SFFYF - Signify: Offers 5% Dividend Yield Covered By A 14% FCF Yield

2023-03-23 11:30:00 ET

Summary

- Signify, a spin-off from Philips, is a specialist in lighting solutions.

- The underlying free cash flow result of the company is still impressive. Expect the FCF to hover around 500M EUR per year for the next few years.

- A portion of the FCF is used to cover the dividend, the remainder is used to reduce the gross debt and net debt on the balance sheet.

- Signify is not expensive.

Introduction

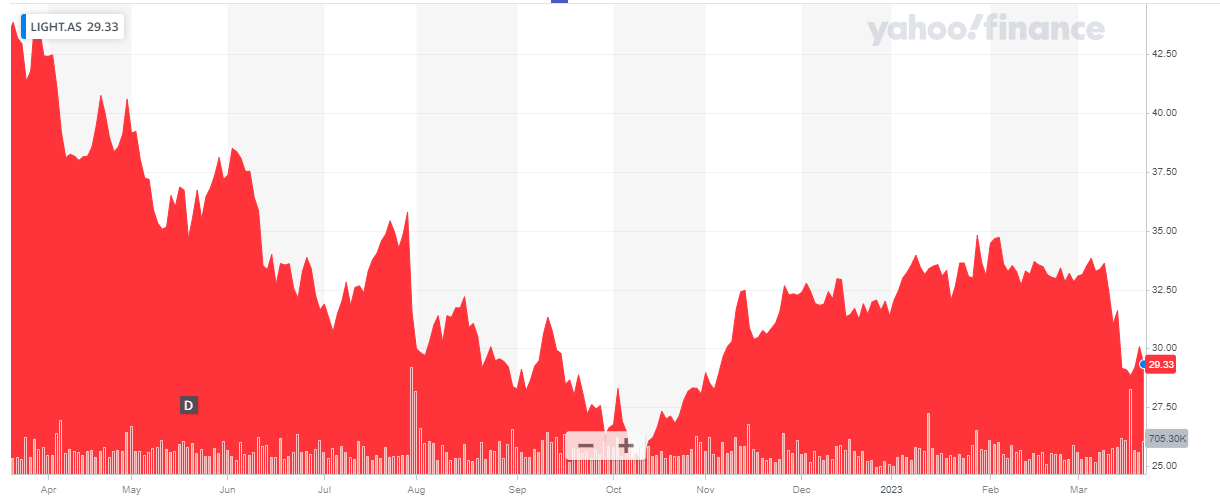

It's been almost six months since I turned bullish on Signify ( PHPPY ) ( SFFYF ) in the fourth quarter of last year, and the share price hasn't disappointed. While the share price was trading at just 26.22 EUR when I wrote the previous article, the current share price is 29.3 EUR while the stock reached a high of approximately 35 EUR earlier this year. Needless to say, I am happy with the share price performance, but I wanted to have a closer look at the company's full-year performance and guidance for 2023.

{kind=link}

The company's main listing on Euronext Amsterdam is much more liquid, with approximately 50,000 shares being traded on a daily basis. The current market capitalization is about 3.7B EUR, based on a total amount of just under 125M shares outstanding. Signify used to have a pretty aggressive share buyback plan, but a 1B+ EUR acquisition a few years ago meant a shift in priorities to debt reduction and balance sheet strength. That's fine with me and likely the best choice given the recent evolution of interest rates.

I turned bullish in October last year and the performance lived up to my expectations

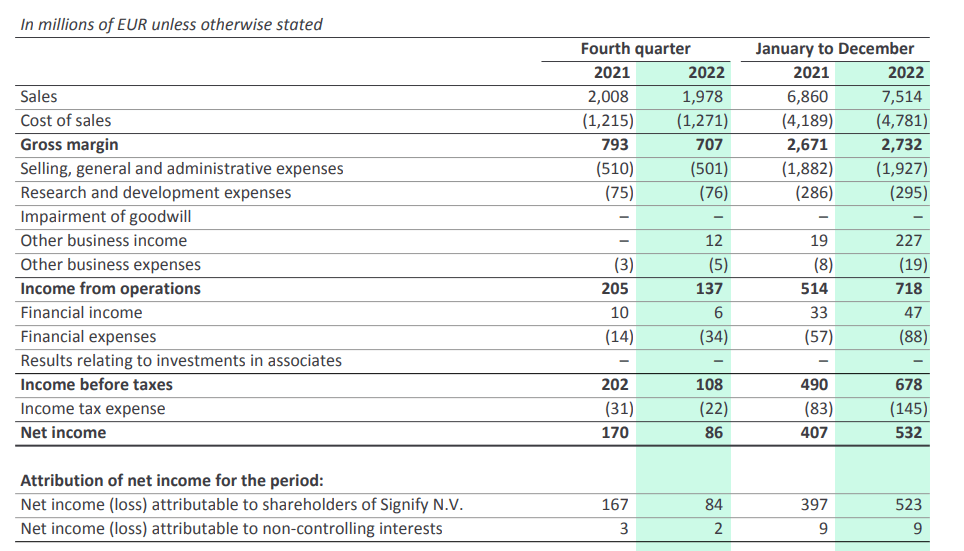

The main reason why I liked Signify is its very strong free cash flow generation. And Signify didn't disappoint in 2022. The total revenue came in at 7.5B EUR which is a 9.5% increase compared to the preceding year while the comparable sales growth was approximately 1.2%. As the inflation rates had an impact on the entire world economy, Signify didn't escape the impact of a higher inflation rate either as its EBITDA margin (Signify reports an EBITA result and no EBITDA result) fell from 11.6% in 2021 to 10.1% in FY 2022.

That's not ideal but considering the hand Signify was dealt with, I am pleased with how the company tackled the issues with a continuing strong focus on the connected lighting business which benefits from the push toward energy efficiency.

{kind=link}

As you can see in the image above, the company was still able to increase its gross margin while its operating income increased by approximately 40%. But it's easy to see the increase in the income from operations was fueled by the 208M EUR increase in the 'other business income' which pushed the operating income to 718M EUR. As I explained in my previous article, that was related to the gain on the sale of real estate assets, a non-recurring item bringing in almost 200M EUR. A nice gain, for sure, but non-recurring.

The reported net income was 532M EUR of which 523M EUR was attributable to the shareholders of Signify while the remaining 9M EUR was attributable to the non-controlling interests. The reported EPS was 4.18 EUR per share, based on an average share count of 125M shares. But the normalized net income would obviously have been approximately 30% lower.

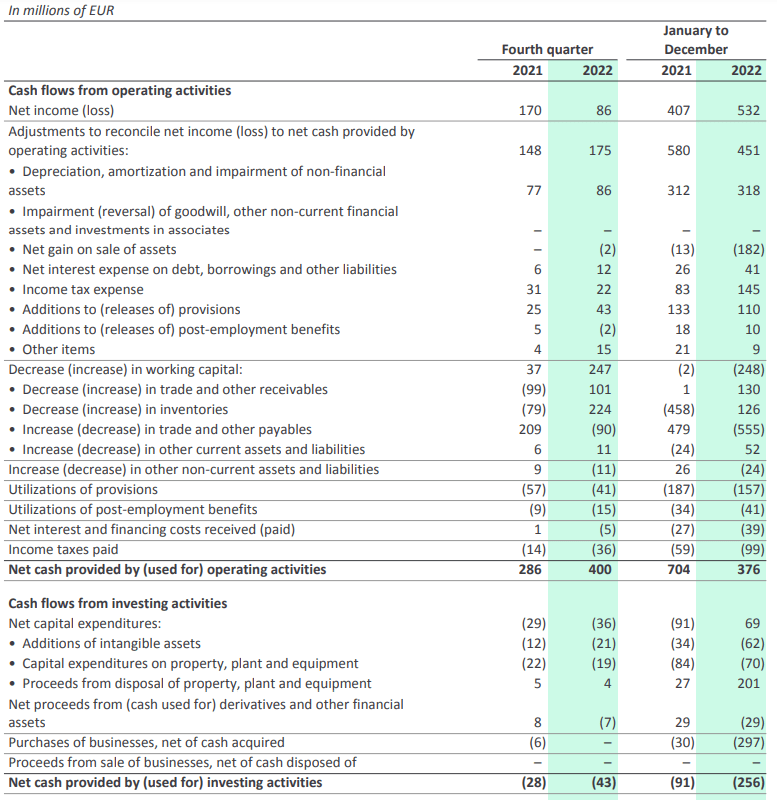

My original investment thesis in 2020 and the follow-up article in 2022 were focusing on the ability of the company to generate a positive free cash flow. And in Signify's case, it still makes sense to focus on the cash flow statement, as it also isolates the impact of the non-recurring gain on the sale of real estate.

As you can see below, the company reported an operating cash flow of 376M EUR, but this includes a 248M EUR investment in the working capital position. Adjusting the reported result for this element, the underlying operating cash flow was 624M EUR. That's still lower than the 706M EUR in adjusted operating cash flow reported in 2021 but keep in mind Signify is still working towards restoring its margins.

{kind=link}

From the 624M EUR in operating cash flow, we still need to deduct the 132M EUR in capital expenditures (an increase compared to the 118M EUR in capex incurred in 2021) which results in a net underlying free cash flow of 492M EUR (compared to almost 600M EUR in 2021). Divided over almost 125M shares, the underlying free cash flow per share (excluding the non-recurring contribution from the sale of real estate) was approximately 4 EUR per share. The main reason for this difference is the substantial difference between the depreciation expenses of 318M EUR and the total capital expenditures, which are less than half that.

You also notice Signify only paid 99M EUR in taxes although 145M EUR was owed, but that includes the taxes owed on the sale of the real estate assets.

Signify has also already provided a guidance for 2023. Unfortunately, no revenue guidance was given but the average consensus for the FY 2023 revenue is 7.25B EUR . Signify did provide an EBITA guidance and an FCF guidance: it plans to increase its EBITA margin to 10.5-11.5% while the free cash flow result should be 6-8% of its total revenue.

That still complicates the calculations, as there's for instance no way of knowing how the working capital elements will have an impact on the free cash flow generation. But based on a consensus estimate of 7.25B EUR for the revenue, the free cash flow result will come in anywhere between 450M EUR and 600M EUR. Looking at the consensus estimate, the average free cash flow result is estimated at 612M EUR for 2023 followed by 666M EUR for 2024. The lowest estimates for both years are 448M EUR and 367M EUR respectively, but that is completely depending on what those analysts are expecting in terms of working capital needs as those estimates range from 448-688M EUR in FY 2023 and 367-657M EUR in 2024.

Investment thesis

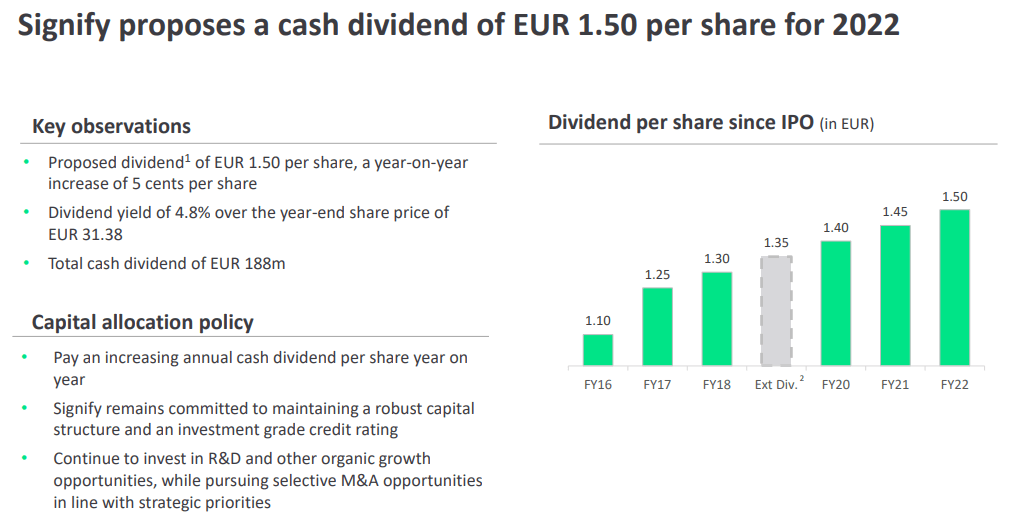

I think it is safe to assume Signify's 2023 free cash flow result will likely come in around 500M EUR, again adjusted for working capital changes. This makes the stock still very appealing as even after the share price increase since my October article was published, the implied FCF yield is still approximately 14% while the 1.50 EUR dividend represents a dividend yield of in excess of 5% (subject to the standard 15% Dutch dividend withholding tax) while the company retains a large chunk of cash to reduce its net debt.

{kind=link}

The net debt stood at 1.36B EUR as of the end of last year, resulting in an enterprise value of 5.05B EUR. That's just over 6 times EBITDA (this time including the depreciation expenses) which is reasonable. Don't expect massive revenue or earnings growth from Signify, but the dividend should be reliable while the company works on reducing its net debt.

For further details see:

Signify: Offers 5% Dividend Yield Covered By A 14% FCF Yield