SNDA - Sonida Senior Living: Lagging Peers Is A Turnaround Likely?

2023-05-02 08:43:28 ET

Summary

- Sonida Senior Living may be running into significant liquidity issues, announced at its last earnings.

- This, despite potentially strong core operations, according to management.

- Profit growth and return on equity has been drifting lower for several years, a hurdle to overcome.

- Reiterate hold.

Investment Summary

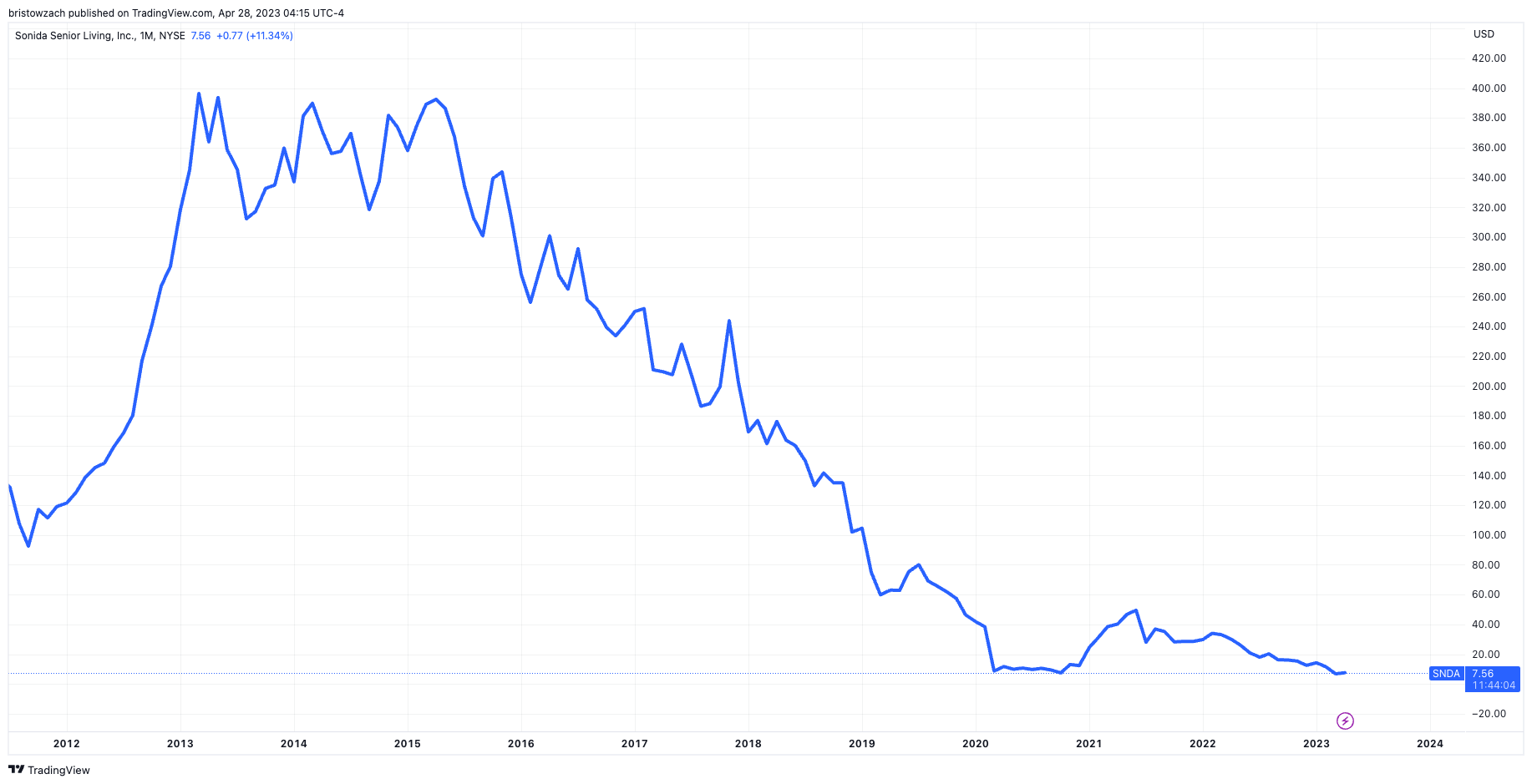

No change in the medium-term outlook for Sonida Senior Living, Inc. (NYSE: SNDA ) in my best estimation. Since the last time SNDA was covered, the company's market value has fallen 47% over a 4-month time period. Added to that, in its latest quarterly update SNDA also mentioned "there is substantial doubt about our ability to continue as a concern". This, added to the fact it missed the Street's conservative bottom-line estimates. Further, its cash on hand has plummeted 79% YoY to $17mm on the ledger. You can see the long-term value erosion in the chart below.

SNDA Equity Line

{kind=link}

The risk to its equity position is equally as potent. Investors have demonstrated in recent months the ability to force supply and drive market values toward the floor, even on a whisper of lost confidence. Here, I quantify the firm's lack of value-added for shareholders, unable to recycle retained earnings back into earnings growth. That, and the decline in operations and financial performance over the last 5–6 years. There is too much risk for this kind of special sits play in my playbook. However, there's plenty to consider nonetheless. I believe the market has correctly valued SNDA. Rate hold.

Broad sector is under pressure

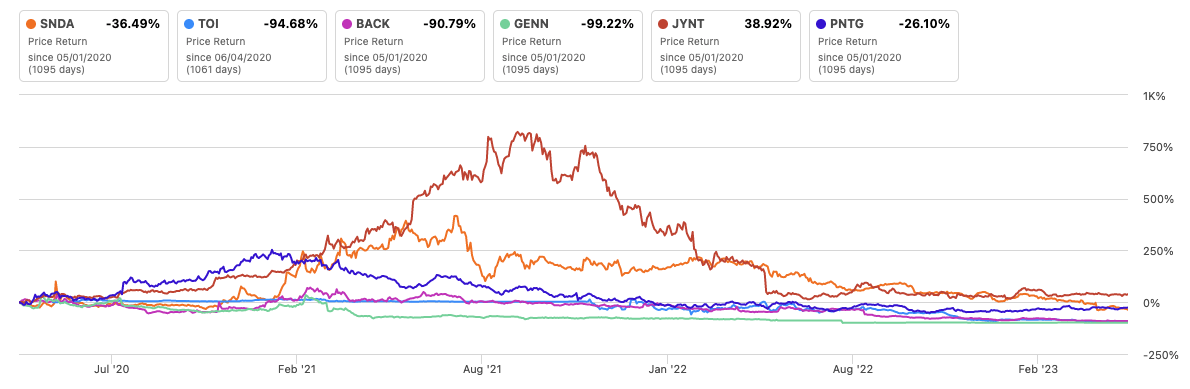

The pandemic and all of its economic symptoms were not kind to SNDA and its peers. The entire sector has remained under pressure since 2020, with no respite in sight. You'll note in Figure A.1, the price performance of SNDA and comparable peers has been woeful since April 2020 up to the present day. All but Joint Corp. ( JYNT ) has slipped into oblivion, with The Oncology Institute ( TOI ), Genesis Healthcare ( OTC:GENN ) and IMAC Holdings ( BACK ) down some 90–99% over this time. Aside from that, research published by GrantThornton in 2022 showed that U.S. senior living bankruptcies have increased substantially since the pandemic, up more than the previous 5-years combined.

Fig. A1

{kind=link}

Fig. A2

Data: Taken from GrantThornton, "Senior living sector slow to recover from COVID-19"

There must be an economic viability as to why the sector has struggled so much since the pandemic. Sectors that have remained profitable and generated positive returns on incremental capital have been rewarded over the same time, even when considering the 2022 selloff.

With respect to SNDA and peers, it's important to note that a number of factors are at play here:

- Firstly, and most notably, the major factor was the reduction in occupancy rates stemming from the pandemic and its subsequent policies. This is true for both living and medical facilities. For example, assisted living and independent living occupancy rates have slipped from 84.6% and 89.7% in 2019 to 81.4% and 85% in H2 2022 respectively. Although this wasn't tied to excess mortality due to Covid-19. research from NORC last year showed that 51% of U.S. senior living properties experienced no Covid-19 deaths in 2020.

- Increase in PPE costs as a result of heightened demand from the pandemic. These facilities have enormous PPE requirements as it is. The increase in unit costs hurt margin growth, and increased OpEx.

- Staffing has been a major factor, too. The typical staffing costs for managed living and medical facilities is ~60% of OpEx. Reimbursement rates are increasing slower than wage increases, and Covid-19 drove up labor rates as well.

- Related to the above, lower occupancy is tied to lower staffing rates. A recent American Health Care Association ("AHCA") survey found that 98% of all homes are finding difficulties in hiring staff. Service growth is difficult if this is the case.

- Profitability at the margin. It has been a profitless race to the bottom for many operators in the space. The same AHCA survey also found that ~90% of all U.S. nursing homes are operating at a 3% margin in 2020. This was driven by all of the factors above.

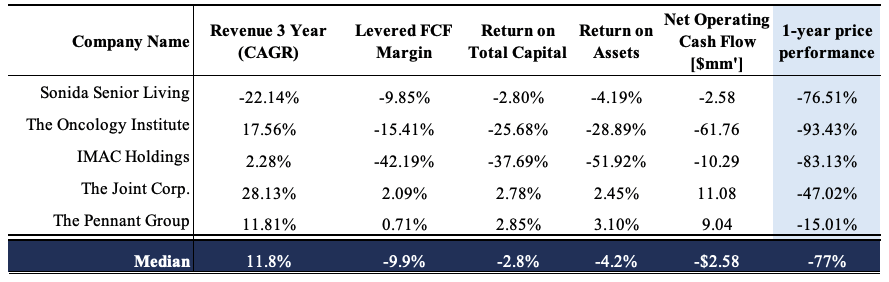

It is tremendously difficult for the SNDA's peers in the sector to catch a bid when top-line growth, FCF margins and returns on capital each fail to beat the benchmark. Looking at JYNT and PNTG, both has certainly fared the best out of the names shown below. Despite a difficult 1-year, this YTD both are up 17% and 29%, respectfully, with the others deep in the red. It doesn't take long to see that, each JYNT and PNTG have grown revenues consistently since 2020, are free-cash flow and operating cash flow positive, and each post low single-digit returns on capital and assets, respectively. However, these results still don't outperform the benchmark, nor are they shared with the remainder of the group.

Consequently, the combination of Covid-19 impacts hurting occupancy, increasing costs, compressing margins, that are driving profitability into the negatives, means returns in the sector have been sub-standard. These firms haven't generated a return on capital above the opportunity cost of capital, so investors are looking to put capital to work elsewhere. With these trends likely to continue, these future expectations have been baked into the stock prices of SNDA and peers, in my estimation.

Fi. A3

{kind=link}

Low probability, high risk

The company's stock saw a large supply following the going concern announcement. Swaths of sellers dropped their positions and price immediately dropped c.40% in reaction. Yet, this is a confusing case, because, on the Q4 FY'22 earnings call, CEO Brandon Ribar said:

Related to the overall stability of occupancy across our portfolio, nearly half of our owned communities were at or above 90% occupied for February and half of those were 95% occupied or more .

Further, when pressed about the issue of SNDA to continue operating, management also said:

So at this point, we have gotten the reservation of rights letter, but we are not in a formal event of default and we believe that we are having productive conversations with the lending group to address this and the broader debt composition profile overall. ..

...we do feel strongly that we are going to be able to move past this.

With respect to debt maturities:

July 1st of next year, there are 12 loans that are due under Fannie Mae.

There will be only a matter of time to see how this one plays out.

For those wanting to take on this kind of special situations theme then here are the factors for consideration.

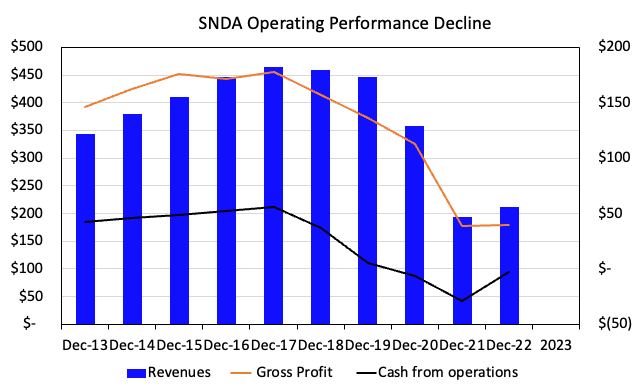

One, SNDA's operating performance has been pulling lower for at least 5-years now. With some respite in FY'22, there is a long road ahead, and the cash flow problems continue to be a pressing issue. Without the top-line growth, as seen in FY'13–17 below, it is difficult to foresee a major turnaround in profitability. This is further seen in the cliff gross profits rolled off over this same time. On $211mm in revenues last year ~$40mm came to gross profit. Both numbers are seeing less cash flow to back them up as well. Annually, cash outflows have increased to as much as $28mm in recent years. It would take ~$400mm in top-line revenues on ~$150mm in gross profit to see it get back to previous highs here.

In my opinion, it comes back to the top line. No growth at the top, no meat for us at the bottom. Looking forward, management are focused on SNDA's memory care product, Magnolia Trails, that saw 13% YoY growth last year. This was backed by two key drivers – 1) 7% occupancy increase, and 2) 500bps rate increase. Hence, a potential springboard to latch on to. But there needs to be more. More arteries feeding into the business pump in order to get moving once again. The cash preservation plan was discussed extensively on the Q4 call, but even this is difficult to contain with $625mm in long-term debt remaining, nearly 3x FY'22 revenues, many due next year.

Fig. 1

{kind=link}

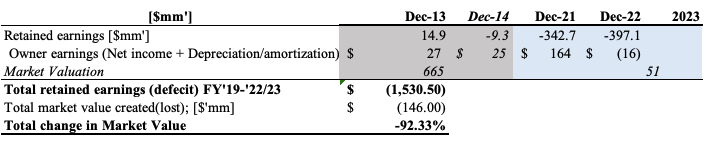

Two, a dollar in SNDA's hands has been less valuable than if it had returned the cash to shareholders since FY'15 at least. Consider the market's long-term average return of ~10–12%, SNDA hasn't generated value on the incremental capital it has invested. In fact, each dollar invested (using retained earnings) has actually related to a loss in market value for shareholders. The longer-term selloff in the company's earnings can be traced back to this, in my opinion. If you compare the retained earnings(deficit) over the long-term to SNDA's market cap, you can see they've both suffered heavily. There's been a 92% loss in incremental market value since 2013, otherwise $614mm, whereas the accumulated deficit has broadened to $1.5Bn.

The return it has generated on retained earnings has been negative, so it's a difficult task to convince investors to take that risk when there's drains and pulls on liquidity/cash. It hasn't created substantial value in this regard, and the market has not rewarded it's value by paying higher multiples. Even with the pessimism in its share price, the company still trades at 78x trailing earnings, and I doubt a flock of investors will be willing to pay $78 for every $1 in profits any time soon. You can see the accumulated deficit since FY'16 and the change in market cap below. It is not unreasonable to foresee these challenges continuing in the near future, into FY'23–24.

Alas, in my opinion, there is no mispricing in the market's value and the intrinsic value for SNDA. These are two important facts to consider in the SNDA investment debate. Not only are there liquidity and cash flow risks for the business, the ability to create value going forward is difficult to ascertain at this point. There is a hurdle to overcome, that is for sure. In my investment cortex, this doesn't match up with investing first principles.

Fig. 2

Owner Earnings in . (Data: Author, SNDA 10-K's)

Fig. 3 – Return on retained earnings, $146mm loss in total market value

Note: Market value is Market capitalization, measured in millions. (Data: Author, Seeking Alpha, SNDA 10-K's)

{kind=link}

Valuation and conclusion

There is little merit to see SNDA trade at a large discount to the sector at 0.23x sales. For example, the sector trades at 4.1x sales, and SNDA's 5-year P/S ratio is 2.47x. That SNDA is priced at a discount is self explanatory. Going back to Figure A3 at the beginning of this report, it is clearly observed that SNDA is situated below the peer median across all key measures. In particular, the negative 22% 3-year CAGR suggests to me that investors aren't paying a premium to the company's revenue expectations, and would expect a discount for this instead. Second of all, SNDA is priced at 78x trailing EBITDA, and this is miles above the sector's 15.7x comparable ratio. The disconnect is quite clear here. With absent revenue growth and lagging ROA, return on capital and FCF margin, it is understandable by SNDA would trade at a discount to peers.

Further, there's difficulty to appraise the assets for SNDA given the firm's capital has become less productive on an ongoing basis. There is less predictability of its future cash flows, meaning we will require more data after the liquidity adjustments are made across this year. Hence, 0.23x sales could be correct, but not a discount in my opinion. Even at that level, we are talking a valuation of $7.35-$7.50, about fair market value. Therefore, in my opinion the market has correctly priced SNDA correctly at its current levels.

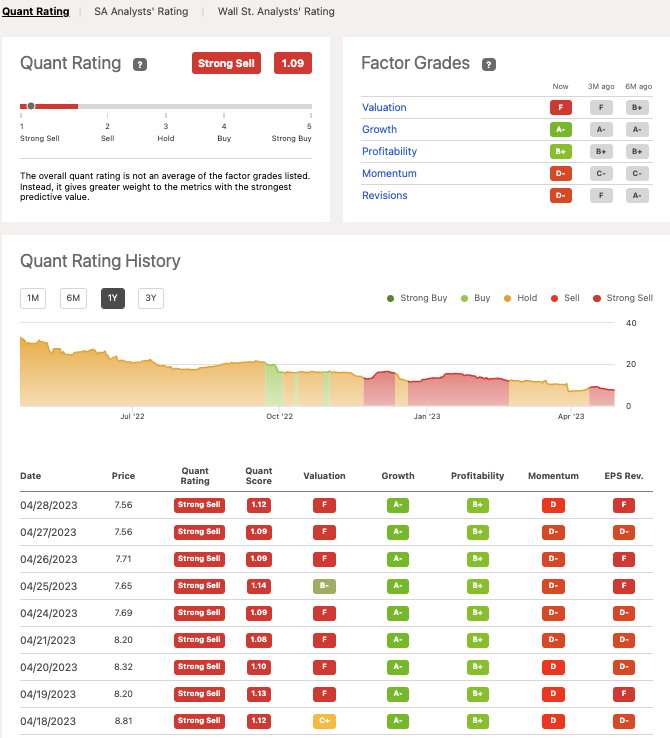

If there ever was a measure of sentiment, the quant system here on Seeking Alpha provides it. The system has been advocating SNDA as a strong sell, correctly capturing its gradual wind downwards. I believe these indicators provide an objective viewpoint by synthesizing loads of data into a very clear composite. It also suggests that valuation, momentum (the price investors are paying for SNDA to create value from retained earnings) and EPS revisions are weak [Figure 4], in support of the findings presented here today. It is difficult to see any future re-rating without significant revenue growth, in my opinion. Without a directional view on the market, I continue to rate SNDA as a hold. There is risk that operations could decline further, added to that, current valuations.

Fig. 4

{kind=link}

With these key facts on display, there is questionability on bullish sentiment looking forward. The firm's ability to create value over the next 3-years is unknown, beyond cash preservation measures. There is scope for SNDA to rate higher if it surprises at earnings time, that is certain. However, the instability in cash flows is not something I am willing to risk on. Net-net, reiterate that SNDA is a hold.

For further details see:

Sonida Senior Living: Lagging Peers, Is A Turnaround Likely?