TCTZF - Sohu: An Unsafe Investment With Declining Sales

2023-08-01 13:20:33 ET

Summary

- Sohu.com is a declining business with a dysfunctional business model.

- The company's main product, the PC game TLBB, has potential in China but is of little interest to the overseas player.

- Created in 2007, TLBB is an old computer game and therefore losing popularity among players.

- Investing in Sohu has a significant geopolitical risk.

Thesis

Sohu.com Limited ( SOHU ) is a declining business in my opinion. A company based mainly on only one computer game does contain some potential, but its realization is probably unlikely. In order for the PC game TLBB to achieve more sustained success, a comprehensive strategic plan for its development would be needed. There is currently no such plan. Brand advertising, which formed a significant part of the company's business in the previous decade, is also shrinking year by year. I think that Sohu is also threatened by geopolitical risk, which is caused by the tensions between China and Taiwan.

Business Overview

Sohu.com Limited was founded in 1996 by Charles Zhang. He also currently owns 33.79% of Sohu's shares. The company is headquartered in Beijing. In 2000, Sohu was listed on Nasdaq. An important part of Sohu's business is the production of computer games through its subsidiary Changyou. The latter was part of Sohu as a subdivision in 2007-2009. Then, in the period 2009-2020, Changyou operated as an independent company on the stock exchange. However, as of 2020, Changyou is once again a subdivision of Sohu. In the past, Sohu also owned the internet search engine Sogou. In 2021, Sohu sold its search engine Sogou to Tencent Holdings Limited ( TCEHY ) for $1.18 billion. It can be said that the current Sohu.com Limited consists of two sub-divisions. One of them is so-called. "former" Sohu, whose main business is brand advertising. It has three main parts.

- Sohu Media Portal is an online news portal in mainland China.

- Sohu Video offers online video content.

- Focus is an online real estate services and information provider.

Another subdivision is Changyou, which is involved in the production of computer games. The computer games segment (Changyou) accounted for 80% of Sohu.com's sales revenue in Q1 2023. While brand advertising ("former" Sohu) provided only 14% of the company's sales revenue.

A game called Tian Long Ba Bu (TLBB) accounts for 65% of the sales in the PC games segment. TLBB accounts for 52% of Sohu Group's total sales revenue.

The PC game TLBB also has a mobile version called Legacy TLBB Mobile. This mobile version generated $72.6 million in sales revenue in 2022, which in turn is approximately 10% of Sohu Group's total sales revenue.

So it can be said that Sohu.com today is largely a company based on one computer game. 62% of the company's sales come from a single computer game. In addition to TLBB, Changyou has 6 other PC and mobile games , but their sales are marginal.

In addition, Sohu has a small business segment that could be called other business. This segment accounts for only 6% of Sohu's sales revenue. This additional segment consists of paid subscription services, interactive broadcasting services and revenue sharing from other platforms.

Economic Results Of The Last Decade

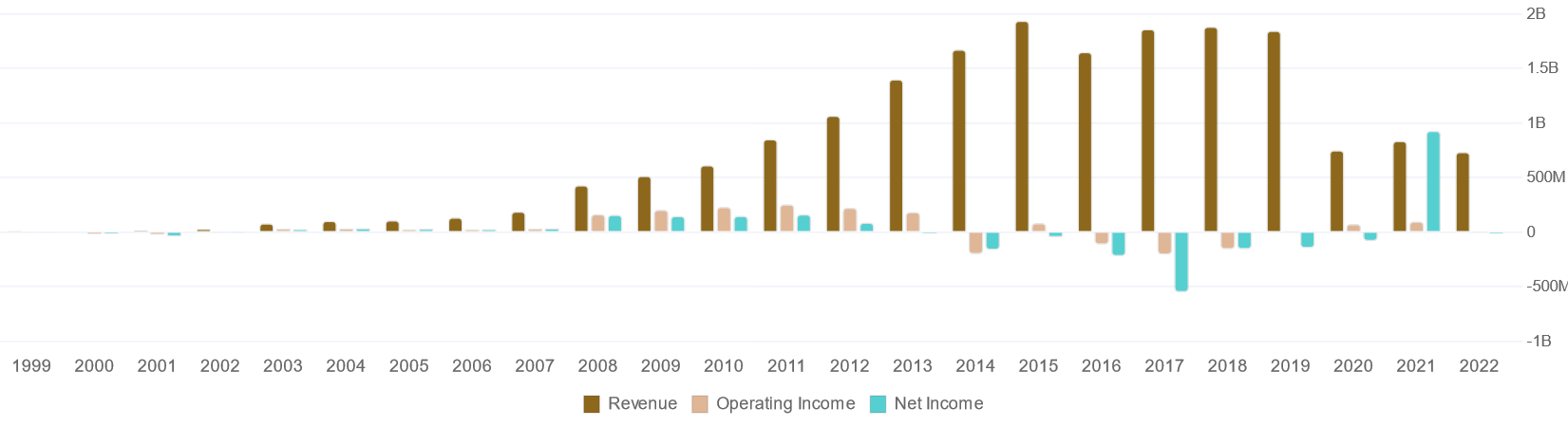

First, let's take a look at Sohu's sales and net income figures for the period 2006-2022.

Sohu`s revenue, operating profit and net profit 1999-2022 (roic.ai)

{kind=link}

| year |

| 1999 |

| 2000 |

| 2001 |

| 2002 |

| 2003 |

| 2004 |

| 2005 |

| revenue |

| 2 |

| 6 |

| 13 |

| 29 |

| 80 |

| 103 |

| 108 |

| net income |

| (3) |

| (19) |

| (44) |

| (1) |

| 26 |

| 36 |

| 30 |

| net profit margin |

| (213.30%) |

| (323.13%) |

| (335.28%) |

| (3.61%) |

| 32.77% |

| 34.53% |

| 27.49% |

| 2006 |

| 2007 |

| 2008 |

| 2009 |

| 2010 |

| 2011 |

| 2012 |

| 2013 |

| 2014 |

| 134 |

| 189 |

| 429 |

| 515 |

| 613 |

| 852 |

| 1067 |

| 1400 |

| 1673 |

| 26 |

| 35 |

| 159 |

| 148 |

| 149 |

| 163 |

| 87 |

| (15) |

| (167) |

| 19.28% |

| 18.49% |

| 36.97% |

| 28.69% |

| 24.25% |

| 19.10% |

| 8.17% |

| (1.09%) |

| (9.96%) |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 1937 |

| 1650 |

| 1861 |

| 1883 |

| 1845 |

| 750 |

| 836 |

| 734 |

| (50) |

| (224) |

| (555) |

| (160) |

| (149) |

| (86) |

| 928 |

| (17) |

| (2.56%) |

| (13.57%) |

| (29.80%) |

| (8.50%) |

| (8.09%) |

| (11.48%) |

| 111.03% |

| (2.36%) |

Sohu`s revenue, net income and net profit margin Currency: USD, in millions source: roic.ai

This table gives an overview of the development of Sohu.com Limited during the last 24 years. In the period 1999-2001, the increase in net loss was still faster than the increase in sales. Therefore, net profit margins then deteriorated. The period 2002-2009 was very successful for Sohu. During this period, both sales and profits grew rapidly. The business model worked profitably. The net profit margin went from negative territory to positive territory and reached over 30% in some years. The first signs of downward movement began to appear in 2010, when the net profit margin began to weaken. In the period 2010-2015, sales continued to grow, but the net profit margin gradually worsened. From 2013 until today, the company's business model has stopped working. In all years (except 2021) money has been burned. The positive result in 2021 was due to the sale of the search engine Sogou to Tencent Holdings Limited (TCHEHY).

The reason for the decline of Sohu, in my opinion, has been the loss to its competitors in the field of brand advertising and internet search engine business. If in the business of online news and brand advertising there can be several players in the market at the same time, in the search engine business there can only be one of them in my opinion. The latter is clearly proven by the example of Google.

Results Of The First Quarter Of 2023

The results of the first quarter of this year also confirm the continuation of the decline. The company's revenue was $161.79 million vs. $ 193.42 million a year ago. Net loss per share was (0.53) cents vs. with the previous year's profit of 0.07 cents.

Viewed by business segment, the result was as follows: Brand advertising sales in the first quarter were $22.5 million. This was 5% less than a year earlier. Online gaming sales were $129.5 million, down 18% year over year. Although TLBB is the company's most popular selling item, demand for this game can also be seen to decrease. In order to restore and increase demand, it is necessary to constantly add innovations and improvements to the game. However, this requires expenses.

Although the number of user accounts for PC games increased by 8% year-on-year to 2.2 million users, at the same time the number of active payment accounts decreased by 4%. The computer games offered by Changyou are mostly free for the user in the basic version, the fee is added only after the player wants to use some additional elements in the game that make the game more interesting. Due to the last fact, the number of actively paying accounts is an important factor for the company. In the first quarter of 2023, there were 0.9 million active paying accounts. In the mobile games sub-segment, the number of active accounts and actively paying accounts decreased by approximately a third compared to a year ago. Although the decrease in active payment accounts may be partly due to the "natural obsolescence" of games, the question of the sustainability of these games may also arise here.

The Evolution Of the TLBB Computer Game Over The Years

Sohu's flagship product, Ti an Long Ba Bu (TLBB) is a multiplayer online role-playing game. In other countries it is also known as the Dragon Oath. The story is based on Louis Cha's novel Semi-Gods and Semi-Devils. Although before 2016 this game was also distributed on servers in Europe and the USA, today it is closed in these regions. It is a martial arts game where players have the option to play in any way and "decide their own destiny". The game is based on Buddhist cosmology. The story is based on three heroes, which are Qiao Feng, Duan Yu and Xuzhu. They all have a role to play in this game. The events take place in the ancient Kingdom of Dali, which existed on the territory of modern China in the 10th-13th centuries.

In addition to China, Dragon Oath has a server in Malaysia and Vietnam. In 2011, Changyou made also a customized version of this game for the Turkish PC game market.

The computer game TLBB (Dragon Oath) was created in 2007. Its "younger brother", the mobile game Legacy TLBB Mobile, was created by the same development team in 2017.

Following table shows the revenue of one of Sohu/Changyou's most popular computer games, TLBB, since 2009. The data is incomplete because I could not find it for some years. The following data only concern the computer game TLBB (does not including the results of the mobile game Legacy TLBB Mobile).

| year |

| 2009 |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2022 |

| TLBB revenue |

| 250 |

| 411.9 |

| 315.6 |

| 219.7 |

| 197.7 |

| 200.9 |

| 378.5 |

in millions of USD sources: Changyou Annual Reports 2014-2018, Sohu`s Annual Report 2022

The table shows that the popularity of TLBB was on the rise until 2014. Then, in the period 2014-2017, the sales of this computer game decreased. Over the past 5 years, TLBB has started to grow in popularity again. The renewed popularity is certainly a good sign for the company, but it may not be enough to save Sohu's generally dysfunctional business model. It will be interesting to see how the players will accept the new game TLBB Mobile , which will be launched in the third quarter of 2023.

The following table shows the development of the sales numbers of Sohu's online games business in the period 2016-2022.

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Sohu online game revenue |

| 395,709 |

| 449,533 |

| 389,788 |

| 440,908 |

| 536,684 |

| 638,225 |

| 585,424 |

source: Sohu`s Annual Report 2022

As with TLBB's sales numbers, overall online game sales have generally been on the rise since 2016. One of the catalysts for this growth has certainly been the organic growth of the Chinese computer game market.

China's Online Gaming Market Outlook

Since Sohu's computer game business is also significantly dependent on the overall development of the Chinese computer game market, let's take a quick look at that as well.

In March of this year, Goldman Sachs published an interesting article on the Chinese computer game market. I'm referencing some thoughts from this article.

- With 650 million users and $45 billion in sales, China's computer game market is the largest in the world.

- As a whole, the online gaming market has 3.2 billion users worldwide.

- Chinese computer game manufacturers have good potential to go into overseas markets. This potential has also been successfully realized in recent years. For example, in the global mobile game market, the share of Chinese game manufacturers has increased from 6% in 2015 to 22% by 2022.

- The spending of the Chinese population on computer games has risen to 0.6% of the country's gross domestic product. For comparison, in Japan the corresponding figure is 0.8% and in North America 0.4% of the gross domestic product.

To what extent is the computer game TLBB of interest to players outside the Chinese cultural space? I think rather not very big. This game is related to Chinese traditional lore. However, this tradition is not well known in other parts of the world. In addition, it is quite an old game, which was created already in 2007 and therefore has already exhausted itself. At the same time, the new TLBB Mobile game launched in the 3rd quarter of this year may be successful in China. As the share of mobile games in the world is currently on a fast upward trend compared to traditional PC games, the new TLBB Mobile can help significantly increase the revenues of Sohu's mobile games sub-segment.

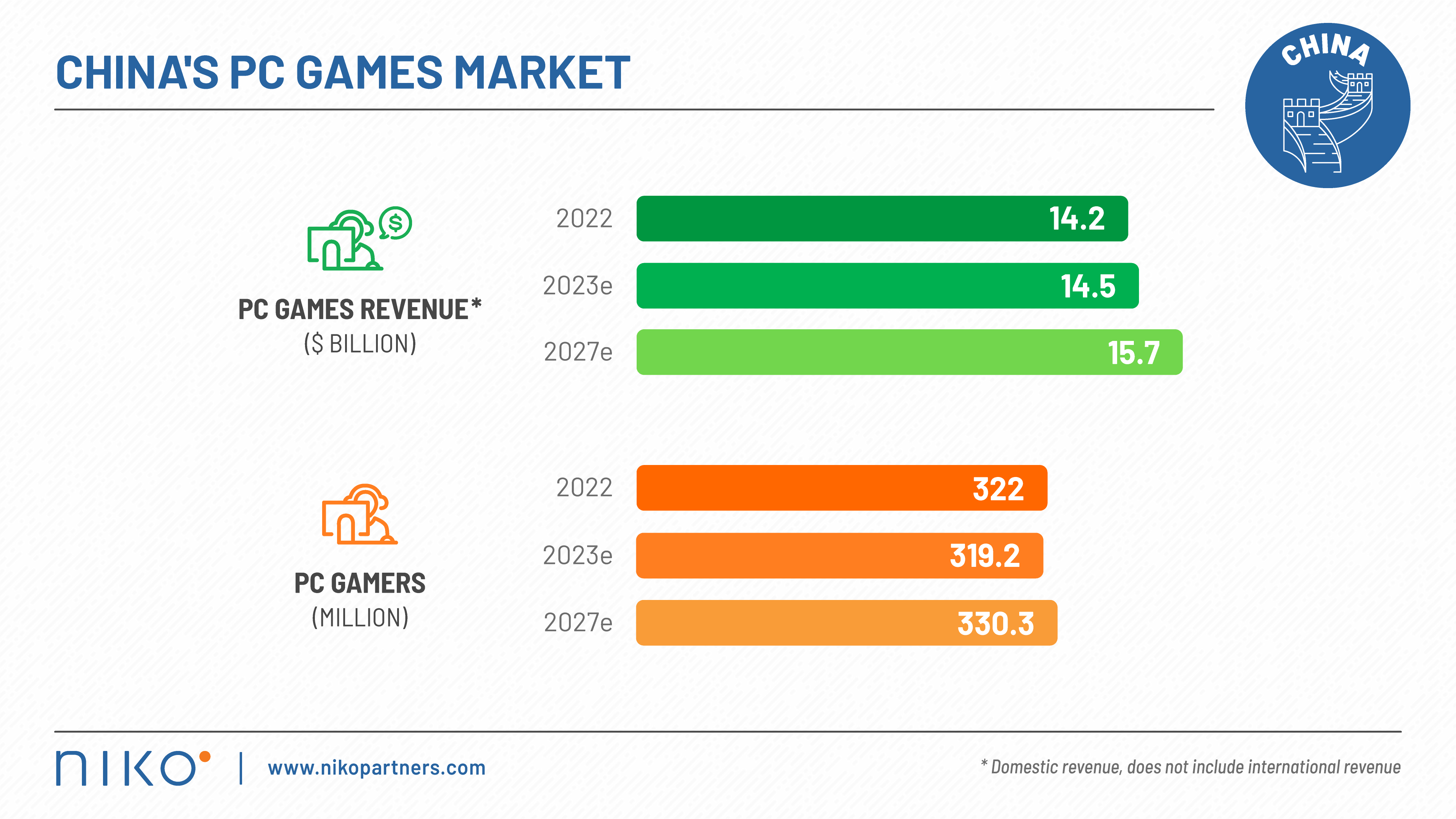

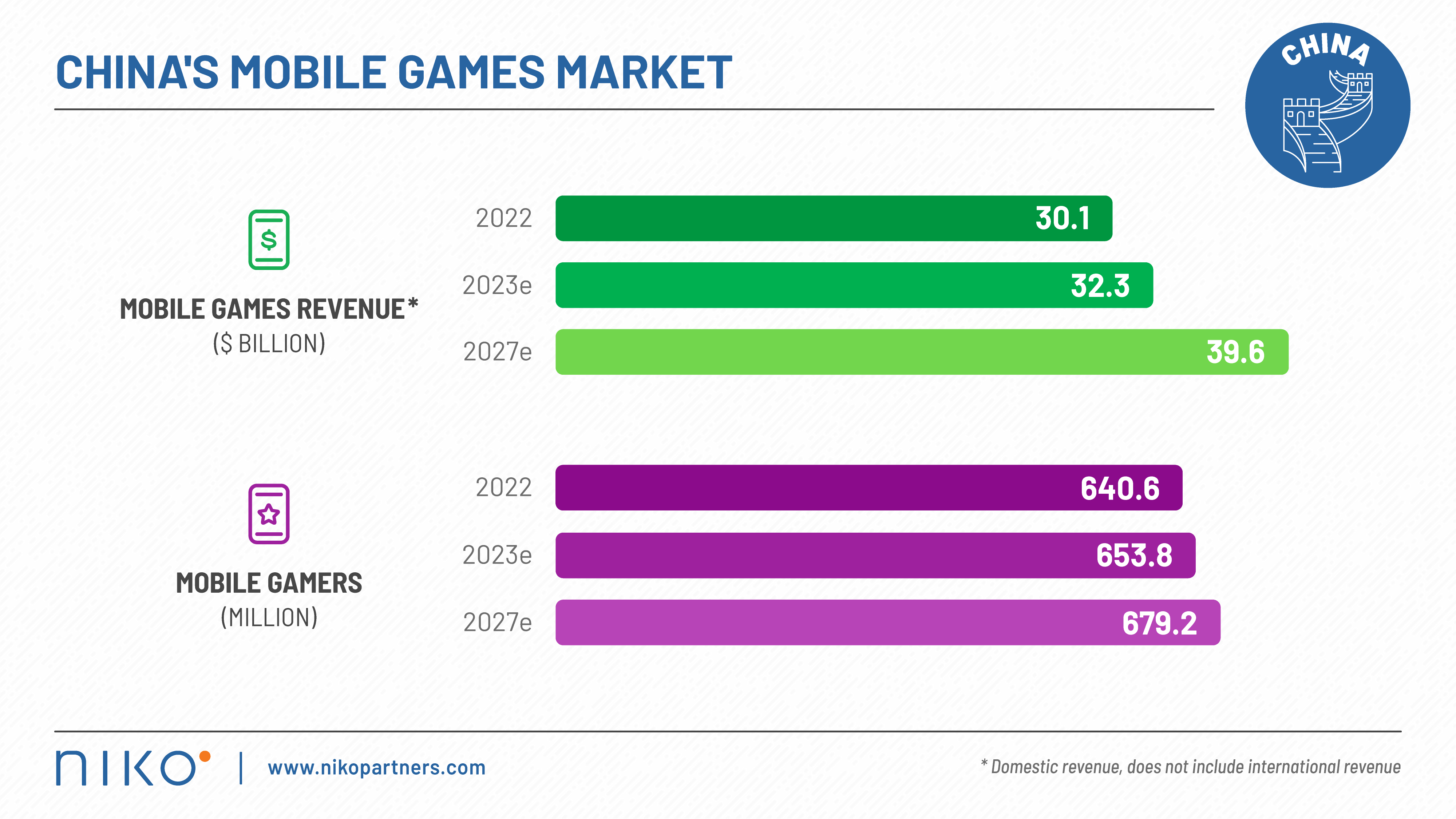

Next, let's see what growth is predicted for the Chinese computer game market. Conventionally, the market of computer games can be divided into three parts. These are PC games, mobile games and console games. Nikopartners.com provides a forecast for all sub-segments of the Chinese computer game market for the next 5 years.

China`s PC games market forecast for 2027 (nikopartners.com)

{kind=link}

Based on the above forecast, China's PC gaming market will have an average annual growth rate of 2.02% during this period.

China`s mobile games market forecast for 2027 (nikopartners.com)

{kind=link}

However, the average annual growth of mobile games in the same market is much faster, i.e. 5.63%.

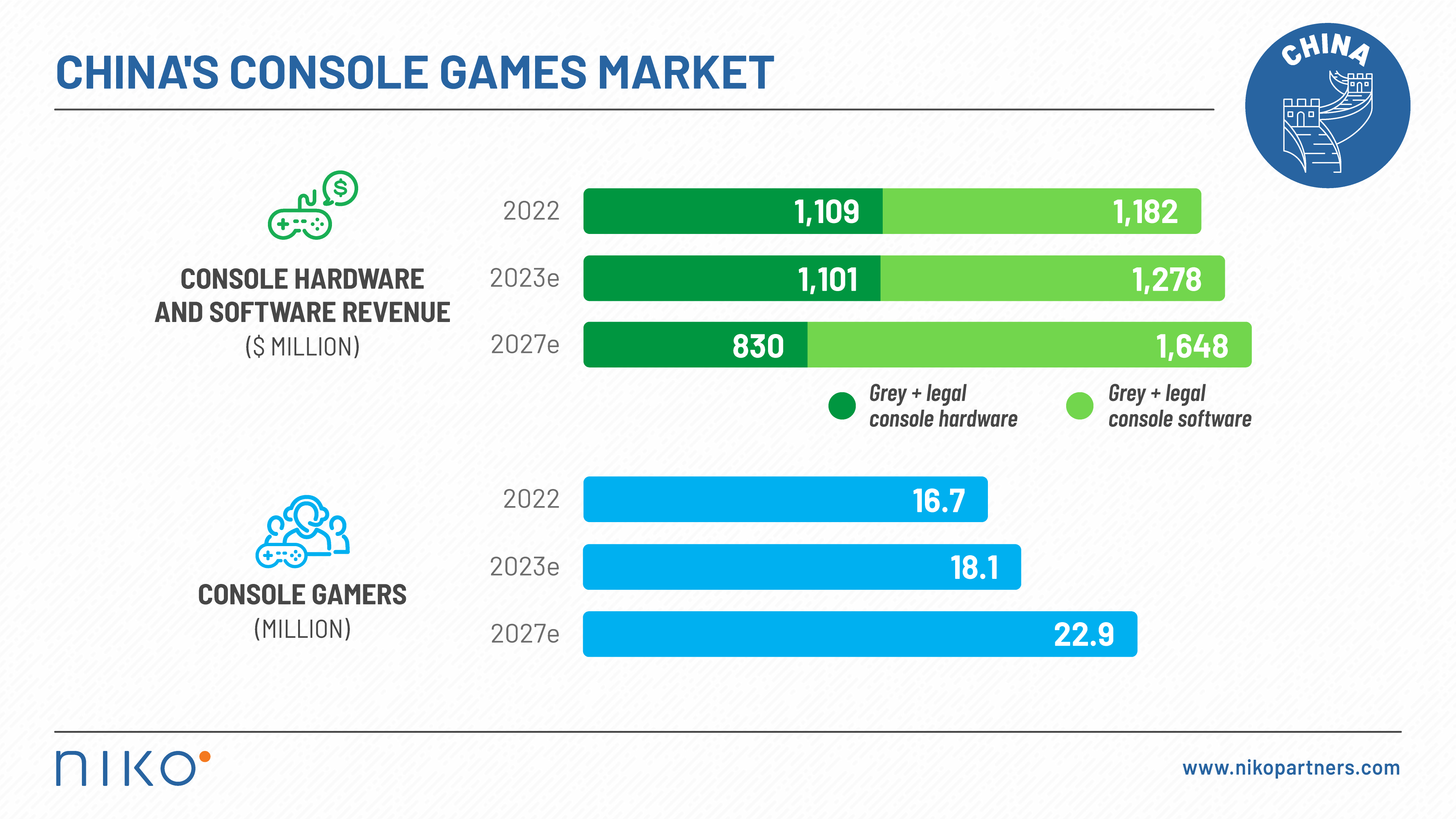

Only a marginal, approximately $2 billion, share of China's computer game market is made up of the console games sub-segment. The example below illustrates this.

China`s console game market forecast for 2027 (nikopartners.com)

{kind=link}

As can be seen from the above examples, mobile games are already the largest sub-segment of the Chinese computer game market. It also has the fastest growth rate.

Sohu's Balance Sheet and Debt Ratio

As of Q1 2023, the company had total assets worth $1,968.9 billion . Total liabilities were $864.1 million. Total equity was $1,104.7 million. The debt/equity ratio is therefore 0.78. This is a perfectly reasonable rate in my opinion. Based on the macrotrends.net data I have, Sohu has never been under a very high debt burden since 2009. Maybe with the exception of the whole of 2020 and the first half of 2021. After the sale of search engine Sogou to Tencent, Sohu's debt/equity ratio has decreased significantly.

Valuation

Using the discounted cash flow method, at a 7% discount rate, we get the intrinsic value of Sohu at $8.3. At an 8% discount rate, the intrinsic value of the company is $5.7

I got these results using the following data: Free cash flow ((TTM)) $23.7 million, total cash $525.5 million, total debt $864.1 million, shares outstanding 33,740,000, current stock price $ 11.10, expected growth rate 0%, growth stage duration 10 years, terminal growth rate 2%, terminal stage duration 5 years. I used 0% as the expected growth rate because Sohu has been mostly unprofitable over the past decade.

So, based on the discounted cash flow method, Sohu's stock is significantly overvalued in my opinion.

However, according to the price/book ratio, this company is quite cheap. Sohu's price/book ratio is currently 0.34 . The median price/book ratio of the sector is 1.65. While equity is $1.104 billion, intangible assets make up $52 million of that total. Sohu currently has a market capitalization of $372 million. At the current price level, Sohu shares could be bought at approximately 3 times lower than the book value. However, the problem is that the company's business model is not working and it has not been able to generate profit for a long time.

Risks

My current perspective on Sohu is negative. Therefore, I would primarily analyze the upside risks below.

As the main upside risk, I see the possibility that new versions of the PC game TLBB may turn out to be more successful than expected. Also, some of the new PC games created by Changyou may prove to be successful globally. As Chinese computer game manufacturers are seen to have good opportunities in overseas markets in the coming years, a new computer game created by Changyou could bring a turnaround to Sohu's business as a whole. Such changes can make the company sustainably profitable again and increase the share price by up to 3 times in my opinion.

As downside risks, I see the continued decline in sales of Sohu's brand advertising business. Additionally, a downside risk is the declining popularity of the company's most popular product, TLBB. Also, the lack of a clear long-term plan for the further marketing of the TLBB game. In addition to these downside risks, Sohu also has significant political risk.

If China does decide to attack Taiwan, it will likely lead to a sharp drop in Chinese stocks, similar to what happened to Russian stocks in February 2022. Also, the Chinese political leadership can expect regulations that hinder Sohu's business activities. Investing in a region with such a political background represents significant additional risk.

Conclusion

Since 2013, Sohu's business has gradually gone downhill. Since then, there have been significant changes in the proportion of business segments. While brand advertising used to have a large share in Sohu's sales revenue, today computer games are the main sales item. The company's most popular product, the computer game TLBB, has had mixed success. Although since 2017, sales of TLBB have increased significantly, based on the results of the last quarter, its popularity is declining due to so-called "natural aging". At this point in time, Sohu's business model does not work in my opinion, as the company has not been able to be consistently profitable for years. In addition, Sohu faces significant geopolitical risk due to Sino-Taiwanese relations and potential regulations from China's authoritarian government.

Although I currently hold a small amount of Sohu shares in my portfolio, my view on the company remains negative. If there are no positive results in the next three or four quarters, I will probably sell my Sohu investment.

For further details see:

Sohu: An Unsafe Investment With Declining Sales