UDMY - Skillsoft Corp. Is Showing Some Hard Warning Signs

2023-11-20 09:43:46 ET

Summary

- Skillsoft Corporation warrants a sell rating due to poor revenue growth, persistent debt, and lack of profitability.

- Skillsoft faces strong competition from other online learning providers who offer similar products at lower prices.

- Skillsoft's share price has declined considerably and the company is not expected to achieve profitability in the near future.

Investment Thesis

Skillsoft Corp. ( SKIL ) warrants a Sell rating, in my view, due to poor revenue growth, persistent debt, and lack of profitability. Additionally, while high demand for online learning is expected to continue, Skillsoft is at risk of being overcome by other competitors due to its high relative prices. While its share price presents a tempting value buy, multiple fundamental issues should serve as a warning sign to investors.

Company Overview and Primary Competitors

Skillsoft provides online content and services to teach leadership and business skills. The com pany’s 12,000 courses include programming, leadership, risk compliance, and many more. Skillsoft has a long track record of quality online education, having served 86 million customers in over 150 countries.

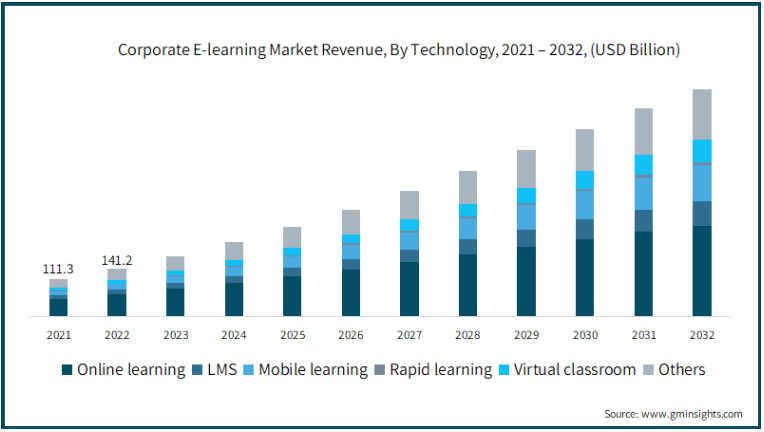

Skillsoft obtains revenues through predominantly content subscriptions (65.8% of revenue in 2022) but also from virtual on-demand content and coaching (34.2% of revenue in 2022). The corporate e-learning market is expected to grow to $665B in 2032, up from $141B in 2022, a CAGR of 15.5%.

{kind=link}

To fulfill this increasing demand, there are numerous competitors in the corporate online learning market space. Competitors of Skillsoft include Microsoft’s LinkedIn Learning, BetterUp Inc. (private company), Udemy, Inc. ( UDMY ), Coursera ( COUR ), NAVEX Global (private company). Due to their similar business models and size, UDMY, COUR, and Chegg, Inc. ( CHGG ) are used in this article for comparison with Skillsoft.

Stagnant Growth and Persistent Debt

The first fundamental red flag for Skillsoft justifying a sell rating is its lack of revenue growth. While SKIL has been able to maintain stable revenue since late 2021 at approximately $140M per quarter, it has been unable to achieve significant growth. Furthermore, its total assets have gone down notably this year, while its debt remains relatively constant.

Skillsoft Revenues, Assets, and Debt in Previous Quarters

| Q3 2022 |

| Q4 2022 |

| Q1 2023 |

| Q2 2023 |

| Q3 2023 |

| Revenues |

| $140.6M |

| $139.4M |

| $140.3M |

| $135.6M |

| $141.2M |

| Total Assets |

| $236.6M |

| $322.5M |

| $405.7M |

| $345.1M |

| $312.4M |

| Net Property, Plant & Equipment |

| $28.9M |

| $24.7M |

| $24.8M |

| $17.1M |

| $16.5M |

| Long-Term Debt |

| $599.0M |

| $582.9M |

| $583.4M |

| $580.7M |

| $579.6M |

Source: SEC.gov filings

In 2022, Skillsoft acquired Codecademy , expanding its ability to present online learning for certain technical skills. The acquisition was expected to immediately grow Skillsoft’s revenue growth and gross margin. Unfortunately, the company has not seen any significant growth and has been unable to achieve profitability since the acquisition.

On a macro level since the COVID pandemic, businesses have increased in-person work for employees and reduced teleworking. While other e-learning peers have also dealt with this trend, competitors have still been able to achieve growth. Additionally, top peer competitors, Udemy and Coursera, have been able to maintain relatively low levels of debt.

Skillsoft and Primary Competitors Revenue Growth and Debt

| SKIL |

| UDMY |

| COUR |

| Sector Median |

| Revenue Growth (YoY) |

| 5.18% |

| 17.61% |

| 22.6% |

| 8.48% |

| Total Debt |

| $64.37M |

| $8.63M |

| $8.47M |

| N/A |

| Net Debt |

| $492.45M |

| -$470.81M |

| -$712.86M |

| N/A |

Source: Seeking Alpha, 17 Nov 23

Looking forward, SKIL is expected to see YoY revenue growth of just 5.25%, compared to 17% and 21% for Udemy and Coursera respectively. Skillsoft, similar to Udemy and Coursera, does not offer a dividend. Low revenue growth and lingering debt represent the first concern for investment in Skillsoft.

Lack of Profitability

The second strong red flag for Skillsoft is its lack of profitability. SKIL has had only one profitable quarter in recent years ($41.7M in Q1 ‘21). All quarters since then have not been profitable. In contrast, other top competitors UDMY and COUR have been able to achieve more favorable net income margins and returns on equity. Chegg, which focuses more on academic e-learning versus business, has been able to achieve profitability over the past year.

Skillsoft and Primary Competitors Profitability Metrics

| SKIL |

| UDMY |

| COUR |

| CHGG |

| Net Income ((TTM)) |

| -$658.0M |

| -$139.2M |

| -$147.9M |

| $10.37M |

| Net Income Margin ((TTM)) |

| -118.26% |

| -19.75% |

| -24.29% |

| 1.41% |

| Return on Common Equity ((TTM)) |

| -99.28% |

| -39.64% |

| -22.37% |

| 1.00% |

| Cash From Operations ((TTM)) |

| -$5.95M |

| -$24.12M |

| -$15.50M |

| -$1.75M |

Source: Seeking Alpha, 17 Nov 23

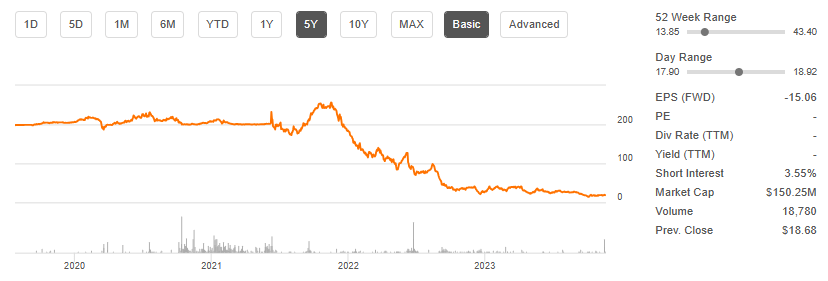

A key factor for SKIL’s inability to produce positive net income lies in its operating expenses. In its latest 10-Q, SKIL had a quarterly operating expense of $126M and produced a revenue of $141M. In comparison, Coursera, had lower operating expenses ($122.9M) with greater revenue ($165.5M) last quarter. As a result of Skillsoft’s inability to produce positive net income, its share price has suffered. SKIL is down over 90% from its high of $255.40 in fall 2021. While rebounding from an all-time low of $13.85, SKIL has been a clear underperformer in its sector.

{kind=link}

Encroaching Competition

The third red flag for Skillsoft is its increasingly strong competition. In Skillsoft’s own annual report, it states that it expects the market to remain “ competitive in the future due to its highly attractive qualities.” Two key competitive advantages of Skillsoft are its over 20 years of experience providing education and its product quality. Skillsoft has received numerous awards for quality content including two Training Magazine Network Choice Awards . However, other competitors have been providing courses at lower prices.

Microsoft’s LinkedIn is reported to sell individual courses for $20 to $50 and provides an annual subscription of $26.99 per month. Udemy courses cost anywhere from $12.99 to $199.99 depending on the topic. Coursera courses range from $29 to $99. While Skillsoft does not publicly advertise the cost of their courses, it has been noted that their plans start from $1,500 per license.

Skillsoft and Primary Competitor Price Ranges

| Skillsoft |

| Coursera |

| |

| Udemy |

| Price Range |

| $29-99/course ; or $59/month |

| $20-$50/course ; or $26.99/month |

Source: Derived from multiple sources, 17 Nov 23

Of note, while Skillsoft has been providing courses for over 20 years, there are new e-learning companies entering the market frequently at lower prices. Although Skillsoft has a long reputation of providing quality courses, smaller more agile companies are undercutting Skillsoft’s prices. To add to the gloomy outlook for Skillsoft, it is investing a comparatively low amount into research and development than its competitors. Last quarter, Skillsoft allocated $17.8M to courseware development, compared to $37.6M for Coursera and $30.3M for Udemy.

Valuation

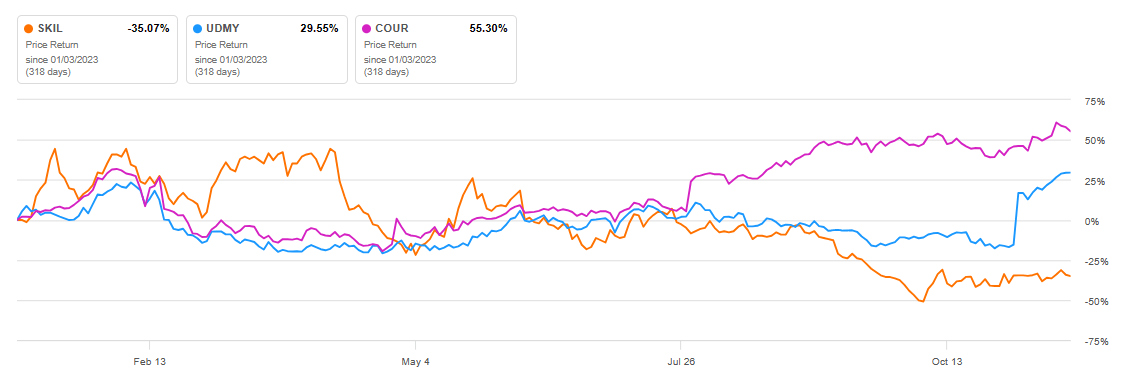

Due to the relatively low revenue growth, negative net income, and persistent debt, Skillsoft’s share price has declined considerably. YTD, Skillsoft is down 35%, compared to positive returns for Coursera and Udemy. However, SKIL is currently 33% higher than its 52-week low of $13.85.

{kind=link}

Multiple firms give SKIL an average price target of $60.75 . This is immensely optimistic given the company’s shaky fundamentals. With a current price of $18.44 at the time of writing this article, the average price target represents a return of over 300%. Those advocating for SKIL as a buy will likely point to its EV/Sales of 1.16, an EV/EBITDA of 10.97, or a Price/Book of 0.32.

SKIL Price Return (Seeking Alpha)

However, Skillsoft’s estimated Forward EPS is -$15.06 and the company is not expected to achieve profitability within the next year. In comparison to competitors, Skillsoft is at risk of experiencing reduced market share with no tangible path towards improvement. Therefore, Skillsoft warrants a sell rating and will underperform both its competitors and the market over the next year.

Risks to Investors

Skillsoft will likely be able to maintain consistent revenues due to its subscriptions. The company has a long record of high-quality education and has been awarded for superior products. However, there is no indication that the company can achieve profitability soon. Skillsoft conducted a 1-for-20 reverse stock split in late September 2023 in an attempt to increase share price. However, this effort has ultimately been unsuccessful. Since late September, SKIL’s share price has remained stagnant.

Skillsoft has held a 24-month beta value of 1.58 and is therefore volatile compared to the market overall. If Skillsoft can turn a positive net profit, it could present a solid value buy given its low price. However, Skillsoft has the highest total debt with lowest revenue growth, compared to its competitors. The company presents low momentum compared to its peers and therefore is at risk of losing market share.

Concluding Summary

While other competitors have had similar struggles achieving profitability, Skillsoft stands out as an underperformer. The lack of revenue growth and persistent debt indicate fundamental issues plaguing the company. Peer competitors offer similar online learning products at lower prices. Given Skillsoft’s challenges, it seems unlikely that the company can turn things around to achieve solid profitability. Furthermore, Skillsoft has comparatively low investment into future course development. Therefore, while SKIL may be tempting as a value buy, it warrants a sell rating.

For further details see:

Skillsoft Corp. Is Showing Some Hard Warning Signs