GNENY - Sodium Instead Of Lithium: Important News For All Lithium Investors

2023-04-25 05:48:27 ET

Summary

- The current projections are that by 2030 95% of all lithium will be used for batteries, mainly in EVs.

- The Chinese EV manufacturer Chery is the first which will use sodium batteries. This company has about 4% market share in China and builds very affordable EVs.

- The energy density of Sodium-ion batteries is about 30% less than lithium, but in some areas, this does not matter.

- If sodium could capture only 5% of the electric car market, this would already be a lot and relatively unexpected.

Introduction

This is a follow-up article to my first article , published on December 11, 2022, about the possible competition for lithium batteries. It makes sense to read this one first for those who haven't already, as I don't want to repeat too much. The article mentioned concerns the advantages and disadvantages of lithium and sodium, respectively.

This article is about the Chinese market, the geopolitical environment, and the first manufacturer to use sodium-ion batteries.

LCE demand - a brief summary

Surely most readers already know that the estimates for this decade are that the demand for lithium carbonate (LCE) will multiply from about 500k metric tons in 2021 to 3 to 4 million metric tons. Therefore, there have already been numerous warnings that the potential availability will not keep up with the demand, even though many new lithium projects are currently being developed.

Not long ago, in 2015, less than 30 percent of lithium demand was for batteries; the bulk of demand was split between ceramics and glasses (35 percent) and greases, metallurgical powders, polymers, and other industrial uses (35-plus percent). By 2030, batteries are expected to account for 95 percent of lithium demand, and total needs will grow annually by 25 to 26 percent to reach 3.3 million to 3.8 million metric tons LCE.

Lithium price

The lithium price has fallen about 70% from its high point for several reasons. Q4 2022 was the strongest quarter ever for electric car sales and rose by 53% YoY, crossing the 10M mark for the first time. However, it was still weaker than expected as China had its last covid restrictions at the end of 2022. Furthermore, Chinese subsidies for EV buyers expired on January 1, 2023, which put additional pressure on prices. It could be that market observers and lithium producers have overestimated a bit, and too much lithium came to the market too fast.

Supply is coming on stream faster than you can say 'boo', demand remains strong but prices have been unsustainable for some time now.

Analyst Dylan Kelly of Ord Minnett in Sydney.

{kind=link}

What is the lithium cost calculated for an electric vehicle? Converted, the price for one ton is currently $25k, which means $25 per kilogram, and in an EV battery, there are about 16kg LCE , which equals $400. This calculation is likely incorrect since it assumes that EV manufacturers buy at spot prices, which they probably don't, but have long-term supply contracts. However, as a rough guideline, this approach is helpful. $400 per vehicle just for the lithium sounds like a lot to me.

The Chinese market

Overall, however, China is the most important and largest market for electric cars. A fact that will become even more important later when it comes to Sodium.

{kind=link}

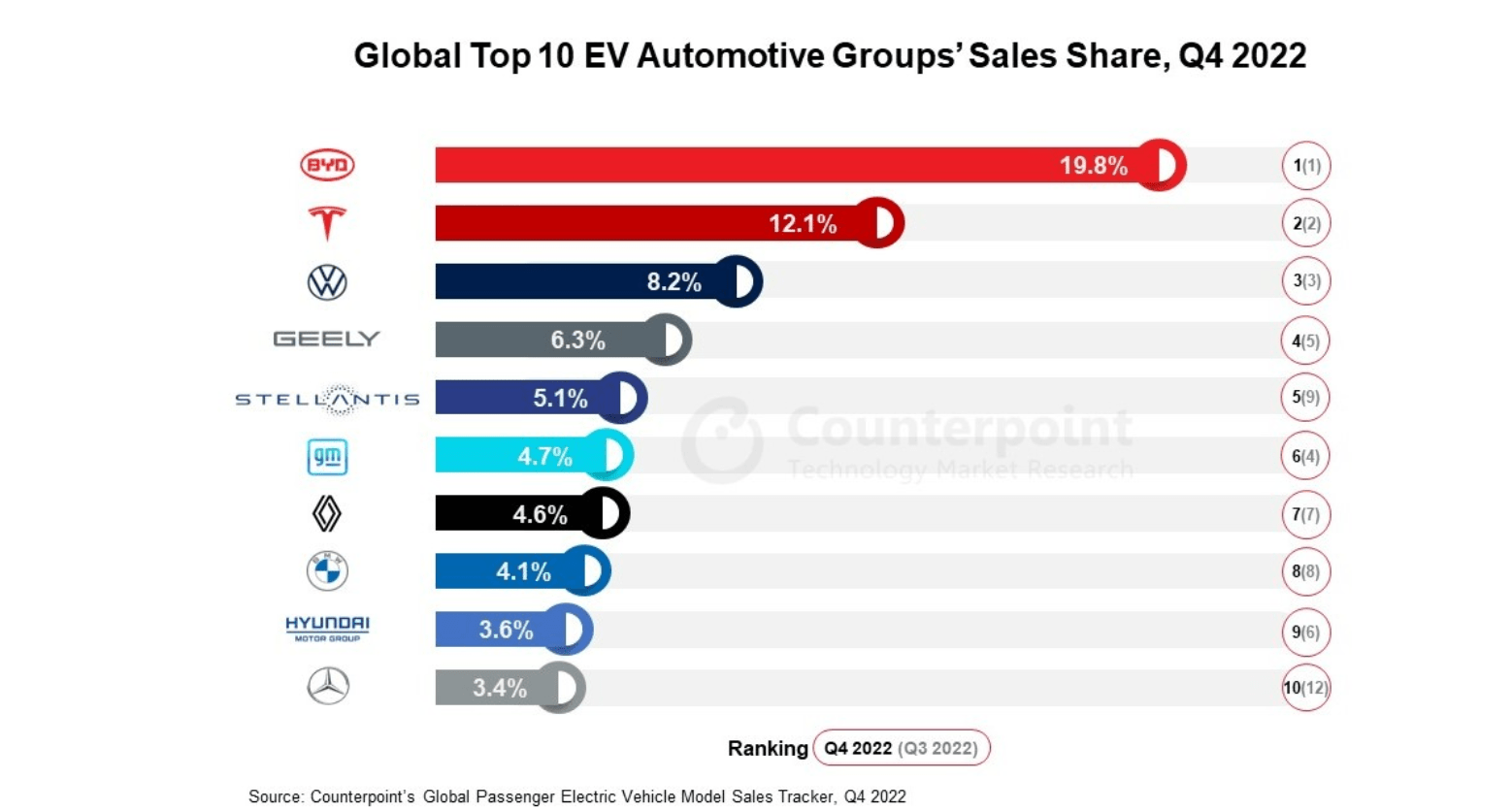

This is also reflected in the ranking of the largest global EV manufacturers, where BYD is the undisputed leader.

{kind=link}

Massive acceleration of EV sales could emerge from a complete ban on the sale of new combustion engines. I think, eventually, this will happen in China, the US, and Europe.

An even stronger policy would be to ban the sale of combustion vehicles. This is a controversial matter in China but local governments could lead the way. In August 2022, the government of Hainan province proposed a complete ban on the sale of combustion cars by 2030 in its implementation plan for peaking carbon emissions. Some experts suggest Beijing city should do the same.

The geopolitical framework of the lithium market

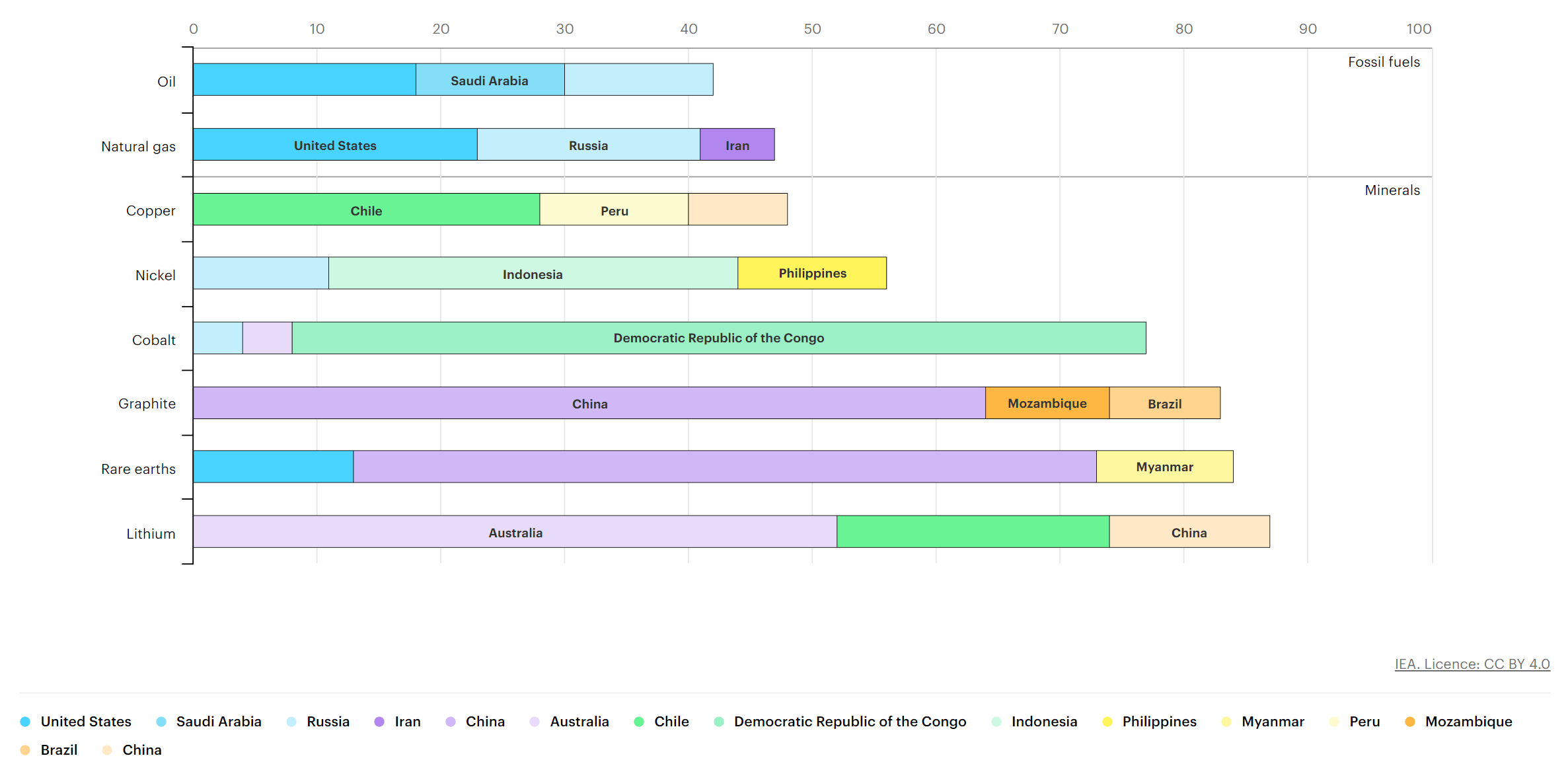

The following chart shows the major producing countries in the extraction of selected minerals and fossil fuels in 2019.

{kind=link}

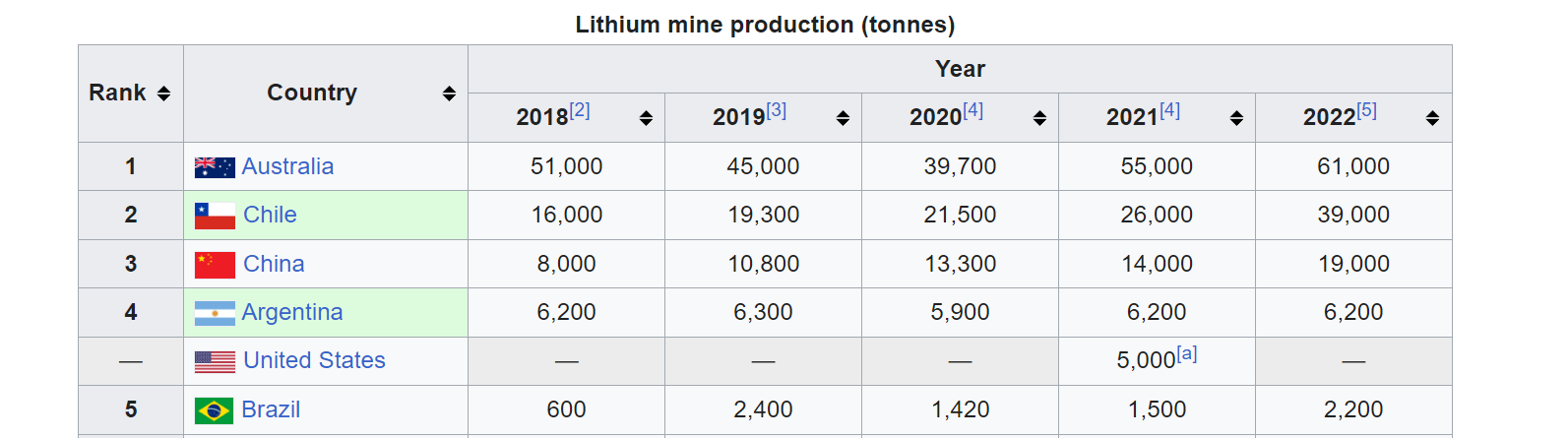

And in the following chart, we can see that the leading countries tend to extend their lead even further; the share of Chile is getting larger. Overall, production is highly concentrated.

{kind=link}

In addition, the following chart shows the leading countries in processing selected minerals and fossil fuels in 2019.

{kind=link}

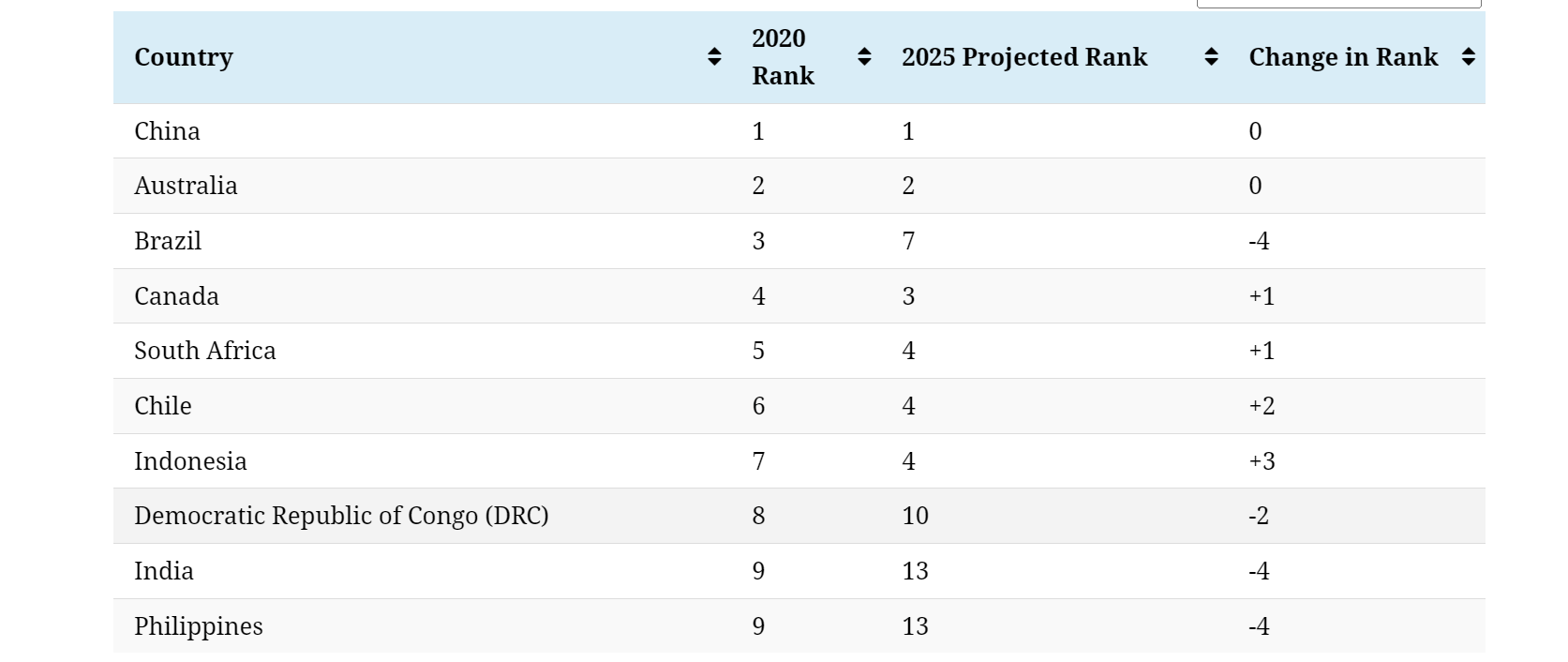

And one last chart, where an attempt was made to establish a ranking of the overall significance of the countries along the entire battery metal supply chain.

China's dominance in the rankings shows that refining capacity is just as important, if not more, as access to raw materials and mining capacity.

China does not boast an abundance of battery metal deposits but ranks first largely due to its control over 80% of global raw material refining capacity. Additionally, China is the world's largest producer of graphite, the primary anode material for Li-ion batteries.

Australia comes in at number two due to its massive lithium production capacity and nickel reserves. Following Australia is Brazil, one of the world's top 10 producers of graphite, nickel, manganese, and lithium.

{kind=link}

With oil and gas, it was and is the case that a few countries accounted for 40 to 50 percent of production and processing. I think what happened is that China realized early on that electrification was their way out of fossil fuel dependence. At least much earlier than the West realized it. Because, unlike the United States, China hardly produces any oil and gets most of its oil delivered via tankers, all of which arrive through a few straits. That means it would be relatively easy to cut China off from its energy in the event of a conflict. This is something that already doomed Germany in both world wars.

So, what they have started to do is to make worldwide supply contracts for lithium. Meanwhile, they have an even bigger monopoly in lithium processing than there ever was in fossil fuels. However, these are also graphics from 2019, and the market is changing quickly and dynamically. In the meantime, the West has also recognized that one must become active here. In this respect, the lithium market will be more diversified in the future, and this is a win-win situation for all parties. Then countries can use the once-bought lithium, graphite, cobalt, and nickel quantities also under the use of recycling repeatedly.

What am I trying to say?

The switch to batteries makes sense from a geopolitical point of view for all sides, but especially for oil and gas-poor regions like China and Europe. Fossil fuels have tremendous advantages and are very energy dense. However, they are also gone once burned and therefore require constant new extraction and deliveries, which is a significant risk, especially for an oil-poor country like China. With lithium and other commodities, the situation is different: The total quantity of metals is constantly increasing, and little is wasted as it is fed by newly mined metals and recycling.

This change from centralized to decentralized energy should be safer for countries overall, especially in crises or war scenarios. A network of millions of batteries, wind turbines, and solar roofs is much more decentralized than just a few thousand large power plants.

Given this framework on all political decisions that we have seen for some years now, the way of electrification seems to be a sure thing. I don't know whether climate change is the real reason for these political decisions or the points I mentioned, but in the end, it doesn't matter. In any case, we are now on this path.

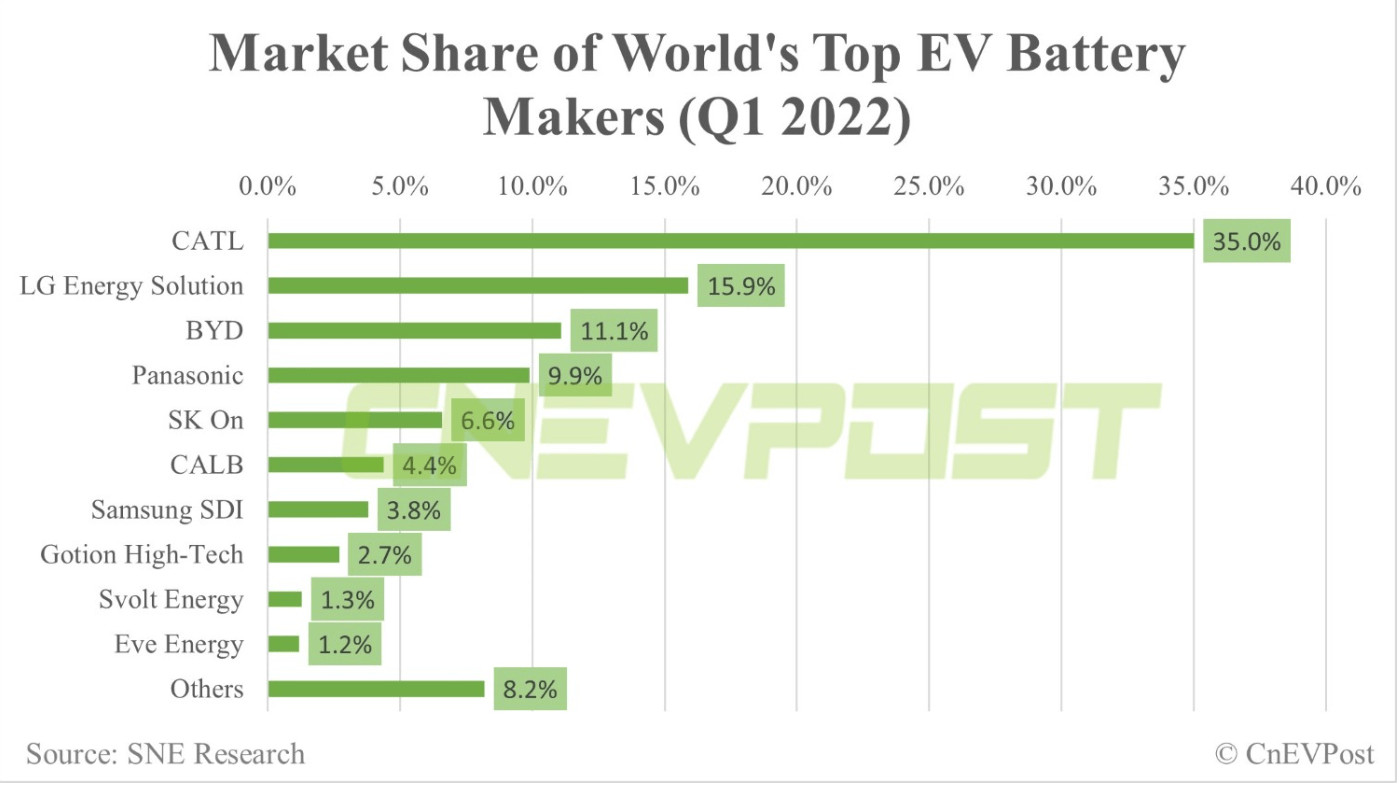

The case for Sodium

CATL is the largest battery manufacturer in the world and is ramping up its capacity at an incredible pace .

{kind=link}

Last year, the company announced that it would set up a production line for sodium batteries in 2023. In December 2022, there were rumors that BYD would release a sodium-based vehicle in 2023. This has proven untrue, but another Chinese manufacturer is now the first to use sodium batteries: the state-owned corporation Chery.

I had never heard of this company. However, according to Business Insider , the company sold 110k cars in 2021 and is one of the cheapest manufacturers overall. Vehicles can be bought for as little as $6000 . The company has about 4% market share of electric vehicle sales, about half as much as Tesla.

Nothing has been published about the exact energy density of these batteries. In my first article about Sodium, I wrote the following:

The energy density of 160 Wh/kg is significantly lower than that of current batteries, which can hold about 270 Wh/kg. However, the density is expected to increase to 200 Wh/kg in the next generation. There are other advantages as well. CATL's sodium cell has excellent cold resistance (90 percent capacity at minus 20 degrees) and outstanding fast-charging capability (0 to 80 percent in 15 minutes).

Sodium Instead Of Lithium: The Biggest Risk To All Lithium Stocks

Overall, it can be assumed that the energy density per kilogram will be about 30% less, and thus the vehicle must either have a shorter range or a higher weight with the same range. Since this manufacturer produces particularly inexpensive cars, they want to reduce costs further. Because one of the great advantages of sodium is its immense abundance: the earth's crust consists of 2.83% sodium but only 0.01% lithium.

How much these savings are is also not known. Sodium battery costs are nowhere near as low as they could be since it´s just starting. The price of Tesla's batteries was still $132/kWh in 2021, meaning thousands of Dollars per vehicle. I'm not sure where this information came from exactly, but here's what I found:

CATL first-generation sodium-ion cells cost about 77 USD per kWh, and the second generation with volume production can drop to 40 USD per kWh.

If a long-term Sodium market emerges and a production chain is established, the price would drop significantly lower in the next few years. That would be huge savings for manufacturers. Further above, I wrote that despite the now fallen price of lithium, the lithium for a single electric vehicle still costs $400. So if manufacturers find a real alternative to lithium, they will seize this opportunity.

Where sodium makes sense, and where does it not?

Sodium is cheaper but bulkier and heavier. The first thing I think of is fixed energy storage, which is needed in huge quantities to store excess energy from renewable power generation. As we all know, this is the most significant disadvantage of wind and solar. Power generation is irregular, so you must store excess power during peak times to use again during lull periods. This requires a lot of storage capacity, likely consisting of millions of small systems. Why use expensive lithium for this?

The first commercial vehicle to use sodium is from a manufacturer that makes particularly low-cost vehicles; that's not a coincidence. One possibility is that manufacturers offer different versions of their vehicles and use Sodium batteries in the low-cost ones. So every buyer can decide if he wants the trade-off savings against a lower range.

But there are also cases where the range is unimportant, and there could be a big market. Namely with autonomous self-driving vehicles. What difference does it make if the range is 30% less as long as it is in the triple digits? If people order a self-driving cab via an app to drive 10 kilometers in a city, this vehicle will drive itself to recharge. For the users, it makes no difference. They probably even prefer a sodium vehicle because this leads to lower acquisition costs for the owner and, thus, lower prices for the users.

Conclusion

I´m not saying that lithium is death with this article. On the contrary: there is a link in this article that shows how CATL is massively expanding its production. The massive expansion of lithium batteries is and remains the most likely scenario. But this production expansion does not come as a surprise; it already occurs in all future demand projections for lithium.

What does not appear is an unexpected competitor threatening to capture a part of the EV battery market. Of course, I don't know if this will happen; it will only become apparent over the next few years. From my analyses of lithium companies, I know that production is to be ramped up as quickly as possible because these companies also assume that lithium demand will explode. So the danger is that unexpectedly in a few years, there could be a lithium oversupply and, therefore, low prices. If sodium could capture only 5% of the battery market, this would already be a lot and relatively unexpected. As I said, the current projections are that by 2030 95% of all lithium will be used for batteries, mainly in EVs. Smartphones etc., will also increase but contain very little lithium.

I think over the next few years, lithium will remain a good investment. Sodium still has to prove itself in practice, and how the further technical developments will go remains to be seen. As a lithium investor, I want to invest where the lowest production costs are because these will have the best margins even at low lithium prices. And if lithium becomes too cheap, the competition will have to stop their production first. However, we are still far away from such scenarios. The Chinese economy is picking up again, and virtually all EVs will still contain lithium in the next few years.

Overall, this is nevertheless the greatest danger for lithium stocks. This metal is expensive, and its extraction harms the environment. Therefore, a cheaper and more environmentally friendly alternative would be bad for the respective companies but better for the future of mankind.

Stocks for which this article is relevant:

AKE:CA , ALB , OTCPK:ARYMF , BATT , OTCPK:CXOXF , OTCPK:GNENF , OTCPK:GNENY , ION , LAC , LAC:CA , LIT , LTHM , OTCPK:MALRF , OTCPK:MALRY , OTCPK:OROCF , OTCPK:PDDTF , OTCPK:PILBF , PLL , SGML , SGML:CA , SLI , SQM ,

For further details see:

Sodium Instead Of Lithium: Important News For All Lithium Investors