FOUR - Shift4 Payments: Strong Execution Track Record At Reasonable Valuation

2024-01-20 05:15:54 ET

Summary

- I am bullish on FOUR due to strong execution and profitability growth without risking the balance sheet.

- The company has significant room for growth, as evidenced by the success of similar companies like Lightspeed Commerce and Toast Inc.

- FOUR's vertical expansion strategy and partnerships, particularly in the sports and entertainment industry, provide opportunities for further growth and market share expansion.

Overview

My recommendation for Shift4 Payments (FOUR) is a buy rating, as I really liked how management has executed so far, growing business profitability without putting the balance sheet at major risk. The valuation is not too demanding as well, given that it is trading at multiples similar to more mature peers despite having a much better growth profile.

Business

FOUR is a merchant acquirer specializing in integrated payment processing and value added services in the US. They cover a wide range of industries such as Food & Beverage (F&B), Lodging & Hospitality, Sports & Entertainment, Retail, eCommerce, etc. Merchants benefit in four main ways: simplified operations, faster time to market, lower acceptance costs for all-in payments, and less overall complexity.

Lots of room available to grow

Initially, FOUR's focus was on the F&B and hospitality industries, which are very large industries that have substantial room for growth. One does not need to look too far to find evidence of this. We just need to look at the historical performance of Lightspeed Commerce ( LSPD ). LSPD is a point-of-sale [POS] solution provider for the F&B and hospitality sectors, and it has grown at a tremendous pace despite the weak macroeconomic environment. Over the past few years, revenue has almost doubled from $77 million to $730 million between 2019 and FY23. This clearly suggests significant room for growth. Another player that also suggests plenty of room for growth ahead is Toast Inc. (TOST). Like LSPD< the business has also grown significantly, where revenue has 6x from $665 million to $3.6 billion as of 3Q23 LTM. Take restaurants, for example. I believe the reason for such growth is that the market is long underserved, with many businesses operating on legacy platforms. In today's era, legacy platforms simply cannot keep up with the innovations that modern cloud POS offers, like integration with the food delivery platform, live reporting, integration with other tech equipment in the restaurant, such as the kitchen display system, etc. From a TAM perspective, 81% of restaurants are still using traditional legacy POS systems, which means there is still significant room for growth.

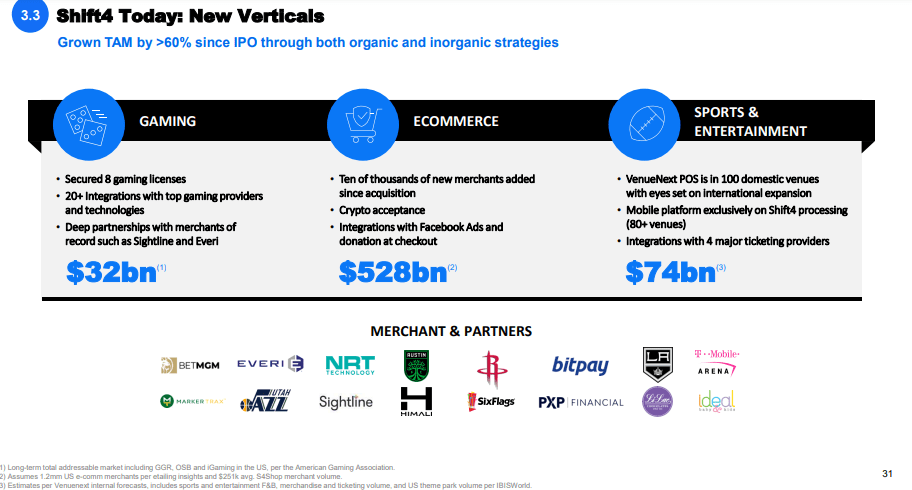

In recent years, FOUR's strategy of vertical expansion has been quite fruitful, allowing the company to enter new markets including e-commerce, gaming, non-profits, healthcare, and sports and entertainment (including stadiums). In addition, FOUR's management has stated that the company's 5-year worldwide strategic partnership with Starlink satellite broadband might generate an annual payment volume of more than $100 billion. With all these new verticals included, the growth potential for FOUR has significantly widened. By just including the three new verticals, it has increased FOUR's TAM by a combined total of >$600 billion.

"With a specific Starlink payment opportunity, some analysts say it could reach over $100 billion a year. The agreement includes a commitment to convert domestic volume to Shift4 beginning in the first quarter of 2022." 3Q21

{kind=link}

Of the 3, I really like the progress that FOUR has made in the sports and entertainment industry, where it continues to demonstrate success in winning marquee venues across, and with the recent acquisition of Appetize , FOUR has instantly added <600 venues to its customer base and more than 3x its market share across major leave sports, theme parks, and well-known venues. Specifically, within this vertical, I believe ticketing represents a significant opportunity given FOUR's integrations with the top 3 U.S. ticketing providers, Paciolon, Seat Geek, and Ticketmaster. I believe this is an important point to note, as it puts FOUR in a favorable position to be the vendor-of-choice when it comes to processing ticket volumes for these big boys. Because of FOUR venue acquisition strength so far, it has a major presence in the commerce experience for most parts of the consumer purchasing journey, for instance: mobile ordering, concessions, merchandise, parking, etc. In my opinion, these venues' management teams are more likely to incorporate ticketing into the same analytics package and platform so they can see a more complete picture of revenue. For ticketing volumes, FOUR stands to gain since stadiums can dictate the preferred payment processor to their ticketing provider, who in turn has their own payment processor on the back end. Encouragingly, this seems to be happening in real time as FOUR is already showing positive traction in winning ticketing, and management clearly knows that it is in a favorable position to continue doing so.

We have only just recently completed this TicketMaster integration, and we've already announced three ticketing wins this quarter, The Dolphins, The Orlando Magic, and the San Francisco 49ers. Now in college sports, we added University of Georgia.

Our leading fan first mobile technology is the true point of difference that opens the door to provide payments throughout the entire venue, and we are unique in our ability to unlock ticketing volumes through our integrations with major providers, such as TicketMaster and SeatGeek. from: 3Q2023 earnings call

The reason I am specifically highlighting this ticketing opportunity is because the unit economics are very favorable. Based on management's words, ticketing provides an additional 5x the volume and 3x the spread.

"Now the category leader in the space and not just stopping with like in-seat ordering and concessions. But going for ticketing where you get 5x the volume and 3x the spreads." Susquehanna get carded virtual conf (signup required)

Strong track record of execution and growth

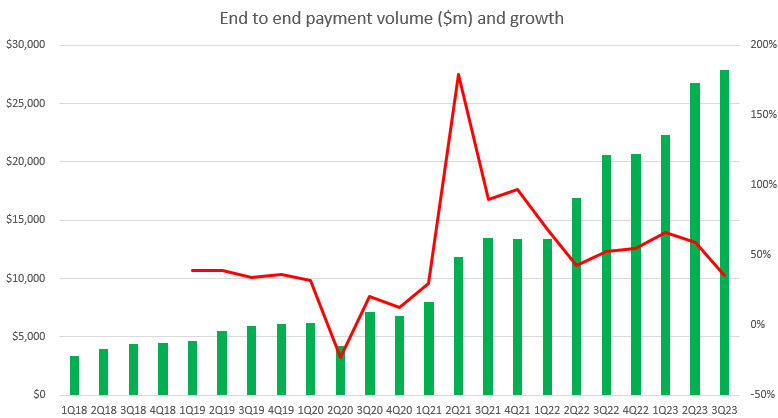

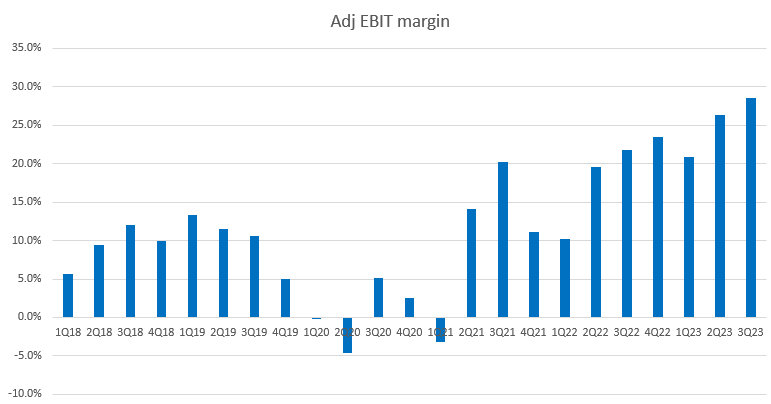

A great idea without great execution amounts to nothing. Thankfully, Four has demonstrated a very strong track record of growing business profitability even in the current weak macro environment. Through execution and acquisitions, FOUR has managed to grow its end-to-end payment volume from $3.3 billion to the current level of $27.9 billion, all the while maintaining more than 50% growth on average. Even in the recent quarters, where the macro backdrop was clearly not positive for consumer spending, FOUR continued to grow at an average of 54% over the past 4 quarters.

{kind=link}

I think an even more important distinction to make here is that FOUR payment volume growth was not acquired through heavy discounts or promotions that are not sustainable. The fact is, FOUR has grown the business at a staggering pace while improving its adjusted EBIT margins from mid-single-digits to the current 29%. This is an amazing feat, as it suggests that FOUR could potentially accelerate growth from here if it decides to reinvest some of the margins back for growth.

{kind=link}

Lastly, and arguably the most important factor in today's capital market environment, is that FOUR achieved all these feats without putting the balance sheet at severe risk. While FOUR is in a net debt position, it is within a reasonable range (currently ~3x LTM EBITDA). Considering the pace at which FOUR is growing and is generating positive free cash flow, there should be no issues with the leverage ratio continuing to decline from here. Based on consensus estimates, FOUR is expected to generate $623 million in EBITDA in FY24, which will reduce the leverage ratio to just 1.6x. This will give Four a lot of financial flexibility to conduct acquisitions again, further expanding its empire.

Valuation and risk

Author's valuation model

According to my model, FOUR is valued at $91.33 in FY24, representing a 25% increase. This target price is based on my growth forecast of 30% over the next two years, with FOUR achieving its FY23 growth guidance. Given management's track record of execution, I think their guidance is highly reliable. I am not making the assumption that EBITDA margin will expand, as I believe management will keep margin at this level and reinvest an excess profit for growth, which is the right thing to do. FOUR has already shown the market that they can grow profitability, which I think has earned itself enough creditability to forsake some margin to drive more growth.

Using other mature peers like Fiserv (12x forward EBITDA), Global Payments (10x forward EBITDA), and PayPal Holdings (8x forward EBITDA) as benchmarks, I believe FOUR can continue to trade 11x forward EBITDA (which is where it is trading today) given it has higher growth potential but a lower margin (that is expanding).

A potential risk that could cause the stock price to fall is that management messes up on acquisitions, such that they fail to extract the intended synergies (either revenue or cost), which causes margin or revenue to perform worse than expected. This will break the creditability that management has built so far.

Summary

I am bullish on FOUR. FOUR demonstrated robust growth in profitability without jeopardizing its balance sheet, and is trading at multiples that are not demanding when compared to more mature peers while exhibiting superior growth. Notably, the entrance into ticketing within the sports and entertainment sector presents a lucrative opportunity with favorable unit economics.

For further details see:

Shift4 Payments: Strong Execution Track Record At Reasonable Valuation