WMT - SDY: High Yield Dividend Aristocrats May Continue To Stagnate

2023-12-04 20:09:29 ET

Summary

- Dividends are not free money but are paid out of a company's cash on the balance sheet, pressuring intrinsic value expansion over time.

- Dividend growth investing may be less attractive in the current market environment, with interest rates on competing forms of income higher than the yields of many dividend growth payers.

- The SPDR S&P Dividend ETF has underperformed the broader market and its top holdings face challenges, while consumer staples stocks, the ETF's largest exposure, are trading at rich valuations.

- We prefer the net-cash-rich balance sheets and strong free cash flow generation found within the stylistic area of large cap growth, which has been popularized by the media as the Magnificent 7.

By Brian Nelson, CFA

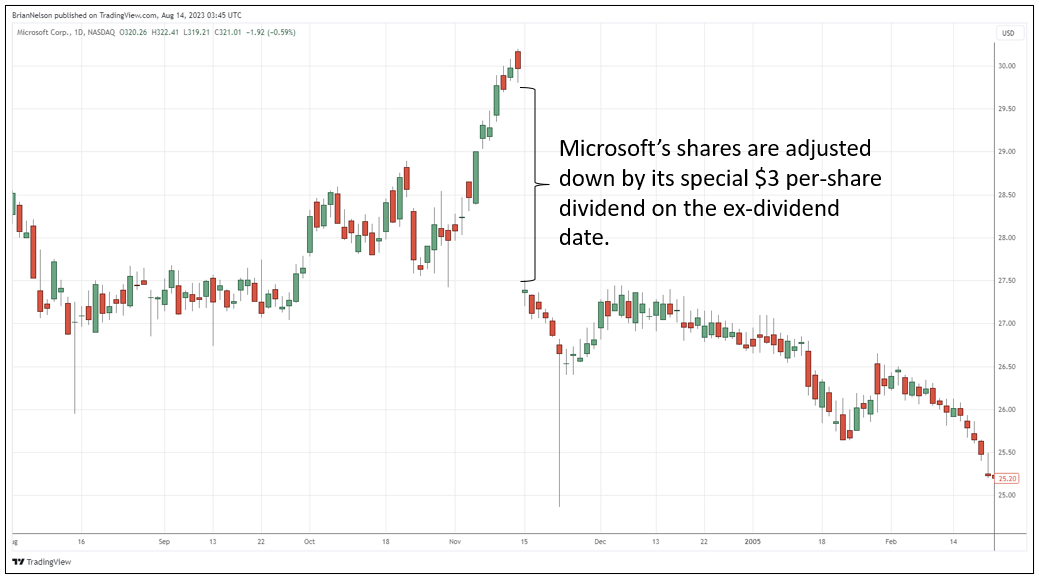

The dividend, itself, is not a driver behind a company's intrinsic value, but instead it is paid out of the cash that a business holds on the balance sheet. In general, companies generate free cash flow that can accumulate on the balance sheet, and when a company pays a cash dividend, the cash is then reduced by the amount of the dividend on the balance sheet. Since net cash is an addition to the present value of a firm's future expected free cash flows to calculate intrinsic value in the discounted cash flow method, the payment of a dividend is then a reduction in a firm's intrinsic value over time. This is why the stock price of a dividend payer is adjusted downward in the market by the amount of the dividend on the ex-dividend date (see image below). We talk extensively about this important topic in this article , and we walk through how the dividend impacts valuation in this educational article .

When a company announces a dividend, its share price is reduced by the amount of the dividend on the ex-dividend date. (Trading View)

{kind=link}

We think it is important for Seeking Alpha readers to understand the mechanics of a dividend payment because it should not be viewed as free money or like a bond coupon. As the free dividend fallacy explains, if you have a $10 stock and it pays a $1 in dividends, you now have a $9 stock and a $1 in cash dividends that either can be reinvested, can be used to purchase a different company's shares, or spent during retirement. The dividend is not incremental, but rather it should be viewed as getting paid with one's own money, as the investor already owns all the assets that the company decides to pay out. In other words, had the company not paid a dividend, the share price performance, or its capital appreciation, would have been higher due to the build-up of cash on the balance sheet. This is why it is so important to add back dividends to capital appreciation in the total return calculation.

Much has changed during the past 10 years when it comes to dividend growth investing. Years ago, the markets operated in a near-zero interest rate environment and an intense focus on dividends may have made a lot sense as alternatives to income growth were difficult to find. But more recently, the Fed's contractionary monetary policy has sent interest rates on competing forms of income (e.g. certificates of deposit) to levels much higher than that of dividend payers, namely the high yield Dividend Aristocrats. For those unfamiliar with the SPDR S&P Dividend ETF ( SDY ), it " seeks to provide investment results that, before fees and expenses, correspond generally to the total return performance of the S&P High Yield Dividend Aristocrats Index."

Looking at the high-level data for this ETF, earnings growth is expected to only be in the mid-single digits, yet the ETF trades at almost 17 times forward earnings, and the index, itself, trades at over 19 times current earnings, according to data from State Street. That's quite pricey, in our view, especially when considering that the ETF offers just a ~2.7% dividend yield, well below that of risk-free assets these days by nearly half. We include the SDY as an idea in our simulated Dividend Growth Newsletter portfolio, but mostly for diversification reasons, and to have some exposure to a benchmark, but we would not be surprised to see returns of this broader index stagnate in coming years. It just seems more reasonable for this particular index to trade more in-line with a 15x earnings multiple, as that of the equal-weight S&P 500 (RSP), given the paltry earnings growth and net-debt ridden balance sheets found among many high yield Dividend Aristocrats.

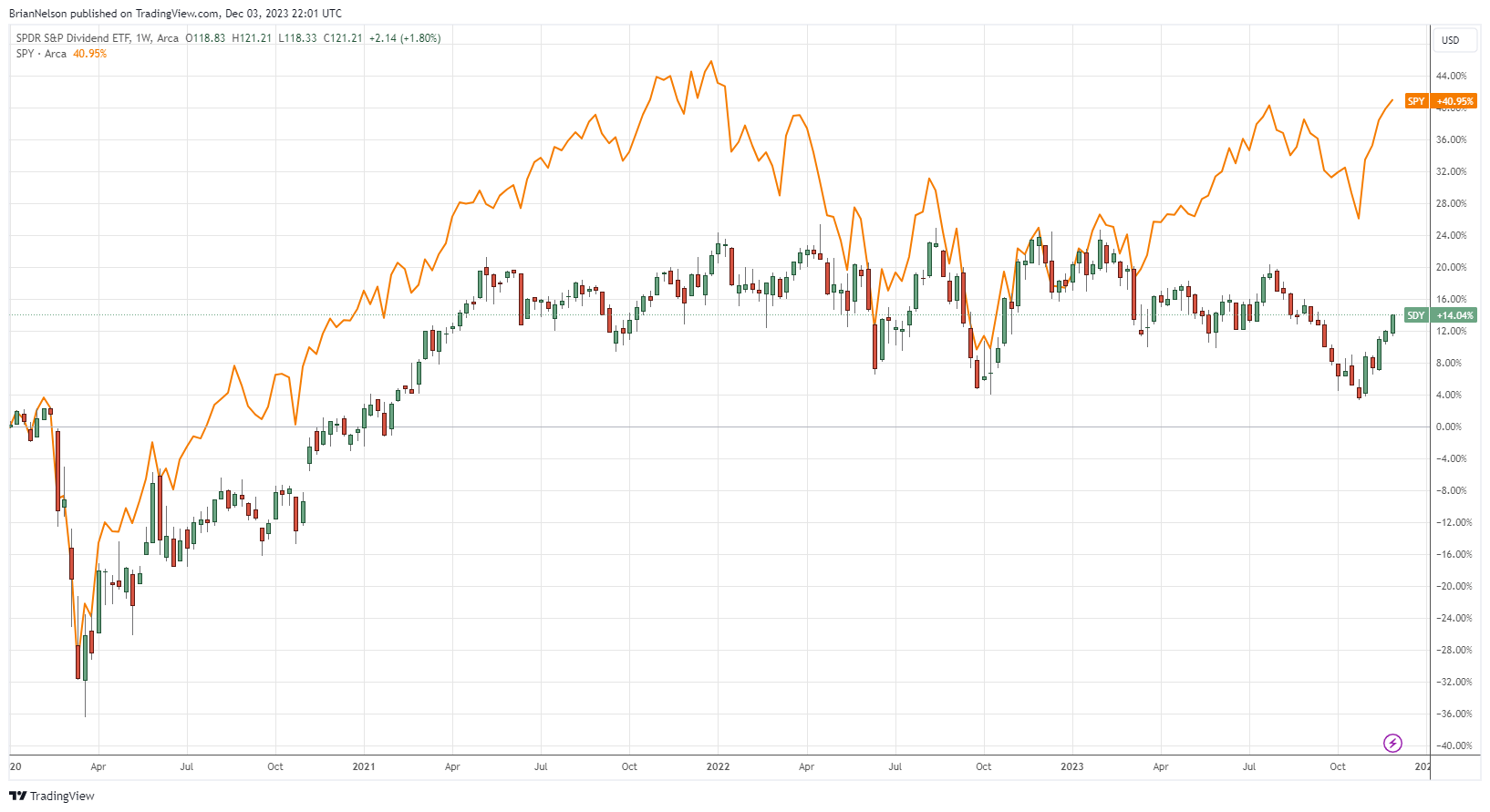

The SDY has trailed the broader market index since 2020. (Trading View)

{kind=link}

The market seems to agree that dividend investing may be getting a bit too crowded these days, with shares of the SDY down 3% so far in 2023, while the broader market-cap weighted S&P 500 ( SPY ) is up more than 20% over the same time period. From the beginning of 2020, the index has also trailed the broader stock market and really didn't have a period of relative outperformance throughout, even during the depths of the COVID-19 meltdown. As we look at the SDY today, its top four holdings leave a lot to be desired as well. 3M ( MMM ) is dealing with contingent liabilities related to PFAS chemicals and faulty earplugs. We're downright bearish on the prospects of Realty Income ( O ) as we write in this article . IBM has dropped the ball when it comes to artificial intelligence, while Target ( TGT ) is still trying to overcome its public relations misstep.

SDY Top Holdings (State Street)

The consumer staples sector accounts for more than 20% of the High Yield Dividend Aristocrat index as well. According to data from FactSet , consumer staples stocks, as a group, are trading at roughly 19x times forward earnings. Many consumer staples equities sport net debt positions on their balance sheets and are facing organic volume pressures as consumers trade down to private-label brands. More recently, entities such as Walmart ( WMT ) have been talking about disinflation and deflation, and this can't be good for many consumer staples stocks, which have grown accustomed to pushing through price increases in what once was an overheated inflationary environment. Inflation is now much more subdued, and price-driven earnings growth will be much more difficult to achieve in coming years for many consumer staples businesses, in my opinion.

Instead of high yield dividend growth equities that we believe will have stagnating returns in the coming years, we prefer the more attractive area of large cap growth that has now been popularized by the media as the Magnificent 7. This group of stocks sport tremendous net-cash-rich balance sheets and generate gobs and gobs of free cash flow. With stock prices a function of net cash on the books and future changes in expectations of free cash flow, it's no wonder why the promise of artificial intelligence [AI] has been a boon for the Magnificent 7 as the market builds in greater expectations of future free cash flow generated by the proliferation of AI and the many changes it brings in coming years. All told, we like large cap growth over the high yield Dividend Aristocrats, and you can read our cash-flow-based take on the Magnificent 7 in this article .

For further details see:

SDY: High Yield Dividend Aristocrats May Continue To Stagnate