SEMHF - Siemens Healthineers: Strong Return Still A 'Buy'

2023-12-10 23:28:31 ET

Summary

- Siemens Healthineers reported strong 4Q23 results with revenue growth of 11% and adjusted EBIT growth of 16%.

- The company aims to achieve double-digit EPS growth by 2025 and beyond through expansion in new areas and geographies.

- Despite a slight premium in valuation, the company has the potential to generate a significant rate of return for investors.

Dear readers/followers,

If you remember my work on Siemens Healthineers ( OTCPK:SEMHF ) ( OTCPK:SMMNY ), you'll recall that my last article, like in every article since I first started covering the business, considered it to be a "BUY" from a valuation perspective, combining fundamentals with forecasts and potentials. While my last article was during the depths of a deep drop, this was timed very well - take a look at the comparative RoR at the same time next to the S&P500.

Seeking Alpha Healthineers (Seeking Alpha)

Anyone who believed the company would remain at the low valuation we saw it at during September was proven momentarily wrong. Finding quality in the current investment context isn't as hard as it once was - but I would argue that it's still difficult to find quality and undervaluation at the same time. This is especially true for lower-yielding companies. A few years ago, a yield of 1-2.5% wasn't a big deal - risk-free rates and interest rates were so low that low dividend yields caused a shrug, no more.

I believe that while Siemens Healthineers offers no material or attractive dividend, but makes up for this with a combined upside and attractiveness in this context.

Let me show you what I mean.

Siemens Healthineers - An upside of double-digits still at this time.

What has changed since the last article I published back in September is that the company, back in early mid-November, published its 4Q23 results. This in turn resulted in an upswing - and that's what we'll take a look at here. (Source: 4Q23 Siemens Healthineers )

The company comes in 4Q with a strong finish to an overall volatile year, not in the least in terms of the company's valuation. We have 1.16x book to bill, a revenue growth of 11%, an adjusted EBIT growth of 16%, and generating over half a billion euros in Free Cash Flow.

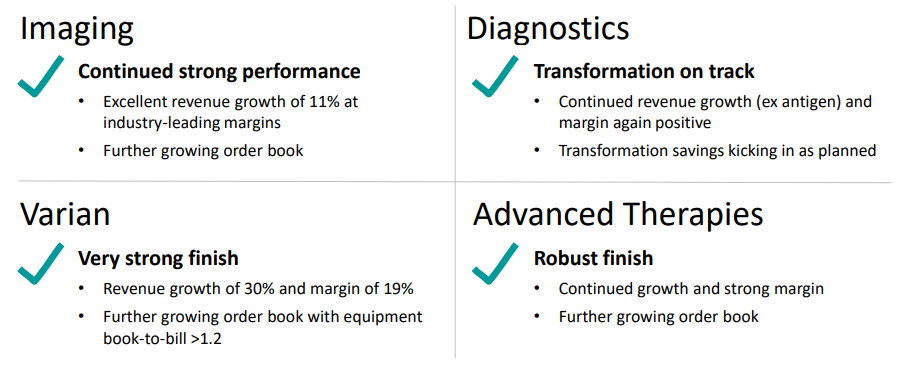

This growth came from across all of the company's attractive segments.

{kind=link}

Siemens Healthineers IR (Siemens Healthineers IR)

I am no longer invested heavily, or to any real extent in pharma, with very few exceptions. Instead, my focus in investing has been the medtech sector. Siemens Healthineers is a very obvious example of this ambition and target. The company confirmed in 4Q23 the quality of this idea, showing innovations introduced to most market segments, reorganizing the diagnostics segments, executing pricing measures, winning partnerships, growing EPS by 13%, and an adjusted basic EPS of just north of €2/share. The company also proposed a dividend of €0.95/share. For the native ticker SHL, this comes to a dividend yield of just south of 2%, currently trading at €52/share. (Source: 4Q23 Siemens Healthineers)

The company's current plan is relatively simple. Sustaining that double-digit EPS growth by 2025E and beyond, with a target for adjusted EPS growth of 12-15% CAGR in 2 years, with double-digit targets beyond 2025.

This growth will be achieved in two ways.

First of all, expansion of the company's care and products. The company obviously wants to expand its sales to new areas and new geographies. This will likely be the main growth vector for the company, boosted by innovation around the world as we see more adoption of things like robotic treatments, new theranostic agents, better devices, and new drugs. The company is almost in all of these segments. Challenges in key sectors such as hospitals also provide tailwinds here, with staff shortages, hospital consolidation, cost pressure, and growth in the overall procedure. Then there are the "classic" trends that we've been looking at for 5-10 years and which I in my non-analyst work face every day as well - such as the growing population, and the growing aging population. (Source: 4Q23 Siemens Healthineers)

All of these trends are generally favorable one way or another to Siemens Healthineers. Beyond that, optimizing pricing and making sure the operations run as smoothly as possible should ensure that the company manages to "stay ahead" here.

{kind=link}

Siemens Healthineers IR (Siemens Healthineers IR)

Overall, it cannot be argued that 4Q was a very strong finish to a good year. The growth we're talking about came in all geographies except China, which was negative due to a temporary downturn, but still did not impact heavily the company's margin growth for the year, with EBITDA margin up 1.6% in this year alone, and a 23% increase in company FCF for the year.

The quality of the revenues generated by this company is very high. We're not talking about one-time revenue sources, but recurring revenues with services and software as a key portion of the mix. While little over 55% is still non-recurring, we're now at over 40% recurring revenues within the company's core segments Imaging, Varian, and AT, while Diagnostics has a recurring revenue model where 90%+ of the revenue is recurring , due to reagent revenues and a razor-razorblade business model (the concept of which should be fairly self-explanatory). (Source: 4Q23 Siemens Healthineers)

We can also view this as a product of the environment from a post-pandemic perspective.

{kind=link}

Siemens Healthineers IR (Siemens Healthineers IR)

The most meaningful indicator for any sort of company growth here is the book-to-bill - and as you can see, this indicator is going straight in the positive direction over time and compared to 2020. This reflects the equipment order growth, and while these trends move in the ups and downs, they have held at a relatively steady level overall - when one area is down, another is up - for some time.

The outlook for the 2024 fiscal is a positive one as I see it. I expect continued revenue growth despite macro challenges of at least 4%, upwards of 5.5% potentially. The company goes to 6.5%, 7% ex-antigen, with a basic EPS growth of up to €2.3/share. If this materializes, then this company is not currently at its valuation premium, but below it, and could present an interesting investment.

But before we decide that, let me show you the core ups and downsides I see for Healthineers here.

Risks & Upside

The risks to Siemens Healthineers are mostly valuation-related. While we could go into the risks inherent in a MedTech business of ups and downs - and the company has seen its share of slight cyclicality since its listing in 17/18, the overall trend has been an EPS growth rate of around 8% annually, and investors have done very well for themselves with a total TSR since mid-2018 over 11% per year.

The main risk to watch for, according to this analyst, is therefore the valuation at which you "BUY" Siemens Healthineers. As long as that is solid, you should be solid.

The upside is this legacy of quality medtech that you're buying into. The current estimated growth rate in earnings calls for this company to see an upward trajectory of at least 10-15% per year for the next 3 years. Provided this materializes, this presents, even at a slight premium, a significant RoR potential for valuation-conscious investors.

Let's look at valuation.

Valuation for Healthineers

The valuation for Healthineers is tricky here. If you recall my "base" price target for the company from my last investment article, it comes to €56/share. I'm not changing this target here, and this is for the native SHL ticker on the German stock market. However, we also need to acknowledge that the company, on a normalized valuation basis, trades at 25.4x P/E, with a 5-6-year valuation average of 25.5x. That means that it's really a hairline's width from being at a premium, despite my share price target.

My target is forward-looking. My target also means, in this context, that I accept this premium (one of the few I accept) and that I would expect the company's growth rates to materialize more or less as they are expected here.

If this comes to pass, then this investment has the potential to generate for investors an annualized rate of return of 16.29% at the safety of the parent's credit safety of A+, despite Healthineers itself not having any sort of credit safety (nor does it need one, with Siemens). The company also has a debt/cap of less than 36%, to mention that as well.

This means that the company, despite its valuation, has the potential to generate over 50% RoR in 3 years with one of the safest profiles in MedTech. My own potential TSR is upwards of 70% because I invested far cheaper when the company was at my last article's pricing level.

I'm not stumbling over rocks at this point to invest in Healthineers. It's a fair price, and I certainly won't change my price target here - but there are many alternatives available on this particular market, many of which offer significantly better upsides to you as well. 16-17% annually is market-beating and great, but 20-30% aren't "hard" to find per se, not anymore.

So take a look at Healthineers - and see if it fits your investment profile. This would be my typical M.O. for this company, and what I view to be a fairly objective view of looking at this business. Despite what's going on in the world today, I do not view this as a good time to "lose your head" and start throwing curveballs in the hope of making a buck - or a thousand.

I am doubling down on quality. Healthineers is one of those qualitative companies that I am doubling down on.

S&P Global analysts who follow the company are surprisingly positive despite the material premium here. Out of 20 analysts, 18 have the company at a "BUY" or "Outperform", only 2 at "HOLD" and none at a negative rating. The targets start at €48/share with a high range of €61/share, and an average of €57/share, very close to my own €56/share. In this case, I am in agreement with the analysts here and would consider the company a clear "BUY" up and until the company hits that €56/share.

Here is my thesis for the company as it stands.

Thesis

- Healthineers is among a class-leading group of companies in the medtech/equipment sector. While not the most profitable nor the most qualitative, nor the highest yield available, it nonetheless presents an appealing thesis with the potential for a double-digit upside at a parent's credit safety of A+/A1. This is worth noting and worth considering.

- I give the company a rating of "BUY" due to the aforementioned combinations of fundamental stability, strength, peer/comp appeal, and relative upside in an uncertain world. What challenges there are, I believe Healthineers will master.

- Healthineers is now a company that I can consider "cheap" as it has dropped significantly from my latest set of results and overall estimates.

- My PT is €56/share for the native, updated per December of 2023.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is now no longer "cheap" to me, but still constitutes a "BUY" here.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Siemens Healthineers: Strong Return, Still A 'Buy'