SBSW - Sibanye Stillwater: Buy The Leading Choice For PGM Mining Before The Turn

2023-03-24 00:47:20 ET

Summary

- Platinum and palladium are both projected to be undersupplied by new mine production again in 2023.

- Any serious/further disruption from Russian supplies to the world market could cause a huge spike in platinum group metals pricing.

- A new round of money printing by central banks to combat a developing recession this year may cause a massive influx of PGM investor interest, a hedge against future inflation.

- The primary realistic option to own a low-cost platinum/palladium mining concern is through Sibanye Stillwater.

If you are worried about another round of money printing by the world's central banks later this year, to prevent our debt-laden economy from entering a serious recession, why not purchase some platinum/palladium exposure? Both platinum and palladium are forecast to be in supply deficits in 2023 by industry organizations . In addition, a record speculative short position now exists in palladium futures trading.

Assuming investor demand as a commodity hedge erupts from new fiat currency devaluations, a robust price rise in the platinum group metals [PGM] cannot be ruled out into 2024. On top of this scenario, Russia supplies much of the globe with the platinum group metals, through sales by Public Joint Stock Company Mining and Metallurgical Company Norilsk Nickel ( NILSY ). Norilsk Nickel is no longer available to U.S. investors with sanctions imposed during the Russian invasion of Ukraine. And, market participants are worried any hiccup in scaled-back Russian sales to western economies could generate a real shortage of these metals.

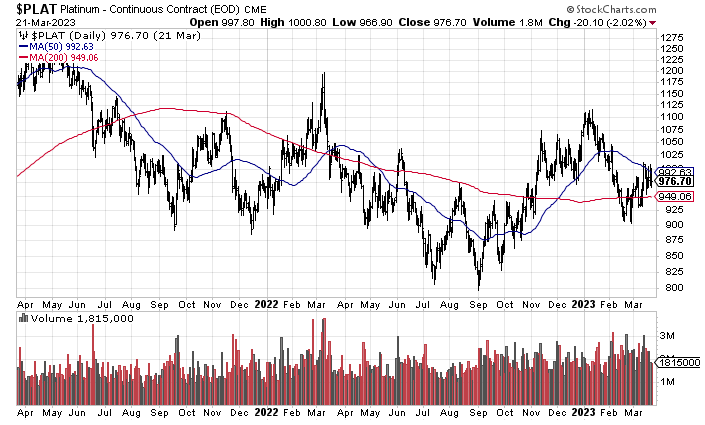

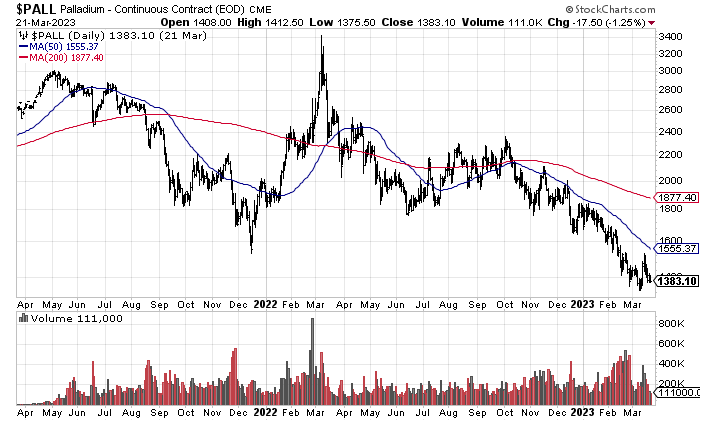

The most interesting part of the setup for platinum and palladium is prices for both have not moved in a bullish direction over the last year. Fears of an approaching recession, and somewhat lower-than-projected deficits in palladium/rhodium have held back any advance.

StockCharts.com - Platinum Nearby Futures, 2 Years of Daily Price & Volume Changes StockCharts.com - Palladium Nearby Futures, 2 Years of Daily Price & Volume Changes

{kind=link}

{kind=link}

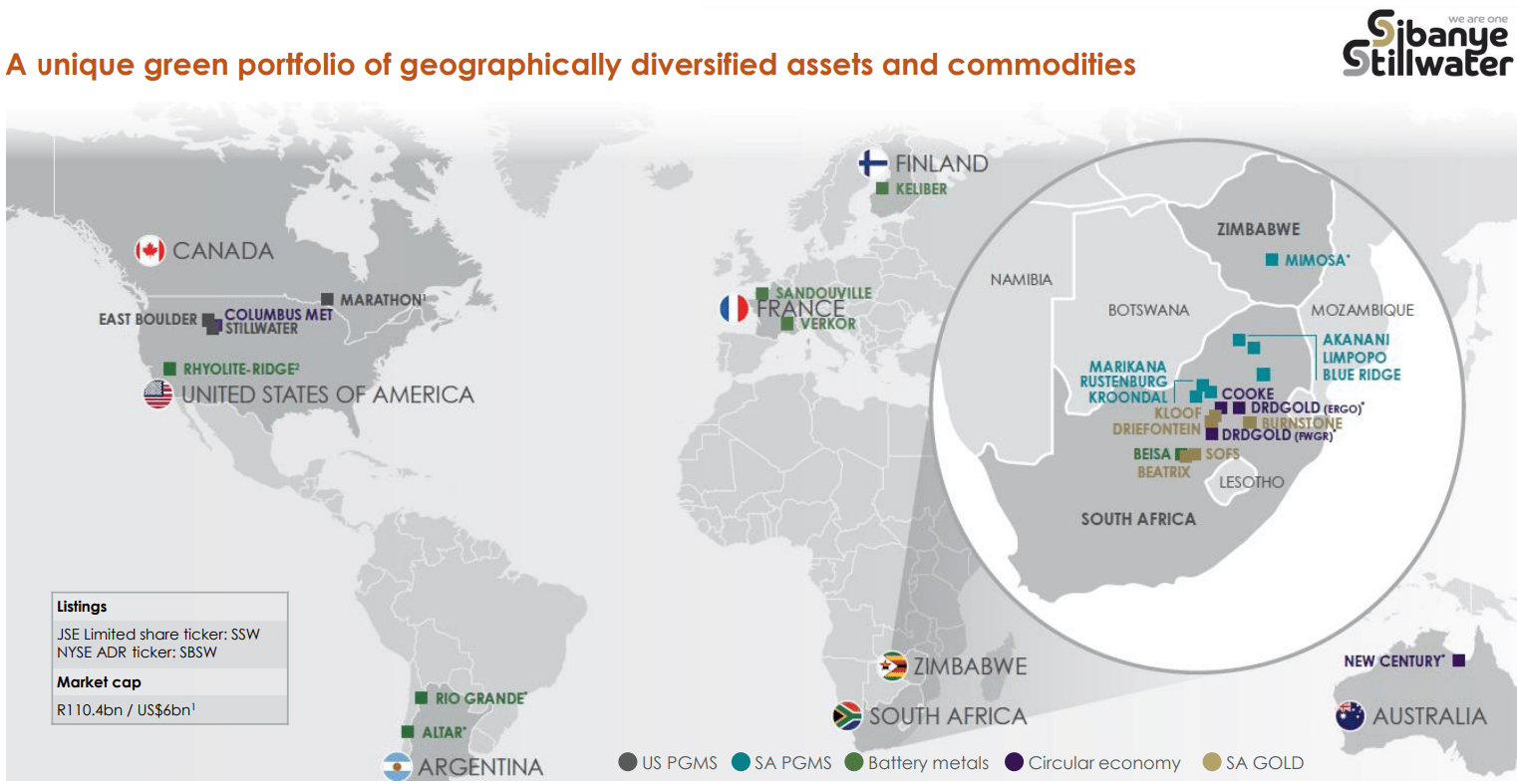

How can investors take advantage of the situation? Outside of a low number of direct commodity-holding ETFs like the Aberdeen Standard Physical Platinum ( PPLT ) and Palladium ( PALL ) funds, even fewer options exist in the mining category for retail investors. By far the strongest-situated miner is located in South Africa, currently pushing (reinvesting cash flow) to diversify into electric vehicle and green energy-critical lithium and nickel mines throughout the world. That name is Sibanye Stillwater Ltd. ( SBSW ), generating about 80% of 2022 sales from PGM mining.

Company March 2023 Investor Presentation

{kind=link}

Sibanye's Low Valuation

The biggest SBSW draw to me is a clear undervaluation on trailing and projected operating results. On basic price to trailing sales, cash flow, and book value, enthusiasm for the stock has definitely disappeared in early 2023. Low single-digit ratios for each of these fundamental multiple creations point to real distaste for the business. Ten years of median average data places the current valuation at a minimum 20% discount to recent trading history.

YCharts - Sibanye Stillwater, Fundamental Ratios, 10 Years

However, the earnings valuation picture and outlook is even stronger for new share buyers. Below is a decade-long graph of the P/E setup. SBSW's forward estimated P/E of less than 4x is one of the lowest you can find at any major mining firm in the world today.

YCharts - Sibanye Stillwater, P/E Ratios, 10 Years

In addition, enterprise value calculations (including no net debt) highlight Sibanye Stillwater as one of the smartest bargains available to commodity-producer investors. EV to forward projected EBITDA under 2x is a 10-year low, while EV to forward revenues of 0.7x is the lowest since early 2014, when the share price was $3 (South Africa Sibanye and U.S. producer Stillwater merged in 2016).

YCharts - Sibanye Stillwater, EV to EBITDA & Sales, 10 Years

Lastly, you would rationally think the only way multiples on operations this low could exist, could be a function of extended debt or depleted resources. Nope and nope. The company holds more cash than debt currently, with only limited interest expense. And, platinum/palladium reserves are estimated to persist decades into the future .

YCharts - Sibanye Stillwater, Net Debt & Interest Expense, 10 Years

The Standout Platinum Group Metals Miner

In terms of performance for investors over the previous decade, Sibanye Stillwater is the hands-down #1 choice for honest and diversified platinum and palladium (plus rhodium) exposure. In terms of 10-year total returns, SBSW has outperformed platinum/palladium bullion prices represented by the Aberdeen ETFs, and even outshined the VanEck Gold Miners ETF ( GDX ), with a stellar +256% advance.

YCharts - Sibanye Stillwater vs. PPLT, PALL, GDX, Total Returns, 10 Years

The closest peer company may be African-focused Anglo American Platinum ( ANGPY ). Impala Platinum ( IMPUY ) and minor player Platinum Group Metals Ltd. ( PLG ) in South Africa are other weaker choices, while Norilsk is no longer an option because of sanctions against Russia. The 10-year total return graph below highlights the winning SBSW argument for ownership with its robust +256% gain (+14% compounded annually), against +86% for ANGPY and net losses for the other three.

YCharts - Platinum Group Metals Producers, Total Returns, 10 Years

How has Sibanye Stillwater performed against an expanded list of diversified miners including Anglo American plc ( NGLOY ), Teck Resources ( TECK ), BHP Group ( BHP ), Rio Tinto ( RIO ), Vale SA ( VALE ), AngloGold Ashanti ( AU ), and Barrick Gold ( GOLD )? Again, it has led the pack for shareholder gains over the last decade.

YCharts - PGM, Major Base Metal & PM Producers, Total Returns, 10 Years

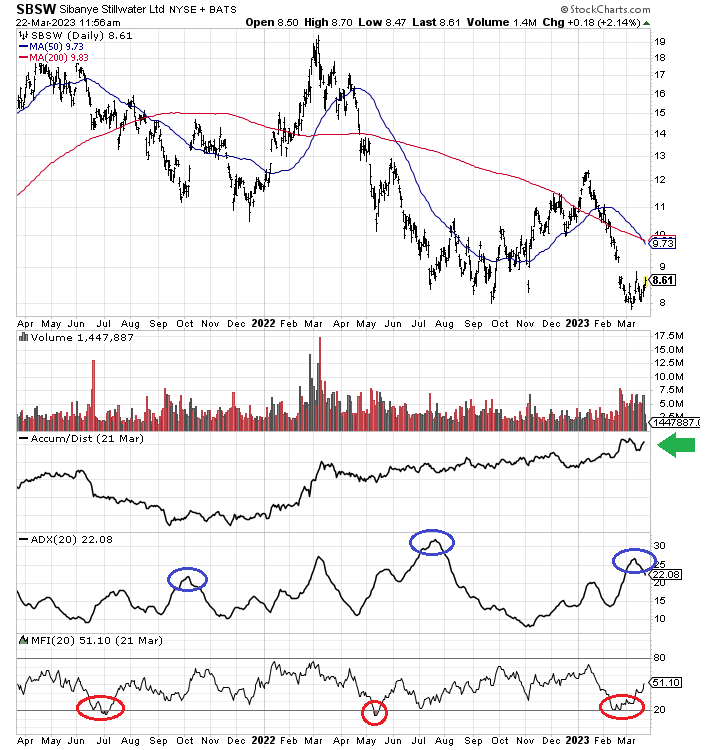

The bad-news, good-news story for Sibanye Stillwater can be reviewed on the 2-year chart of daily trading activity below. The bad news is price has performed in a horrible fashion over the past few years, down roughly -50%. The good news is this bearish trend has opened a wonderful buy opportunity for forward thinkers, with a washed-out valuation and not much excitement part of the investment setup.

From a technical readout, a steadily rising Accumulation/Distribution Line does indicate a massive amount of buying-on-weakness intraday (marked with the green arrow). And, the stock was dramatically oversold into the sub-$8 quote during early March. Both the 20-day Average Directional Index (blue circles) and 20-day Money Flow Index (red circles) are signaling a cyclical bottom may be forming soon. If another price drop closer to $7 materializes into April on recession fears, that may mark the final drop for this move. It may also be possible that price has already bottomed, however.

StockCharts.com - Sibanye Stillwater, 2 Years of Daily Price & Volume Changes, Author Reference Points

{kind=link}

Final Thoughts

Management's effort to diversify away from South Africa's riskier-than-normal investment backdrop is a welcome development. I believe the push into lithium and nickel will pay nice dividends (literally) for shareholders years into the future. The balance sheet is rock solid. And, the valuation is tilted toward a future share quote advance.

All we need is a big jump in the platinum group metals, and Sibanye Stillwater could easily jump to new 52-week highs above $17 per share, a good DOUBLE for price appreciation. One more positive: the company is committed to large dividend payouts when times are booming. Over the last two years, SBSW has paid out a cash yield averaging 8% annually.

YCharts - Sibanye Stillwater, Trailing Dividend Yield, 10 Years

What are the risks? 2022 was actually a rotten year for the company, and a lingering excuse for weak stock price trading so far in 2023. Despite its high returns and yields on investment, unusual floods at the company's Montana mines and labor strikes in South Africa really cut into results last year. Lately, management has warned of electricity and power shortages affecting production. The biggest overall risk comes from its core operations in Africa. This area of the world is constantly changing politically, and rules/laws governing mining could turn detrimental to SBSW with little warning. Hence, the ultra-low valuation logic on the business today.

But, if you are willing to take on the district, jurisdiction and geopolitical risk of African asset ownership, the potential rewards under a rising price regime for precious metals could be outstanding into 2024 (SBSW does also run a significant gold mining operation/reserve-base in South Africa generating 17% of sales in 2022).

I am planning to repurchase a stake in coming weeks, alongside renewed positioning in platinum and palladium bullion ETFs. It's somewhat possible we get a recession-scare selloff first in the dual-purpose industrial/precious metals of platinum and palladium (like the initial pandemic-induced economy shutdown dump of March-April 2020), before the bull story really gets into gear.

I don't foresee the SBSW share quote declining below $5, even in a worst-case severe recession scenario, where the platinum group metals decline another 20% to 30% from current levels. Such a price would represent a 20% discount to book value, equaling the widest discount in 2018, since the Stillwater merger.

The best-case upside is a move back above $20 a share is next for shareholders, the all-time high in 2021. This forecast assumes platinum, palladium, and rhodium rise 50% from present pricing by the first half of 2024 on better industrial/investor demand and continued shortages of the metals. On top of rising sales, a valuation reversion-to-the-mean swing toward long averages would likewise play into this final price target.

My conclusion: with outlier risk on investment no greater than -40% vs. outside total return potential reward of +150% (including presumed dividends on improving earnings) over the next 12-18 months, a Buy rating is warranted.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

Sibanye Stillwater: Buy The Leading Choice For PGM Mining, Before The Turn