SCTBF - Securitas: The Way To Go With This Investment Involves Options

2023-08-13 03:50:11 ET

Summary

- I have been invested in Securitas for the past 5 years, entering and exiting based on valuation and uncertainty.

- Securitas has declined significantly due to structural issues, but there is an upside and undervaluation opportunity.

- The company's profitability has been affected, but gross and operating margins are slowly improving. Debt levels are high and need to be reduced.

Dear readers/followers,

My work on Securitas ( OTCPK:SCTBF ) has been recurring, albeit infrequent compared to my coverage of other companies. This should not be misconstrued as disinterest or a lack of skin in the game for the company. I have, more often than not, held some sort of position in this business for the past 5 years - entering when good prices reign, leaving when I see overvaluation or uncertainty and am able to do so with a profit.

At this time, what I see will be covered in this piece - because there is an appeal in certain ways, and there is an upside to be had here.

In this article, I'll be clarifying the upside, and the undervaluation opportunity that Securitas, despite everything, does present.

Securitas - upside from low-margin security services

So, the last time I covered Securitas was actually well over a year ago. The company has declined significantly. I sold out of most of my position before the decline here due to structural merger issues and was proven right at the time. I then bought back in at a better price, though at a marginal position/size compared to my original stake.

This is a foundationally good company facing structural issues. Security services are a low-margin business overall. It would be an exaggeration to say that Securitas struggles with profitability. The company is definitely profitable, but its net profitability has been affected over the past few years, dropping from a higher level to a lower level of a single-digit profit margin. The company's gross and operating margins are intact and are slowly improving as of the full year and the quarterlies, which creates an interesting position.

I say the company is foundationally sound. But this is somewhat at odds, at least if you don't understand the company's business model and its safety, its current debt, and other metrics. Interest coverage is down to below 6x, and the debt/EBITDA due to mergers is still just north of 5.8x. That is extremely high for this company.

The business has a plan to carve and cut into this and reduce it - but it will take time. This is a core reason why the company is currently being traded down. Fundamentals are a big thing.

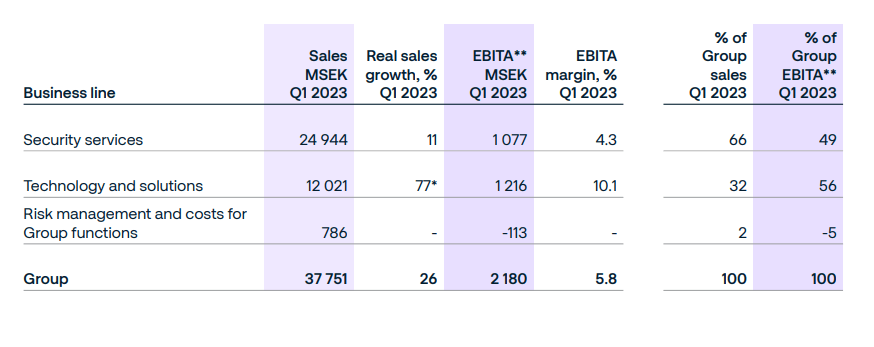

Here is a high-level view of the company's current business operations and the profitability we're seeing from them overall.

{kind=link}

To anyone familiar with the sector, this should in no way be a surprise. These sorts of companies tend toward relatively high operating expenses and costs, driving net income down - though sub-4% is lower than the company has been historically. Unfortunately, significant improvement is unlikely in the short term.

The reason that it's important is that even if we're seeing improvements and momentum in key areas, which we are, the company is facing years of paying down its debt, with higher interest costs than previously. These cost headwinds combined with continued inflation, and considering the number of employees the company has, means that I don't really see substantial bottom-line improvements in the short term.

I expect an operating margin at or around 6-7% going forward, driven by digital and tech improvements, while some fundamental advantages will cause organic sales growth. For 2Q23, we saw some of these things confirmed and materialized.

This includes solid organic sales growth, with double-digit growth as expected in the tech/solutions segment, and positive momentum from significant contract renewals. It's also coming in at a substantial operating margin improvement - 70 bps.

The company reported a 9% improved operating cash flow - but that number, despite that overall improvement still came in negative at -9M SEK.

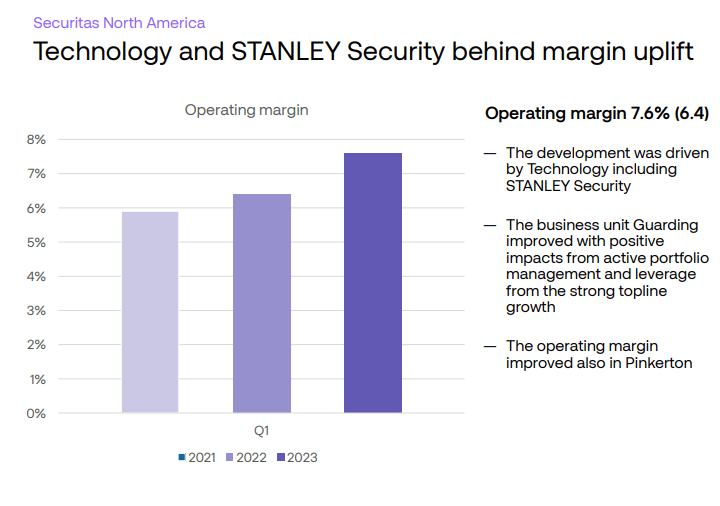

The big questions for the quarter are/were the interaction of STANLEY as well as the downpayment of debt. Because on a high level, the shift in the company's services is going well.

{kind=link}

With the shift, I'm referring of course to a higher percentage of the company's revenues coming from Tech & Solutions, which is what we want to see given the relative cost advantages of the sector compared to traditional security services. Both segments will still be important going forward, but it's growth in the former that I'm interested in here.

The company also uses geographical segmentation. NA has fully recovered its organic sales growth since cratering in early 1Q22. Major client renewals and good new business is driving sales, together with a continued healthy order backlog. Overall client retention is actually down 2% - to 85% from 87%, but this shouldn't worry you overly much. There's still a lot of instability in the market, and I'd be more worried if this becomes a trend.

The focus should be on the margin improvements driven by STANLEY and the tech sector, which are significant no matter how you slice them.

{kind=link}

But if you think NA looks good, EU looks even better. The geographical segment managed organic sales growth of 13%, with strong price increases and organic sales growth. Some inflation adjustment is in order, especially given the Turkish exposure. However, in the Securitas Europe segment, the retention rate for clients remains at an impressive 90%+.

One of the issues faced by the company at this time is actually labor shortage. Subcontracting and start-up costs are up, and despite increased top-line, the operating margin in Europe hardly improved at all, only by 10 bps, which I would deem to be little more than a rounding error here.

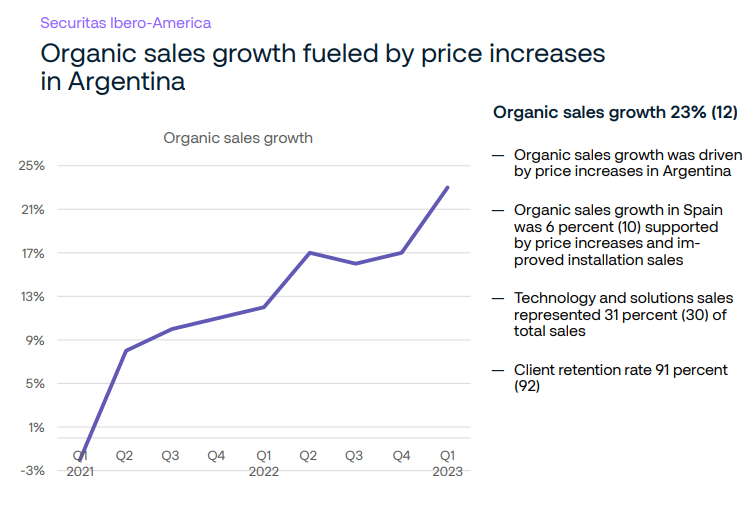

Ibero-American security remains one of the company's growth vectors. Solid trends were recorded here, and the sector has one of the strongest retention rates out there.

{kind=link}

The company is going into this interest rate environment with comparatively high debt and interest costs, as well as an ongoing transformation program in both Europe and Ibero-America, which are still slated to cost well over 1.1B SEK over the next year or so. The total costs, including everything for 2023, is set to be somewhere between 500-600M - and that's net of other incomes, at an FY2023 IAC basis.

Because Securitas is Swedish, this comes though at a massive FX tailwind. Given the weak state of our native currency, the exchange rates and the laggard nature of our currency in its current state, which is almost 15% higher than a year back, are driving some significant changes in both sales and income.

The thing I'd want to put my focus on, however, is neither FX nor sales, but debt. FY22 and the M&A of STANLEY saw the company's net debt/EBITDA balloon to a level of 4x net debt/EBITDA, from a low level of 1.9x. This level is, as of now only marginally improved. 1Q23 saw the leverage at around 3.8x, or around 41B SEK of net debt based on March 2023, which is actually up due to IAC and FCF.

This is not worrying as such , not from a higher perspective, given how conservatively indebted and laddered these maturities are. Securitas, for instance, has nothing coming due this year.

Securitas IR (Securitas IR)

The company also lacks any financial covenants for this debt, and still has over 5.3B SEK of liquidity, with an over 10B SEK revolver that's still completely undrawn. The bridge facilities for STANLEY are also not really worrying. This is reflected in S&P Globals' unchanged credit rating for Securitas here, which is completely unchanged from 2022, and still is at BBB-rating. The company continues to value this, which should be noted - I believe that Securitas values IG above its dividend, and well it should.

Here is the "new Securitas" and its targets.

{kind=link}

I am on board with this plan - obviously, otherwise, I wouldn't be invested in the company. I do believe that the EBITDA margins are lofty and may not be delivered, but I'd personally be happy with a 4-4.5% net margin for the company, as long as the forward focus is on a more tech-heavy sales mix, with reduced exposure to personnel and wage inflation.

With that, I'll move to valuation for Securitas.

Securitas - Valuation is tricky

So, the valuation for the business isn't easy here. How do you value a company that, despite a good business model, is probably in for a number of years of overall "pain" due to financing/debt costs and transformation costs while paying a yield that is without a doubt below the risk-free rate?

There are ways to go about doing just that. One option is long-term investing - ignore the debt, which is close to 50% of LT debt/cap here, and focus on nearly 4% yield coupled with eventual upside from earnings.

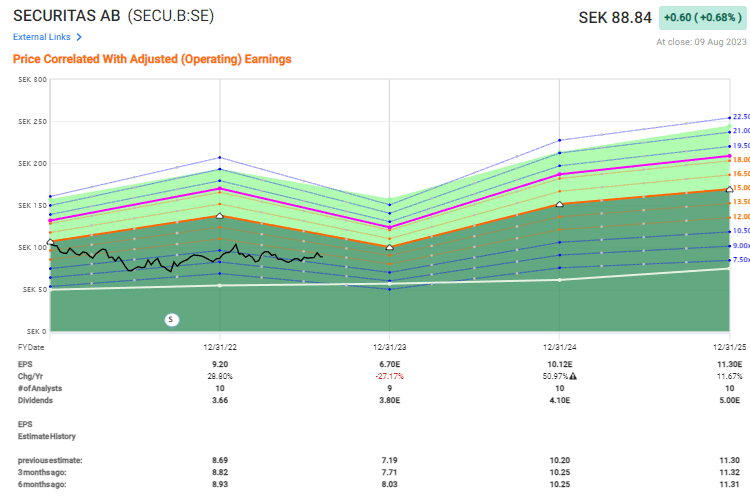

The fact is, the company is forecasted to increase earnings by a massive amount due to the STANLEY M&A and this new formula. Take a look at some of those expectations here.

{kind=link}

Why wouldn't you invest here, right? The upside in 2025E if we do see this sort of development, and 15x P/E is a thing, then we see triple-digit returns.

But before you get out your wallets and start deploying capital, dear readers, let's make a few things clear.

First of all, Securitas is not good at hitting targets. Analysts here have a negative miss ratio of 50%+ on a 1-year basis with a 10% margin of error. There are plenty of issues with estimating a 50%+ EPS growth rate from a company with a sub-4% net margin.

So, let me just say "no", - I have issues with that forecast.

That's number one. Based on a 20-year growth rate of single digits, any such upwards momentum is unlikely to be sustained. Between the years of 2008 to 2016, the company barely grew 4-5% per year.

That being said, the company is clearly cheap here. The upside is clearly there. If you're willing to wait, you're likely to get paid. That's why analyst PTs, all things considered, are very solid here with a good upside in the double digits.

S&P Global analysts, 12 of them, give SECU-B as a native symbol a range of 70 SEK low to 150 SEK high - a massive variance, with only 3 analysts at a "BUY", but with an average PT of 101 SEK. Most of the analysts are at a "HOLD" here despite the upside you're seeing in the illustrative example above.

I would say that this is how I also view this investment here - with care.

So why am I positive, and why do I think you can go long the company here?

Aside from writing cash-secured Puts at attractive prices, there are multiple avenues into an investment like this. Securitas falls into a category of investments where I believe the company is attractively priced for the longer term, warranting a "BUY", but may not outperform in the 1-2 year term due to pressures/headwinds.

For that reason, the avenue of investment I've done here is a high likelihood of 16.65% returns annualized until December of 2023.

How have I done this?

I buy-wrote a covered call/shares on Securitas at a share price of 90.53 SEK , while writing the strikes at 83.21 , giving me an effective cost basis of 80.28 based on a premium of 10.25 SEK, and a real intrinsic premium of roughly $30 contract sold, and I sold several dozen contracts.

My highest possible return until December of 2023 is 16.65%. If the company is at or above my strike at that time, I will sell the company, netting the premium and expecting one already-declared dividend of around 2% payable prior to the expiration.

If the company is below my strike , then it's likely that I will keep my shares, but at an effective cost basis of 80.28 SEK, which makes the company a very good investment in my book, with a conservative upside of a 16x P/E of almost 140%. It's also likely I will write further calls if this happens to enhance my returns further.

As I've said - the minimum return that I "want" is 15%. In this case, I managed 16.65% conservatively, and that's what I like here.

Here is my thesis for the company.

Thesis

- There's a lot to like about the security company Securitas, which is a worldwide known brand and business. The company's current challenges notwithstanding, I believe long-term investment makes sense at an attractive entry price.

- For the next 12-18 months, the pressure in earnings, inflation, costs, and integration call for this to be a riskier investment. My strategy dictates that I work this differently, and I've done so with buy-writes, annualizing over 16% RoR.

- The company is a "BUY". I give it a long-term PT of 110 SEK/share, but there may be a long time before this is realized.

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

For further details see:

Securitas: The Way To Go With This Investment Involves Options