CRARF - Societe Generale: 2026 RoTE Target Shows Structurally Lower Profitability Still Attractive Risk-Reward Opportunity

2023-09-19 03:31:45 ET

Summary

- Societe Generale unveils a 9-10% RoTE target for 2026 at its Investor Day, some 2.5% lower than peers.

- The new 40-50% payout ratio is set to be based on reported rather than underlying numbers from 2023, potentially lowering payouts.

- Basel IV impact of 0.85% on CET1 ratio, with a trough expected in Q1 2025.

- Boursorama and ALD only businesses to grow risk-weighted assets organically.

- 40% upside to my fair value estimate of 34 EUR/share based on current trading of peers and profitability targets.

Introduction

Societe Generale ( OTCPK:SCGLF ) held its Investor Day on September 18. The presentation is available here while the press release can be found at this link . For reference, you can also access the company's H1 2023 results presentation here . I also covered SocGen back in February most recently here . In this article, I will share my highlights from the Investor Day and compare how Societe Generale stacks against French peers at the end.

Financial Targets

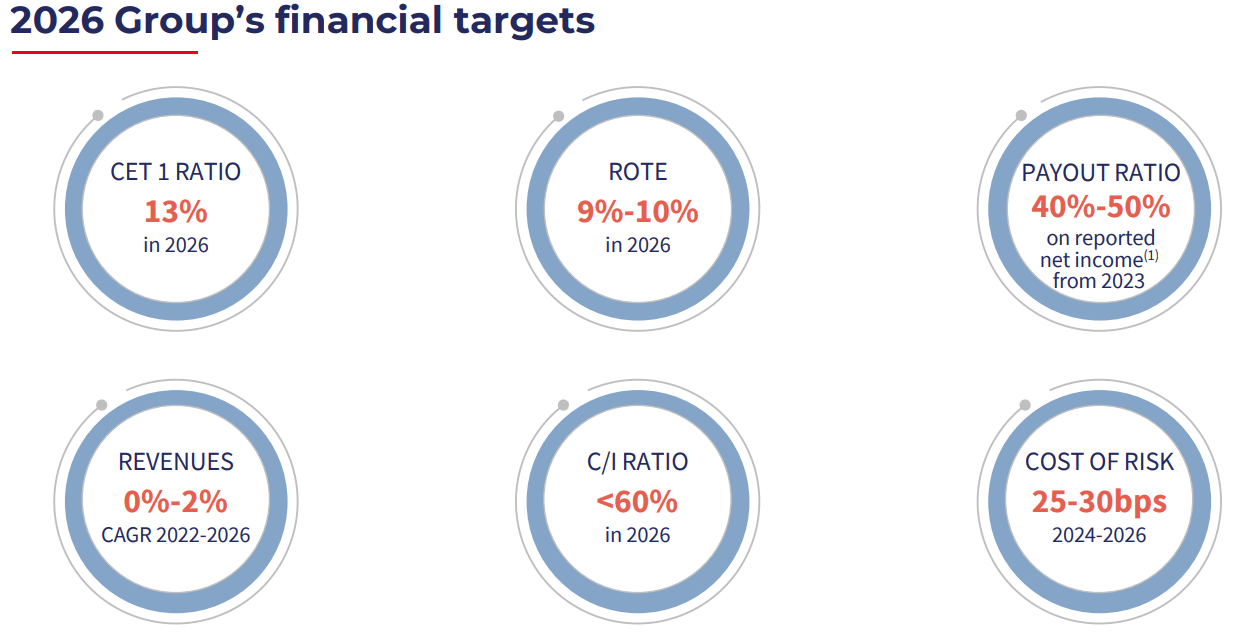

The Investor Day covered the period 2023-2026, with the 2022 results serving as a starting point. As a result, the French lender communicated new 2026 financial targets:

- A CET1 ratio of 13%, under Basel IV (set to be introduced in 2025);

- Average annual revenue growth of between 0% and 2% over 2022-2026

- Cost-to-income ratio below 60% in 2026;

- RoTE of 9-10% in 2026

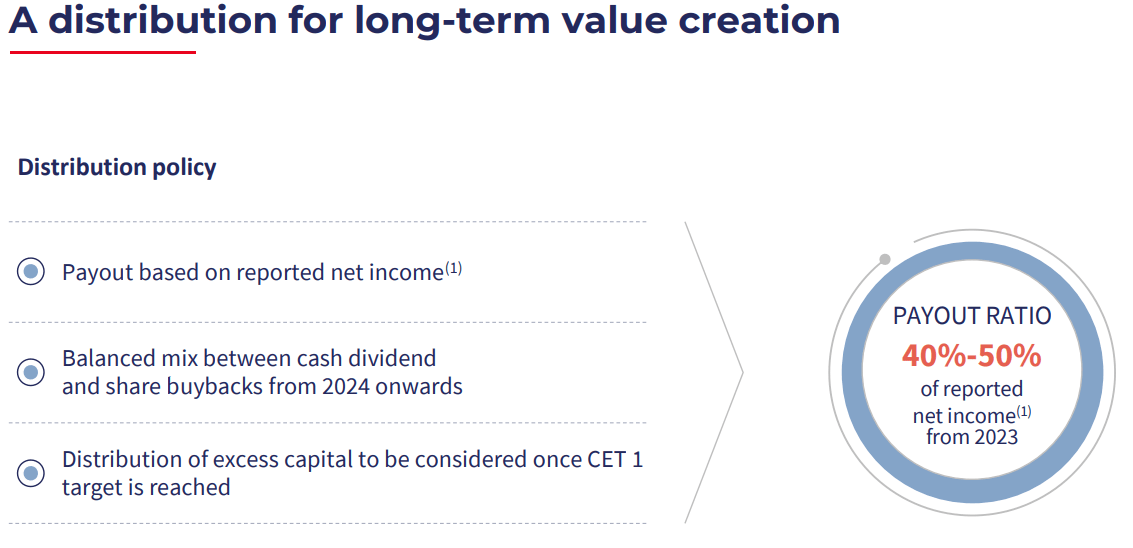

- Payout ratio of 40-50% of reported net income, starting in 2023

- Cost of risk 25-30 basis points 2024-2026

{kind=link}

2023 Investor Day Presentation

My first biggest takeaway is that SocGen did not raise its profitability target . Instead, the midpoint 9.5% RoTE is actually marginally below the previous 2025 target of 10% and below the 12% generally targeted by large French peers such as BNP Paribas ( OTCQX:BNPQF ) and Credit Agricole ( OTCPK:CRARF ). Nevertheless, it is largely in line with the 9.1% underlying RoTE achieved in H1 2023. So while the new target can be seen as disappointing, it is also realistic and reachable at the same time.

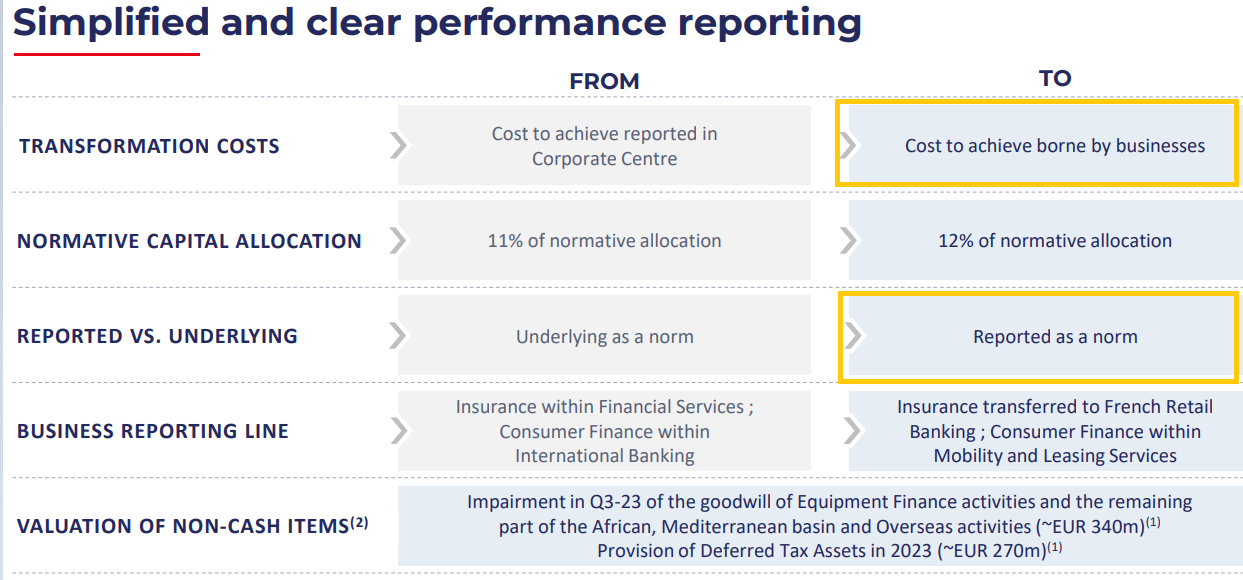

The other key takeaway is the lower payout ratio of 40-50% on reported net income from 2023. Previously, SocGen targeted a 50% payout on underlying net income (which largely ignores restructuring costs and other select items). This is part of a larger shift at the French lender, with more prominence given to reported numbers and not allocating restructuring costs in the Corporate Center for example:

{kind=link}

2023 Investor Day Presentation

As a result, it is fair to expect that cumulative shareholder payouts in respect of 2023 will decrease relative to 2022, given the tendency of reported numbers to be lower than underlying results:

{kind=link}

2023 Investor Day Presentation

As per the press release, the 2026 Cost/Income (C/I) ratio of below 60% will be the result of:

- 6% reduction from cost savings

- 3% reduction from the end of the Single Resolution Fund payments

- 2.25% on lower restructuring charges

- 4.75% higher on inflationary impacts

In Q2 2023, the Cost/Income ratio stood at 65.8%.

Capital Position

Societe Generale maintained a CET1 ratio of 13.1% in H1 2023, a 3.4% buffer against its 9.73% requirement. The bank expects a 0.85% negative impact from the introduction of Basel IV in 2025. As a result, the CET1 ratio is expected to trough in Q1 2025 before recovering later in the year and into 2026:

{kind=link}

2023 Investor Day Presentation

For the remainder of 2023, the bank is set to absorb a further 0.5% regulatory headwind to CET1 capital.

Division highlights

Despite some movement of businesses across divisions, Societe Generale is set to continue to report operations in three key segments:

French retail banking (28.4% of H1 2023 net banking income)

The French retail banking division targets a Cost/Income ratio of below 60% in 2026, with improvements driven by the French networks merger and profitability at online bank Boursorama . Boursorama, along with vehicle lessor ALD are the only two areas where organic capital will be allocated.

Global Banking and Investor Solutions (37.9% of H1 2023 net banking income)

The division is targeted to deliver a Cost/Income ratio of below 65% in 2026, the weakest result in the group. The focus is set to be on maintaining current operating performance, with lower risk-weighted asset use and higher advisory/fee business .

International Retail, Mobility & Leasing Services (33.7% of H1 2023 net banking income)

The division is set to remain the most profitable in Societe Generale's portfolio, with a Cost/Income ratio target of below 55% in 2026. The improvement will come from the full impact of LeasePlan-ALD synergies (which were pushed back one year due to the late closing of the deal), as well as continued contributions from the bank's Czech Republic / Komercni Banka/, Romania /BRD/ and Africa operations.

Societe Generale relative to French peers

Before we consider Societe Generale's valuation, the comparison with BNP Paribas and Credit Agricole does not generally stand in SocGen's favor:

| Bank\Financial Metric |

| RoTE |

| C/I |

| CET1 H1 2023 |

| BNP Paribas |

| 12% in 2025 |

| 60% in 2025 |

| 13.6% |

| Credit Agricole |

| 12% in 2025 |

| 58% in 2025 |

| 11.6% |

| Societe Generale |

| 9.5% in 2026 |

| 60% in 2026 |

| 13.1% |

Source: Company disclosures

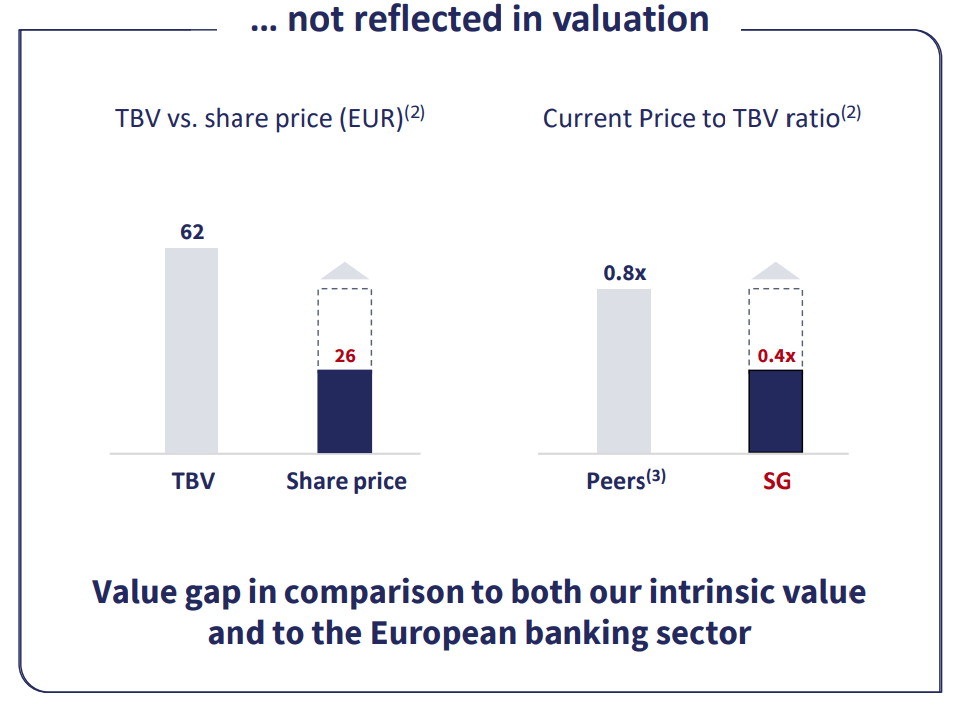

We see that SocGen targets a RoTE profitability some 2.5% lower than its closest peers, despite similar C/I ratios. As a result, Societe Generale is likely to retain a structurally lower valuation than its closest peers, as is currently the case:

| Bank |

| Price relative to tangible book |

| BNP Paribas |

| 0.72 |

| Credit Agricole |

| 0.78 |

| Societe Generale |

| 0.39 |

Source: Author calculations

Nevertheless, the current discount appears too large, with a more realistic target being 0.55 of tangible book value, or a price of 34 EUR/share. This represents an upside potential of 40% should the profitability target be reached.

Conclusion

Societe Generale's new profitability target disappointed markets, with the stock falling on the news. Nevertheless, I reckon the shares represent an attractive risk-reward opportunity relative to peers and rank them a buy. Time will tell whether the new management team manages to address the value gap.

{kind=link}

2023 Investor Day Presentation

{kind=link}

2023 Investor Day Presentation

Thank you for reading.

For further details see:

Societe Generale: 2026 RoTE Target Shows Structurally Lower Profitability, Still Attractive Risk-Reward Opportunity