SDHY - SDHY: High Yielding Short-Duration Junk Bond Fund

2023-03-04 06:21:34 ET

Summary

- The SDHY fund primarily invests in short-duration junk bonds to generate income and capital appreciation.

- It pays an attractive 7.6% of NAV distribution that appears sustainable at current treasury yields and credit spreads.

- However, investors need to watch out for a 'higher for longer' Fed that may continue to increase interest rates, potentially causing more duration losses.

- Furthermore, in engineering an economic slowdown, the Fed may widen credit spreads, which would be another headwind for SDHY.

The PGIM Short Duration High Yield Opportunities Fund (SDHY) invests in short-duration high yield securities to fund a high current income. It pays an attractive 7.6% of NAV distribution yield that appears sustainable at current treasury yields and credit spreads.

However, investors need to be mindful that a 'higher for longer' Fed may continue to act as a headwind to fixed income investors, especially as it tries to engineer an economic slowdown to tame stubborn inflation.

Fund Overview

The PGIM Short Duration High Yield Opportunities Fund is a closed-end fund ("CEF") that provides high current income and capital appreciation through a portfolio of primarily non-investment grade ("junk") fixed income instruments. The SDHY fund seeks to maintain a weighted average portfolio duration of less than 3 years.

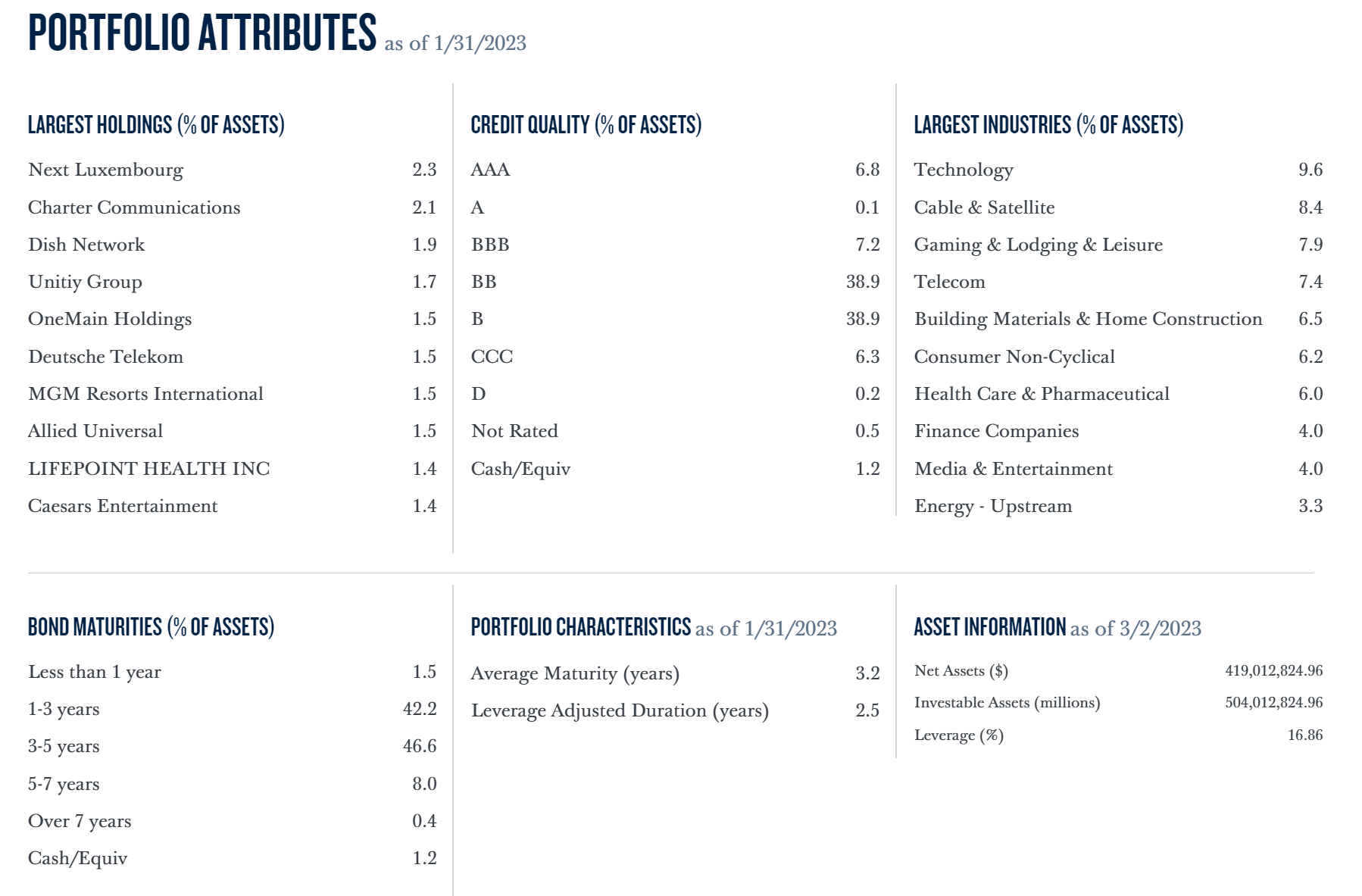

SDHY has $504 million in managed assets and $419 million in net assets for 17% leverage. The fund charges a 1.75% net expense ratio (Figure 1).

{kind=link}

Portfolio Holdings

As designed, SDHY's portfolio has a weighted average duration of 2.5 years (Figure 2).

The fund's credit quality allocation is concentrated in securities rated BB and B, each comprising 38.9% of the portfolio. Investment grade securities (BBB and above) account for 14.1% of the portfolio.

{kind=link}

Sector-wise, SDHY's largest industry weights are Technology (9.6%), Cable & Satellite (8.4%), Gaming & Lodging (7.9%) and Telecom (7.4%).

Returns

The SDHY fund has limited operating history with a November 2020 inception date. In 2021, SDHY's performance was 3rd quartile with a 4.3% return compared to the Morningstar category High Yield Bond . In 2022, SDHY delivered 1st quartile performance with a -7.9%, as the fund's relatively low duration shined through (Figure 3).

{kind=link}

Investors should note that in 2022, fixed income assets were negatively impacted across the board as the Federal Reserve increased short-term interest rates by 425 bps to fight inflation.

Returns Inline With Duration-Adjusted Index

To put SDHY's returns into context, figure 4 shows the returns of the iShares iBoxx $ High Yield Corp Bond ETF ( HYG ), which returned 4.1% and -11.4%, respectively, in 2021 and 2022.

Figure 4 - HYG historical returns (morningstar.com)

For the HYG ETF, its 3.9 year effective duration was the primary driver behind a -11.4% return in 2022. If we were to scale HYG's returns to 2.5 year duration (a first order estimate assuming interest rate shifts were constant across the curve), we should expect a high yield index fund with 2.5 year duration to return approximately -7.5% in 2022.

In fact, SDHY returned -7.9%, so its performance was roughly inline with the high yield asset class adjusted to 2.5 year duration.

Distribution & Yield

The SDHY fund pays a monthly distribution of $0.108 / share, which annualizes to a 8.4% forward yield. On NAV, SDHY is yielding 7.6%. Figure 5 shows that the SDHY fund has used return of capital ("ROC") to fund a portion of its distribution in fiscal 2022.

Figure 5 - SDHY has utilized ROC to fund part of 2022 distribution (SDHY 2022 annual report)

{kind=link}

Is SDHY's Yield Sustainable?

Regular readers of my articles will note that I am often critical of CEFs that pay double digit distribution yields that are too high relative to the fund's earnings power. With respect to SDHY, I think the analysis is slightly more complicated.

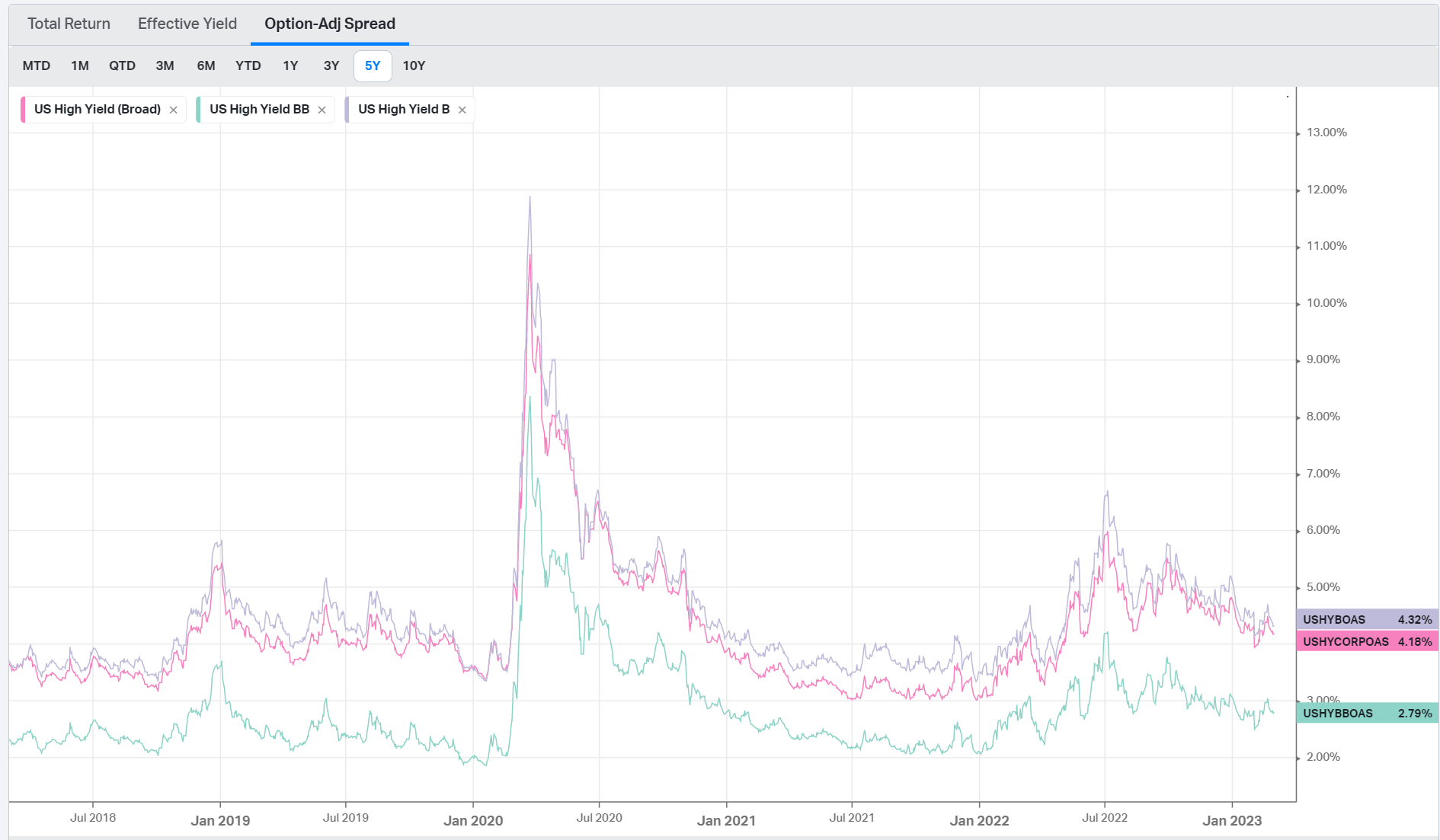

First, I think SDHY should be capable of funding its distribution out of investment income. My reasoning is simple. If we look at the U.S. treasury yield curve, we can see that after the Fed's 2022 rate hikes, we now have 2 and 3Yr treasury securities yielding 4.9% and 4.6% respectively (Figure 6).

{kind=link}

We also know that high yield credit spreads on average are trading at 4.32%, with BB credits trading at 2.79% and B credits trading at 4.18% (Figure 6).

{kind=link}

So the average 2-3Yr high yield corporate bond in SDHY's portfolio is yielding 7.5% to 9%, which should be marginally sufficient to fund its 7.6% of NAV distribution.

Watch Credit Spreads And Interest Rates

However, being able to fund its distribution does not mean the SDHY fund is without risks. As we can see in figure above, credit conditions are actually very benign at the moment, with high yield credit spreads trading much tighter than they were in mid-2022 and near long-term lows.

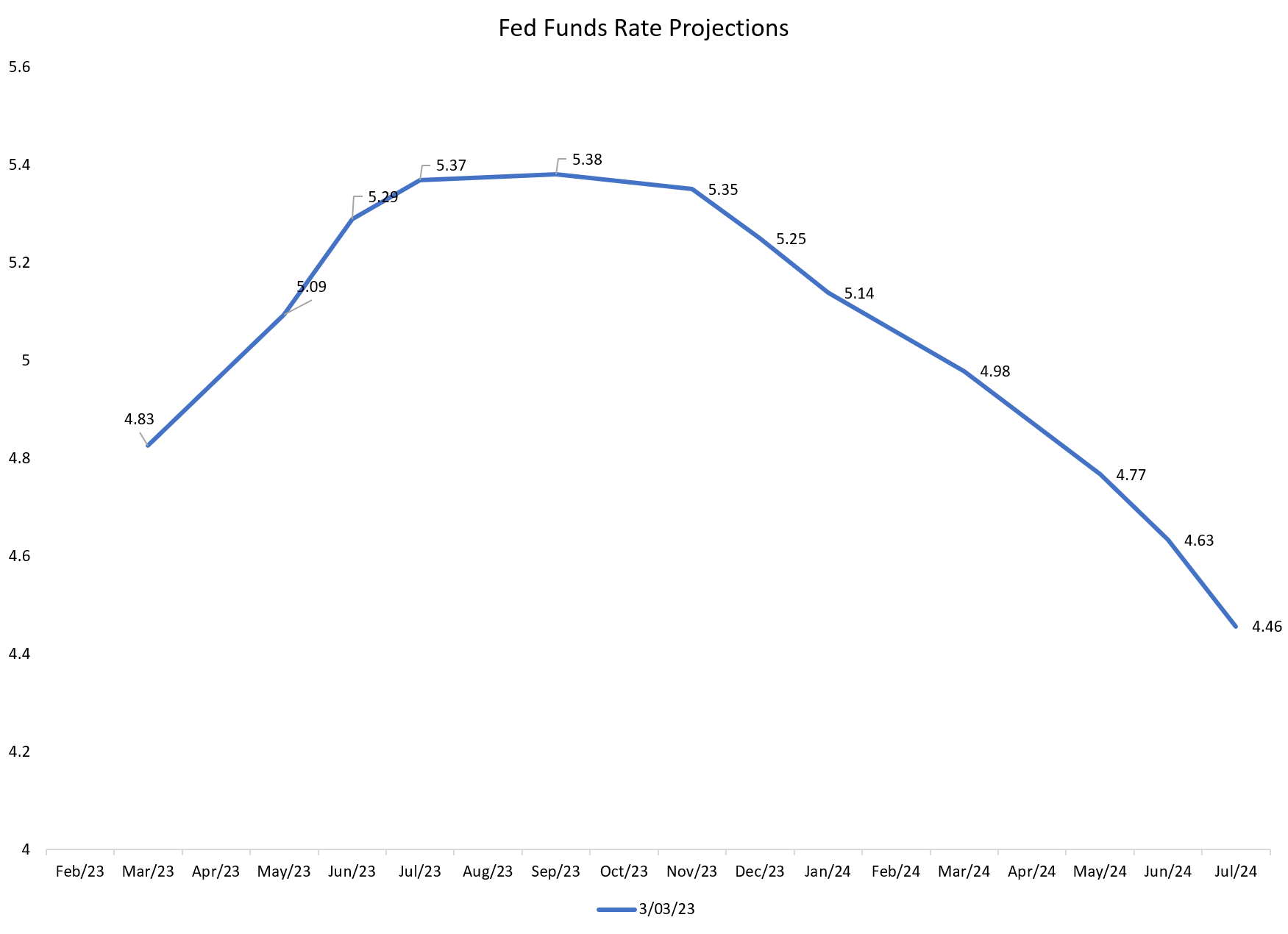

At the same time, we have the Federal Reserve vowing to raise interest rates 'higher for longer' in order to tame stubborn inflation. In fact, after a series of inflation surprises in the past few weeks, traders are now expecting the Fed to raise Fed Funds Rates to 5.38% at the September FOMC meeting (Figure 7).

Figure 7 - Terminal Fed Funds Rate expectation (Author created from CME data)

{kind=link}

If Fed interest rate hikes follow the path expected by the market, then treasury yields may have more upside, which could act as a price headwind for SDHY. Furthermore, the Fed is trying to engineer an economic slowdown in order to tame inflation, which should argue for wider credit spreads. All else equal, wider credit spreads will be detrimental to SDHY.

Conclusion

The SDHY fund is a CEF focused on short-duration high yield fixed income instruments. It pays an attractive 7.6% of NAV distribution yield that appears sustainable at current treasury yields and credit spreads. However, investors need to be mindful that a 'higher for longer' Fed may continue to increase interest rates for a few more quarters, which could be a headwind for SDHY due to its modest duration exposure. Furthermore, in engineering an economic slowdown, the Fed will mostly likely cause credit spreads to widen, which would also be a headwind.

For further details see:

SDHY: High Yielding Short-Duration Junk Bond Fund