SEAS - SeaWorld Entertainment: Taking The Necessary Steps To Restore Its Good Reputation

2023-12-19 21:07:26 ET

Summary

- SeaWorld Entertainment operates theme parks, with its flagship park founded in 1964 in San Diego.

- The company has faced controversy over its treatment of marine animals, leading to changes in practices since 2017.

- Thanks to these measures taken and considering that it is currently trading at 8x EBITDA, the valuation would offer an attractive return in a base scenario.

Investment Thesis

SeaWorld Entertainment ( SEAS ), a group of theme parks with a well-known brand, has encountered numerous challenges that have tarnished its reputation in society. From fatal accidents within the park to accusations of animal abuse, the company has faced significant public relations issues.

However, since 2017, SeaWorld has initiated changes to its entertainment model and embarked on geographical expansion, positioning itself in a turnaround situation where, based on my analysis, the potential downside appears limited. In this article, we will delve into the steps the company is taking to address its reputation problems, analyze its financial metrics, and project its profits to justify why I believe it is a ' buy ' at the current price.

{kind=link}

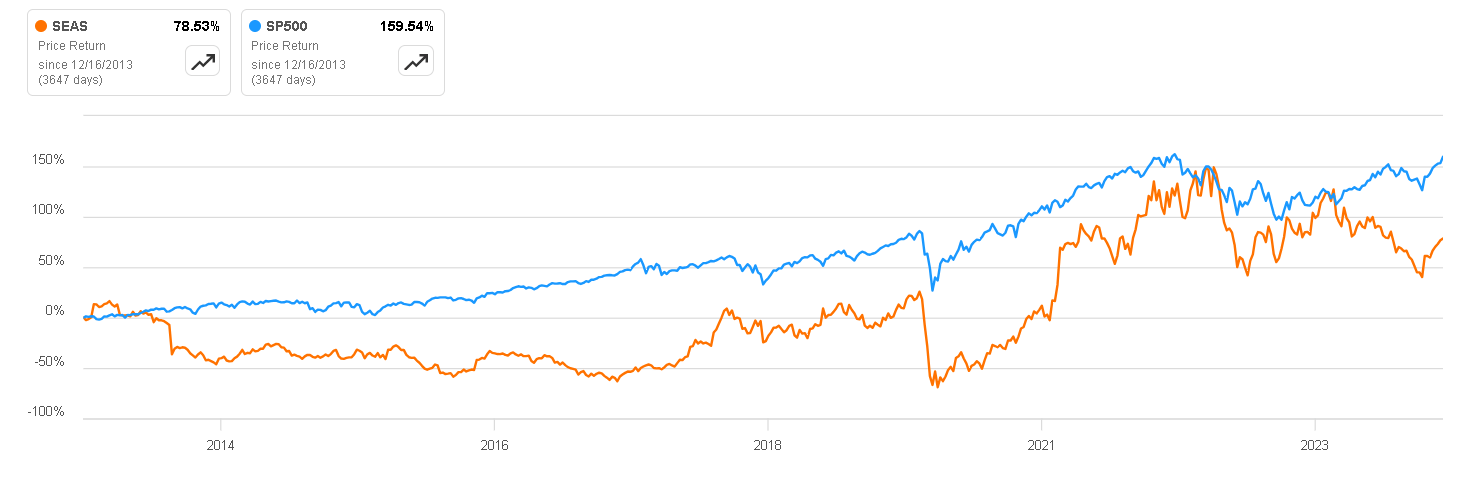

Price Performance vs S&P 500 (Seeking Alpha)

Business Overview

SeaWorld Entertainment is a theme park and entertainment company that operates a chain of marine mammal parks and theme parks. The company is best known for its flagship park, SeaWorld, which originally opened in San Diego, California, in 1964. SeaWorld parks feature a variety of marine animal exhibits, live shows, and attractions. The company's reputation is substantial. Between 2019 and 2022, three of its parks ranked among the top 10 most visited in the United States : SeaWorld Orlando, Florida; Busch Gardens Tampa Bay, Florida; and SeaWorld San Diego, California.

In addition to the three SeaWorld parks, the company also operates two Busch Gardens theme parks, four Aquatica parks, a Discovery Cove, an Adventure Island, a Sesame Place, and a Water Country USA. Recently, the company opened its first international park in Abu Dhabi—more on this later.

SeaWorld Investor Presentation

Loss of Reputation and Decline

Since its founding, one of the park's assets has been the exhibition of marine animals captured in the wild to offer shows related to orcas, sea lions, and dolphins. However, in recent years, especially since the premiere of the documentary "Blackfish" in 2013, where the practices carried out at SeaWorld were denounced, the company began to suffer from bad press , and the criticism ended up transforming into the withdrawal of advertising contracts with brands such as Taco Bell, the American Automobile Association, and some toy manufacturers, like Mattel.

PETA Campaign (PETA)

This has led to changes in the company's practices, including a shift away from breeding killer whales, announced in 2016. In 2017, the company announced the cessation of aquatic shows with the remaining mammals.

This loss of reputation and the need to reverse the trend become both the greatest risk and an opportunity . On the one hand, we can notice how since 2013 the levels of attendance at the parks have decreased, and although the company does not break down the percentage of attendance represented by the SeaWorld parks, it can be inferred that a large part of this decline is due to this loss of reputation. So, if the company fails to change the market perception about its treatment of animals and its cruelty-free service, its revenue may not grow in the coming years. Likewise, a turnaround situation could occur if the company manages to offer alternative forms of entertainment and education that resonate with visitors. This might include emphasizing conservation efforts, providing interactive exhibits, and showcasing marine life in a more naturalistic setting.

If SeaWorld can successfully navigate these challenges, it has the potential to continue being successful for many years. However, the theme park industry is competitive, and ongoing public perception and societal values will play a significant role in shaping SeaWorld's future, so this risk should not be taken lightly .

{kind=link}

Author's Representation

Key Ratios

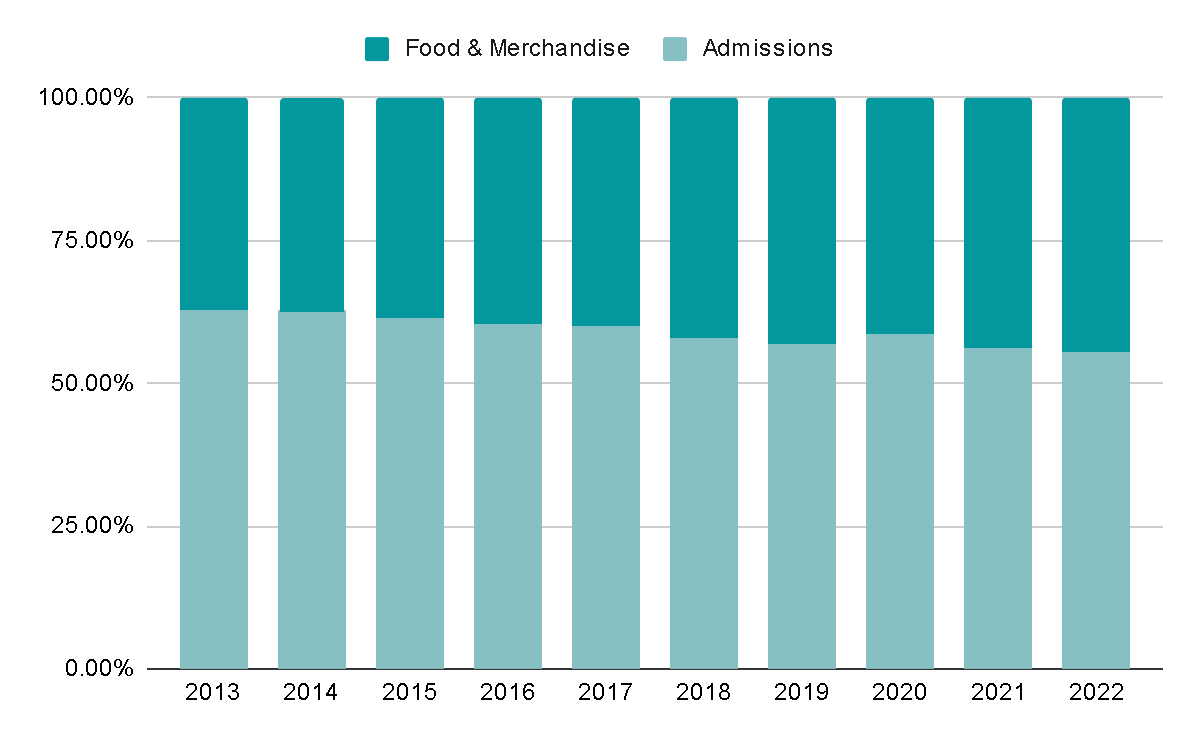

Currently, 55% of the revenue comes from admission tickets to the park. However, this category has only grown by 0.5% annually in the last decade due to a 0.7% annual decrease in park attendance. This decline has been compensated by an annual increase in ticket prices by 1.25%.

On the other hand, Food & Merchandise represented 37% of revenue a decade ago and now constitutes 44%, with an annual growth rate of 4%. This segment will play a crucial role in improving revenue per capita – the amount a person spends in a day visiting the company's theme parks. Enhancing menus at higher prices or offering value-added combos can contribute to boosting this metric.

Regarding the news of the first international theme park in Abu Dhabi, where the price of each ticket is around USD100 ( 375 United Arab Emirates Dirham ), the revenue per capita from the entrance ticket alone would surpass the current global average of USD79 for the company's parks, which includes both entrance and food. This represents another significant measure to increase revenue per capita in the coming years.

{kind=link}

Author's Representation

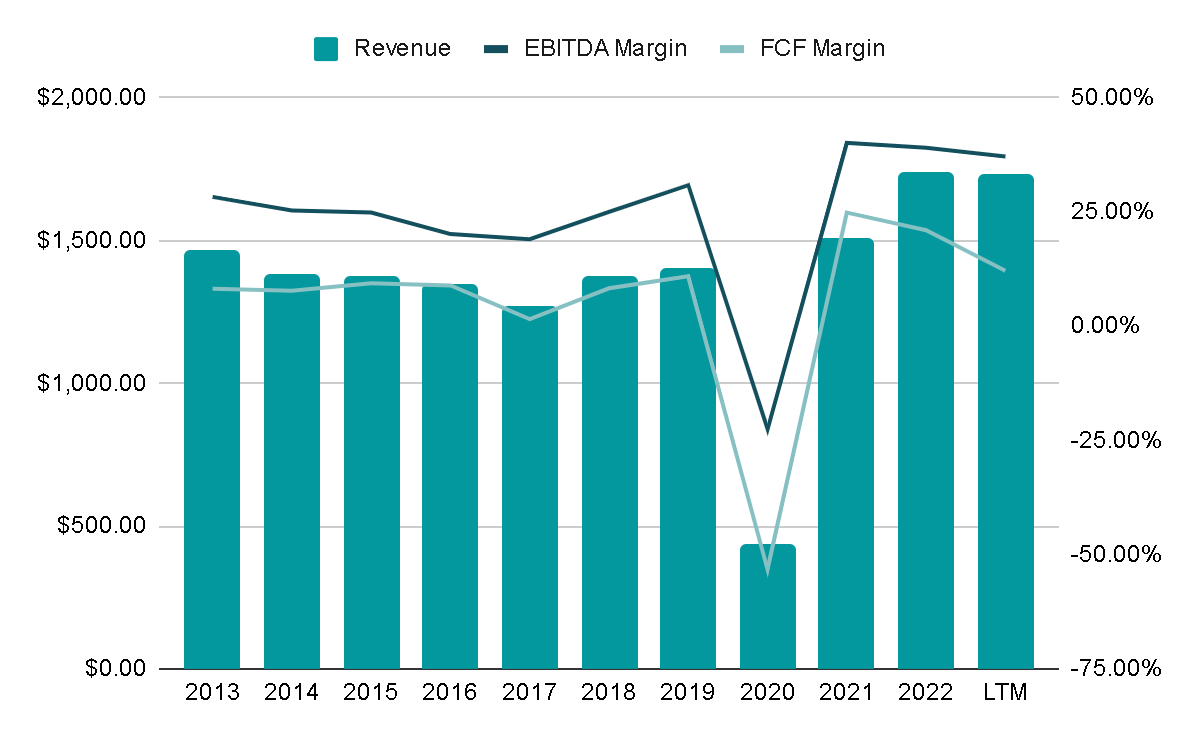

In the last decade, the company's total revenue grew at a slow rate of 2% annually. However, since implementing measures to improve the reputation of the parks in 2016 and 2017, the growth has surpassed 5% annually. The margins have also seen significant expansion, indicating a potential turnaround.

{kind=link}

Author's Representation

Between 2018 and 2021, the company relied heavily on debt to finance its operations. However, following an increase in interest rates, in 2022 and the last twelve months, the company has managed not to issue debt and relies purely on cash from operations. This showcases intelligent management with a sound capital allocation policy.

{kind=link}

Author's Representation

Capital is typically used for Capital Expenditures to refurbish and maintain parks, which are somewhat capital-intensive. It is also used to build new parks, such as the recent one in Abu Dhabi. Additionally, 63% of the capital has been used to repay the issued debt, especially that which was issued in 2020 to navigate the COVID-19 crisis. This debt was almost fully paid off in 2021.

Notably, the company allocated $1.2 billion for buybacks in recent years. They repurchased around 6-7% annually. However, during FY2022, they repurchased an impressive 12% of outstanding shares in a single year. In the last twelve months, they repurchased an additional 8%.

This buyback strategy is attractive as a means to compensate for weak earnings per share growth. For example, Net Income in the last five years has grown by 40% annually, but Net Income per Share has grown by almost 50% annually. In the long term, this becomes a significant differentiator for the performance of the stock price.

{kind=link}

Author's Representation

As mentioned earlier, the company currently holds almost $2 billion in net debt , representing just over 3x the EBITDA generated.

The debt mainly comprises a Term Loan maturing in 2028 with an interest rate of 7.45% and a Senior Note maturing in 2029 with an interest rate of 5.25%, making it a relatively expensive debt due to elevated interest rates. While this presents a challenge, the change in tone in the Federal Reserve's speech and its plans to begin reducing interest rates in 2024 comes at an opportune time. This indicates that the debt may become cheaper , and if the company manages to refinance a portion of this debt, it could reduce the amount of interest paid.

Although I wouldn't consider this debt an imminent danger, it is an aspect that could be improved, and it seems that the macroeconomic conditions are favorable for such improvements to take place.

{kind=link}

Author's Representation

Valuation

To get an idea of ??the performance we could get if we bought the shares at the current price, I will project revenue and margins five years from now and then apply an exit multiple.

In this case, I will consider two scenarios, as the company's performance could vary considerably depending on the resolution of its reputation issue. Below, I will detail my assumptions for each case.

Bear Case

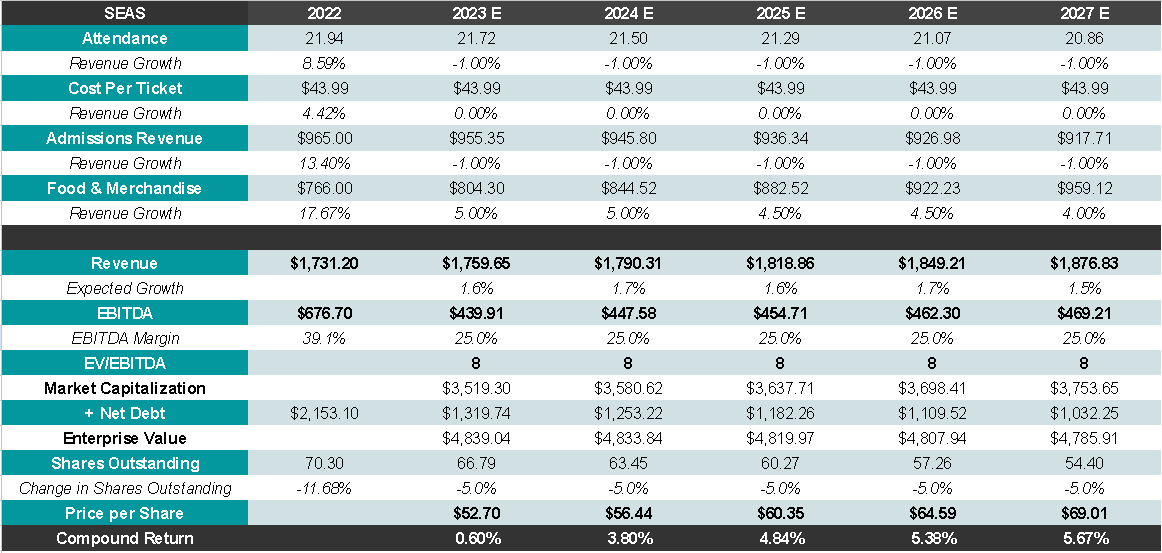

In a pessimistic scenario , the company may not be able to reverse its bad reputation, resulting in a 1% annual decrease in the volume of attendees. Consequently, they would be unable to increase the average ticket price to compensate for this decline in attendance. On the other hand, revenue from the sale of Food & Merchandise would increase by 4.5% annually.

This would yield an annual revenue growth of 1.7%. If EBITDA margins returned to the 25% of previous years and the exit multiple was 8x EBITDA, we could expect an annual return ranging between 5% and 6% .

{kind=link}

Author's Representation

Base Case

In the scenario I consider realistic , the company would increase attendance by 1% annually, and the average ticket price would rise by 1.5% annually. This could be achieved through higher entrance prices in international parks and price increases in line with inflation. The growth of Food & Merchandise would remain the same as in the previous case.

If the EBITDA margin is reduced to 30% and the exit multiple is 10x EBITDA, we could expect a return of almost 17% per year, assuming the company continues to repurchase shares at rates of 5% per year.

{kind=link}

Author's Representation

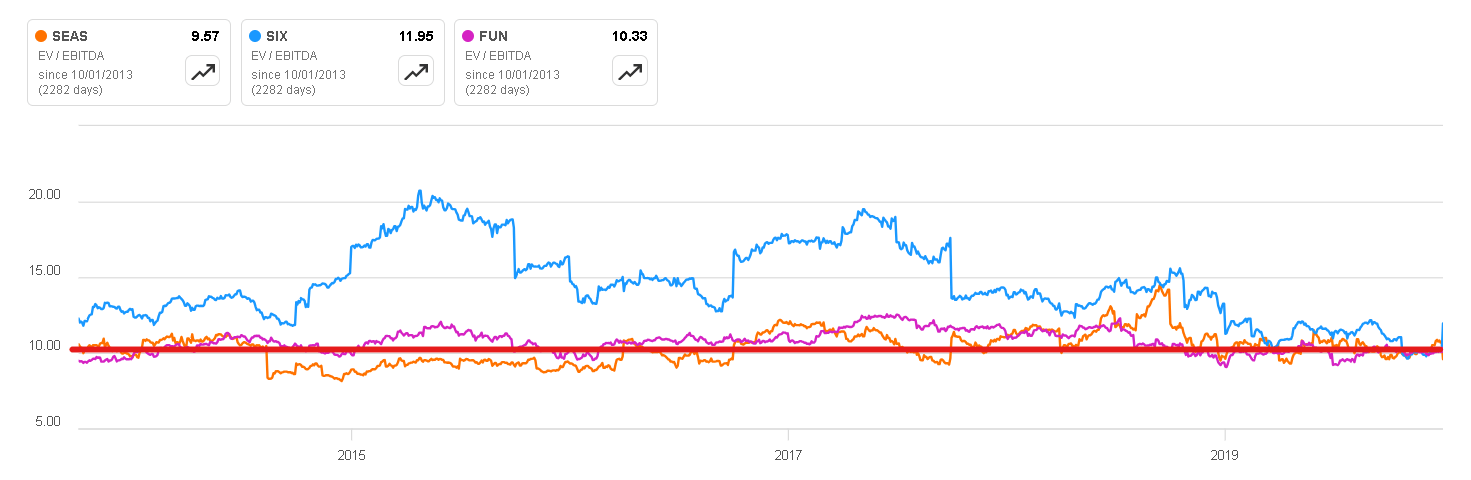

The selection of the EV/EBITDA ratio was based on the historical multiples of SeaWorld and similar companies. These are usually between 8 and 12x EBITDA, so I consider 10x to be a more than reasonable multiple.

{kind=link}

Seeking Alpha

Final Thoughts

SeaWorld's situation presents inherent risks, but it also holds interesting revaluation potential. It falls into the category of a scenario where 'if I win, I win a lot, and if I lose, I lose little .' Even in a negative scenario, the performance could be positive. In a neutral and realistic scenario with 3% growth, reduced margins, and fewer buybacks than usual, we could still double the capital in five years.

It's crucial to be mindful of the risks , which should not be underestimated , such as high debt and the company's reliance on a complete reinvention of its business model to remain successful.

Considering all these factors, I have decided to assign SeaWorld a ' buy ' rating. I find the starting point attractive, providing a sufficient margin of safety in a company that, despite undergoing a significant transition, if executed correctly, the 'SeaWorld' brand is recognized enough to return to visitor growth and I believe that the company has been taking appropriate measures to make possible this turnaround story.

For further details see:

SeaWorld Entertainment: Taking The Necessary Steps To Restore Its Good Reputation