SJB - SJB: A Good Tool To Hedge High Yield CEFs

Summary

- ProShares Short High Yield ETF is an inverse fund.

- The vehicle seeks daily investment results that correspond to the inverse (-1x) of the daily performance of the Markit iBoxx Liquid High Yield Index.

- SJB encapsulates both rates and spread components when looking at HY - i.e. it is a hedge for a total return.

- The fund is a great tool to hedge HY risk in an investor's portfolio and can be used on a 2:1 ratio when looking at well managed HY CEFs.

- This article covers CEFs / portfolio construction.

Thesis

Throughout the current market downturn I have been long a couple of high yield CEFs that I consider core positions in my portfolio. Even though I did believe duration assets were going to be hit in 2022, I wanted a core stream of income, and felt 'married' to certain names, even after trimming some of the exposure. Some investors may have tax reasons for not liquidating long held names, but at the end of the day not all retail investors will be comfortable sitting 100% in cash even when a recession is fully on the horizon.

For those investors I am going to discuss today the ProShares Short High Yield ETF ( SJB ), which is a great tool to hedge high yield CEF risk. The fund seeks daily investment results that correspond to the inverse of the daily performance of the Markit iBoxx Liquid High Yield Index . I am going to provide a more detailed look at the index below, however an investor should just frame it as a proxy for unleveraged HY positions.

SJB Hedging Performance

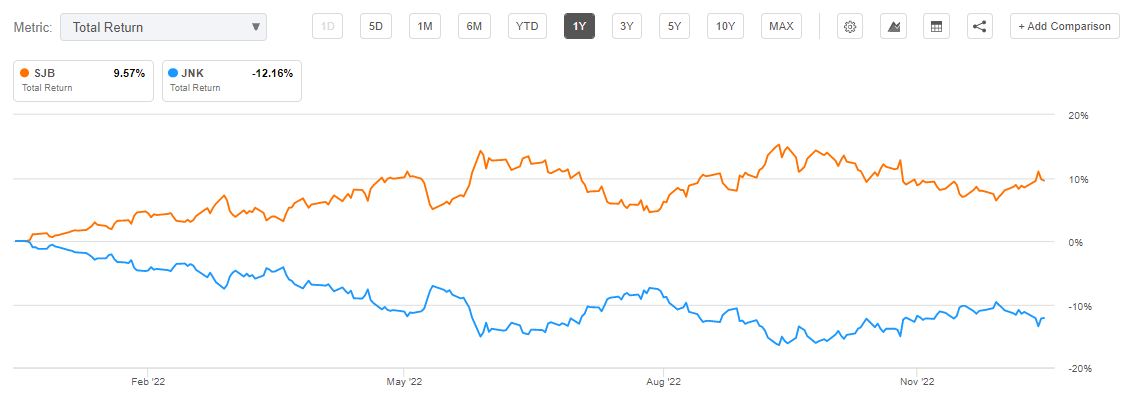

Hedging refers to the ability of an instrument to offset the performance of another one, thus leaving a retail investor with a neutral result. Hedging can be done for a single risk factor such as interest rates, or for the entire total return. Let us look at how SJB did against an unleveraged high yield instrument, namely the very popular SPDR Bloomberg High Yield Bond ETF ( JNK ):

{kind=link}

We can see a nice 'mirroring' performance, where JNK was down -12% last year while SJB was up 9.5%. We have a basis here of around 2.5%, which is fairly small. Kindly keep in mind that inverse instruments are supposed to mirror performance perfectly only on a 1-day basis, but they present differences or 'drift' on longer time-frames.

JNK is unleveraged, so the relationship is fairly close to a 1:1 performance. That means that a retail investor long JNK at the beginning of the year and unwilling to divest the respective position, could have just bought SJB and achieved a fairly flat result in 2022. Please keep in mind the above chart is on a total return basis, thus it includes dividends.

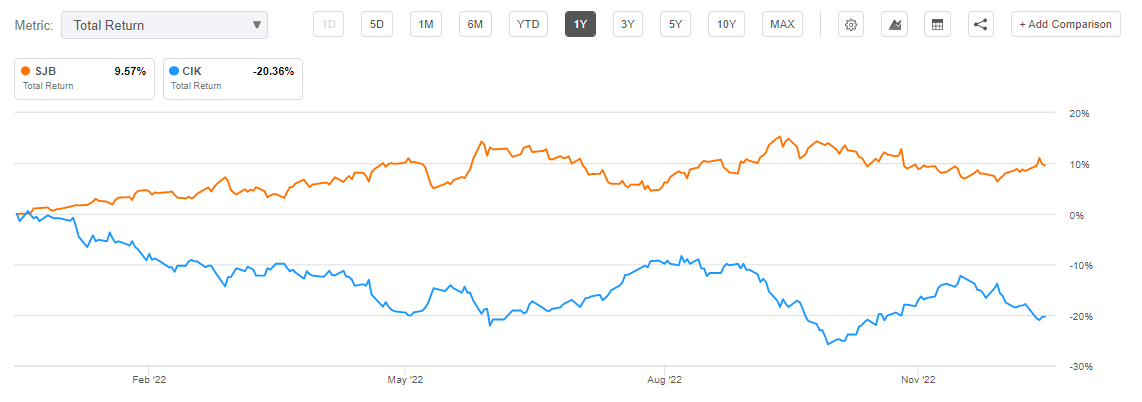

Let us have a look at how SJB does against a HY CEF, namely ( CIK ):

{kind=link}

We can see CIK is down around -20% in 2022 while SJB is up 9.5%. We expect CIK to be down more than JNK because it is leveraged. Most of the well run HY CEFs were down around -20% in 2022, hence CIK is a good proxy to use. SJB offers only -1x returns, hence when looking at hedging a HY CEF a retail investor must use a 2:1 build - i.e. 2x the SJB notional for the CEF hedged. That would translate into $200 notional for SJB to hedge $100 notional of CIK.

Keep in mind that SJB encapsulates both rates and spread components - i.e. it is a hedge for a total return. Some instruments hedge just interest risk for example. In the above example CIK's performance in 2022 was driven by higher interest rates and wider credit spreads. A 2:1 hedging build via SJB would have hedged out both of those components.

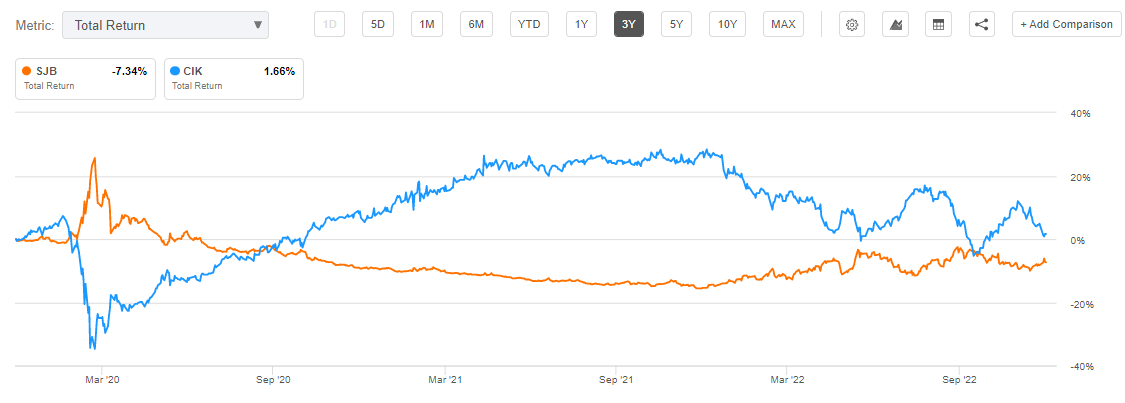

On a longer time-frame the relationship breaks down:

{kind=link}

Inverse instruments do not work well on longer time-frames (i.e. more than one year usually). It is the case here as well. Do not use SJB as a long term buy-and-hold hedge. Use it for shorter, discrete time frames.

Index Description

Let us have a closer look at the Index which is utilized by SJB in terms of providing a -1x performance:

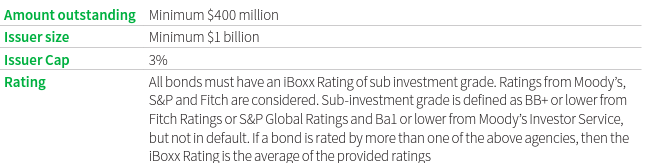

The Markit iBoxx® $ Liquid High Yield Index is a market-value weighted index designed to provide a balanced representation of U.S. dollar-denominated high yield corporate bonds for sale within the U.S. by means of including the most liquid high yield corporate bonds available as determined by the index provider. Currently, the bonds eligible for inclusion in the index include U.S. dollar-denominated corporate bonds for sale in the U.S. that are issued by companies domiciled in developed countries are rated sub-investment grade by Moody's Investors Service, Fitch or S&P; are from issuers with at least $1 billion par outstanding; have at least $400 million of outstanding face value; and have at issuance an expected remaining life of 15 years or less. There is no limit to the number of issues in the index. Index rebalances occur monthly.

The index is a reflection of the U.S. high yield market, being overweight BB names:

Index Ratings (Index Fact Sheet)

Through its build, the index ensures it captures only liquid names from large issuances:

{kind=link}

Conclusion

SJB is an ETF that seeks daily investment results that correspond to the inverse of the daily performance of the Markit iBoxx Liquid High Yield Index . An investor can think of the index as an unleveraged proxy of the U.S. HY universe. SJB hedges the total return of the index, meaning it covers both rates and spread risk factors. On a 1-year basis SJB provides a positive mirroring result for JNK, one of the largest well-known junk ETFs. High Yield CEFs are leveraged instruments, hence the optimal hedge ratio is 2:1 when using SJB. Back testing SJB versus CIK in 2022 utilizing a 2:1 ratio (i.e. for each $100 of CIK notional and investor would need to purchase $200 of SJB) yields an almost flat result for the year. Most of the well run HY CEF cohort exhibited a similar result as CIK in 2022. A retail investor who holds a long position in a HY CEF and does not want to liquidate (for tax reasons or purely to have a steady stream of income) can use SJB to hedge negative market moves in the HY space. As an inverse instrument, SJB does not work correctly for long periods of time - plan on using it maximum for one year time-frames.

For further details see:

SJB: A Good Tool To Hedge High Yield CEFs