately 76% of the division's revenue. As for the prior, Sasol's chemicals business services industrial needs on a global basis and spans roughly 60% of the company's broad-based revenue mix.

Although the company hosts a diverse set of revenue streams, its framework is extremely reliant on industrial output, which is inextricably linked to the economic cycle.

H1 Report Assessed

Sasol released its half-year earnings report last month, revealing 26.6% year-over-year revenue growth and a basic earnings-pr-share decrease of 3%. The company guided its investors lower prior to the earnings release, citing factors such as rising input costs, the Eskom crisis in South Africa, and weaker commodity prices as critical concerns.

As revealed before, during the first half of its 2023 financial year, Sasol experienced top-line growth. However, the firm succumbed to costs. In our view, and as explained later in the article, Sasol will soon feel the burden of lower top-line growth and sustained cost pressures.

{kind=link}

Mining

The company's mining segment's EBIT fell by 5% year-over-year amid issues with South Africa's national railway company, Transnet . Civil unrest is growing by the day in South Africa, and railways are deteriorating with every transit. Moreover, due to the ongoing South African electricity crisis, Sasol will likely need to ramp up its external coal purchases amid lower throughput from its own mines, consequently diminishing its profit margins.

Gas

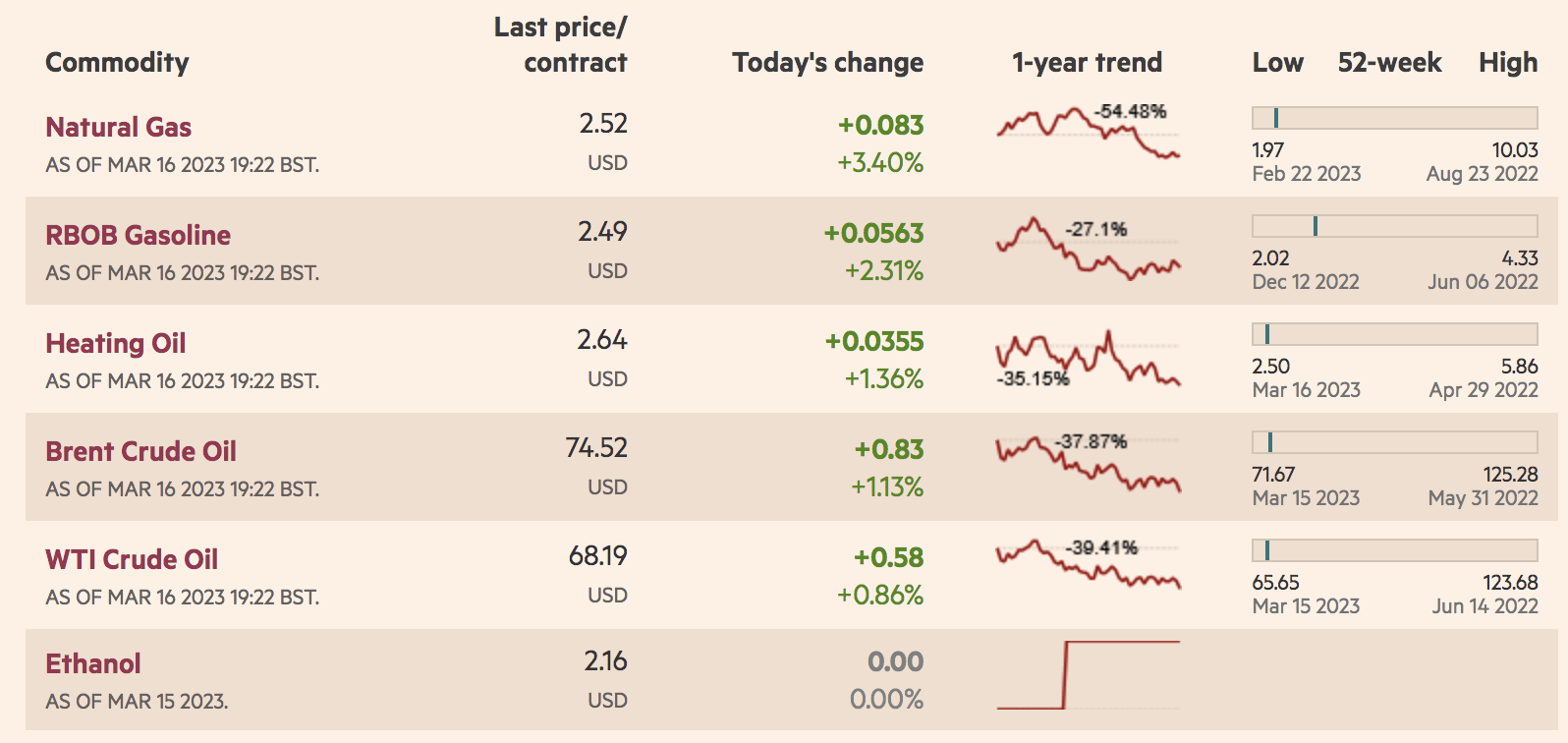

Furthermore, Sasol's gas unit has extended its EBIT by 26% year-over-year. However, a few features need to be kept in mind. Firstly, Sasol's EBIT included approximately $270 million in sale proceeds via the sale of its Canadian shale holdings, which is considered a non-recurring event. On top of that, oil, coal , and gas prices have capitulated since the start of Sasol's H1, and they are unlikely to recover, given that there has been a structural break in the economy, which includes smoother supply routes and lower core demand.

{kind=link}

On a positive note, Sasol says its Mozambique drilling plan is "progressing ahead of plan and continued with a good safety performance". For those unaware, a regional war has developed in Mozambique during the past few years, and the nation's power grid issues are rife. Therefore, Sasol's mere 2% regional decline in year-over-year production illustrates the business's robustness.

However, unfortunately, we anticipate the firm's regional operations to suffer in the coming quarters for the same reasons as mentioned before. Also, Mozambique's at runaway inflation ( 10.3% as of February ), meaning Sasol's regional maintenance and expansion CapEx might be higher than usual.

Fuels

Sasol's fuels segment saw an 11% year-over-year decline in H1 due to a suffering consumer base. For example, the company's downstream activities in South Africa were severely impacted by a regional economic decline in South Africa, which caused both individual consumers and enterprises to taper on their spending. Sasol might struggle with the same issues in the years ahead, as little is being done to suggest South Africa's economy will abate a significant drawdown induced by the capitulation of its national energy provider, Eskom.

South Africa Consumer Confidence (Trading Economics; BER)

{kind=link}

Chemicals

As per its H1 release, Sasol's chemicals business experienced year-over-year EBIT declines of 86% and 87% in Euroasia and America, respectively, while its African EBIT retreated by 15%.

Most of these losses were due to impairment tests, which remeasured the firm's chemicals asset base. Although the impairment losses can theoretically be backed out of core earnings, the size of the impairments is a tangible concern as they reflect the adverse nature of the firm's commodity price basket trajectory. More importantly, although these impairments can be recovered in due course, they convey Sasol's lower cash-generating potential in today's economic climate.

Valuation and Dividends

At face value, most would argue that a stock with a forward dividend yield of 6.28% and a price-to-book ratio of merely 0.66 is undervalued, right? Well, no, because tail risk must be considered.

As previously mentioned, Sasol's commodity basket is under immense pressure. In our opinion, most of the price risk was due to an easing in supply chains, which caused commodity prices to level after a sustained period beyond their moving averages. However, we anticipate further declines stemming from demand-side factors.

Using the U.S. as a benchmark, apart from most durable goods prices, evidence suggests that core inflation remains resilient, indicating that consumer spending power is in check. Non-core has dipped significantly, which aligns with our argument that commodities have tapered as a consequence of free supply chains. However, by going with the inverted yield curve for one reason, we think a structural break is pending, which would lead to weaker core spending power, a potential recession, or, even worse, an economic catastrophe.

U.S. Inflation Numbers for February (Bureau of Labor Statistics)

{kind=link}

Furthermore, the previously stated facts about South Africa's struggling infrastructure and Sasol's impairment losses must be considered when looking at Sasol's book value.

Lastly, Sasol's dividend coverage ratio of 2.73 is solid. However, the asset's payout ratio of 107.42% signals an unsustainable dividend, especially given the possibility that higher regional CapEx in Mozambique, lower net income, and lower chemicals segment depreciation might cause its free cash flow to equity to taper.

Final Word

Although Sasol Limited is an incredibly well-managed company with a stock that's trading at a price-to-book discount, we think investors must avoid throwing caution to the wind as various systemic and uncovered risks persist.

Sasol suffered significant impairment losses within its chemicals segment during its latest operating half-year. Moreover, a capitulation in oil, gas, coal, and chemical prices coupled with macroeconomic tail risk poses significant headwinds. Lastly, Sasol Limited is struggling with persistent systemic issues in South Africa and Mozambique, which might taper its forward-looking earnings.

With all factors considered, we assign a cautionary hold rating to Sasol Limited with an indefinite outlook.

For further details see:

Sasol Limited: A Potential Value Trap