SBSW - Sibanye Stillwater: An Opportunity For The Brave

2024-01-05 11:15:41 ET

Summary

- Sibanye Stillwater's stock has not seen growth due to a decline in key metals prices, but I still hold the shares and am going to average down again.

- The company has successfully reduced costs and prioritizes its green metals strategy, focusing on battery and future-facing commodities.

- Despite a decline in metal prices, the company's stock is cheap compared to the overall sector, and if prices recover, it should see strong growth.

- There are many risks, so buying an SBSW is still an idea for the brave. Be that as it may, I think the worst is over for SBSW.

Instead Of An Investment Thesis

I've been covering Sibanye Stillwater Limited ( SBSW ) stock for the past 2.5 years and each time I've looked at the financial position of the company, I've come to the conclusion that I should average down my position and consider SBSW as a long term investment. However, this approach to position building is only good when the cycle is complete, and we finally see growth, which has not been the case with SBSW since the initiation of my coverage.

{kind=link}

Why hasn't the cycle reversed, and we haven't eventually seen growth in SBSW? It's about the fall in prices for key metals for the company in the period we're analyzing:

{kind=link}

Matthey data, Oakoff's compilation

However, I continue to hold the company's shares and hope for the cycle turn described above. In addition, I will most likely consider a more active dollar cost averaging of SBSW to reduce my average purchase price more quickly.

My Reasoning

Sibanye Stillwater, initially a high-cost operator of labor-intensive South African gold mines, has successfully reduced costs since its spin-out from Gold Fields in 2013. The company expanded into the platinum group metals ("PGM") space through acquisitions such as Rustenburg , Aquarius , Lonmin , and Stillwater, which now contribute significantly to its profits and value. Currently, Sibanye Stillwater is prioritizing its green metals strategy, aiming to focus on battery and future-facing commodities while reducing its geographical presence in South Africa.

The company exhibits high revenue diversification across metals (based on 1H 2023 revenue breakdown):

- 15.8% Platinum

- 22% Palladium

- 23.9% Rhodium

- 26% Gold

- 4% Nickel

- 3.7% Chromium

- 4.6% Other metals

Almost all of these metals are involved in the green transition, primarily in the automotive industry. The company anticipates sustained growth in demand for its metal portfolio. Metals utilized in battery production are expected to experience the most significant increase in consumption.

{kind=link}

SBSW's latest IR materials

As far as the actual results for the latest period are concerned, little has changed here since my last article on the company in October 2023, as SBSW publishes half-yearly reports and not quarterly reports. Just to refresh our memories, I'll repeat some key data figures.

In 1H FY2023, the group's adjusted EBITDA declined by 37% to $776 million compared to the same period in 2022, mainly due to a substantial drop in PGM prices and operational challenges in certain regions. However, improved performance in the South African gold operations partially offset these factors. The revenue for the period was $3.33 billion, reflecting a 14% year-on-year decrease.

Sibanye Stillwater was well-prepared for the downturn in the industry. As of the end of H1 2023, the company's cash and cash equivalents were slightly below borrowings, resulting in a net debt of $14 million and a net debt to adjusted EBITDA ratio of 0.01x.

{kind=link}

SBSW's IR materials

However, the 1H FY2023 balance sheet is a thing of the past. With a significant portion of the company making operating losses, I believe SBSW is already facing a problem in financing its operations. Sibanye's recent decision to raise $500m in the form of convertible bonds can also be interpreted as a strategic response to the stress in the PGM business. Against this background, the company's attempt to cut staff appears to be a justified step, in my view.

Seeking Alpha, SBSW

Anyway, as PGM prices continue to fall, SBSW shares are likely to remain under pressure. Nevertheless, I hope we'll see an increase in demand for PGMs and gold this year. As CPM Group Vice President of Research Rohit Savant wrote in mid-December 2023 , the traditional auto industry should not be written off despite the growth of electric vehicles. He also expects increased PGM demand in China due to the implementation of China 6 emission standards.

He forecasts gold to trade at US$1,897 per oz., up 7.3% from an average of US$1,768 per oz. in 2020. Silver will also jump to US$26.50 per oz., an increase of 30.2% from US$20.34 per oz. Likewise, PGMs are on the rise: platinum to US$1,081 per oz., up 22.1% from US$885 per oz., and palladium to US$2,313 per oz., an increase of 6.8% from an average of US$2,166 per ounce.

Source: CPMGroup

Other third-party research agencies partially agree with the positive outlook on PGMs in 2024. According to EcoTrade's outlook for PGM metals , platinum is anticipated to maintain a deficit of 445 koz, with challenges in South African production persisting due to falling PGM prices and potential mine closures. Autocatalyst recycling for platinum is predicted to remain weak, influencing a trading range of $800/oz to $1,100/oz. Palladium is forecasted to experience a significant deficit, driven by subdued secondary supply and declining demand in the automotive sector. Potential production cuts and supply risks pose challenges, leading to an estimated trading range of $700/oz to $1,200/oz. Rhodium is projected to be in a slight deficit, with risks including power cuts and production reductions in South Africa. Automotive demand for rhodium is expected to decrease by 5%, influencing a trading range of $3,500/oz to $6,500/oz, reflecting a more normalized market with potential price pressure from weaker net demand but upside potential from supply reduction risks in South Africa.

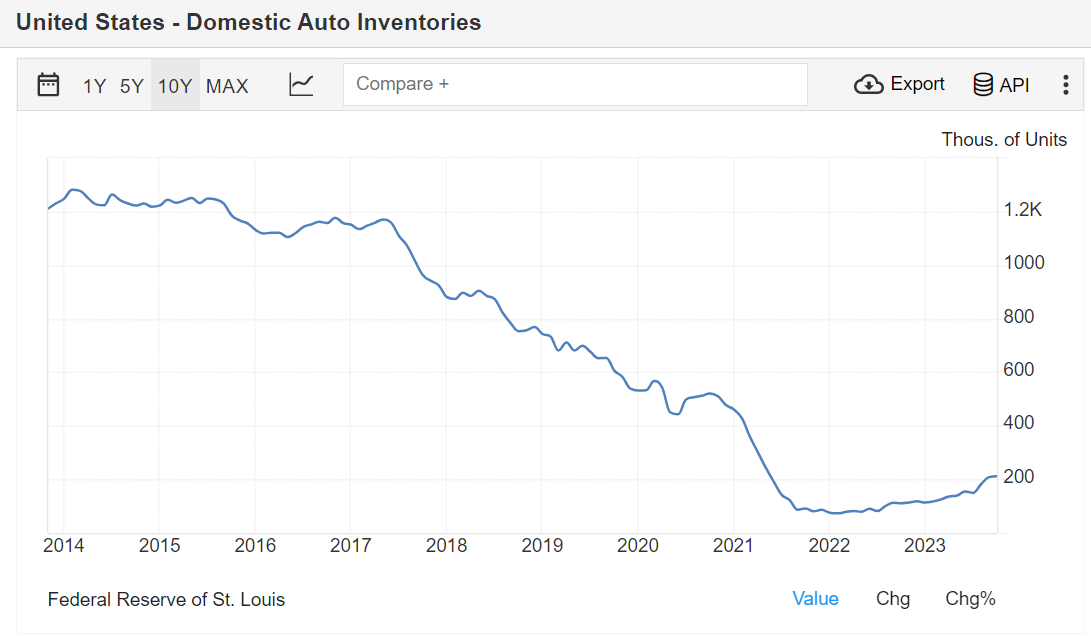

I am inclined to think that these forecasts are not far from reality, because the main source market for the use of the above-mentioned metals - the automotive industry - is still in a structural deficit if you look at the long-term dynamics of inventories .

{kind=link}

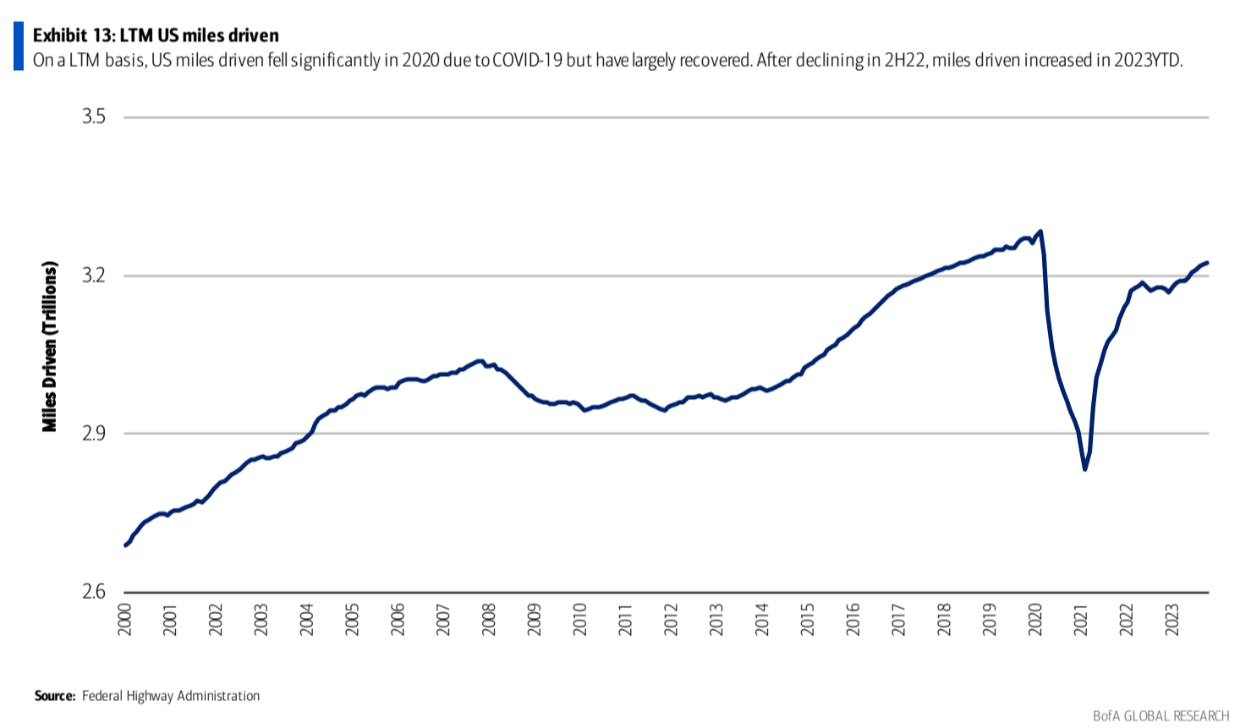

At the same time, according to Bank of America data from the end of December 2023, i.e. post-COVID, Americans have not used their cars less often - there has been a further increase in 'miles driven', which means more wear and tear and breakdowns and thus a higher demand for new cars going forward.

{kind=link}

I think if interest rates fall, consumers in the US and the rest of the world will be more likely to be able to afford a new car - a direct incentive for the car industry to produce more cars, driving up demand for the metals needed to make them. Therefore, I think that positive forecasts from third-party research institutes are actually more likely to come true than forecasts about a possible continuation of the price decline.

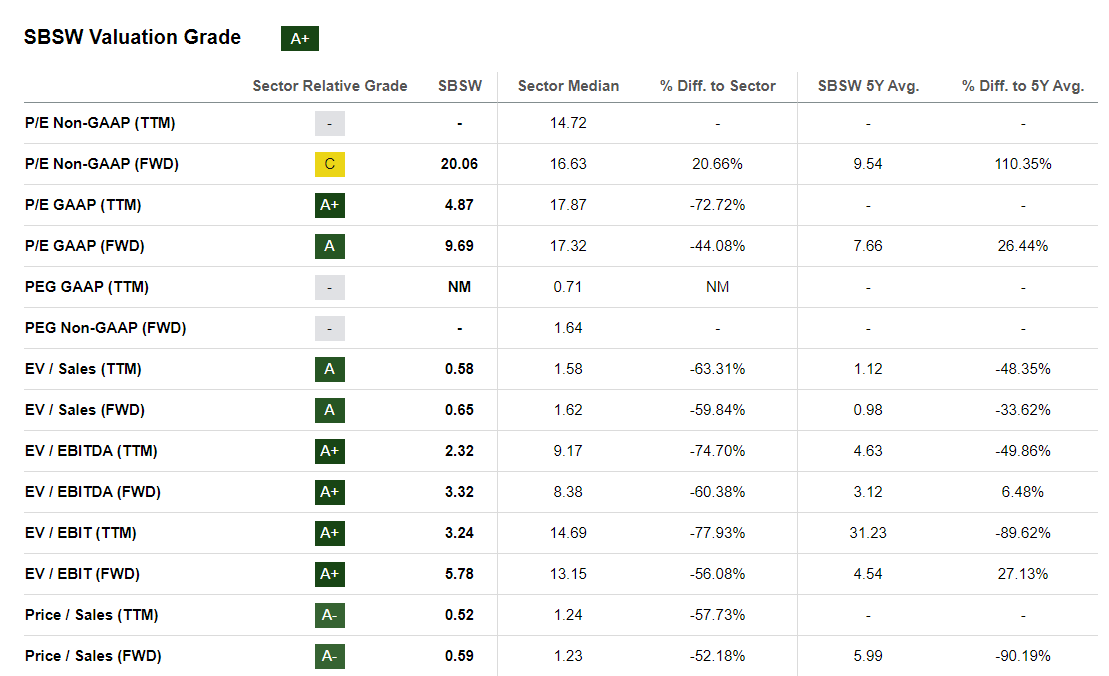

Despite a significant decline in metal prices in recent years, the company is currently trading with a forward price-to-earnings ratio for 2023 at around 9.7x , which is quite cheap versus the overall sector:

{kind=link}

Seeking Alpha, SBSW's Valuation

To provide context: at the peak of the current cycle in 2021-2022, the company earned nearly $4 billion in cumulative net profit, surpassing its current market capitalization.

{kind=link}

Seeking Alpha, SBSW, Oakoff's notes

So if PGM prices recover to even a fraction of the above forecasts, SBSW shares should respond with strong growth. In this regard, I agree with another Seeking Alpha analyst, GoldStreetBets Research, who called the stock a cheap call on PGM and gold prices.

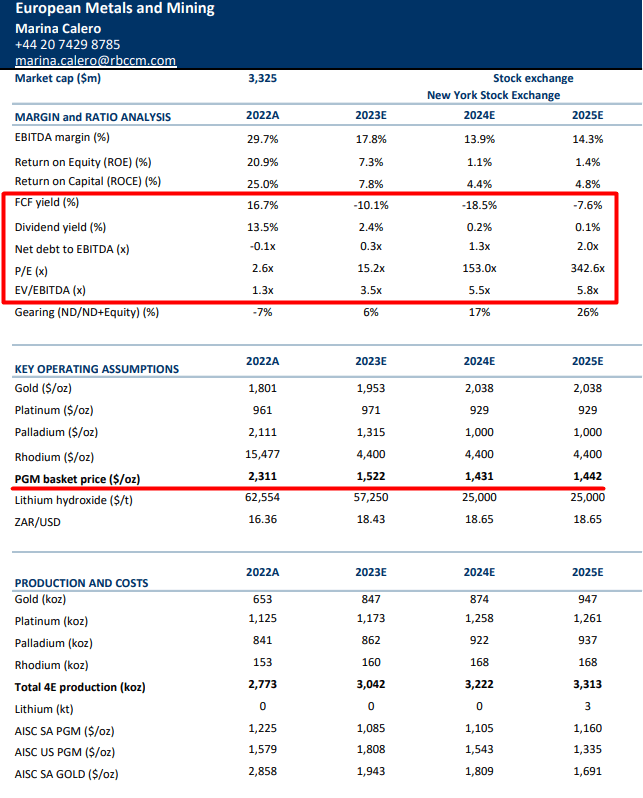

What happens if this option doesn't work out? Obviously, current P/E ratios will increase tenfold - this is clearly seen from the December 2023 RBC's forecasts [proprietary source]. Pay attention to the PGM price basket forecast and the resulting valuation multiples:

{kind=link}

But even in this scenario, SBSW's EV/EBITDA - in my opinion a more realistic measure of company valuation in this sector - will be below 6x, which is well lower than the industry median. Today, by the way, this ratio is at a historic low.

So in my view, the Sibanye Stillwater shares appear to be cheap in each of the possible scenarios.

Risks To Consider

Labor unrest has been a recurrent issue for Sibanye Stillwater, impacting production and costs. Ongoing threats of strikes, particularly at its gold mines and PGM operations, pose a continuous risk to the company's operations and shareholder sentiment.

The financial performance of SBSW is highly susceptible to fluctuations in commodity prices and currency exchange rates. A decline in gold or PGM prices, coupled with a stronger South African rand, would likely have adverse effects on earnings due to the company's operational gearing.

Economic downturns or changes in the market, such as decreased demand for precious metals, can adversely affect the company's financial results and stock price. Environmental and social responsibility is an increasingly important factor for investors, and any failure by Sibanye to meet ESG standards could lead to reputational damage and regulatory consequences.

Additionally, if inflation abates earlier than expected or if the company successfully manages to offset inflation through improved productivity or cost reduction measures, it could result in higher-than-expected earnings. Conversely, persistent or higher-than-expected inflation may pose challenges to the company's profitability.

Your Takeaway

I believe and hope that PGM metal prices will rise in 2024. If I am right, Sibanye Stillwater's stock will be one of the main beneficiaries of this event, as its current valuation looks very cheap. But of course, there are a lot of risks, and the recent news about the bond issue and the closure of the Kloof 4 gold shaft in South Africa does not bode well for a quick financial recovery.

I continue to view SBSW as a long-term idea and will be watching the company's results as they are released. I do not rule out downgrading the company to "hold" or "sell" if my expectations of demand are not met, and will follow this recommendation regardless and liquidate my position.

Be that as it may, I think the worst is over for SBSW, so I intend to increase my position if the stock falls further and if there are still clear signs that the demand side is going to get stronger. I therefore confirm my 'buy" rating today.

Good luck with your investments!

For further details see:

Sibanye Stillwater: An Opportunity For The Brave