SSTI - SoundThinking: A Financial Overview Margins Need To Improve Dramatically

2023-09-06 00:04:42 ET

Summary

- SoundThinking Inc. has seen a significant decline in its share price over the past 5 years, indicating a need for improvement in profitability.

- The company's main revenue generator is ShotSpotter, which detects gunshots and alerts law enforcement. Other products include CrimeTracer, CaseBuilder, and ResourceRouter.

- SoundThinking's financials show mixed results, with strong revenue growth, but unpredictable profitability and efficiency. The company lacks a competitive advantage and needs to improve operating margins.

Investment Thesis

I am going to take a look at SoundThinking's ( SSTI ) historical financials to see if there is potential for long-term investment at this share price, which is down over 60% in the last 5 years. The company's slowdown in revenue growth and contraction in margins tell me that the company still needs a lot of work to sort out its profitability. For new and current investors, I give it a “hold” rating until we see dramatic improvements in operating margins.

Briefly on the Company

The company recently changed its name to SoundThinking Inc. from ShotSpotter in April 2023. The company offers transformative solutions for law enforcement. Products include their main revenue generator ShotSpotter which detects gunshots in a certain mile radius and then alerts law enforcement to the location. The company makes around 70% of its total revenues from ShotSpotter, while CrimeTracer, which is a search engine for law enforcement to sift through a billion criminal justice records to generate leads and make connections, CaseBuilder, a management and reporting system, and ResourceRouter, which directs the resources of law enforcement efficiently, makes up most of the remaining revenues.

Financials

All the graphs below will be as of FY22 because I like to look at the overall long-term trend rather than fluctuating numbers q-o-q. I will include some numbers from the most recent quarter for extra color if needed.

As of Q2 ’23 , the company had around $4m in cash, which was reduced from around $10.5m at the end of FY22. The company has no debt on its books so that is a good position to be in. The company is more flexible in how it can operate on a daily basis, how to put the operating cash flow to use, and the cash on hand for further expansion and growth.

The company's current ratio is a little bit on the lower side of my liking. I like to see companies be in the range of 1.5-2.0. SSTI had around 0.8 at the end of FY22 and .73 at the end of Q2 '23, which is even worse. Most of the company’s current liabilities come in the form of short-term deferred revenue, which is revenue not recognized yet because of the subscription-based business model. It is common to see such revenues in subscription-based models because the customer may have paid for the whole year of services and the company still has an obligation for the whole year. In my opinion, the current ratio below 1 here is not a problem because the unearned revenue will be earned later in the year.

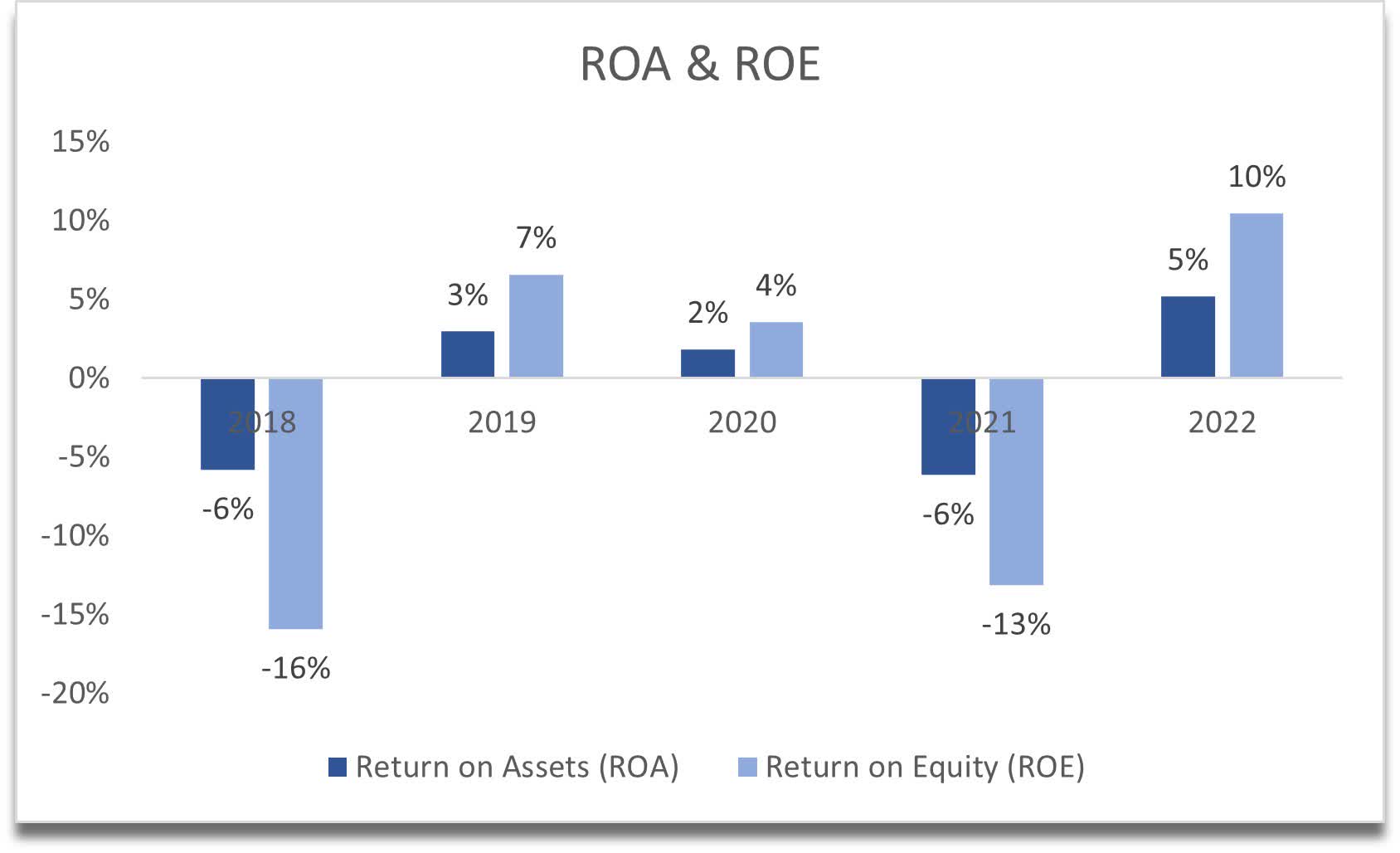

In terms of efficiency and profitability, the company's ROA and ROE have been very unpredictable over the last 5 years and no clear trend is apparent. At the end of FY22, the company did manage to reach my minimum for ROA of 5% and ROE of 10%, however, I'm not sure how likely the company will continue to perform like this given the company in the first half of ’23 is already in an operating loss. The management needs to utilize the company’s assets and shareholder capital more efficiently in the future.

{kind=link}

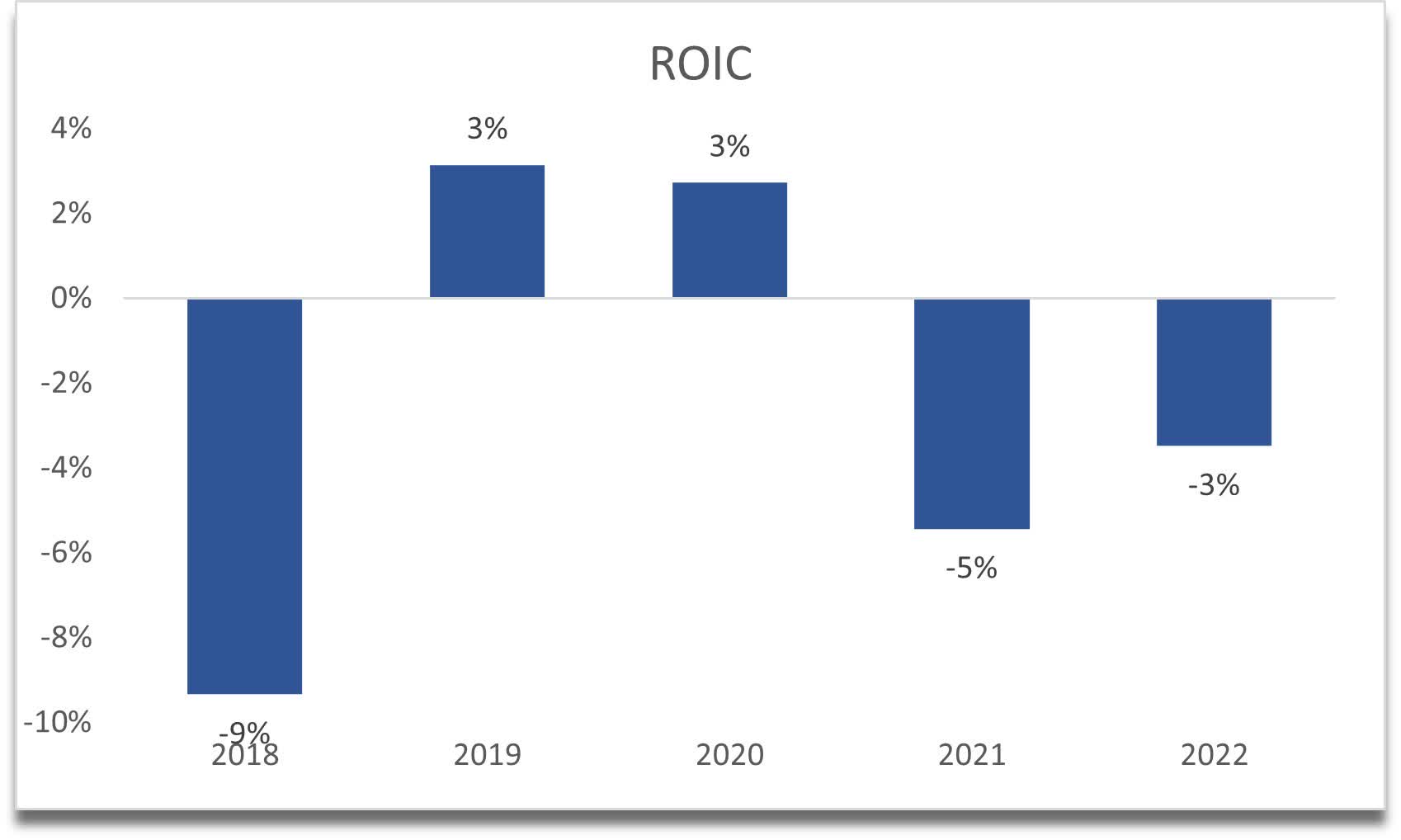

The company’s competitive advantage or moat is non-existent. I am looking for at least a 10% return on invested capital and SSTI in the last 5 years only had 2 positive returns, so this tells me that the company does not have any competitive advantage or a strong moat.

{kind=link}

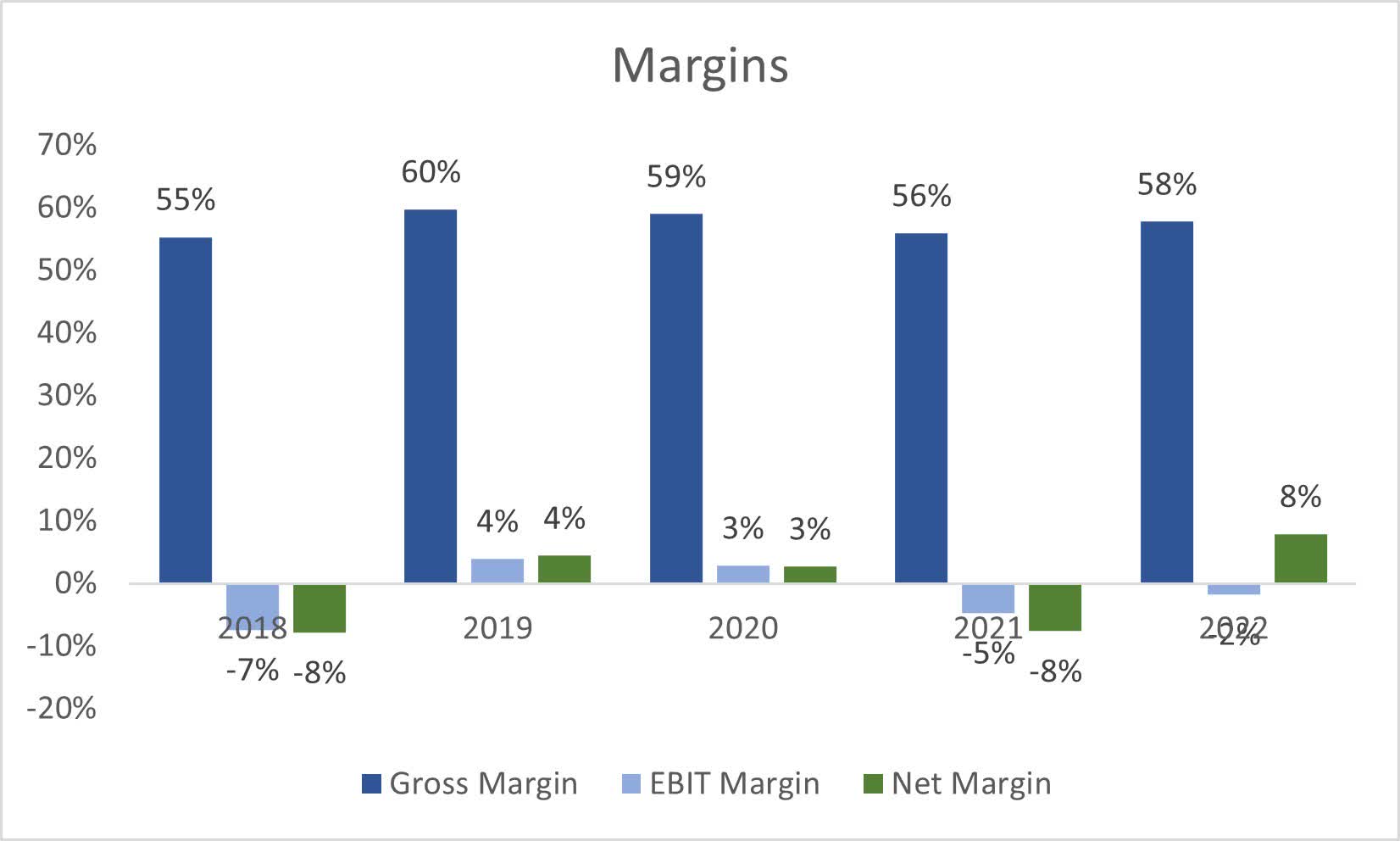

In terms of margins, gross margins are decent, however, the company’s operating margins need a lot of improvement. Sales and marketing and General and administrative make up the bulk of operating expenses. The management attributes this explosion in operating expenses to a higher number of employees compared to the same quarter last year. I would like to see personnel costs coming down in the future, but it is hard to tell whether they will, as I did not see any indication in the transcripts.

This is the most crucial item for my valuation analysis because if the company cannot tame operating expenses considerably, the company is going to burn through its cash reserves quickly, and will have to take on debt to keep operating, which they have $25m available from its credit facility, but that wouldn't be ideal in my opinion.

{kind=link}

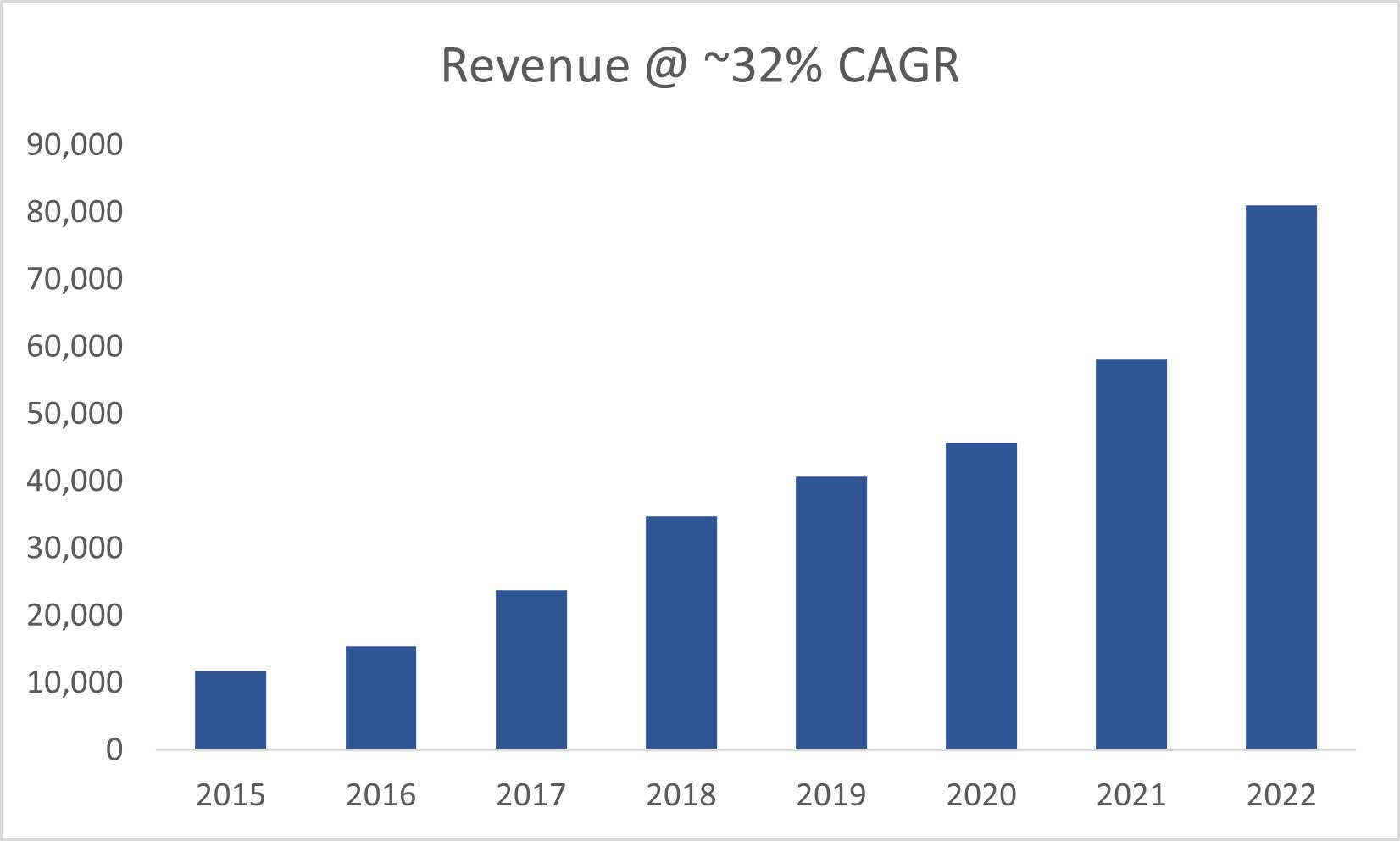

Speaking of revenue, the company has experienced very respectable growth over the last while, growing at around 32% CAGR since 2015. The management in the latest transcript guided for the full year to be at around $92m in revenues which translates to around 14% revenue growth. That is quite a bit lower than historical growth, which makes me a little worried about future estimates and how optimistic I can be in my model.

{kind=link}

Overall, the company’s financials are a mixed bag in my opinion. I don’t see a clear trend in profitability or efficiency, but I do see that the revenue growth in the past has been very strong, with what I hope is only a hiccup in FY23. Let’s see what an enticing risk/reward for me would be.

Valuation

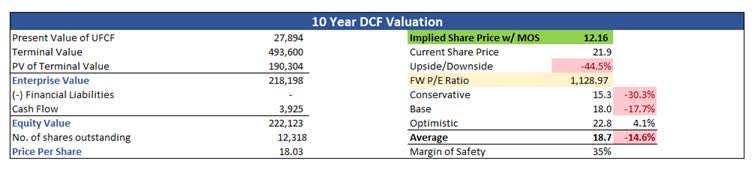

If the company didn't guide such low revenue growth in FY23, I wouldn't have had a tough time growing the company's revenues in the mid-20s, however, now I don't think I can do that, so for my base case scenario, I went with an 11% CAGR for the next decade. For the optimistic case, I went with 15% CAGR, while for the conservative case, I went with 9% CAGR. These may be on the conservative side; however, I would need to see what kind of revenue growth the company will be able to achieve next year to see if the high number of growth returns.

In terms of margins, I was more generous here. The company cannot operate on a constant loss for a long time, so I decided to improve gross margins by around 500bps or 5% over the next decade while improving operating margins by around 20% in the next decade. My reason is that the company will have to tone down on the mentioned operating expenses to become profitable, and I believe the company is being aggressive right now because it is in that expansion phase, which will stabilize over the next 10 years.

But since I don’t know how well this is going to work for the company, I will add a 35% margin of safety to my final calculations to give me some breathing room. With that said, SSTI’s intrinsic value is around $12.16 a share, which implies that the current share price is too expensive for me and does not offer a good risk/reward with so many unknowns in the margins area.

{kind=link}

Closing Comments

Even with what I consider to be quite an optimistic outlook on margins in the future, the company is a bit overvalued right now and does not offer a good risk/reward for me. The company does have a really promising product that saves lives, and I believe that it will succeed in the future, now that AI is also in the mix these days, I can see how the product can be enhanced even further going forward. However, if the management is not able to tame operating margins in the next couple of years, I don’t think it is a good time to invest right now and would wait for a clear trend in how the company is operating. I would like to see improved profitability and efficiency metrics, and also revenue growth to come back into the 20s before I consider investing.

The company has a lot of growth potential as it still covers a very small area of the US and internationally, so I will be looking for those revenue numbers to continue to grow at a faster pace if the product is essential in law enforcement and safety areas in the future.

For further details see:

SoundThinking: A Financial Overview, Margins Need To Improve Dramatically