SCTBY - Securitas: Why There Could Be A Reckoning With An Upside

2023-12-18 15:49:06 ET

Summary

- Securitas has consistently underperformed the market due to operational issues, making options plays a favorable strategy.

- The company's profitability has been affected, but gross and operating margins are slowly improving.

- Securitas has achieved price and wage balance, improved net debt, and realized cost synergies, leading to margin improvements.

Dear readers/followers,

For the past year and more, Securitas ( SCTBY ) has been a sub-par overall investment. I say that because the company has consistently underperformed in the overall market, while we've seen significant surges across the sector. Now, there are reasons as to why we've seen such underperformance on the part of this company - and they're operational.

When we have company issues that turn out to be operational, not related to mispricing in the company's valuation alone, then I tend to favor options plays, because it takes away some of the risks if I can get the company at a price I believe to be attractive.

In this case, this has been a very successful strategy.

I've consistently been able to expose capital at attractive strikes, and have never been ITM on a Securitas option in 2023, and I don't expect to be ITM for the options that expire today either.

I believe the time is ripe for a quality update to this company and to see where Securitas might go on a forward basis.

What are the issues here that I am talking about, you might ask?

Well, I have bought shares in Securitas for the past 5 years, entering and exiting based on valuation with both common share purchases as well as with options.

So let's see what we have going for us here as we move into 4Q23, looking at 3Q23 and the upcoming full-year results.

Update for Securitas AB

Security service businesses like Securitas remain low-margin businesses overall. It's not surprising, therefore, to see low margins for the company. However, at the same time, It would be a clear exaggeration to say that Securitas struggles with profitability.

The company is profitable, but its overall net profitability has been affected over the past few years, dropping from a higher level to a lower level of a single-digit profit margin.

However, we have a number of very significant changes from where the company was during 2022 and when the share price was at trough-level valuations.

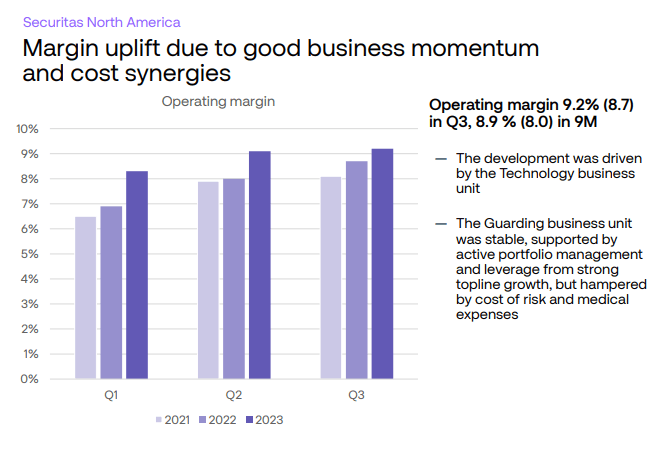

As of 2Q23 The company's gross and operating margins were intact and are slowly improving as of the full year and the quarterlies, which creates an interesting position, and in 3Q23 we saw a continuation of this trend. 3Q23 is the quarterly report that I am looking at for comparison here.

Not just a slight continuation either. The margin improvements were significant. The company was able to report an organic overall sales growth of 8% for 3Q23, which is sequentially higher and higher on a YoY basis as well. The fact that this was driven mostly by price increases is only a small issue - as the company's sales show that demand for Securitas services continues to be high.

This continued level of demand will be something to be on the lookout for in the next few quarters - and to make sure that margins remain solid.

Overall, operating margins improved by 40 bps YoY, which again might not sound much, but is a lot for this sort of business. All three of the business segments are contributing actively to this improvement, which means that the company is showing a turnaround here. Securitas has in fact achieved a price and wage balance on a group-wide basis for YTD 2023.

Net debt improved, which was one of the things I said I was on the lookout for in my previous articles, to 3.1x from 3.6x, and the all-important integration of Stanley, which has been a subject for quite a few quarters, is going according to plan as well.

Most of the anticipated 500M SEK synergies have already been realized at this stage. These cost synergies are also the main reason why the company is seeing improved margins as well, with a continuation of these margin improvements during 3Q.

{kind=link}

The company is also finally leaving some markets - while some chaos, in this case, is "good for business", some markets are hard to make work, and Securitas has seen long issues in markets like Argentina. I therefore considered it a positive piece of news that the company exited the Argentinian market, which is also part of the improved operating margin. Most other markets are markets that the company is managing well, including markets like Spain, Portugal, and similar markets, where margin improvements were visible.

That being said, the company's recent upswing is a product of broader market and macro trends, not specific improvements that weren't already very clear in 3Q23. The company is still in the midst of its EU-Ibero-America transformation program which still has CapEx effects for this year. Stanley is not in any way "finished" in terms of integration either, but we can expect a continuation here.

The divestment of Argentina is going to net a capital loss of 3.3B SEK, reported as IAC with most of that being accumulated non-cash FX impairments/losses, with another negative 122M SEK cash flow impact, mostly investment activities.

The current SEK weakness also had significant tailwind effects for 3Q23 - effects that won't be as strong in 4Q23 now that FX is normalizing back down again at 10.25 SEK/USD today.

The positive effect for the company here includes delevering of the company's previously-high debt. As I said in my last article, this is one of the key factors to look at here - and the company is almost down to below 3x again here, even if these numbers are before IAC.

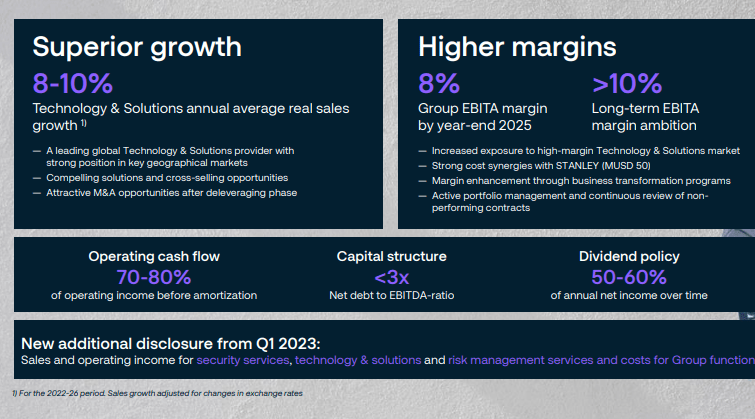

The company has high hopes in building what they call the "new Securitas", which I have been writing about before, but will mention here again.

{kind=link}

Given this company's poor track record (yes, I'll call it poor here), I wouldn't take any such estimates with more than a teaspoon of salt - but we can at least confirm that the company has some sort of upside here if the price is low enough.

On the fundamental side - meaning not debt, but actual business trends, the company is in a very good position. Its tech transformation is going forward, and the market for quality guarding and security services in this macro is only going in one direction here as I see it, up.

We have the company's investor's day in March of 2024 - I intend to attend the day here to get an update on the company, along with other investor days that come around at the same time.

Let's look at company risks and upsides here.

Risks & Upside

The risks for Securitas are operational, for the most part. The company has been in a significant slump for the past year and more. A turnaround seems to be happening, but at the same time, I see the visibility here as lower than I'd like for the timing specifically.

The last time I covered Securitas was well over a year ago. The company has declined significantly. I sold out of most of my position before the decline here due to structural merger issues and was proven right at the time. I then bought back in at a better price, though at a marginal position/size compared to my original stake.

This expresses well the upside you can get if you take some time to get the valuation "right" for the long term. I am currently in the green on this company, and while the yield isn't the best view it is good enough for what it offers. Securitas also has fundamental tailwinds in the form of the macro environment on its side - this is the main upside to the company here.

My overall risk/reward assessment continues to be that at the right price, Securitas provides outperformance potential.

Now let's look at what price this makes sense.

Securitas Valuation

Securitas is not as attractive as it was only a few weeks back - naturally given the latest trends for this week. We're seeing a significant EPS decline for this year, estimated to bring in about 2.52 SEK on a per share basis but not impacting the company's dividend which is still estimated to stay at 3.5% in terms of current yield.

The company's IG rating remains impacted at BBB-, but the debt/leverage is down and long-term debt to cap is now below 46%. I no longer view this as anything in significant danger, especially if we assume that the company manages a turnaround and its estimate of 10-11 SEK on a per-share basis for the next year, which seems likely given the current quarterly trends.

Forecasting Securitas at the long-term 15x P/E implies a reversal potential to a 15x of 2025E of upwards of 175-180 SEK, which is almost triple digits from the current share price, or 38.63% per year.

Likely?

I would say you should estimate the company going no higher than 140-150 SEK even if the margins improve and the company manages its synergies and improvements. This puts us at around 25% per year, which is good enough (more than good enough even) given my current investment goals.

Securitas is much more attractive below 90 - but even today, I see a double-digit eventual upside for this company. S&P Global analysts give Securitas a price range of 74 SEK to 153 SEK with an average of 105 SEK. That's an upside of 8% - not much, but I believe it can go far higher than that. 6 analysts out of 12 currently have a "BUY" rating or similar, while a mix is at "HOLD" or "SELL", reflecting the uncertainty of the upside and timing in the company's current valuation.

My overall stance, seeing my previous price target of 110, is to maintain this. This 110 SEK price target is the shorter-term target - I could even lower it given the current risk-free rate. However, anything towards the longer term means this goes up to at least 130-140 SEK, possibly to the 150 SEK level.

The question here is the timing of these upsides and results.

Based on this, I give the company the following thesis.

Thesis

- There's a lot to like about the security company Securitas, which is a worldwide known brand and business. The company's current challenges notwithstanding, I believe long-term investment makes sense at an attractive entry price.

- For the next 12-18 months, the pressure in earnings, inflation, costs, and integration call for this to be a riskier investment. My strategy dictates that I work this differently, and I've done so with buy-writes, annualizing over 16% RoR. I keep this stance in my 2023 article update.

- The company is a "BUY". I give it a long-term PT of 110 SEK/share, but there may be a long time before this is realized.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

While not necessarily cheap any longer, I still view the company as a "BUY" given the overall fundamental trends and quarterly improvements that we've been seeing. I therefore say "BUY" here.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Securitas: Why There Could Be A Reckoning With An Upside