PM - September's 5 Dividend Growth Stocks With 5.31%+ Yields

2023-09-20 00:53:12 ET

Summary

- Dividend growth stocks can provide reliable cash flows and promote share price appreciation.

- With this piece, we are screening dividend stocks based on safety, growth, and consistency.

- September's top dividend growth stocks with high yields we are touching on include NewLake Capital Partners, Armada Hoffler Properties, Kinder Morgan, 3M, and Philip Morris International.

Written by Nick Ackerman.

For some background on this monthly publication, here is my view on dividend growth stocks :

Dividend growth stocks aren't always the most exciting investments out there. They often aren't grabbing the headlines, and they aren't the stocks running up hundreds of percentages in a year. In fact, they are often some of the least exciting stocks. And that is precisely their strongest selling point. With such a vast world of dividend growth stocks available out there, it is important to screen through to see if there are any worthwhile investments to explore.

They are stocks that provide growing wealth over time to income investors. Dividend growers are often larger (not always), more financially stable companies that can pay out reliable cash flows to investors. Some are slower growers than others. Some are going to be cyclical that require a strong economy. Some are going to be secular, which doesn't generally rely on a more robust economy.

Dividend growth can promote share price appreciation. Of course, that is if these companies are growing their earnings to support such dividend growth in the first place. Trust me. There are yield traps out there - I've owned a few that I'm not particularly proud of.

I like to think of investing in dividend stocks as a perpetual loan of sorts. Essentially, every dividend is a repayment of your original capital. Eventually, holding long enough, you have the position "paid off." It is all returned back into your pocket from that point forward.

All of this being said, it is important to understand my approach to dividend stocks and why screening dividend stocks can be important for income investors. These are September's five dividend growth stocks that might be worthwhile for a deeper exploration. As with any initial screening, this is just an initial dive - more due diligence would be necessary before pulling the trigger.

The Parameters For Screening

I'll be using some handy features that Seeking Alpha provides right here on their website for this screen. In particular, I will be screening utilizing their quant grades in dividend safety, dividend growth and dividend consistency.

Dividend Safety is relatively self-explanatory. These will be stocks that SA quants show reasonable safety compared to the rest of their various sectors. The grade considers many different factors, but earnings payout ratios, debt and free cash flow are among these. This category will be stocks with A+ to B- ratings.

For the dividend growth category, we have factors such as the CAGR of various periods relative to other stocks in the same sector. Additionally, the quants also look at earnings, revenue and EBITDA growth. As we will see, this doesn't mean that every stock with a higher grade has the growth we are looking for. This just factors in that the dividend has grown or earnings are growing to support dividend growth possibly. For these, the grades will also be A+ through B- grades.

Finally, for dividend consistency, we want stocks that will be paying reliable dividends for us for a very long time. In particular, hopefully, they are raising yearly, though that isn't an explicit requirement. We will also include stocks with a general uptrend in dividend payments, which means there could have been periods where they paused increases for a year or two.

After looking at those factors alone, we are left with 522 stocks at this time from the 527 listed last month. I'll link the screen here , though it is a dynamic list that constantly updates regularly. When viewing this article, there could be more or less when going to the link.

From there, I wanted to narrow down the list a lot more. I then sorted the list by forward dividend yield, from highest to lowest. Since these will be safer dividend stocks in the first place, screening for those among the higher payers shouldn't hurt.

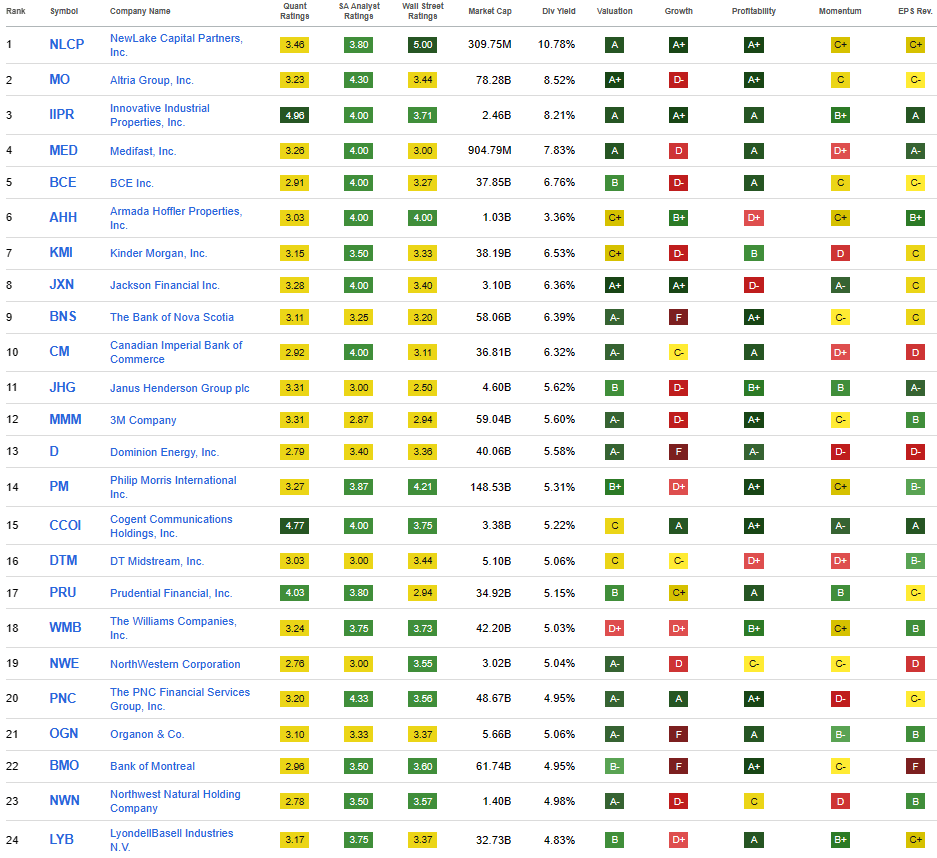

I will share the top 24 that showed up as of 09/05/2023.

{kind=link}

Several of these we have covered recently, so we will skip over these this month: Altria ( MO ), Innovative Industrial Properties ( IIPR ), Medifast ( MED ), BCE ( BCE ), Jackson Financial ( JXN ), The Bank of Nova Scotia ( BNS ), Canadian Imperial Bank of Commerce ( CM ) and Janus Henderson Group ( JHG ).

Additionally, I'll be skipping over Dominion Energy ( D ). It could be a fair investment, but they cut their dividend in 2020 and raised it only once during the time since the cut. It's been frozen at the same $0.6675 seven quarters since.

With that, we'll be looking at NewLake Capital Partners ( OTCQX:NLCP ), Armada Hoffler Properties ( AHH ), Kinder Morgan ( KMI ), 3M ( MMM ) and Philip Morris International ( PM ). Despite seeing so many repeats this month, we have three names we haven't touched on previously in this piece that would be NLCP, AHH and MMM.

NewLake Capital Partners 10.78% Yield

NLCP is a REIT that is focused on providing warehouse space to the cannabis industry. It's one of the publicly traded ways to access this area of the market, the other way being IIPR, which I hold a position in. NLCP is an internally managed REIT, but it is traded OTC. However, based on a comment in the past earnings call , it would seem they know there is merit to getting listed on a major exchange.

As you saw in our press release, we repurchased over 50,000 shares during the second quarter. While it's great to buy back stock at accretive levels, we would all prefer to have our stock price more accurately reflect the value of our quality portfolio. With an above-market weighted average yield, 14.5 years of remaining lease term and only $2 million of debt, we believe that our stock is well undervalued and we continue to focus our efforts on broadening our investor base to drive demand for our stock.

The most impactful catalyst for this would be acceptance of NewLake stock by institutional custody agents or uplisting to a major exchange. That continues to be a focus for us, and we will be relentless in our pursuit of the objective.

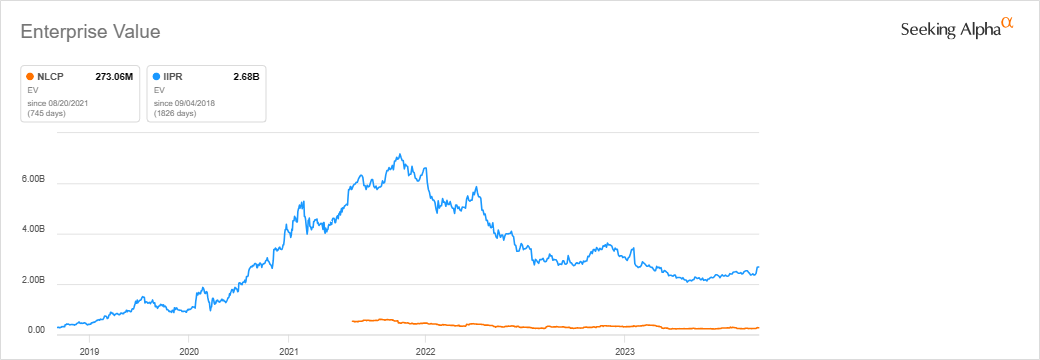

NLCP is considerably smaller than IIPR in terms of enterprise value. IIPR also went public well before NewLake.

{kind=link}

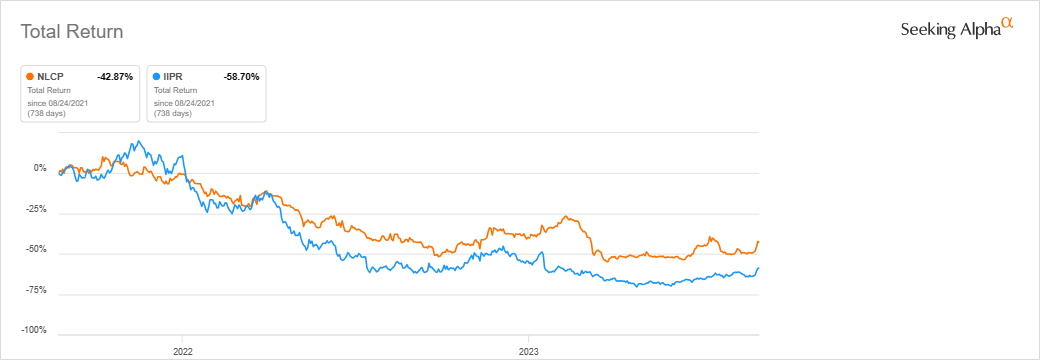

Unfortunately for the new REIT, they came to market at what would prove to be terrible timing as the whole space started to face significant challenges when interest rates were being increased. Both NLCP and its larger peer IIPR have faced significant declines in terms of their total return performance since around the time NLCP launched.

{kind=link}

That not only puts pressure on REITs, but when financing starts to cost something, and we move out of the zero-rate environment, the underlying tenants also start to run into issues. That's why this area of the market would seem to be a more speculative area to put capital to work. However, that doesn't mean we can't get some performance going forward or that these aren't solid income choices.

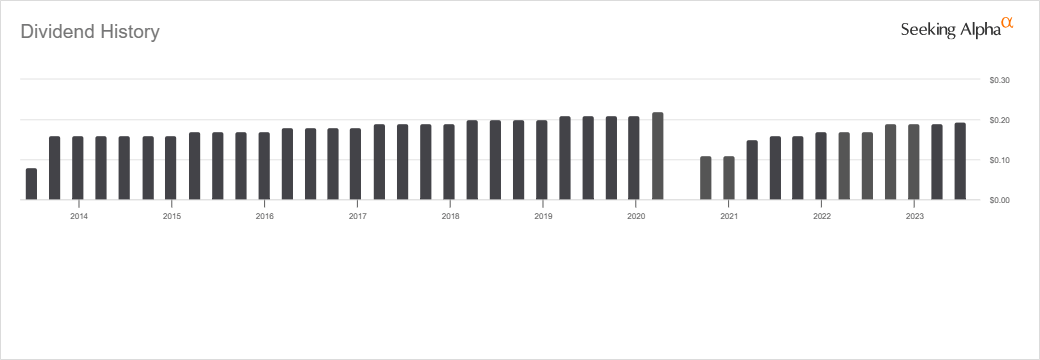

Since launching, NLCP had hit the ground running with dividend increases. Again, this was also similar to IIPR, which had been able to increase its dividend aggressively initially. That pace has slowed down for both significantly.

{kind=link}

At $0.39 for the latest quarterly payout and FFO expected at $1.80 for the current fiscal year, we see that the dividend payout would be around 87%. That isn't that unusual for the space; in fact, if we look at IIPR's payout ratio, it looks like it will be around 88%.

Overall, I believe that NLCP looks like an interesting investment in the REIT space for the more speculative investors out there. This would be something worth exploring deeper in the future.

Armada Hoffler Properties 6.8%

For the second new name to make the list this month, it's actually another REIT name. As an income investor, I have to admit that REITs naturally catch my attention, so I'm always open to explore new REIT opportunities.

AHH is listed as a diversified REIT, and they focus on multifamily, office and retail properties. The largest in terms of contribution to NOI comes from the retail space, but the office is followed closely behind. However, they are a fairly small REIT with only 57 properties total at the end of Q1 2023.

{kind=link}

They had listed 97% weighted average portfolio occupancy, with multifamily and office both sitting at 96%, while the retail portfolio had occupancy of 98%. Any REIT with office exposure has definitely been hit hard with uncertainty going forward. For AHH, they seemed to have been hit during COVID-19 and never really recovered. This is also when they cut their dividend, which had been steadily growing. Despite cutting, I thought it was appropriate for this monthly screening article because they've since raised it several times.

It isn't back at the pre-Covid level yet, but it is trending in that direction. They are running with an FFO payout ratio of just 62.4% based on the latest quarterly dividend amount against the expected $1.25 this fiscal year.

{kind=link}

That FFO estimate sets them up to surpass their 2019 FFO of $1.17. So, there has definitely been some slow growth in terms of that earnings metric, but even still, the share price hasn't reflected the same recovery, and it could be an interesting name to consider taking a further dive.

Kinder Morgan 6.6% Yield

KMI is perhaps one of the more infamous pipeline companies after it was considered a solid income play heading into the oil collapse of 2015/2016. They cut substantially once they converted to a C-corp and raised it a couple of times aggressively but have since only increased it slowly. At this point, it still isn't close to the pre-2016 cut level.

{kind=link}

This is actually only the second time that KMI has made it to this monthly article, where we give it a brief look. The previous and first time was back in April 2023.

One of the reasons for this could be that the share price has been fairly flat since crashing during COVID-19, which is quite similar to AHH. There was some initial recovery in the price, but then it has just gone sideways or even slowly trending lower. This languishing share price, while seeing some increases in the dividend, would raise the yield. Therefore, even if that growth has been fairly slow, a name would be more likely to make this list.

For what it is worth, the company expects distributable cash flow to come in at $2.13 per share through fiscal 2023. Based on the latest quarterly payout annualized, we would be looking at a conservative payout ratio of 53%. Therefore, they have a lot of cushion if we head through a rougher period, and this leaves the capacity to grow further in the future, too.

3M 5.61% Yield

It's a bit surprising to see a dividend king such as MMM make the list. They have 64 years of consecutive dividend growth under their belt.

{kind=link}

However, for those who follow MMM at all, this isn't too surprising. Being hit the litigation from military earplugs and PFAS chemicals is going to put significant strains on the company's cash flows. Some glimmers of hope are that they are starting to come to some settlements on these issues to give some better color on what sorts of damage we are looking at. Even if it looks potentially grim for the dividend, having certainty should help ease some pressure on the stock price.

The company is also looking to spin off its healthcare business, which they noted as making progress toward in their last call .

We've made good progress on our planned spin of our Health Care business, including regulatory filings and system updates in preparation for soft spin. We are also in the final steps of naming a CEO. We continue to work towards closing the transaction by year-end 2023 or early 2024, subject to the required conditions and additional factors we have disclosed in our SEC filings.

While I still consider this name a core portfolio position, it certainly isn't the type of "SWAN" or "blue-chip" type company it had been in past decades. The dividend growth has slowed tremendously over the past few years, and now a cut seems to be more likely than an increase if we are being honest.

If they don't announce a cut before the spin, I fully expect that the spin-off will create a situation where they do a sort of stealth cut. In my opinion, this could be similar to what AT&T ( T ) had done when they spun off Warner. They spin off a significant part of their business and adjust the dividend, but the dividend adjustment is deeper than what it otherwise would be.

Overall, I expect to continue to hold MMM, but I do want to get it out of my core portfolio. I'll continue to DRIP for now, but I think MMM will have a long road to recovery. I would look to replace it with something more dependable and potentially faster growing, which would probably come from something that is offering a lower dividend yield.

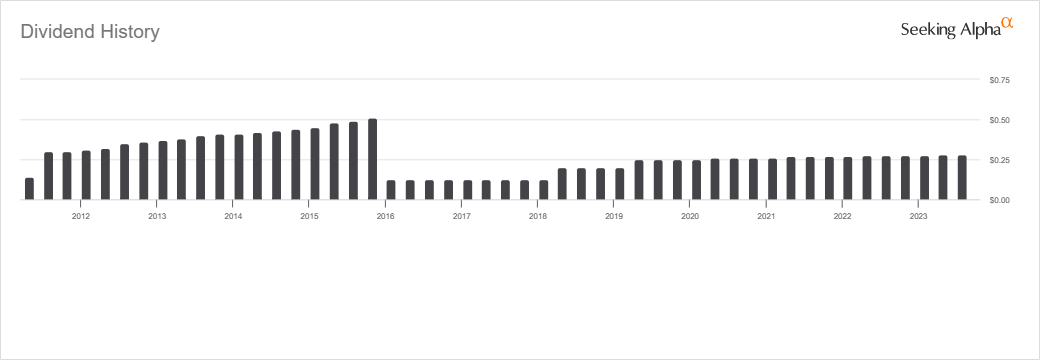

Philip Morris International 5.31% Yield

PM, the old reliable, makes it on our list once again. However, despite being a consistent dividend grower and a relatively higher yielder, it doesn't make its way on this list as often as its old parent, MO. The last time we touched on PM was back in October 2022. So here we are nearly a year later, and it made its way on here again.

PM's stock in the last year has held flat, being down only marginally at -0.83%. The company also hasn't raised its dividend at this time, but it is right on schedule to do so within the next week or two if history is any guide. Since spinning off from MO, they've been raising their dividend every single year. However, the pace of growth has slowed, which the higher initial yield helps compensate for anyway. The latest dividend increase came in at 2.4% and was just recently announced.

{kind=link}

The company is expected to see an EPS of $6.25 this year. That would be up nearly 4.5%, which is in the face of declining demand for cigarettes. Based on this estimate, the payout ratio based on the dividend currently would come in at around 81%. Of course, the big push by cigarette companies is now into smoke-free, where they expect to see higher margins and a larger share of the market.

{kind=link}

This is good news for these investments if they work out since the company has been pouring billions of dollars into these smoke-free alternatives. At the end of 2022, they noted they invested a cumulative $10.7 billion into the category. This was from the $2.4 billion listed in 2015, working out to spending over $1.18 billion per year over the last 7 years.

However, PM isn't limiting themselves to just their IQOS and ZYN pouches. They are looking to broaden out into a wellness and healthcare company. This would be about the opposite of the business that it is today, but with non-recreational cannabinoids being one of their developments, it's not as far removed as it might first appear. Here's a remark from their last earnings call .

We remain committed to developing our Wellness & Healthcare business and continue to see attractive mid and long-term growth potential on many fronts such as inhalable drugs, NRT, and consumer wellness products, including non-recreational cannabinoids, in line with applicable regulatory requirements.

Overall, PM remains a go-to dividend play for a higher yield with a solid track record. The growth might have slowed down. However, as they note themselves, they are looking toward their "smoke-free transformation to deliver sustainable growth." They have their investor day coming up on September 28th, where they noted they will be sharing more.

For further details see:

September's 5 Dividend Growth Stocks With 5.31%+ Yields