SRLN - SEIX: Impressive Performance Vs. Peers Can Continue

2024-01-20 04:20:02 ET

Summary

- The Virtus Seix Senior Loan ETF stands out relative to larger peers due to its superior historical performance and smaller size.

- SEIX charges a reasonable expense ratio compared to peer funds.

- SEIX has delivered downside protection for investors during challenging risk-off environments historically.

- I expect SEIX to continue outperforming peers' funds going forward.

The leveraged loan ETF space is dominated by three funds: the Invesco Senior Loan ETF (BKLN) which has assets of ~$6.4 billion, the SPDR Blackstone Senior Loan ETF (SRLN) which has ~$5.2 billion in assets, and the First Trust Senior Loan Fund (FTSL) which as ~$2.2 billion in assets. The next three largest levered loan ETFs, a group that includes the Virtus Seix Senior Loan ETF (SEIX), have total assets of ~$572 million.

SEIX stands out from its larger peers for one key reason: better historical absolute and risk adjusted performance. While historical outperformance is not necessarily predictive of future outperformance, I believe SEIX strong historical performance means investors should give it a closer look vs larger peers.

ETF Overview

SEIX launched in April 2019 and currently has ~$100 million in AUM. The fund, which seeks to generate high current levels of income, is actively managed and invests in senior-secured floating rate levered loans. The fund's investment process aims to capture upside potential while limiting downside risk.

SEIX has a net expense ratio of 0.62% and 30-day SEC yield of 9.5%. The fund has a three person portfolio management team with all portfolio managers having been in place since August 2019.

Investment Process Overview

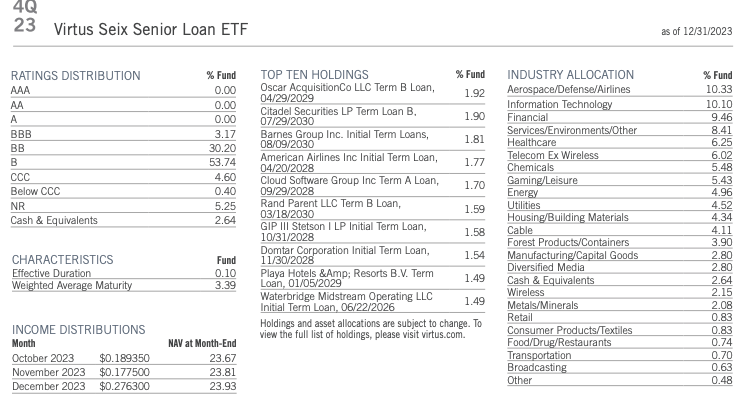

SEIX is focused on the higher quality segment of the leveraged loan universe and typically invests in BB and B rated loans. The fund invests generally invests in strong credits with solid asset protection.

While the fund invests primarily in U.S. borrowers, it has the ability to invest as much as 20% of total assets in non-U.S. borrowers including those located in emerging markets.

Seix Investment Advisors

Reasonable Management Fee

While SEIX's net expense ratio of 0.62% is high relative to the average bond ETF expense ratio of 0.11% and average bond mutual fund expense ratio of 0.37% it is reasonable vs other senior loan funds.

The largest ETF in the space, BKLN, which tracks an index and is not actively managed, has a net expense ratio of 0.65%. SRLN, which is actively managed, has a total expense ratio of 0.70%. FTSL, which is also actively managed, has a total expense ratio of 0.86%. Based on these comparisons, I find SEIX's fee to be reasonable.

Strong Relative Historical Performance

As shown by the chart below, since inception, SEIX has delivered a total return of 25.1%. This compares to total returns of 20.3%, 18.3%, and 16.7% delivered by FTSL, SRLN, and BKLN respectively.

In addition to delivering strong performance than peers, SEIX has also delivered less volatility. Since inception, SEIX has delivered an average 30-day volatility of 3.25%. Comparably, FTSL, SRLN, and BKLN have delivered average 30-day volatilities of 4.55%, 4.88%, and 5.51% respectively.

The result of these two factors is that SEIX has delivered much better risk adjusted returns than its peers. Since inception, SEIX has delivered an average 3-year trailing sharpe ratio of 0.59. This compares favorably to the average 3-year trailing sharpe ratios of 0.44, 0.32, and 0.27 respectively for FTSL, SRLN, and BKLN.

The significant level of risk adjusted outperformance suggests that SEIX's active fundamental based investment approach has added substantial value vs passively managed products and other active approaches.

One potential reason for this, that SEIX small size allows it to be more nimble and take advantage of investment opportunities which are less scaleable. Moreover, smaller funds may be able to enter and exit positions with a lower level of transaction costs as bid/offer tends to be tighter for smaller trades. Historical research has suggested that smaller funds tend to outperform larger funds. Given that SEIX has just $100 million in assets, I believe it is well positioned to continue benefiting from its smaller size relative to peers going forward.

Performance During Risk-Off Environments

Given the fact that SEIX's investment process is focused on risk mitigation, I believe it is relevant to consider how the fund has performed on a relative basis during recent risk-off market environments.

As shown by the chart below, during the COVID-19 related risk market sell-off, SEIX performed quite well on a relative total return basis falling just 3.84%. Comparably, FTSL, SRLN, and BKLN delivered negative total returns of 7.1%, 7.6%, and 8.2% respectively during the same period. SEIX also performed quite well on a relative basis during the 2022 risk-off environment.

I view this historical outperformance during macro risk-off events as an indicator that SEIX has done a good job of picking credits which are higher quality in nature.

Holdings Overview

SEIX is well-diversified in terms of single name exposure with no single holding accounting for more than 1.92% of the fund. The fund is also well diversified in terms of industry exposure with the fund's largest exposure being 10.33% to the aerospace/ defense/ airlines industry.

In terms of credit quality, SEIX has ~3% exposure to BBB rated credits, ~30% exposure to BB rated credits, ~54% exposure to B rated credits, and ~4.6% exposure to CCC rated credits. Comparably, SRLN, BKLN, and FTSL currently have similar credit quality.

In terms of yield, SEIX has a 30-day SEC yield of 9.5%. This compares to 30-day SEC yields of 8.3%, 7.9%, and 8.2% respectively for SRLN, BKLN, and FTSL. Thus, SEIX appears to be invested in a mix of slightly higher yielding securities relative to peer funds.

{kind=link}

Performance Outlook & Risks To Consider

While prior outperformance offers no guarantee of future outperformance, I believe SEIX is poised to continue outperforming its larger peers going forward. I believe that SEIX's smaller size has allowed it to be more nimble and take advantage of less scaleable opportunities. With just $100 million in AUM, SEIX remains a fairly small fund relative to peers.

The biggest risk to consider when contemplating an investment in SEIX or any of its peers is the risk of a macroeconomic downturn. While SEIX's active approach has historically been able to mitigate some of the risks associated with investing in the levered loan market, the underlying securities that SEIX is invested in remain fairly risky. A recession would likely lead to a challenging credit market environment. My macroeconomic view is fairly bullish as I do not expect a recession or substantial economic downturn in the near-term. For this reason, I expect leveraged loans and SEIX to outperform other fixed income products with less credit risk such as U.S. Treasuries or Investment Grade Corporate bonds.

Conclusion

SEIX stands out relative to its larger peers due to strong historical performance. SEIX has delivered better absolute returns with less volatility than other levered loan ETFs. Moreover, SEIX has also outperformed historically during market stress environments suggesting that the fund has done a good job of selecting higher quality credits.

SEIX's net expense ratio of 0.62% is higher than most fixed income products but reasonable in the context of fees charged by other levered loan ETFs.

I believe SEIX can continue to outperform its peers going forward as its smaller size allows for more nimble portfolio management.

For these reasons, I rate SEIX a buy and believe it is poised to outperform other levered loan products going forward. I would consider downgrading the fund if it grows in size substantially or fails to continue delivering better risk adjusted results vs peers going forward.

For further details see:

SEIX: Impressive Performance Vs. Peers Can Continue