SFFYF - Signify: Weaker-Than-Expected Q2 Still A Buy

2023-08-09 02:02:37 ET

Summary

- Signify's Q2 results showed lower sales and a potential slowdown in the non-residential real estate construction market.

- The company lowered its 2023 guidance with an EBITA margin in line with our previous analysis.

- Despite challenges, Signify offers a 5% dividend yield and has the potential to deleverage. We lower our target price, maintaining a buy rating.

It was not a positive quarter for Signify ( OTCPK:PHPPY , OTCPK:SFFYF ). Here at the Lab, we recently initiated to cover the company with a buy rating target and a supportive analysis called ' Time To Enter . ' Since our release (Jun-end), Signify has been up by 6.77% on the stock price level, outperforming the S&P 500 return. Our overweight was supported by 1) an ESG upside due to the current climate change fight to lower energy consumption (LED is more efficient than conventional bulb products), 2) an FCF yield higher than the dividend yield, and 3) a supportive balance sheet with an ongoing de-leverage plan.

{kind=link}

Here at the Lab, we follow an income-oriented strategy with a deep-value analysis. These calls are not easy to make, especially when the company is in a declining cycle. Looking at the Q1 results, we anticipate lower sales of 4.7% and 3% in 2023 and 2024, respectively. Also, we forecast and adj. EBITA level of 10.1% and 10.2% for the next two years. What is critical to report is the company's new 2023 guidance. The new outlook would not appear to be fully de-risked. This is due to lower sales than expected and a potential slowdown in the non-residential real estate construction market. This is Signify's primary market. Today, our internal team lowered Holcim's target price due to the ongoing concern ' About Real Estate ' development.

{kind=link}

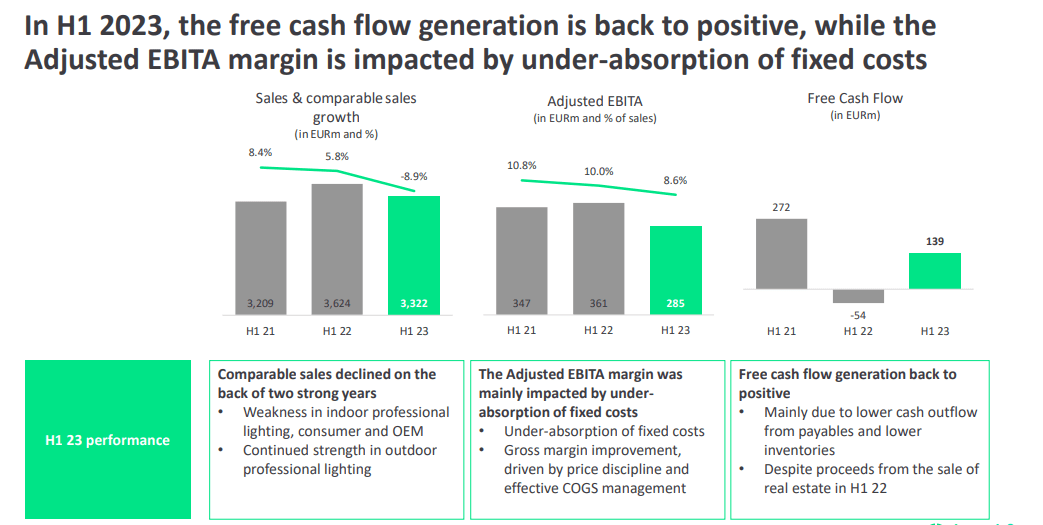

Source: Signify Q2 results presentation

Changes in Estimates

Starting with the CEO's words, he explained how Signify " saw continued softness in the consumer, indoor professional and OEM channels and a slower than anticipated recovery of the Chinese market ." Despite that, the company improved its gross margin; however, Signify operating leverage could be more optimal. In detail, fixed costs do not compensate for the company's ongoing volume decline. Here below our main financial changes:

- Following weaker-than-expected Q2 financial results, we decided to lower our sales forecast by 5% in 2023 and 2024 (from a previous decline of 4.7% and 3%). We are now pricing lower sales than Wall Street average estimates, and our top-line sales are forecasted to be €6.8 billion for the year;

- Following lower volumes, our EBITA should be down. However, we were already pricing a few adverse developments in our initiation of coverage. We are now in line with the company's estimates. Cross-checking analysts, the consensus is pricing in a 10.2% margin. Related to the declining trajectory, the company had negative one-off for a total value of €16 million in Q2 (mainly restructuring costs for €9 million and €3 million of acquisition related-charges);

- Looking at the debt evolution, we slightly increase Signify's financial obligation. Given FCF evolution, we now see year-end debt at €1.1 billion (including financials leasing). We project a €200 million debt reduction target annually until 2027.

{kind=link}

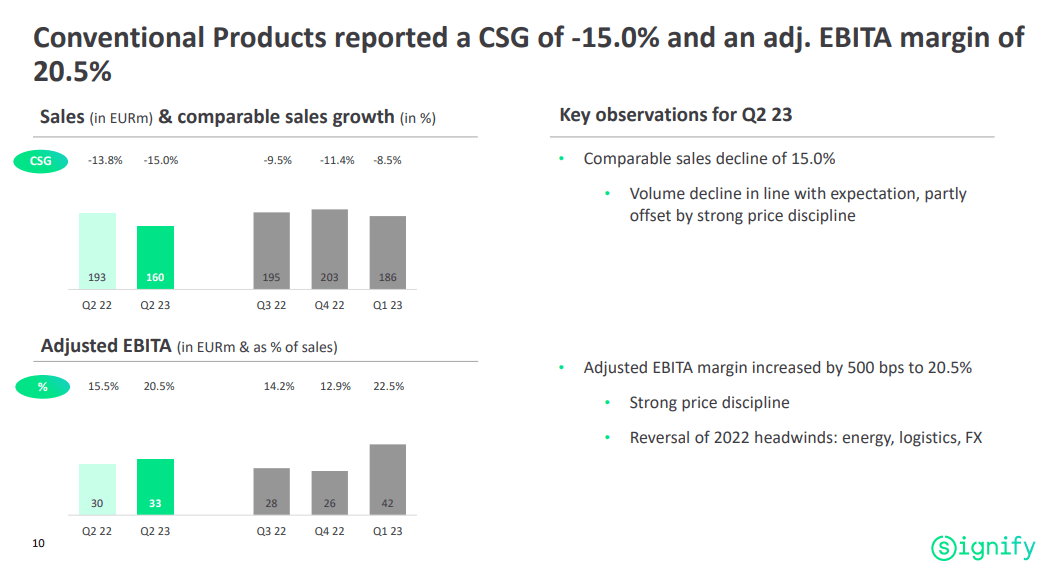

The lighting sector is currently going through a transition to LED-based lighting technologies from traditional lighting systems. This caused the emergence of new competitors and higher investments in the research and development area. This was also recorded in Q2 numbers. In detail, since the transition is not yet completed, this could further decelerate traditional product volume. In addition, higher pricing pressure might cause pressure on profit EBITA margins. This was not recorded in Q2, and despite a volume decline, the company achieved a 20% margin and reversed logistics and FX costs to end clients.

{kind=link}

Conclusion and Valuation

Considering the Q2 results and updating our updated valuation, we decided to lower our target price from €38 to €35 per share, maintaining a buy rating target with a potential upside of 30% from the current stock price value. We know that the combination of Digital Solutions (high multiple) and Conventional Products (low multiple) makes it hard to attract investors; however, this company offers a 5% dividend yield and can deleverage its balance sheet. What is in favor of Signify could be the end of clients' destocking activities, the earnings downgrade removal, and its leading position within the sector. Here at the Lab, we derive our target price on an EBIT forecast of 650 million for 2024 with an unchanged multiple of 8.5x. Considering a higher debt by year-end, we slightly decrease our equity value. In our 2024 estimates, we also derived a 12% FCF yield which is good downside protection even in a soft earnings cycle. On the downside risks, the company is exposed to FX evolution, raw material pricing pressure, and M&A-related risks.

For further details see:

Signify: Weaker-Than-Expected Q2, Still A Buy