ABT - Siemens Healthineers: A High Quality Option In The Healthcare Industry

2023-12-06 15:54:55 ET

Summary

- Siemens Healthineers demonstrates operational superiority and holds a competitive edge in the healthcare industry. With top-tier financial metrics and industry-leading margins, the company outperforms its peers.

- The company holds the number one or two positions in each of its operating segments and has shown solid market share expansion.

- The company's long-term growth targets seem realistic and I share the expectation for the company to grow revenues at mid to high-single digits and EPS in the low double-digits.

- Even when awarding the company a premium over peers, the current valuation is slightly too demanding as shares sit on the edge of fair value and slightly overvalued based on long-term return potential.

- I believe shares would present a more compelling investment case at a share price of below €50 per share.

Introduction

I initiate my coverage of Siemens Healthineers AG ( SMMNY ) with a "Hold" rating following my in-depth research. Siemens Healthineers demonstrates operational superiority and holds a competitive edge in the healthcare industry.

With top-tier financial metrics and industry-leading margins, the company outperforms its peers. However, the current valuation, trading at 23x earnings, appears demanding, presenting limited upside potential in the next 24 months. While a fair value assessment places the shares on the edge of being slightly overpriced, the uncertain macro environment prompts a conservative "Hold" rating.

I recently published my in-depth coverage of GE HealthCare ( GEHC ) here on Seeking Alpha. Despite the Sell rating for GEHC, in that article, I also pointed out just how attractive the medical devices industry is. In my eyes, the industry presents a stable and reliable investment opportunity for conservative investors. Despite not being as fast-paced as technology alternatives, its consistent growth over decades and resistance to economic cycles make it attractive.

Market research agencies predict continued steady growth in the healthcare devices industry at mid-single digits, projecting an increase from around half a trillion in 2022 to approximately $800 billion by 2030. This growth is fueled by global trends such as an aging population, the expanding middle class in emerging economies, and a rising demand for innovative devices and health services. Factors like the prevalence of lifestyle and chronic diseases, a focus on early diagnosis and treatment, and the introduction of advanced medical equipment further contribute to the industry's expansion.

Investors can benefit from this steady and anti-cyclical growth by investing in the industry's leading players like GE Healthcare, Philips ( PHG ), and Siemens Healthineers.

Siemens Healthineers is one of the largest companies operating in this highly fragmented industry. We should keep in mind that it requires significant amounts of R&D spending and testing to bring medical devices to market, and with the sheer broadness of this industry, it is practically impossible to control a large share. Every company has its area of specialty, and even despite its market cap of over $60 billion, Siemens only holds a market share of approximately 4.2% in the medical devices industry. To be precise, the company is the fourth largest in terms of revenue.

{kind=link}

Starting at the basics, Siemens Healthineers is a multinational medical technology company that operates in the healthcare industry. It is a subsidiary of Siemens AG ( SIEGY ), which still owns 75% of the company's shares. Siemens Healthineers focuses on providing a wide range of medical products, services, and solutions to healthcare providers worldwide.

Within the highly fragmented and specialized healthcare equipment industry, Siemens Health focuses on specific verticals like Medical Imaging, Laboratory Diagnostics, point-of-care testing, In-Vitro diagnostics, and advanced therapies, among others, where it competes with the likes of Abbott Laboratories ( ABT ), GE Healthcare, and Philips. The focus on these areas, combined with a number of acquisitions and divestitures over the years to streamline and perfect the product portfolio, has resulted in very decent revenue growth in line with the healthcare equipment industry at a CAGR of 5%. Meanwhile, years of development, innovation, and strategic acquisitions have allowed the company to become a leader in its respective industries, positioning it favorably for decent long-term growth.

The company reports its operations across four segments: Imaging, Diagnostics, Varian, and Advanced Therapies. Let's dive deeper into each of these to understand the company's products, competitive strength, and growth potential.

Imaging - Leading the industry, taking market share, and outperforming peers

Siemens Healthineers' Imaging segment produces a wide range of medical imaging products that are used for diagnostic purposes. The company is known for its innovative technologies in the field of medical imaging, which include equipment like X-ray systems, CT scanners, MRI systems, ultrasound systems, and many more.

Imaging segment products (Siemens Healthineers)

{kind=link}

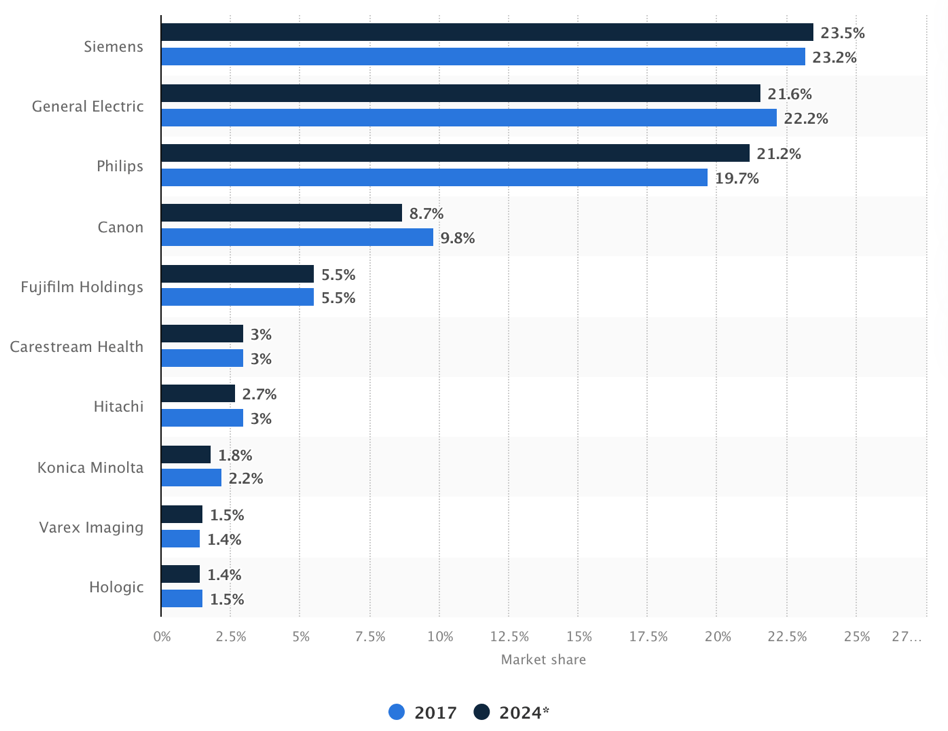

Crucially, with an installed base of over 134,000 machines, Siemens Health is the undisputed industry leader in imaging, commanding a strong market share of approximately 23.5%, up slightly from 23.2% in 2017, according to data from Statista. However, management claims its market share sits closer to 34% after some market share gains in recent years.

Medical imaging market shares (Statista)

{kind=link}

Most importantly, one way or another, the company leads this industry and has seen its market share expand, taking this from Canon ( CAJPY ) and GEHC. The fact that the company has been able to hold onto its leading market share tells me that it is executing steadily and continues to at least remain on par with the competition in terms of technological progress, which I view as promising.

This leading market share makes the company a prime beneficiary of the steady projected growth in this industry. If it slowly continues to gain some share, it could even marginally outgrow the industry, especially as my recent analysis of GEHC showed that the competition is dropping the ball. I expect Siemens Health to benefit from this and pick up more market share over the next few years.

Meanwhile, the diagnostic imaging market is valued at $26.5 billion in 2023 and should continue to grow steadily at a CAGR of around 5.5% through the end of the decade, driven by the rising prevalence of targeted diseases and increasing technological advancements. Siemens Health is well positioned to report revenue growth of its Imaging segment in line with this industry outlook and potentially even slightly above this, leading to revenue growth at mid-single digits for the foreseeable future.

With this segment accounting for 55% of revenue, this is crucial and provides it with a strong growth basis. Whereas I am traditionally quite critical of heavy reliance on a single segment, in the case of Siemens, I do not mind it as much. Of course, I would prefer some better diversification, but Siemens' imaging segment is incredibly strong, has a solid growth outlook, continues to gain share, and is the highest margin segment as well. This segment reported an EBIT margin of 21.7% in its most recent fiscal year and 22.4% in its most recent quarter.

Meanwhile, its closest imaging peer - GEHC - reported a segment margin of 12.1% in its most recent fiscal quarter. This sat within the historical range of 10-13%, as it continues to lack the margins reported by Siemens Health, indicating that Siemens has far superior pricing power and operational efficiency, fueling my confidence in Siemens' imaging operations. Of course, it's hard to compare the segments, and this should be taken with a grain of salt, but it nevertheless indicates operational strength from Siemens.

Also worth pointing out is that 40% of this segment's revenues are recurring, creating additional stability and revenue reliability. Management aims for 5-8% growth in the medium term and EBIT margin expansion of 20-90 bps annually. Considering everything discussed above, including the underlying market growth, the slight expected market share gains, and the incredible pricing power the company already holds, I view these targets from management as realistic and continue to view this segment as an important strength for Siemens Health.

Diagnostics - A promising segment despite near-term headwinds

Siemens Health's second largest segment is its Diagnostics unit, which focuses on providing a range of in-vitro diagnostics (IVD) products and services. In-vitro diagnostics involves the testing of biological samples (such as blood or urine) outside the human body to diagnose diseases, monitor treatment, and assess overall health. This includes equipment like clinical chemistry analyzers that perform tests on blood serum, plasma, and urine, immunoassay systems that detect and measure specific proteins, hormones, and antibodies in blood, and many more.

Diagnostics segment products (Siemens Healthineers)

{kind=link}

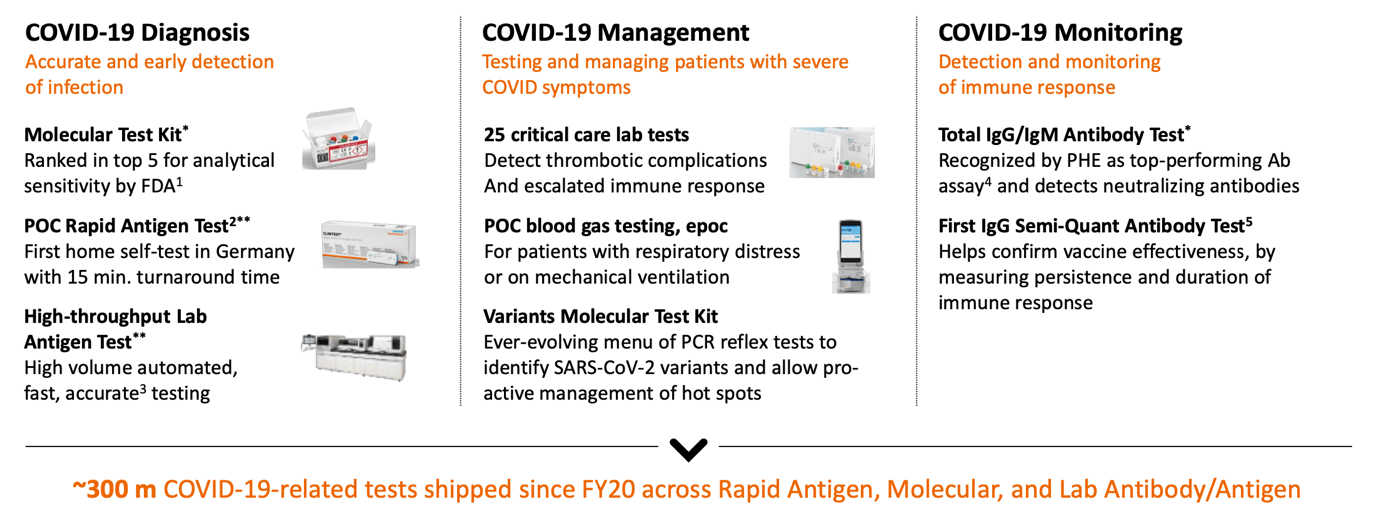

In addition, Siemens Healthineers offers point-of-care testing devices that enable healthcare providers to perform diagnostic tests at or near the patient's location, providing rapid results. This is also why the company has seen great benefits from the COVID-19 pandemic financially, as it rapidly brought strong testing products to market.

The company earned over €2.5 billion from COVID-19 antigen test kits over the last few years, boosting the performance of its diagnostics unit. However, this benefit has largely disappeared with the pandemic, as COVID-19 antigen test kits only brought in €53 million in the most recent quarter.

Siemens Health covid-19 products (Siemens Healthineers)

{kind=link}

Nevertheless, Siemens holds a strong market share in the clinical diagnostics market of 14%, making it the runner-up. Over the years, the company has strengthened its presence in the global IVD market by launching innovative solutions and expanding its presence in high-growth markets.

Still, this market share is less pronounced than we see in many of its other segments, primarily due to this market being highly fragmented. Siemens is one of the most established players but still needs to work on getting the most out of this segment, which does hold great potential.

By simplifying its product portfolio and focusing on a transformation program to boost the segment's performance, management is now trying hard to get the most out of this segment, but this is turning out to be a challenge due to significant competition, making it hard to make meaningful progress.

Meanwhile, the clinical diagnostics market is projected to keep growing steadily as well at a projected CAGR of 5.5% through 2028 , similar to the medical imaging market. The market is expected to grow due to the increasing incidence of infectious as well as chronic diseases and the rising adoption of automated platforms. This still presents Siemens Health with decent growth potential, even if it is only able to hold on to its current market share.

Today, the segment accounts for 21% of revenue, making it quite meaningful. Furthermore, while margins have been down in recent quarters due to the loss of COVID-19 revenue, it is normally able to report a very respectable EBIT margin of 13%. On top of this, diagnostic revenues are incredibly sticky, with a staggering 90% of this segment's revenues being recurring, indicating that any value created will stick with the business for the longer term.

This is because Diagnostic equipment often requires consumables and reagents for proper functioning. Siemens sells these through long-lasting contracts to customers, which results in these incredibly reliable recurring revenue streams. The reagents can only be used with the respective manufacturer's instruments, making these revenues so sticky to Siemens' installed base.

Therefore, I remain quite optimistic about this segment despite Siemens not being the industry leader and facing significant competition. I believe it is a meaningful contribution to the Siemens Health portfolio, lowering revenue cyclicality and potentially growing strongly.

Management aims for revenue growth of 4-6% annually in the medium term, which is a likely scenario. This would sit slightly below the projected growth for the overall industry, but some market share losses are possible, so these estimates aren't unrealistic. On top of this, management aims to grow the EBIT margin to a mid-teens level by 2025, which is not far from the segment's normalized margins.

However, despite these solid growth targets and my enthusiasm for the segment, the company is reportedly reviewing options for the operations that could lead to the sale of the unit, according to Reuters . Also, according to Reuters, the segment could be valued at as much as $8 billion, attracting plenty of interest from private equity firms.

Management has so far denied these claims and continues to claim that it is entirely focused on the segment's restructuring and is bullish on its growth potential here. For now, these are all just rumors, and I, for one, hope it does not evolve any further as I view the segment as a strong part of the Siemens Health portfolio.

Varian - Already the fastest growing segment and still a long runway of growth ahead

Varian is Siemens Health's cancer treatment segment and is the result of the acquisition of Varian Medical Systems in 2021 for $16.4 billion. Varian leads in the field of cancer care, specializing in radiation oncology solutions, including radiotherapy, radiosurgery, proton therapy, and brachytherapy. Products include advanced radiotherapy systems, which are used in cancer treatment, radiosurgery solutions, which allow for the non-invasive treatment of tumors using highly focused radiation beams, and others.

Through the acquisition, Siemens now also holds a strong position in oncology in addition to its already strong presence in cardiology and neurology. Furthermore, the acquisition reflected a strategic move to provide a comprehensive and integrated portfolio of solutions for cancer diagnosis and treatment. By combining Siemens Healthineers' expertise in diagnostic imaging and in-vitro diagnostics with Varian's capabilities in radiation oncology, the company aimed to offer a more holistic approach to cancer care, making it a top pick in the industry and giving it an edge over the competition, which should allow it to keep growing its market share as well.

Prior to the acquisition, Varian held a commanding market share in this industry (radiotherapy) of above 50% . Going by current revenue levels and the size of the industry, today, this still sits comfortably above the 50% benchmark, giving the company a very strong foothold in this industry.

Moreover, the Varian segment today is broader than just radiology equipment, following some acquisitions made by Varian prior to the Siemens acquisitions. As a result, the segment also has exposure to faster-growing verticals of the cancer treatment industry, which should result in a 2025 TAM of $17 billion, growing at a 6-10% CAGR.

Meanwhile, The radiology market is expected to keep growing steadily at a CAGR of around 5% through 2028 as the industry continues to face higher demand due to the growth in cancer patients and the technological revolution the industry is undergoing. Especially as healthcare infrastructure in emerging regions improves due to the growing wealth, this is still a massive growth opportunity. According to Siemens Health :

In the developed markets, the need for new capacity is relatively low and is mainly related to the aging of the population and the growing number of cancer patients.

In the developing markets, however, it is predicted that a large amount of entirely new capacity will be needed in the near future. In the rapidly developing Indian and Chinese markets, for example, the number of advanced oncology devices is still very low relative to the size of the population. In China, the number of Varian machines has grown at an average annual rate of 11% over the past five years.

Overall, this results in a strong outlook for the industry and the Varian segment, which continues to dominate this industry. Management believes it should grow this segment by high-single digits in the medium term, also driven by new synergies and product releases. This should also allow margins to expand rapidly to well above 20% in 2025. In FY23, the EBIT margin was 15.1%, sitting at the low end of the historical range (15-17%) due to recent headwinds. The segment has been facing significant supply chain headwinds in recent years but is now recovering, and this has led to a 4Q23 EBIT margin of 18.7%, already closing in on the 20% mark.

All things considered, I believe these goals are realistic, making Varian the fastest-growing segment in the medium term. With this now accounting for 16.5% of revenue, it won't be a very strong contributor to top-line growth in my view, but its share will expand strongly in the next few years, potentially growing to be the second-largest segment in below five years.

Advanced Therapies - Not overly meaningful in the big picture but operating strongly

Finally, there is the Advanced Therapies segment, accounting for just 9% of revenues in FY23. Meanwhile, though, this specific segment has an installed base of 45,000 and holds a 35% market share, according to Siemens Health.

The Advanced Therapies division provides comprehensive products, solutions, and services tailored for therapy departments within healthcare institutions. Key products within this segment encompass angiography systems and mobile C-arms. Simply put, Siemens Healthineers is involved in developing technologies to support advanced therapies, including robotic surgery and image-guided interventions.

Advanced Therapies segment products (Siemens Healthineers)

{kind=link}

While Siemens Health operates in a very specific niche in this industry and has a limited product offering, it is worth noting that this industry is projected to grow at a CAGR of 16.6% through 2032 . Meanwhile, management itself aims for growth of 5-8% in the medium term, driven by strong growth in both cardiovascular and Neurovascular care. Furthermore, the EBIT margin is expected to expand from an FY23 level of 15.4% to over 20% by 2025, driven by efficiency gains.

Competitive advantages, industry growth, and AI

As discussed in the previous sections, all operating/product segments are expected to continue growing strongly, driven by strong market shares in each due to a strong product offering and approach and a promising underlying industry outlook. The company is a leader in most of its operations, and not without a reason.

However, what further sets Siemens Health apart from the competition is the way the different segments complement each other, allowing Siemens to dominate in certain medical areas like oncology, cardiology, and neurology, as well as the company's holistic approach to these specific areas. According to Siemens, its imaging, Varian, and Advanced Therapies segments are truly synergetic.

Siemens Health focus areas (Siemens Healthineers)

{kind=link}

As management puts it: "The joint portfolio makes us stronger and more valuable for our customers." By offering equipment for all stages of treatment, from detection to surgery, Siemens can benefit from growth in the entire industry and generate more robust relationships with its clients.

This, in combination with everything already discussed, positions Siemens Health favorably to benefit from the secular trends driving this industry, like a growing and aging population and expanding insurance coverage, resulting in more people getting access to health care and the rise in noncommunicable diseases, especially cancer and cardio and neurovascular diseases. This should ensure secular and stable procedure growth, ensuring resilient demand for the company's products and services.

Innovation, particularly AI, is another crucial factor driving growth in the medical equipment industry. The company already has 60+ products in imaging enriched with AI, and the potential for Siemens and its peers as AI continues to develop and demand growth remains massive. Siemens acknowledges this opportunity and is already looking to integrate both image recognition and Gen AI capabilities into its software and equipment.

Using Siemens Health AI solutions in healthcare could, for example, allow healthcare providers to scan hundreds of databases for information about the patient or their illness by using natural language with the power of large language models and get a clear picture. Eventually, using such applications will allow medical professionals to identify possible issues in the course of treatment very easily. Furthermore, AI algorithms can automate the analysis of medical images, identifying patterns or anomalies that may be challenging for human eyes to detect, playing a crucial role in the detection and treatment process.

As for growth in this industry, this is what I wrote in my GEHC article:

Meanwhile, Morgan Stanley estimates that AI will represent 11% of healthcare budgets in 2024, showing rapid growth and making it a massive market.

Moreover, according to Acumen Research and Consulting, as a result of these growing budgets and the focus on AI, the Healthcare AI market is projected to grow at a stellar CAGR of 44% through 2032, representing a massive runway of growth for GEHC.

While the impact of AI innovations for Siemens and peers is still hard to identify precisely, it is safe to say that AI will be a growth driver as the importance and potential of the technology in disease treatment is obvious. However, I do remain careful in integrating this into financial projections due to the uncertainties still present.

The company is poised for strong growth and margin expansion

All things considered, management now targets revenue growth at a CAGR of 6-8% in the medium term, and considering the growth projections for each segment, the contribution of AI, and the company's overall leading position in a steadily growing healthcare equipment market, I believe growth could come in at high-end of management's targeted range. Most importantly, these growth targets for management are realistic and should be achievable.

The company's high-quality revenue stream, of which 55% is recurring, supports this. In Imaging, Varian, and Advanced Therapies, this amounts to 45%, and this comes from service and software revenues. On top of this, Siemens often closes value partnerships, which means the company makes large multiyear deals with customers. These deals include equipment, services, and solutions to be provided and generate significant levels of recurring revenue.

Ultimately, all this recurring revenue stabilizes revenue volatility from quarter to quarter and protects the company from external factors. For example, during the pandemic, Siemens Health reported just two quarters of negative growth due to these recurring revenues.

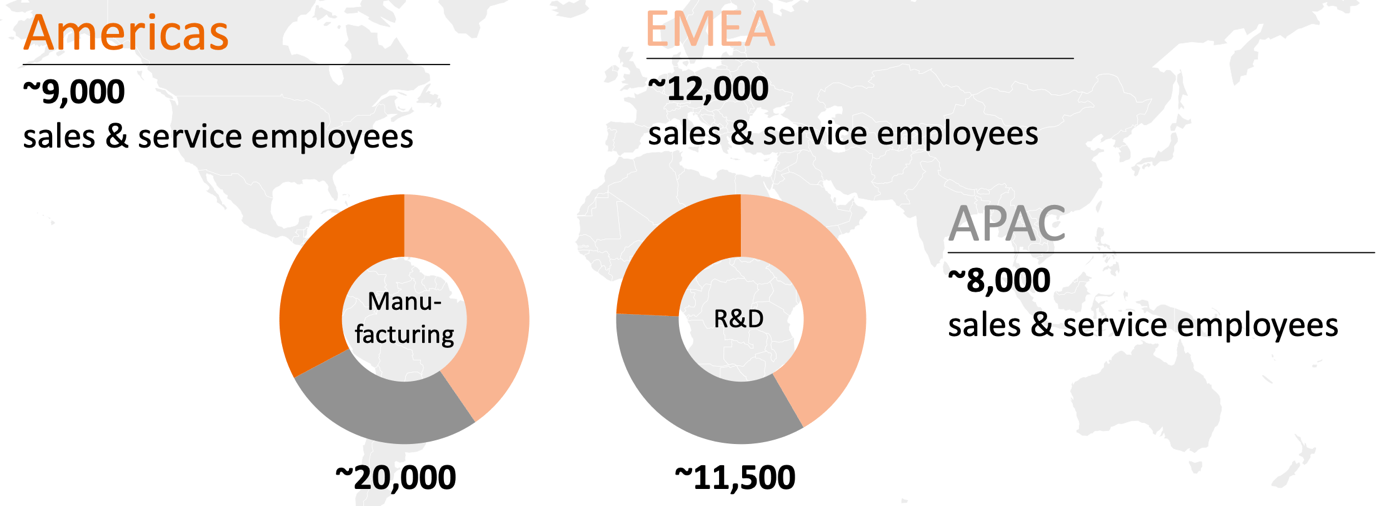

Furthermore, the company is excellently diversified in terms of geographical production and revenue, with the number of employees split over three regions - Americas, EMEA, and APAC - almost perfectly. The company has manufacturing and research facilities across the globe, which allows it to get equipment to customers quickly and be less sensitive to local disruptions. On top of this, no single region accounts for a dangerous level of revenue, with North America, the company's largest region in terms of revenue, accounting for just 41% of fiscal FY23 revenue, followed by the EMEA at 32%, Asia Pacific Japan at 14%, and finally China at just 13%. This indicates that the company's revenues are well diversified geographically and shows that the far majority of revenues are derived from Western and more stable economies, further lowering revenue fluctuations and risks.

{kind=link}

Also, the company has consistently been growing R&D investments in line with revenue. As a result, this has consistently been 9% of revenue, and Siemens remains committed to these investments to drive innovation. This has been one of the biggest negatives in my GEHC article as Siemens competitors lack in terms of R&D spending, and in an industry where innovation is critical and the main driver of growth, one can't afford to drop the ball in that area. Positively, Siemens hasn't, and it remains committed to spending around 9% of its revenue on R&D, translating into over €2 billion annually.

Driven by this investment and revenue consistency, top-line growth should be stable and consistent, giving the company great bottom-line leverage, which should lead to EPS growing at a more meaningful 12-15% in the medium term, according to management. Contributing to this are also the additions of new recurring revenue streams - from expansion into digital and tech-enabled services - which carry higher margins.

I am very impressed by Siemens Health. Unlike healthcare equipment companies I have discussed on Seeking Alpha in recent months, Siemens Health has a strong product portfolio, a substantial market share in each of its end markets, and is operationally superior to any of its peers. The company has a determined and well-educated management team that knows where to steer this company and is realistic in its growth targets. Honestly, I have little negative to say about this company.

However, to better understand its recent financial performance, let's quickly dive into the most recent financial results.

Q4 and fiscal FY23 were impressive in terms of growth, order intake, and margin expansion

Siemens Health reported fiscal Q4 earnings on November 9 and ended the fiscal year on a high, reporting revenue growth of 7.5% YoY but 10.8% excluding antigen revenues, which comes on top of double-digit growth in the prior year. Q4 revenue was €6.06 billion, bringing the FY23 total to €21.68 billion, up 1.2% YoY. The company has shown strong comparable growth throughout the year, with growth accelerating sequentially in each quarter as it continues to recover from significant supply chain headwinds.

This was especially visible in the Varian segment, which grew revenues by 30% YoY in Q3 to €1.02 billion, which also led to significant margin expansion. For reference, over the full fiscal year, the segment's revenue is up just 14.8%. The strong Q4 growth was partly due to catch-up revenues from Q3 but was mostly driven by the successful conversion of the strong order backlog into revenue. On top of this great recovery, Varian still achieved an equipment book-to-bill of 1.2x, which is quite impressive.

Meanwhile, the imaging segment also grew strongly in Q4, with revenues up 10.6%, followed by the Advanced Therapies segment, with revenues up 5%. The Diagnostics segment, however, continued to be impacted by the lower antigen revenues, which resulted in a revenue contraction of 10.6% in Q4 and 24.2% in fiscal FY23. Excluding antigen, the business continued to grow by 2% in Q4 and should see growth improve as it laps easier comparable quarters in fiscal FY24.

Growth was also driven by most regions, with the Americas up 13% YoY and EMEA up 14%, ex-antigen. With these regions accounting for the far majority of revenues, this drove most of the growth. Meanwhile, Asia Pacific Japan was also strong, with revenues up 10% YoY, but this was somewhat offset by 3% negative growth in China as a result of anti-corruption measures by the Chinese government. This should only be temporary, though, and demand is only being pushed forward. This should recover strongly in the next couple of years.

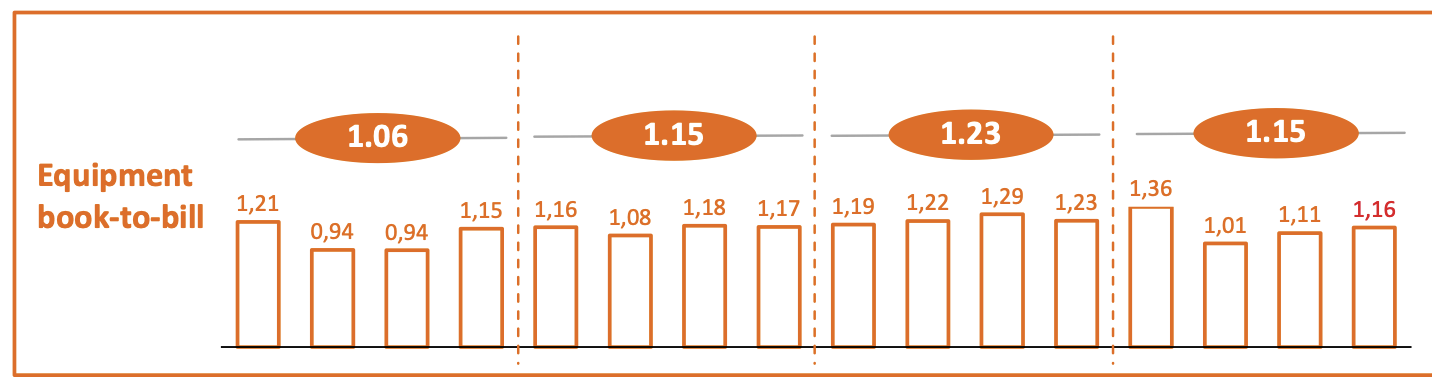

Despite the very resilient top-line performance in both Q4 and FY23, Siemens was still able to report a positive book-to-bill ratio of 1.16x for Q4 and 1.14x for its fiscal FY23, which is just stunning and far stronger than reported by peers. For comparison, close peer GEHC reported a book-to-bill of 1.01. This highlights that demand for the company's products remains incredibly strong, especially considering that the company saw very low orders from China due to local headwinds.

Fiscal 2020-2023 book-to-bill (Siemens Healthineers)

{kind=link}

As a result of the strong Q4 performance, the book-to-bill has been above 1x since fiscal Q1 2021, and this is a crucial indicator of consistently strong demand but also of market share gains as no company is able to match this - and these market share gains are essential. This is how management explained it during the Q4 earnings call:

First, with an equipment book-to-bill continuously above 1, we continue to gain market share, which is the main driver for continuously growing equipment revenues, thereby creating value. Second, by gaining share, we continuously expand our installed base, creating the basis for continuous strong service revenue growth, again, thereby creating value. Third, our innovation leadership lets us participate in the innovator premium in the market, while our continuous growth gives us operating leverage, both expanding our innovator margins and thereby creating value.

I couldn't have said it better, and this perfectly illustrates why this company is able to outgrow its peers. It is able to drive continuous innovation, strengthening customer relations and resulting in market share gains, which then results in these incredible order intake numbers, supporting financial growth.

This, in turn, gives the company greater operating leverage, allowing for margin expansion. In Q4, the EBIT margin, excluding antigen, increased by 160 basis points to an industry-leading 16.3%. This resulted in a fiscal FY23 EBIT margin of 14%, in line with the prior year, as improvements only kicked in in Q4, and the company was impacted by currency headwinds.

A big part of the Q4 margin expansion was driven by the strong rebound in the Varian segment, which saw its margin improve by 660 basis points YoY to 18.7% despite margin headwinds of 100 basis points. Completing the picture, the Imaging EBIT margin fell 40 basis points in Q4, while Advanced Therapies was up 220 basis points.

This margin expansion in Q4 allowed for EPS growth of 3%, despite increased interest and tax expenses in Q4, to €0.58. This brings the YTD total to €2.02. Furthermore, free cash increased 23% YoY in Q4 to €557 million, bringing the FY23 total to €1.28 billion.

As a result of these solid cash flows, management was able to strengthen the balance sheet, lowering its net debt position to €10.8 billion compared to €11.7 billion one year ago, comprised of €1.74 billion in cash and debt of €12.5 billion. This leaves the company in excellent financial health and not far from its net debt/EBITDA target of 3x by the end of 2024. Management plans to keep deleveraging the balance sheet over the next few years beyond its FY24 target.

This healthy balance sheet also allows the company to keep paying a solid dividend. Shares currently yield 1.8% based on a payout of €0.95 per share. With current shares outstanding of just over 1 billion, this means the company currently pays €1.06 billion in dividends annually, well covered by FCF.

Moreover, based on the current fiscal FY24 EPS consensus of €2.21, this represents a payout ratio of just 41.5%, indicating that the dividend continues to be well covered and sits comfortably below management's target range of 50-60% of net income.

Taking my EPS projection for 2026 and a conservative dividend payout ratio at the low end of management's guided range (50%), this results in a potential dividend of €1.42, reflecting a dividend growth CAGR of over 14%.

The most important takeaway is that the current respectable yield of 1.8% is well covered, and investors should be poised for very decent dividend growth going forward. In addition, the company's margins are much stronger than those of peers across the board, demonstrating the company's edge over the competition in terms of pricing power, product quality, and customer relationships.

Outlook & Valuation - Is Siemens Healthineers stock a Buy, Sell, or Hold?

For fiscal FY24, management now guides revenue growth between 4.5% and 6.5%. Excluding antigen revenue in fiscal FY23, this represents growth of between 5% and 7%. This includes the expectation for no antigen revenue in 2024 and Chinese anticorruption campaigns continuing to be a headwind of around one percentage point on both the top and bottom lines. However, it is worth noting that management expects this headwind to be only temporary and that Chinese demand will rebound quickly over the next few years.

Growth will be driven by all segments growing more or less in line with management's growth ambitions communicated earlier. This is quite optimistic considering the headwinds the company is facing and the tough comparison to a very strong 2023. Furthermore, as a result of resilient top-line growth, management also expects to see operational margin expansion in all segments, excluding the headwinds from foreign exchange and the temporary impacts from China. This leads to fiscal FY24 EPS guidance of between €2.10 and €2.30, which is up 9% YoY at the midpoint. This includes a €0.06 headwind from Chinese anti-corruption campaigns and a €0.18 headwind due to the unusually low tax rate in fiscal year '23 and the higher interest rates coming through in fiscal year 2024. This means that excluding these temporary effects, EPS would be up 21%, easily surpassing management's target range of 12-15% EPS growth.

On top of this strong fiscal FY24 guidance, management also reaffirmed its long-term bullishness as it expects growth to remain strong for the foreseeable future, in line with medium-term goals. This means comparable revenue growth in the mid to high single digits and double-digit earnings growth beyond 2025. This will be driven by mid-single-digit growth in Imaging and Advanced Therapies, high-single-digit growth in Varian, and Diagnostics growth in the low to mid-single digits. Consequently, on margins, Imaging is to continue its margin expansion from scale, Varian is to advance to imaging-like margins, Advanced Therapies is to return to industry-leading margins, and Diagnostics margins are to advance to mid-teens. This paints a very bullish picture across the board, and recent performance and developments fully support this, as highlighted in this article.

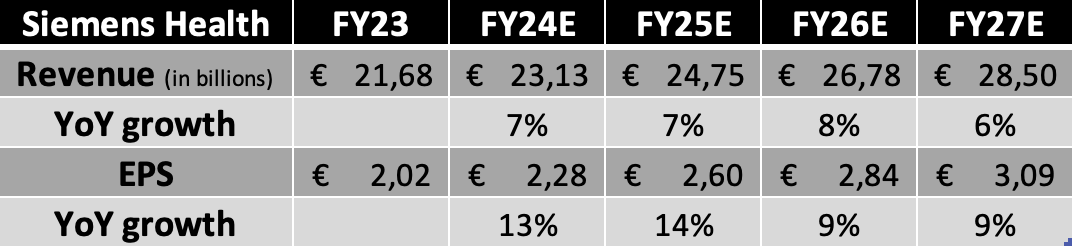

Considering this guidance from Siemens management, my research laid out in this article, and the strong FY23 result, I now project the following financial results through fiscal FY27. This reflects my slightly higher expectations for FY24 than guidance, as I believe management is slightly conservative in its estimates.

Financial projections (Author)

{kind=link}

Overall, looking across the financial and performance metrics, I am quite happy with Siemens Health's performance as it just has the edge over the competition across the board, whether it's top-line growth, margins, order intake, or anything else. In my eyes, this company has a clear competitive advantage and is operationally superior to most of its peers. The company holds the number one or two positions in each of its operating segments and has an industry-leading margin profile that sits far above its closest peers. This is why the company most definitely deserves to trade at a premium.

However, the current valuation might be too demanding. Based on my projections above, shares currently trade at 23x this year's earnings, a significant premium to close but inferior peers Philips and GEHC, and roughly in line with high-quality peer Abbott Laboratories. Moreover, this is a 23% premium to the sector median. And yet, considering the company's impressive growth outlook, revenue reliability and stability, leading market positions, and knowledgeable management team, I believe the company deserves a premium valuation.

All things considered, I believe a 23x multiple is fair, meaning shares currently trade around fair value, indicating these are indeed richly priced. Based on my fiscal FY25 EPS, I calculate a target price of €60 per share, leaving an upside of just 14% over the next 24 months. Furthermore, based on my FY26 EPS projection, from a current share price of around €52.50, investors can expect annual returns of around 7% or closer to 9%, including dividends.

This puts shares on the edge of fair value and slightly overpriced based on long-term return potential. However, considering the current uncertain macro environment, high interest rates, and the risk of a recession, I take a more conservative stance right now and rate shares a "Hold" despite my enthusiasm and bullish growth expectations. I believe shares would present a more compelling investment case at a share price of below €50 per share, a level shares traded on as recently as November 20th.

For now, I rate shares a "Hold" but recommend investors to take advantage of any share price dip below €50 per share to initiate or increase a position in this incredibly high quality healthcare leader.

For further details see:

Siemens Healthineers: A High Quality Option In The Healthcare Industry