SQFTP - Soft Landing Gets Bumpy

2023-09-17 09:00:00 ET

Summary

- U.S. equity markets slumped for a third-straight week while benchmark interest rates returned to the cusp of multi-decade highs after inflation data showed a modest reacceleration in price pressures.

- The disappointing setback follows several quarters of goods-driven disinflation, which was needed to offset some hints of the "wave-price-spiral" effects on the services side- concerns amplified by a UAW strike.

- Finishing lower for the fifth week in the past seven, the S&P 500 declined 0.5%. Despite the uptick in benchmark rates, real estate equities and other yield-sensitive segments were leaders.

- Four REITs raised their dividends this week, while two REITs trimmed their payouts. Commercial real estate brokers faced pressure after CBRE provided a downbeat earnings outlook driven by historically depressed CRE transaction activity.

- One of a small handful of REITs that has remained active on the M&A, Public Storage was little-changed after it completed its previously announced acquisition of Simply Self Storage from Blackstone's nontraded real estate fund - "BREIT" - for $2.2 billion.

Real Estate Weekly Outlook

U.S. equity markets slumped for a third-straight week while benchmark interest rates returned to the cusp of multi-decade highs after inflation data showed a modest reacceleration in price pressures driven by resurgent oil prices. The disappointing setback follows several quarters of goods-driven disinflation, which was needed to offset some hints of the "wave-price-spiral" effects on the services side - concerns that were amplified this week as the United Auto Workers - one of the largest labor unions - initiated a strike after failing to extract a 40% wage increase from the 'Big 3' domestic automakers.

{kind=link}

Finishing lower for the fifth week in the past seven, the S&P 500 declined 0.5% in a choppy week as modestly early-week gains were nullified by the UAW strike on Friday. The tech-heavy Nasdaq 100 also declined 0.5% as cloud giant Oracle dipped after reporting a demand slowdown, while investors were unimpressed by Apple's new product updates. The only major equity benchmark in positive-territory on the week, the Small-Cap 600 finished fractionally higher. Despite the uptick in benchmark rates, real estate equities and other yield-sensitive segments were among the leaders this week. The Equity REIT Index advanced 0.3% on the week, with 13-of-18 property sectors in positive territory, while the Mortgage REIT Index rallied 2.5%. Mortgage rate concerns pressured Homebuilders and the broader Housing Index for a second-week, however, despite solid earnings results from Lennar.

{kind=link}

Energy markets remained in focus this week as Brent Crude Oil prices jumped another 4% to nearly $95/barrel, one of several major commodities that have rebounded sharply from recent lows, a move that threatens to stall or reverse the recent favorable disinflationary trends. Dovish central bank commentary in Europe - in which the ECB signaled that it was likely done with its interest rate hike cycle - helped to partially offset the upward pressure on benchmark interest rates from the UAW strike and the generally disappointing slate of inflation data. The 10-Year Treasury Yield rose by 6 basis points to 4.32% - on the cusp of fresh multi-decade highs - while the policy-sensitive 2-Year Yield rose seven basis points to 5.04%. The U.S. Dollar briefly climbed to six-month highs after the ECB announcement but slipped into the weekend, ending its eight-week winning streak. Seven of the eleven GICS equity sectors finished higher on the week, led on the upside by Utilities ( XLU ) stocks, while Technology ( XLK ) and Industrials ( XLI ) stocks lagged on the downside.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

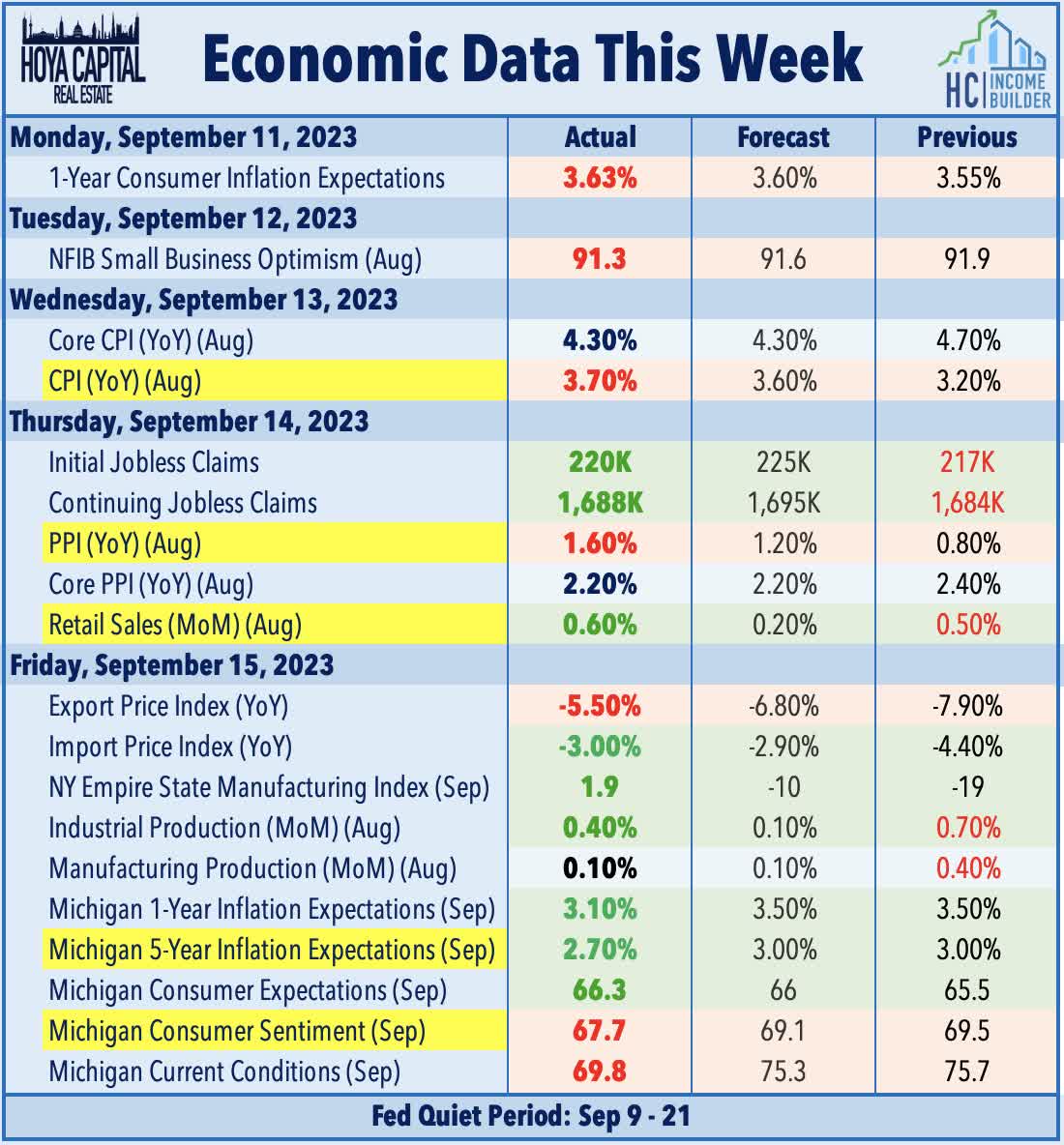

All eyes were on the Consumer Price Index report this week, which showed a disappointing reacceleration of inflationary pressures in August driven by a resurgence in oil prices - the key "swing" inflation input. Fueled by a 10.6% surge in gasoline prices, Headline CPI posted its largest month-over-month increase of the year, pushing its annual increase to 3.7% - in-line with consensus estimates - but up from the 3.2% increase last month. WTI Crude Oil prices - the dominant input in the CPI energy basket - peaked in June 2022 at roughly $120/barrel and had declined as much as 45% from those levels to $67/barrel at recent lows in June before rebounding to near $90/barrel in recent weeks. Retail gasoline prices, meanwhile, also peaked in June 2022 at $5.11/gallon and bottomed in late December at $3.20, but have since increased by 23% from those levels to $3.94/gallon. A bit more encouraging - the metric we watch most closely - CPI-ex-Shelter Index - posted a 1.9% year-over-year increase in August, as shelter inflation still accounted for over 70% of the overall increase in the year-over-year headline CPI figure.

{kind=link}

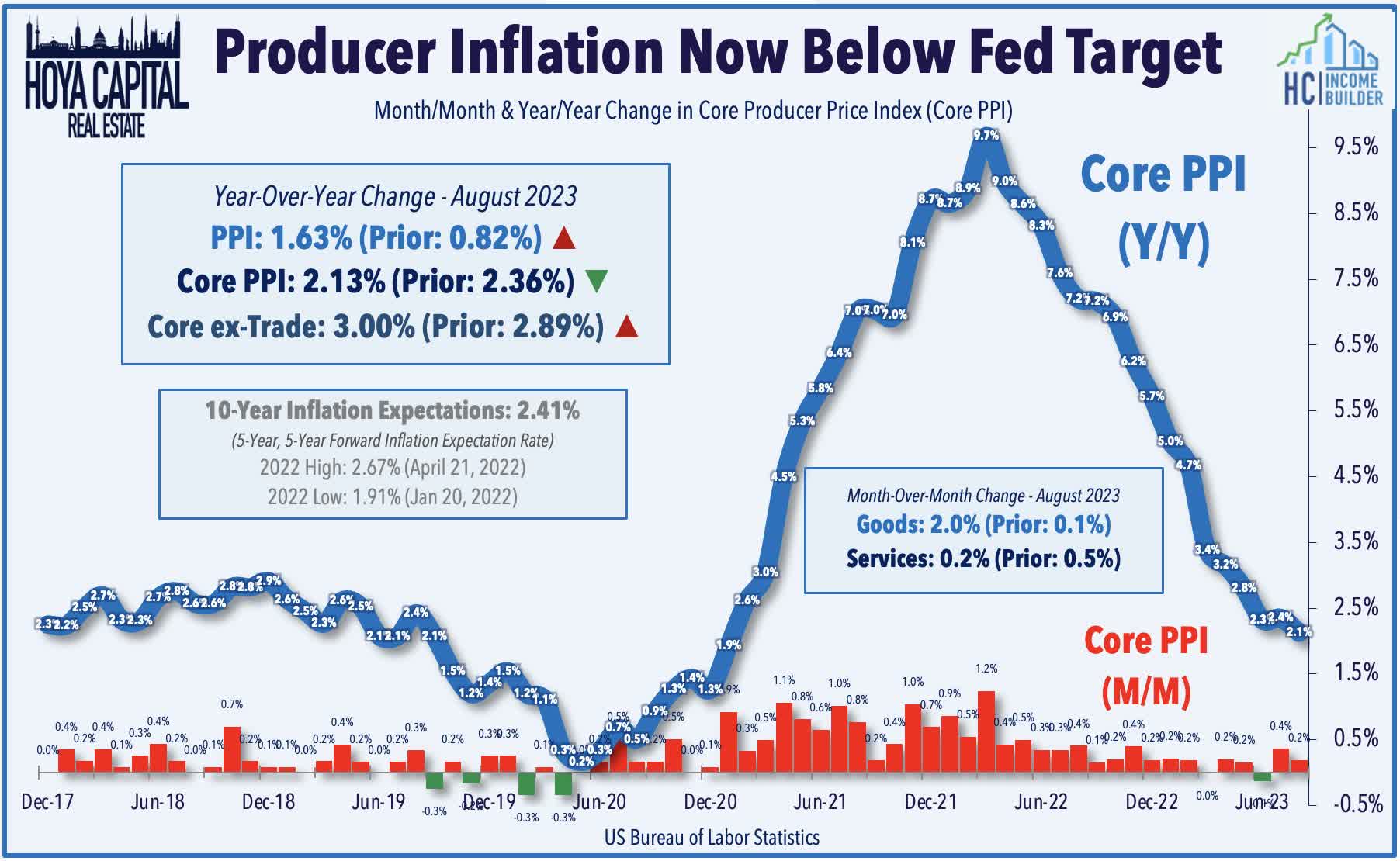

While the Shelter component will start to become a disinflationary tailwind later this year, and while the Median CPI series has shown an encouraging "broadening-out" of disinflation in recent months, the recently-favorable path of disinflation - and by extension, the 'soft landing' - will become considerably more challenging if the Energy component suddenly stops pulling its weight. Energy has been the leading downside contributor to headline inflation since last June. The Producer Price Index data the following day showed similarly mixed trends across the Headline and Core metrics and within the Goods and Services categories, providing evidence for both sides of the inflation debate. The headline PPI rose 0.7% in August - hotter than consensus expectations of 0.4% - which lifted the year-over-year increase to 1.6%, up from 0.8% in the prior month. As with the CPI report, the Core PPI metric (PPI ex- Food/Energy) continued to trend lower. The Goods index increased 2.0% in August - the largest rise since June 2022 - attributable to prices for final demand energy, which surged 10.5%. Over 60% of the rise in the index for final demand goods can be traced to prices for gasoline, which jumped 20.0%.

{kind=link}

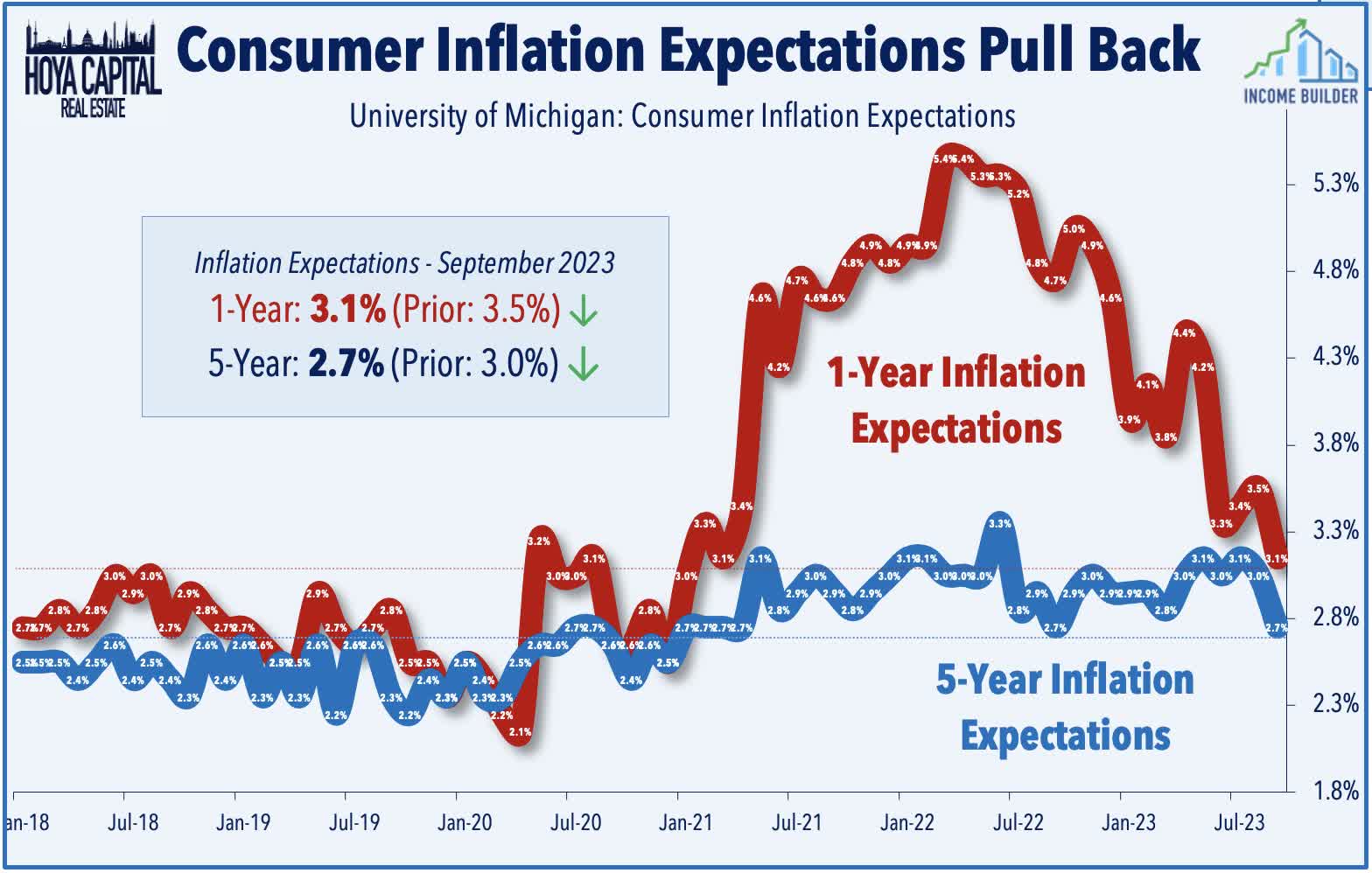

This week's more encouraging inflation data came via the two major inflation surveys. The Michigan Survey of Consumers showed a decline in 1-year consumer inflation expectations to the lowest levels since early 2021 and a decline in 5-year inflation expectations to the lowest in six months. Despite the jump in gasoline prices, consumers now anticipate inflation to be at 3.1% over the next year and 2.7% over the next five years - levels that were effectively back to "normal" pre-pandemic levels. The report also showed that overall Consumer Sentiment ticked down slightly in early September. Earlier in the week, the NY Fed's Survey of Consumer Expectations - showed that median one-year and five-year inflation expectations both edged higher in August. The survey also showed that consumer's expected income growth dropped to 2.9% in August, the lowest reading since July 2021.

{kind=link}

A key look into the health and sentiment of the U.S. consumer, retail sales data this week showed surprising strength in August, contrasting with other recent indicators and corporate commentary hinting at a late-summer slowdown in consumer and business economic activity. Total retail sales increased 0.6% in August compared to the prior month well above the 0.2% forecasted increase - and 2.5% from last year. Gasoline sales drove the bulk of the monthly increase, but spending was also relatively strong in the clothing, electronics, and health categories, while several housing-related categories - furniture and appliances - were generally among the laggards amid a sluggish home sales market. Excluding gas and auto, retail sales appeared weaker, however, with a 0.2% monthly increase, which was 3.6% above last year. As these figures aren’t adjusted for inflation, "real" retail spending is roughly flat year-over-year when adjusted with headline CPI.

{kind=link}

Equity REIT Week In Review

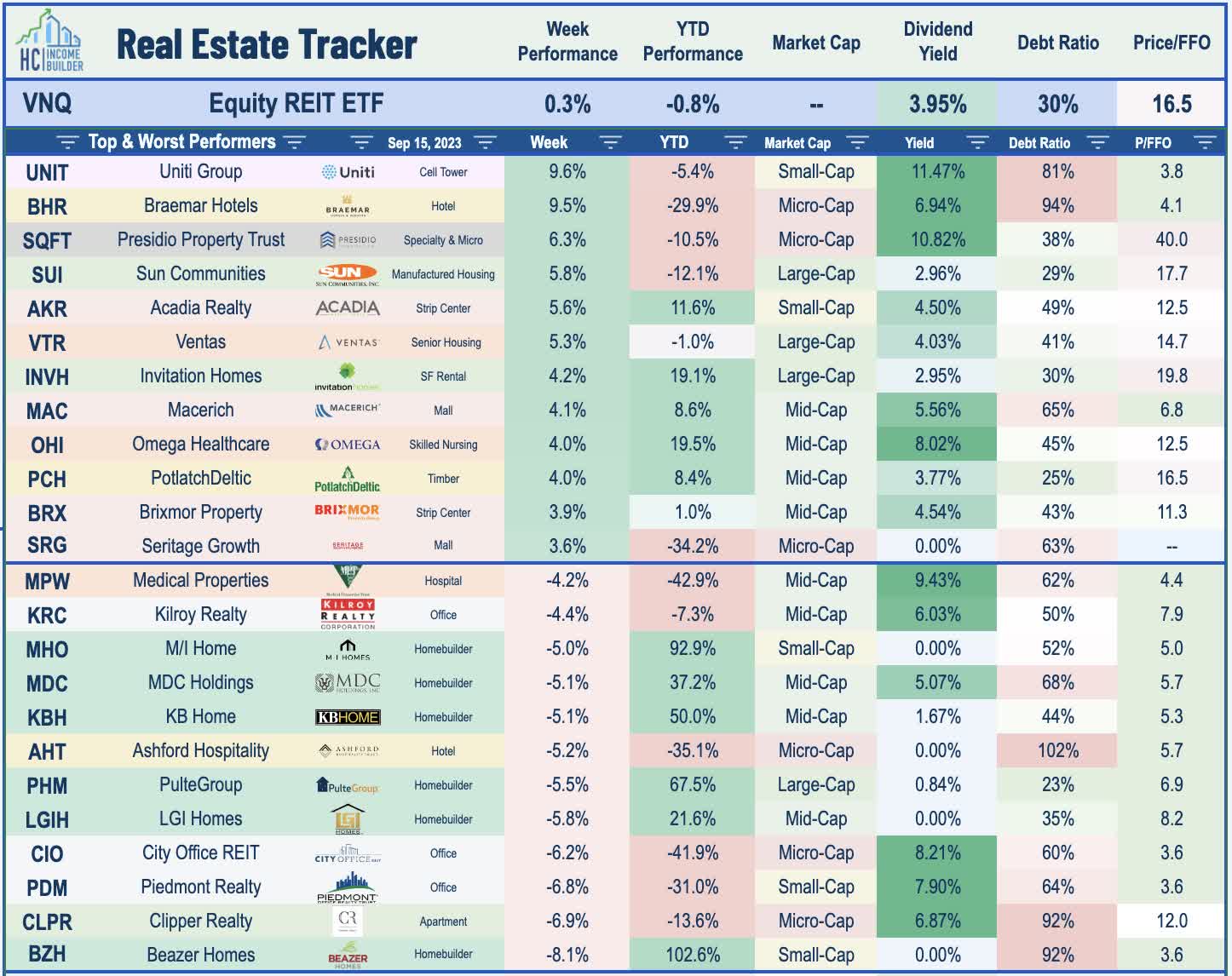

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

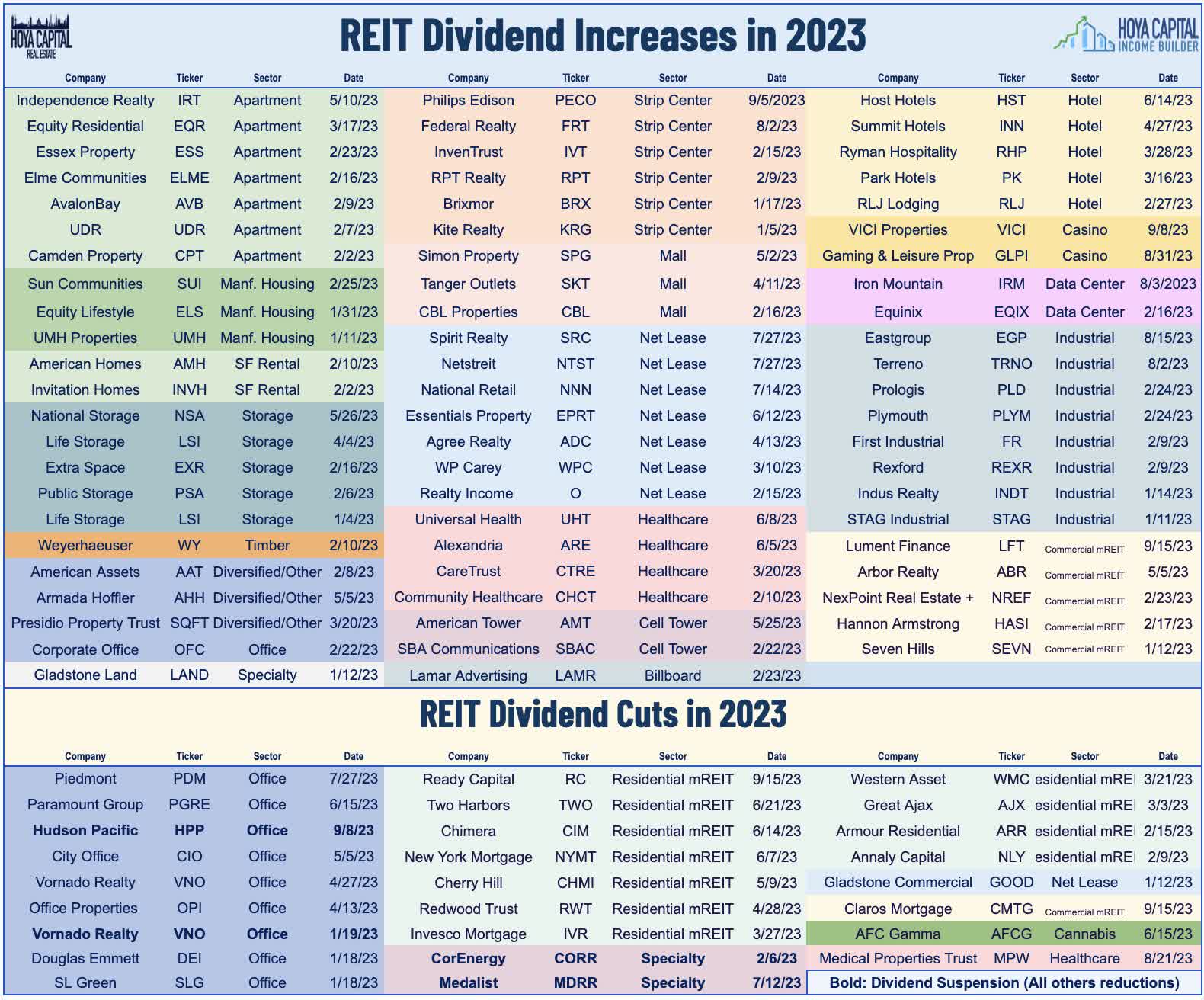

We're in the heart of "dividend season" for the REIT sector. A trio of equity REITs hiked their dividends this week - each of which had already hiked their dividends at least once earlier this year. Host Hotels ( HST ) - the largest hotel REIT - rallied 3.5% after it hiked its quarterly dividend by 20% to $0.18/share (4.4% dividend yield) - its second dividend hike this year - but still slightly below its pre-pandemic dividend of $0.20. Realty Income ( O ) - the largest net lease REIT - hiked its monthly dividend by 0.2% to $0.256/share (5.6% dividend yield) - which is its fourth dividend increase this year and representing a 3.2% year-over-year increase. Fellow net lease REIT REIT WP Carey ( WPC ) gained 0.5% after it hiked its quarterly dividend to $1.071/share (6.7% dividend yield) - up 0.2% from last quarter and 1% from last year. Each of the other 18 REITs to declare dividends this past week held their payouts steady at current levels. We've now seen 68 REITs raise their dividend this year, while 26 REITs have reduced their payouts. As noted in our State of the REIT Nation report earlier this month, overall REIT dividend payout ratios remained very healthy at just 64% in Q2 - its second lowest-level ever and well below the 20-year average of 80%. With a historically low dividend payout ratio, the average REIT has built-up a significant buffer to protect current payout levels if macroeconomic conditions take an unfavorable turn.

{kind=link}

Shares of commercial real estate brokers were under pressure this week after CBRE Group ( CBRE ) provided a downbeat earnings outlook and cautious commentary in a presentation at the Barclays 2023 Global Financial Services Conference. Citing pressure from higher interest rates and depressed transaction volumes, CBRE’s CFO Emma Giamartino noted that the firm is now expecting its earnings per share to fall in the “high-teens range” in Q3. Per Bloomberg, analysts had expected adjusted EPS to remain flat. CBRE dipped nearly 7% - its worst day in three years - while Jones Lang LaSalle ( JLL ) and Cushman & Wakefield ( CWK ) each posted similar losses. CRE brokers have seen historically low transaction volumes in recent quarters as higher interest rates and tighter bank lending has limited capital availability for potential buyers. Meanwhile, downward pressure on property values has made property owners reluctant to sell. With a historically large "bid-ask" spread for private real estate assets, REITs have slowed their acquisitions significantly over the past several quarters with gross purchases of just $7.7 in Q2 - the lowest volume since the depths of the Great Financial Crisis in 2010.

{kind=link}

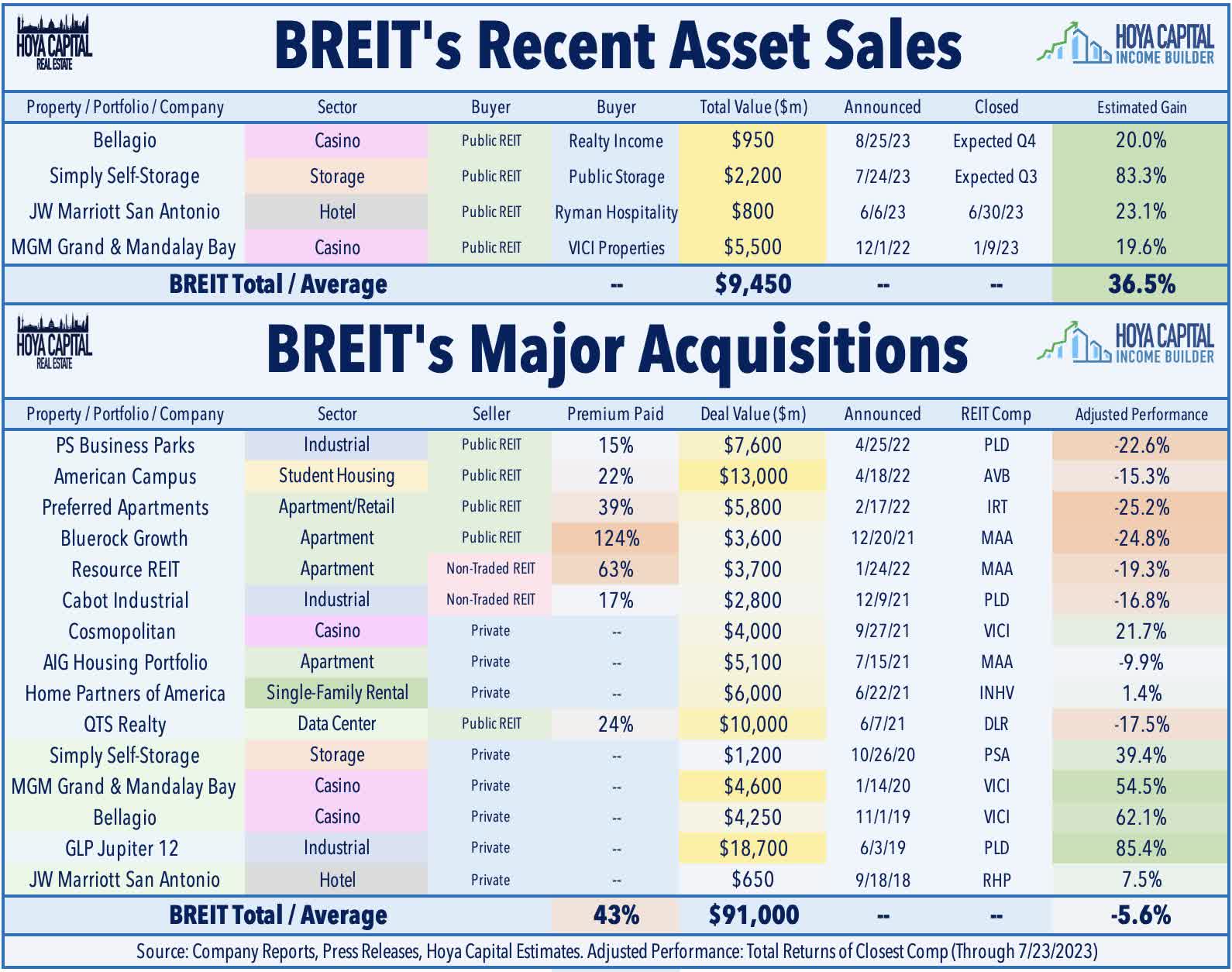

Storage : One of a small handful of REITs that has remained active on the M&A, Public Storage ( PSA ) was little-changed this week after it announced that it completed its previously announced acquisition of Simply Self Storage from Blackstone's ( BX ) nontraded real estate fund - "BREIT" - for $2.2 billion. The portfolio consists of 127 properties and 9M net rentable square feet located across 18 states and in markets, about 65% of which are in Sunbelt markets. We predicted earlier this year that the Simply Storage portfolio - which BREIT acquired in late 2020 - was among the most likely assets that BREIT would sell given its preference to avoid a mark-to-market event by "selling its winners and holding its losers." Four of the six "winners" in BREIT's portfolio are its casino holdings, two of which it has already sold (MGM Grand and Mandalay) and one of which (Bellagio) it sold a partial 20% share to Realty Income ( O ). The other two "winners" are the Simply Self-Storage portfolio and the GLP Jupiter 12 industrial portfolio, which BREIT acquired in 2019. Meanwhile, Moody’s affirmed Public Storage's “A2” senior unsecured debt and “A3” preferred stock ratings following the conversion to an umbrella partnership real estate investment trust ("UPREIT") structure.

{kind=link}

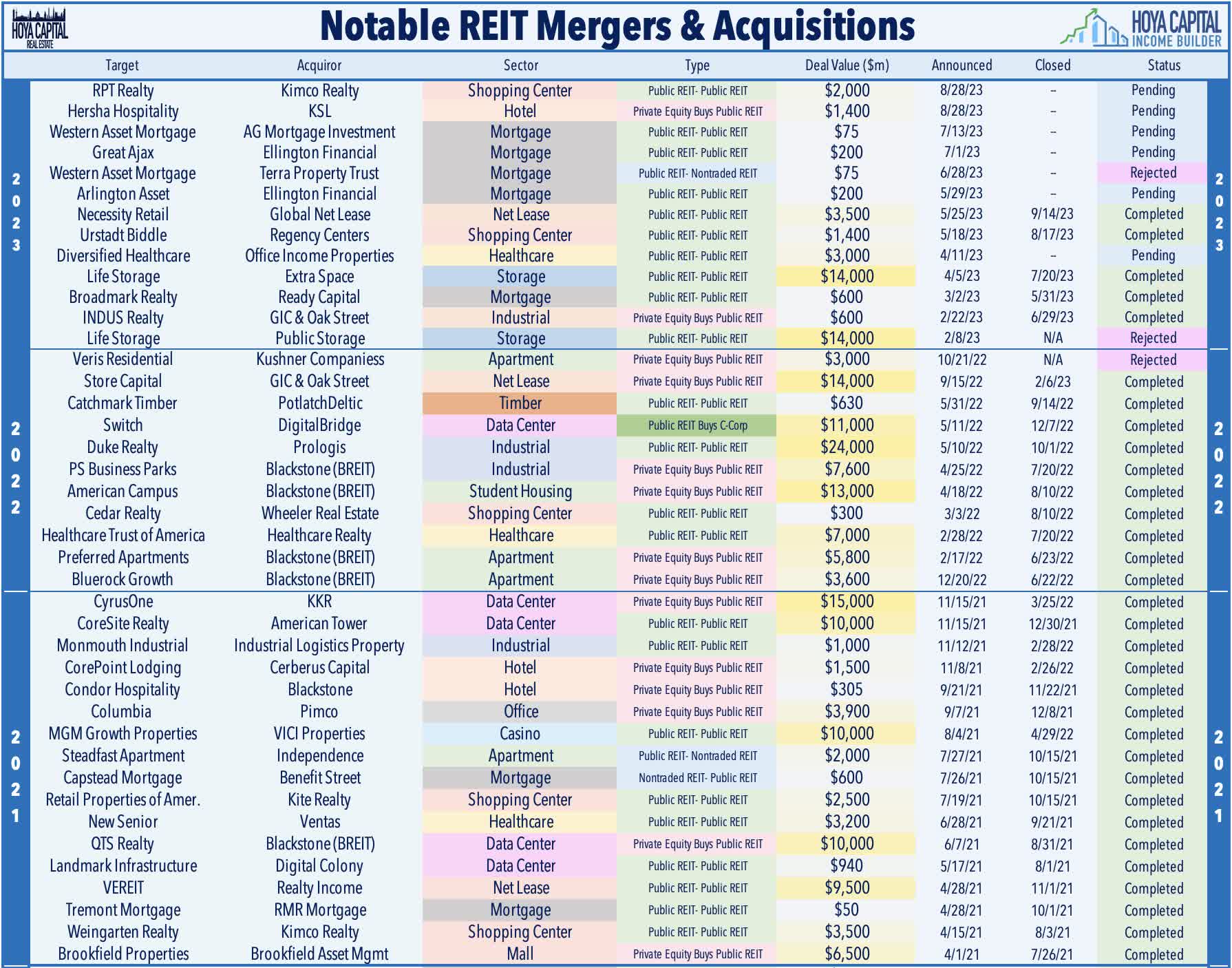

Net Lease : Sticking with the M&A theme, Global Net Lease ( GNL ) and Necessity Retail - a pair of externally managed REITs advised by AR Global - completed their previously announced merger, which included the internalization of both GNL's and RTL's management. Shares of RTL have ceased trading on the Nasdaq. The company cited cost synergies and improved scale as key advantages of the merger, as the combined company owns roughly 1,300 properties with an aggregate enterprise value of $9.5B - a roughly similar size and property sector distribution as other mid-sized net lease REITs Broadstone ( BNL ) and Spirit Realty ( SRC ). As part of the proposed merger, GNL expects to reduce its quarterly dividend by 12% to $0.354 per share (12.7% dividend yield). Elsewhere, micro-cap Presidio Property Trust ( SQFT ) rallied 6% after it announced that its Board of Directors has established a Special Committee of the Board to "explore potential strategic alternatives focusing on maximizing stockholder value."

{kind=link}

Healthcare : Senior housing REIT Welltower ( WELL ) rallied 2% this week after it provided a business update in which it raised its full-year guidance, citing "continued strength" in its Senior Housing Operating Portfolio ("SHOP") and "robust and accretive capital deployment activity." WELL now expects full-year FFO of $3.56 at the midpoint of its range - up from its prior midpoint of $3.54 - representing a 6.1% year-over-year increase. Welltower commented that "expense growth continues to moderate, fueled by further progress on full-time employee hiring" while "favorable demand/supply conditions" have resulted in "favorable occupancy trends across all geographies." Utilizing its at-the-market equity issuance program, Welltower has been among the most active REITs on the acquisitions front in recent quarters, noting that it has completed $1.3B in transactions so far this quarter, fueled by "motivated sellers" and "minimal competition on deals" which has resulted in "increasingly attractive returns." Fellow senior housing REIT Ventas ( VTR ) also rallied 5% after activist investor Land & Buildings renewed its campaign for board changes in a new letter to Ventas shareholders, which hinted hints that L&B may restart a proxy fight. The letter highlighted Ventas' stock price and fundamental underperformance relative to Welltower and concluded that "further action is necessary to address the lackluster returns."

{kind=link}

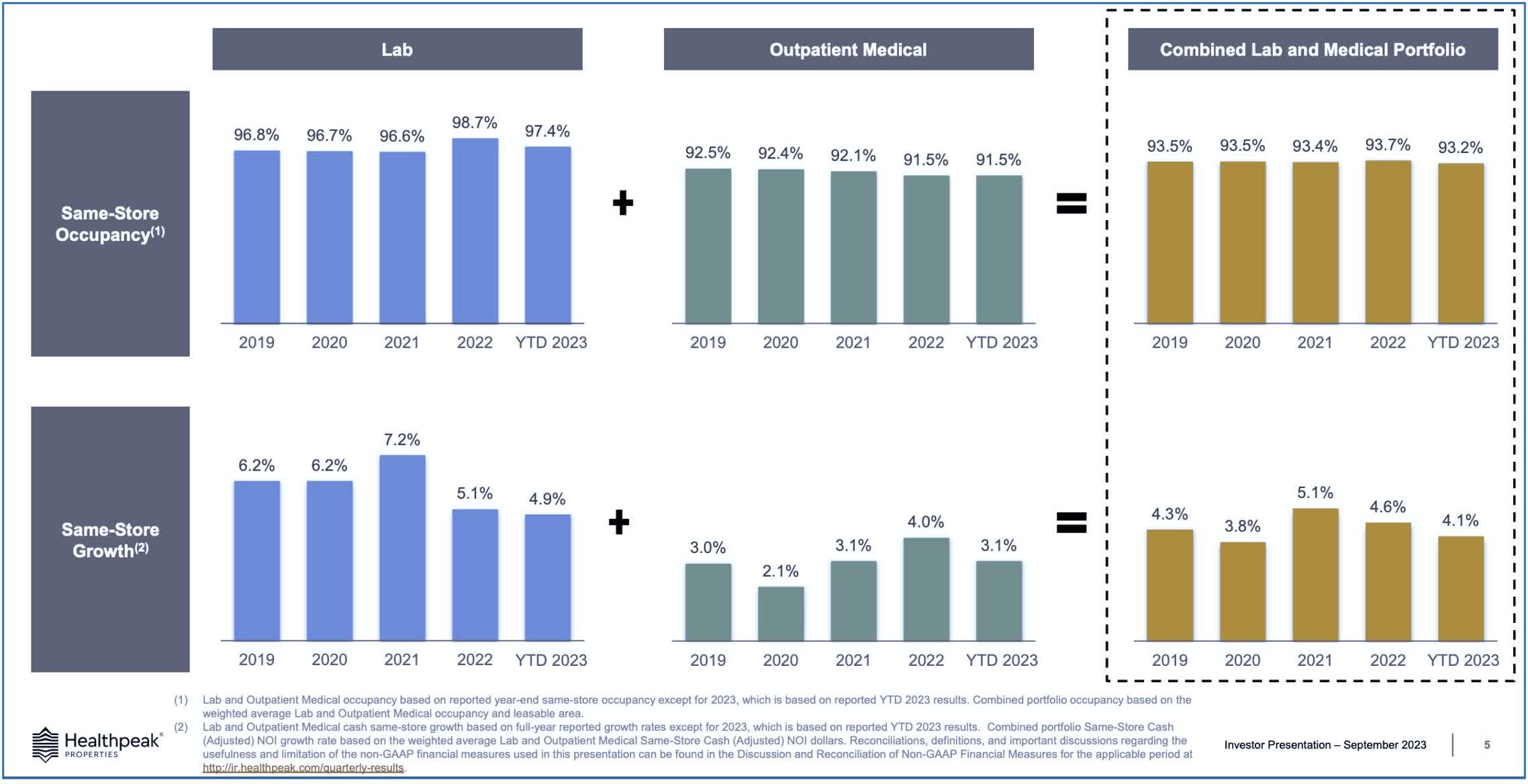

Healthcare : Sticking in the healthcare space, medical office and lab space REIT Healthpeak ( PEAK ) advanced 2% this week after it provided a business update in which it reported that it is "trending to the higher end" of its most recent AFFO guidance ranges "due to favorable recent operating activity." PEAK noted that same-store NOI in its Medical Office ("MOB") segment (40% of NOI) is trending towards the higher-end of its guidance, while its lab segment (50% of NOI) is above the mid-point of guidance. For the year, PEAK has achieved 3.1% same-store NOI growth in its MOB segment and 4.9% in its lab space segment. PEAK addressed concerns about oversupply in the lab space segment - which had seen a wave of development starts in 2021 and 2022 - commenting that supply deliveries are "expected to peak over the next 12-18 months." PEAK also highlighted data showing that biotech M&A and capital raise activity totaled $141B in the first half of 2023 - up over 80% from the year prior - which has eased immediate concerns over rent-paying capacity from several of its smaller tenants.

{kind=link}

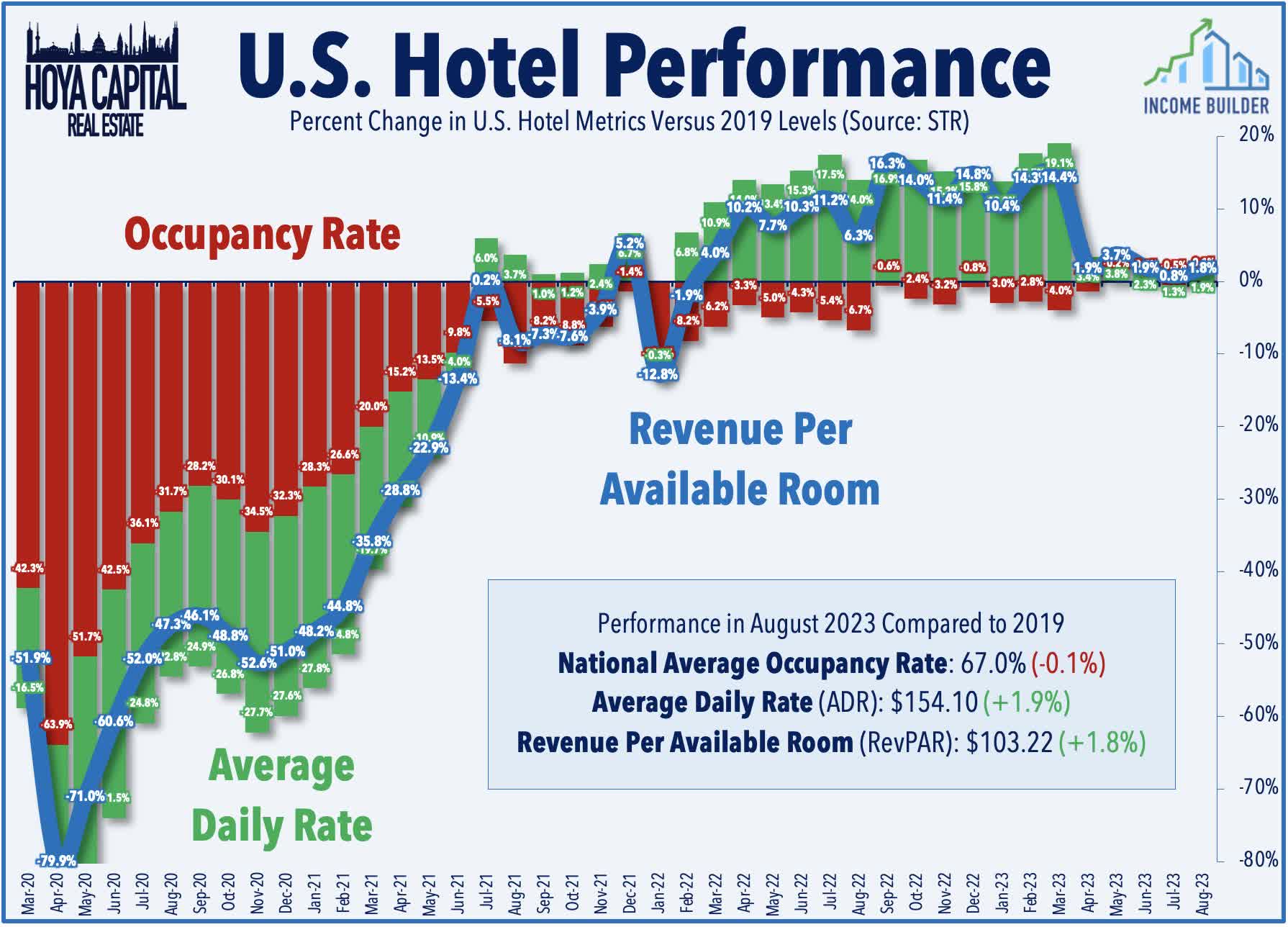

Hotel : Among the leaders for a second-straight week, hotel REITs advanced as Hurricane Lee proved to be less problematic than once forecast, as the East Coast has so far avoided any material impacts from what was previously forecast to be a treacherous Atlantic hurricane season. DiamondRock Hospitality ( DRH ) gained 2% this week after it provided a business update which provided Q3 guidance showing that the firm expects to report RevPAR that is roughly 6% above 2019-levels, representing a modest deceleration from Q2 in which it reported RevPAR that was 8% above pre-pandemic levels. DRH also highlighted several portfolio updates, noting that its 403-room Boston hotel reopened in August following a conversion from a Hilton to an independent lifestyle hotel. DRH also closed on Chico Hot Springs Resort in August, a lifestyle resort in Montana which is DRH’s 15th independent hotel. Travel data firm STR expects that hotel Revenue Per Available Room ("RevPAR") will average about 10% above 2019-levels for full-year 2023. Recent TSA Checkpoint data shows that travel demand has hovered around 100% of pre-pandemic levels since late 2022.

{kind=link}

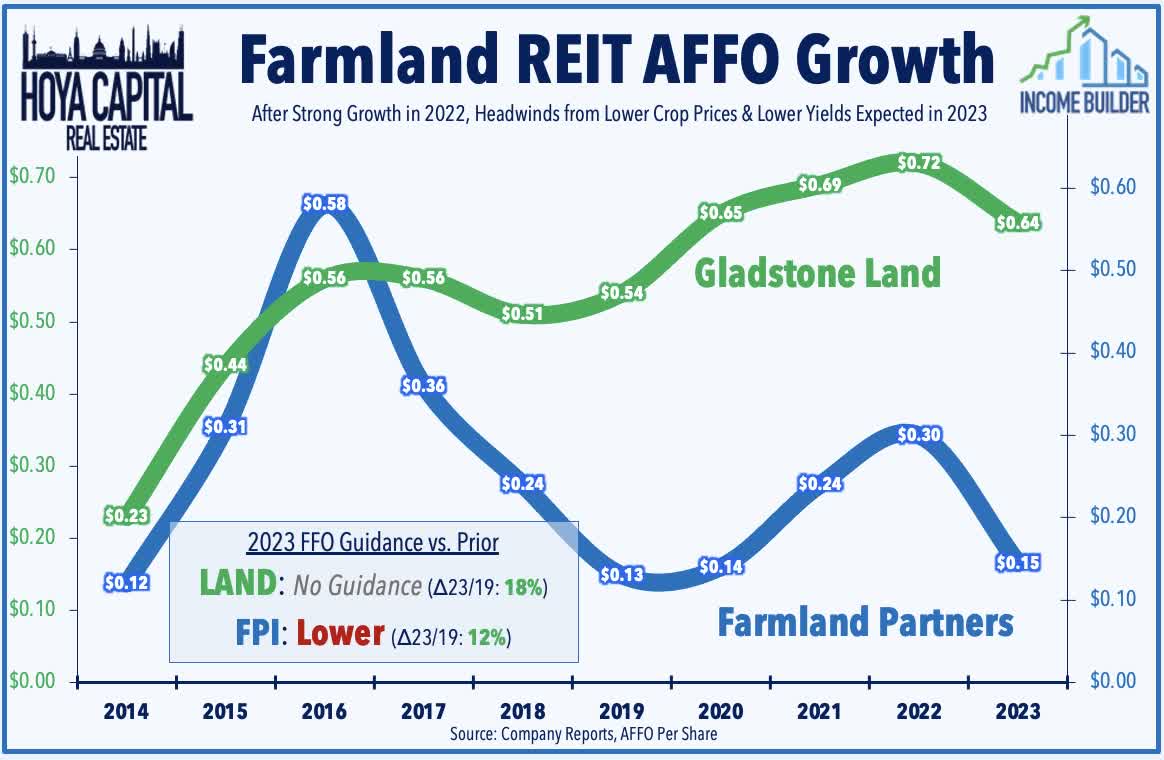

Farmland : Farmland Partners ( FPI ) finished flat this week after it provided business updates on several topics, including recent storms in California and the Southeast, the status of lease renewals, and updated disposition expectations for 2023. FPI noted that Hurricane Idalia and Tropical Storm Hillary caused no significant damage that would impair productivity. FPI also noted that it has completed lease renewals with 50% of the tenants whose lease term expires this year, and that rental rates on these renewed leases have achieved rent increases of more than 15%. FPI also reported that it now expects to sell $190M of farmland properties this year - up from its prior estimate of $135M last quarter. One of the hottest inflation-hedges last year, farmland REITs have laggards this year amid a substantial pull-back in commodities prices from their peaks last May. FPI has been hit by a "triple-whammy" of headwinds: lower crop yield in early 2023 due to drought conditions, lower crop price due to normalization effects after a sharp spike early in the Ukraine-Russia war, and significantly higher interest rate expense due to FPI's elevated level of variable rate debt exposure.

{kind=link}

Last week, we published REITs Are Historically Cheap . Commercial and residential real estate markets remain an easy transmission mechanism - or "punching bag" - of the Federal Reserve's historically swift monetary tightening cycle. The business models of many private equity funds and non-traded REITs were simply not designed for a period of sustained 5%+ benchmark rates or double-digit declines in property values. Private market players and non-traded real estate platforms were willing to take on more leverage and finance operations with short-term and variable-rate debt - a strategy that worked well in a near-zero rate environment but quickly crumbles when financing costs double or triple in a matter of months. "Hope" is the only strategy for some highly-levered property owners amid a dearth of buying interest and dwindling refinancing options. Pockets of distress remain almost entirely debt-driven, however, as property-level fundamentals remain solid across most property sectors. Conditions are aligning in an ideal manner for low-levered entities with access to "nimble" equity capital - conditions that maximize the true competitive advantage of the public REIT model, which these entities have been unable to exploit in the "lower forever" rate environment.

{kind=link}

Mortgage REIT Week In Review

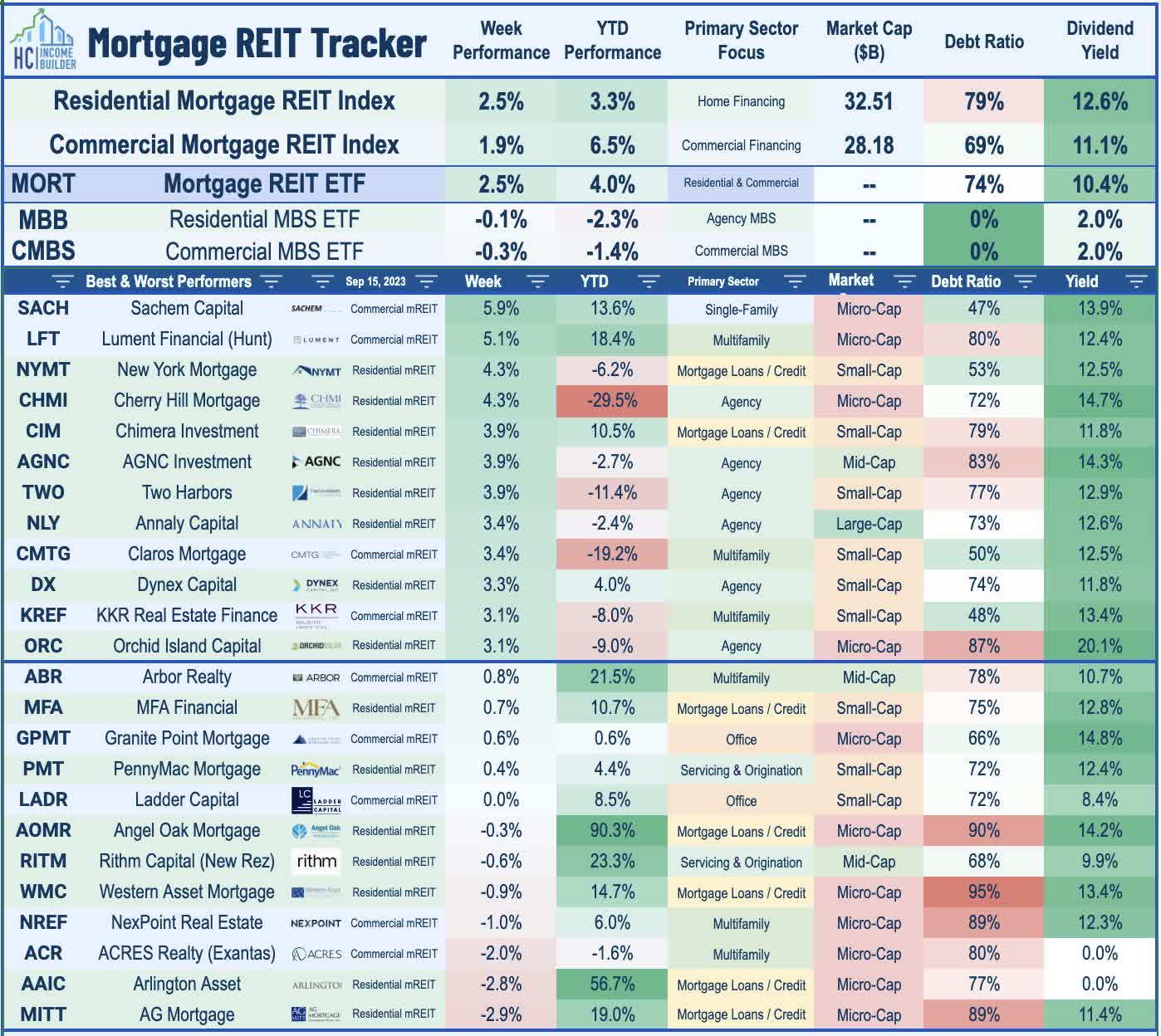

Following declines of nearly 2% last week, Mortgage REITs rebounded this week, with the iShares Mortgage REIT ETF ( REM ) rallying 2.5%. Small-cap Lument Finance ( LFT ) rallied 5% this week after it hiked its quarterly dividend by 17%, becoming the fifth mortgage REIT to raise its dividend this year. Conversely, a pair of mortgage REITs reduced their dividends: Ready Capital ( RC ) trimmed its quarterly payout by 10% to $0.36/share (13.1% dividend yield), which matches its Q2 reported EPS. Elsewhere, Claros Mortgage ( CMTG ) trimmed its quarterly dividend by 32% to $0.25/share (8.4% dividend yield). Each of the other dozen mREITs that declared dividends over the past week held their payouts steady at current levels. In our Earnings Recap , we noted that mREITs stand on steadier ground with dividend coverage after a relatively solid slate of earnings results showing a modest increase in earnings per share. On average, the 21 residential mREITs reported a BVPS decline of 2.2% in Q2 but recorded a 2.0% increase in their distributable EPS. The 19 commercial mREITs reported an average BVPS decline of 1.4%, while the average commercial mREIT reported a 2.5% increase in comparable EPS.

{kind=link}

2023 Performance Recap & 2022 Review

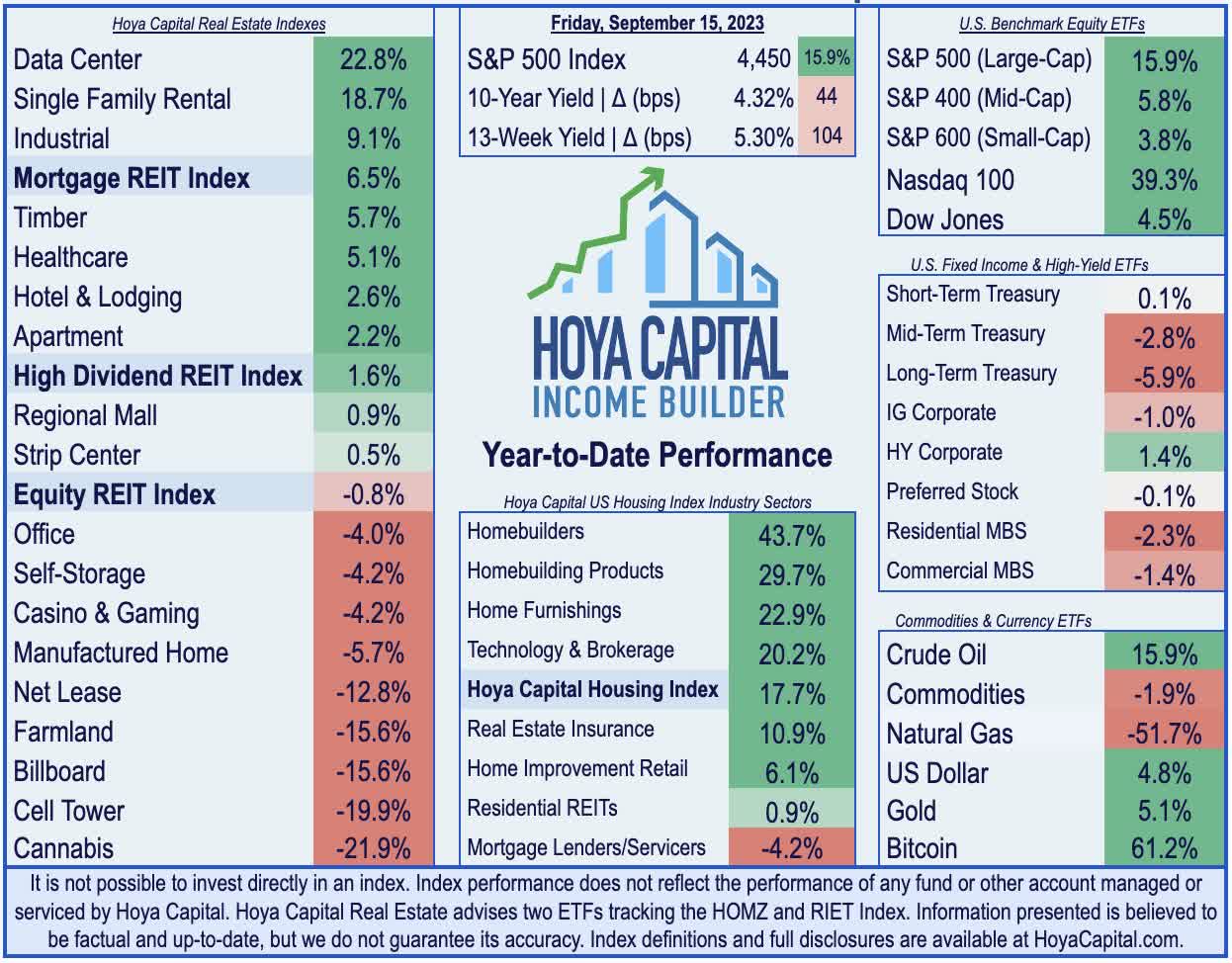

Approaching the end of the third quarter, the Equity REIT Index is lower by 0.8% on a price return basis for the year (+1.5% on a total return basis), while the Mortgage REIT Index is higher by 6.5% (+11.7% on a total return basis). This compares with the 15.9% gain on the S&P 500 and the 5.8% advance for the S&P Mid-Cap 400 . Within the real estate sector, 9-of-18 property sectors are in positive territory on the year, led by Data Center, Single-Family Rental, Industrial, and Timber REITs, while Cannabis and Cell Tower REITs have lagged on the downside. At 4.32%, the 10-Year Treasury Yield has increased by 44 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% in April - and slightly below its intra-day peak of 4.35% in August. The US bond market has stabilized following its worst year in history as the Bloomberg US Bond Index has produced total returns of 0.2% this year. WTI Crude Oil - perhaps the most important inflation input - is higher by 16% this year but remains 15% below 2022 peaks.

{kind=link}

Economic Calendar In The Week Ahead

Central banks are in the spotlight in a jam-packed slate of economic data in the week ahead. The Fed's two-day policy meeting concludes with its Interest Rate Decision on Wednesday. While the Fed is all but certain to maintain the Fed Funds rate at its current 5.50% upper bound in this meeting, the focus will be on the outlook for future rate hikes in November and December. Swaps market now implies a 40% probability that the Fed will hold hike rates once more by the end of 2023 - a probability that has stayed rather consistent over the past month. Before the Fed's decision, we'll see NAHB Homebuilder Sentiment data for September, which declined for the first time in seven months in the last report as a resurgence in mortgage rates has again sapped some momentum from the still-sluggish housing market. On Tuesday, we'll see August Housing Starts and Building Permits data, which is similarly expected to moderate amid a challenging financing environment for both single-family and multi-family development. On Thursday, we'll see Existing Home Sales data which is expected to show sales velocity in August at a 4.10M annualized rate - up slightly from the lows in January of 4.0 million but well below the 2021 highs of over 6.5 million. Housing inventory levels have remained near historically low levels this year due, in part, to the "lock-in" effect on existing mortgages, which has kept a floor on home values and rental rates despite the stiff affordability headwinds.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Soft Landing Gets Bumpy