SCGLF - Societe Generale: A Longer Than Expected Re-Rating Journey

2023-10-05 02:54:15 ET

Summary

- Société Générale investors were not pleased with the company's growth targets.

- Here at the Lab, we positively view the new CEO's intention to reset expectations, but we believe the company's objectives are too conservative, given Boursorama's trajectory and current rates.

- Valuation is very much discounted. Our buy is then confirmed.

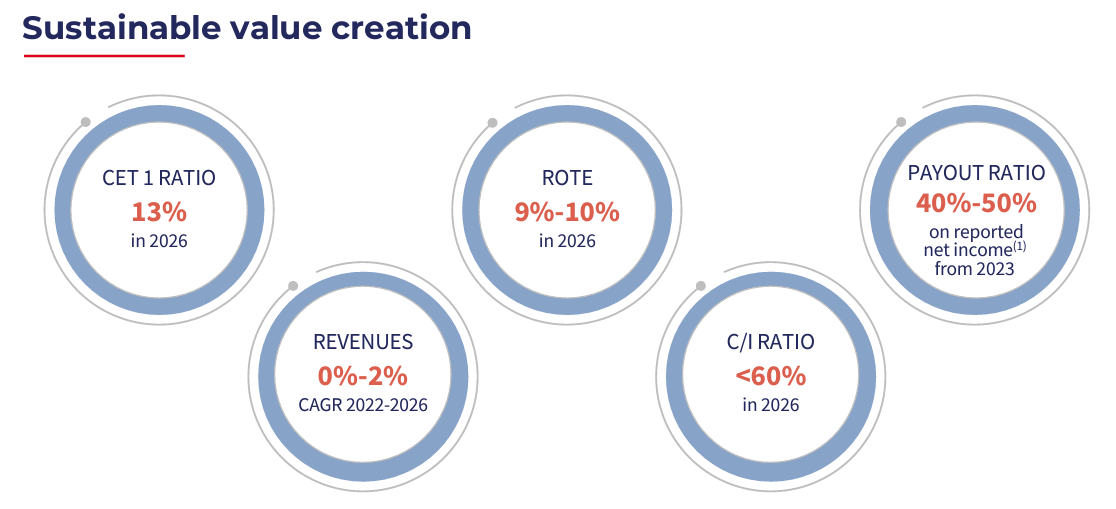

Here at the Lab, we took some time to analyze Société Générale S.A. ([[SCGLY]], [[SCGLF]]) latest CMD strategic plan . In our last publication called ' Asset Quality And More Upside ,' we anticipated better estimates on the company's capital market day, which did not materialize. What we expected to be a positive catalyst has transformed into a negative day for SocGen investors. Wall Street was disappointed by the new targets, such as the RoTE at 9-10% and sales trend between 0-2%, implying no growth in the bank's portfolio.

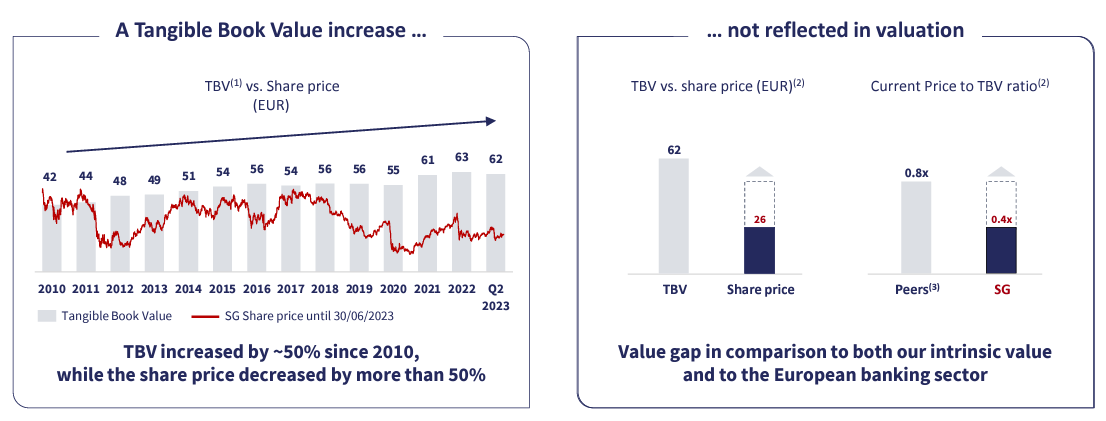

In a nutshell, we positively view the new CEO's intention to reset expectations, and we believe that SocGen's top-line sales, cost/income ratio evolution, RWA, and capital guidance leave the company a clear potential upside to be capitalized over the medium-long term horizon. Therefore, we reaffirmed our target price of €32 per share today, supported by a valuation gap vs. SocGen's tangible book value, which is not well priced in the company's valuation.

{kind=link}

Source: Société Générale CMD presentation

Here are our main key takeaways and forward-thinking assumptions:

- Our internal team finds it hard to believe SocGen's revenue CARG is below 2% over the next visible period (until 2026). Related to the top-line sales, we pencil in a 2.5% revenue growth CAGR over the period thanks to a CIB revenue normalization and lower growth in international retail and ALD; however, with interest rates higher for longer , we believe the bank will fully benefit from net interest margin evolution. In addition, as already mentioned, we believe in Boursorama's positive trajectory. The company leads online French banking and reached five million users in Q2 with positive net profit results (€47 million). Here at the Lab, we welcome a more prudent approach by the new CEO; however, we believe bank estimates are too cautious and conservative;

- Going down to the P&L analysis, we are more satisfied with the expected cost cut of approximately €1.7 billion over the next three years. SocGen aims to deliver a cost/income ratio below 60% at the end of the plan. Given higher inflation over the project, our internal team is optimistic about this development, and we forecast a flattish cost from 2022 to 2026; however, higher revenue will lead to a C/I ratio in line with the company's internal estimates. There might be a positive upside given the merger between LeasePlan and ALD;

-

The new CEO reported concerns about shareholders' remuneration. Raising the CET 1 ratio and cutting the payout is not the right approach, given the other banks' yield (considering both dividend and buyback). SocGen had probably hoped to announce a few disposals before the CMD. Exiting the Africa division and Securities Services and Equipment Finance could increase the CET 1 ratio by approximately 100 basis points and reassure the market. We anticipate a faster capital build given the solid company's numbers, and we already forecast a higher payout ratio of more than 50% in 2024 onwards, considering the buyback;

- The risk-weighted assets growth was lower than anticipated, with a target of €420 billion by 2026 and an average annual growth rate limited to 1%. Related to RWA, we believe SocGen is already incorporating some disposals between €7-19 billion. This scenario could support a higher shareholders' remuneration, as mentioned in point 3.

{kind=link}

Conclusion and Valuation

SocGen can easily beat all the above targets. We were not much above the company's new estimates; our previous 2024 RoTE target was set at 8.7%. Compared to Wall Street analyst expectations, our target price was already set at a comfortable area over the 12m estimates horizon, given the higher provision expected on a potential recessionary slowdown in the EU area. Despite that, the Bank trades at a 2024 4.8x P/E with a Price on the tangible book value of 0.38x (and a RoTE of 8%). We believe this is not justified. Given the ongoing disposal, we add risk to SocGen's payout flexibility. But considering the company's internal forecast, we believe a worst-case scenario is well-priced in. Valuing the company with a 2024 P/TAV of 0.5x and a 5.5x P/E, we confirmed our target price set at €32 per share . SocGen valuation discounts material earnings downgrade, which we are not anticipating. We see disposals as positive catalysts for the stock and continue to rate the bank with a Buy. Lastly, on reverse engineering, the company's stock price is valued with a cost of equity at almost 20% (a value in line with a bankruptcy procedure). SocGen is a business that, in H1, achieved nearly €2 billion in profits.

For further details see:

Societe Generale: A Longer Than Expected Re-Rating Journey