SRRTF - Slate Grocery REIT: A 7.8% Yield And Temporary Relief From Increasing Interest Rates

Summary

- Slate Grocery REIT's recent acquisition is paying off as the AFFO/share increased, resulting in a lower payout ratio.

- The existing interest rate hedges are paying off handsomely, but the underlying rates are increasing fast.

- Slate should be able to hike rent before getting hit with the sharp interest rate increases.

- The book value appears very reasonable as the REIT used a capitalization rate of 6.76%.

Introduction

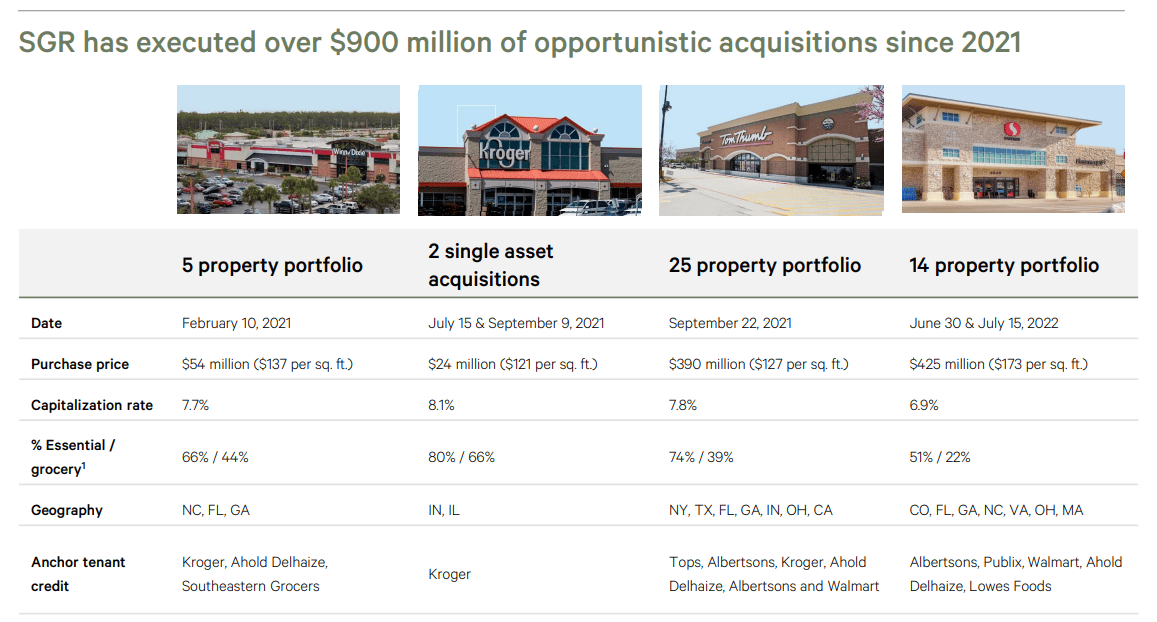

Slate Grocery REIT ( SRRTF ) (SGR.UN:CA) (SGR.U:CA) completed the US$425M acquisition of grocery-anchored commercial real estate in the USA in July, so I was really looking forward to seeing how this REIT performed during the third quarter of this year.

{kind=link}

While I originally wasn't expecting much and I am more interested in seeing how the REIT expects to navigate through this high interest rate climate and how this may impact its 2023 results, it is interesting to check up on Slate Grocery REIT anyway.

The Q3 results

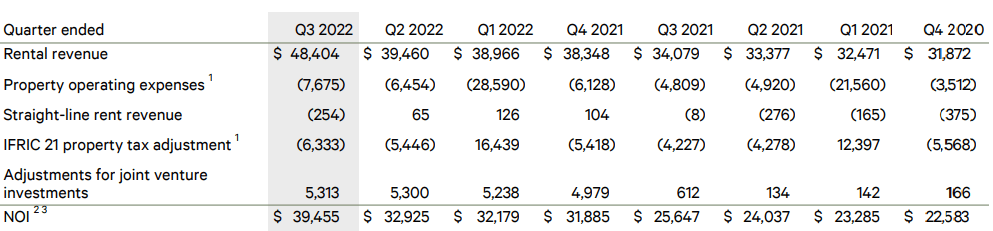

The acquisition immediately resulted in a substantial increase in the net operating income as reported by Slate Grocery. As you can see below, the NOI was coming in at around US$32M per quarter for the three quarters before the acquisition, and this suddenly jumped to $39.5M in the third quarter of this year.

{kind=link}

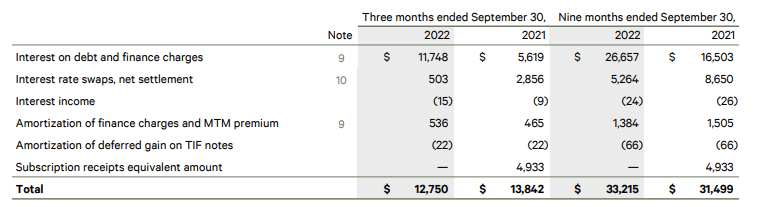

The image above shows the immediate impact of the acquisitions. But as you can imagine, the interest expenses increased as well. While Slate only paid about US$15M in interest expenses in the entire first semester, this jumped to almost $12M in the third quarter of this year alone. And as interest rates continue to increase, I expect Slate's interest bill to increase further beyond the $11.75M incurred in the third quarter.

{kind=link}

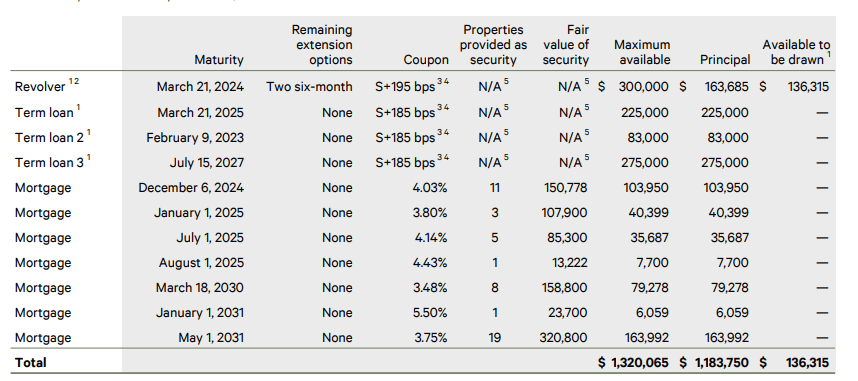

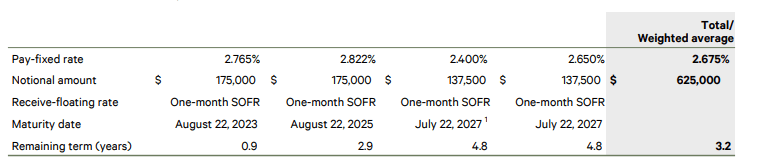

Fortunately a substantial portion of the debt consists of mortgages with a fixed interest rate. While the term loans and revolver have a floating interest rate, about $437M of the debt has a fixed rate . And as the short-term interest rates are high, I wouldn't be surprised if Slate would opt to add more secured debt to its financing mix as that should be cheaper than the unsecured term loans and revolvers.

{kind=link}

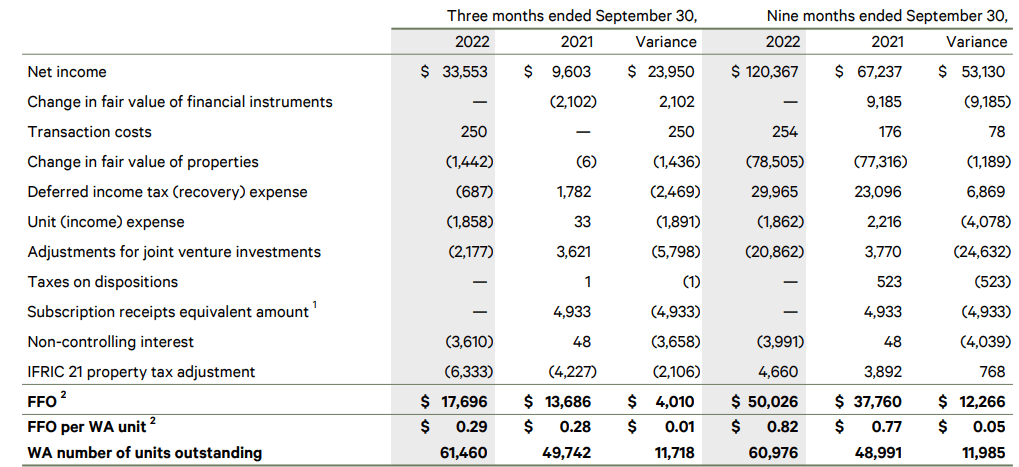

During the third quarter, the FFO increased to $17.7M which represented approximately $0.29 per share, as you can see below.

{kind=link}

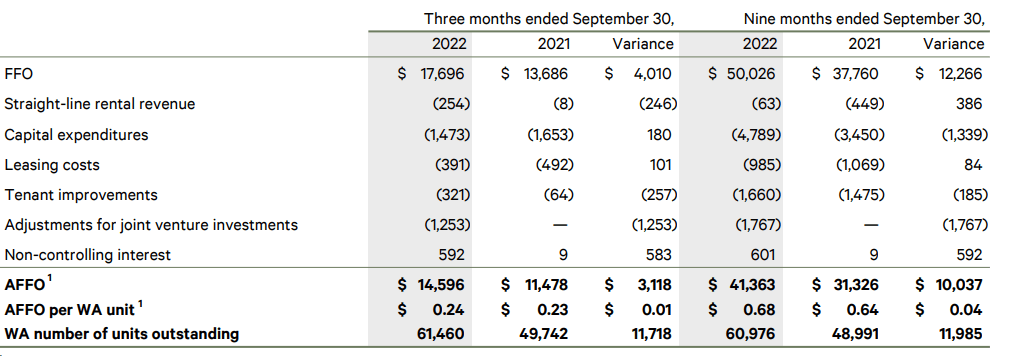

Even more important than the FFO is the AFFO calculation as it includes maintenance capital expenditures. That AFFO was lower than the FFO (as expected, of course), as it came in at $14.6M for an AFFO of $0.24 per unit.

{kind=link}

This means that despite the increase in interest expenses, the AFFO per share increased compared to the $0.22 per share on a quarterly basis in the first two quarters of this year.

The increased AFFO also helps to bring the payout ratio below 100% again. Slate Grocery REIT currently pays a monthly distribution of US$0.072 per share , or $0.216 per quarter. The image below shows the REIT generated $1.36M in additional AFFO after covering the distributions. The payout ratio dropped to just below 91% (versus 98% in the second quarter of the year).

{kind=link}

As of the end of September, the LTV ratio (calculated as the net financial debt versus the book value of the assets) was 51% (including the book value of the joint venture investments). This is quite reasonable but it is important to figure out if the $2.13B book value of the properties (excluding the JV investments) is actually realistic.

{kind=link}

According to the footnote to the financial statements, the weighted average capitalization rate was 6.76% which I think is very fair for an empire with predominantly grocery-anchored commercial real estate. And even if we would use a 7.26% capitalization rate, the fair value of the assets would decrease by just under $185M. The LTV ratio would increase to 56% which is relatively high but still within limits.

{kind=link}

According to the official book value of the assets, the equity value attributable to the Slate Grocery REIT unitholders was $741M, which represents approximately US$12 per unit. Even if I would use the $184M valuation decrease by increasing the cap rate, the net book value per share would likely still come in at around US$10/share as a portion of the valuation decrease will be attributable to the non-controlling interests.

And considering new lease agreements were priced above older deals, it looks like we shouldn't be too worried about the valuation of the assets. From the Q3 conference call (the emphasis is mine):

In the current interest rate and inflationary environment, which we know can contribute to cap rate expansion, our growth in revenue can more than offset any negative impact on our valuations. Our team's operational performance this quarter speaks to the growth embedded in our portfolio. Our asset management team has completed over 520,000 square feet of leasing in the third quarter. New deals were completed at 9.5% above in-place for rent and renewals over 4% of expiring rent .

Investment thesis

I have been following Slate Grocery REIT for years but this is the first time I am warming up to initiating a long position. The most recent (debt-funded) acquisition boosted the AFFO per share despite incurring higher interest expenses and the payout ratio has fallen to just over 90%. While the absolute amount of retained cash is pretty low (US$5M per year, which would reduce the LTV ratio by just 20-25 basis points per year), let's not forget Slate should be able to hike rents and this should at least help to cover the higher interest expenses and keep the payout ratio below 100%.

{kind=link}

The higher interest rates will for sure be felt in the next few quarters although the REIT also has some hedges in place which will mitigate the impact of an aggressive interest rate increase (the hedges basically allowed Slate to lock in a fixed interest rate for almost 90% of its debt). This will buy Slate some time to effectively hike rents before it will be fully hit with the higher market rates (on the conference call, Slate's management mentions it sees current market rates in the 'high 5s' ).

Subsequent to the end of Q3, Slate also completed asset disposals for a total of $19M . This should only have a minimal impact on the NOI and AFFO but could push the LTV ratio below 50%. We will know more when Slate publishes its annual report.

For further details see:

Slate Grocery REIT: A 7.8% Yield And Temporary Relief From Increasing Interest Rates