UGIC - Southern Company: The Pros And Cons Of A Stock And Bond Investment

2023-12-21 09:00:46 ET

Summary

- As bond yields have been in free fall since the beginning of October and the Fed Chair Powell pivot has become a reality, The Southern Company stock has recovered strongly.

- However, its notoriously high maintenance capex, substantial leverage and aggressive capital spending plan raise the question of whether there is any room for shareholder returns.

- In this update, I will take a fresh look at Southern Company's fundamentals, focusing on the company's leverage, debt maturity profile, and dividend growth prospects.

- Given that utilities are typically appreciated among (retired) income investors, I'll share my thoughts on whether I currently consider Southern Company stock a better investment than long-term government and corporate bonds.

Introduction

The Southern Company ( SO ) and Duke Energy Corp. ( DUK ) are the only regulated utilities I have in my portfolio, primarily because I consider them to be among the best, if not the best, in terms of long-term management and presence in a constructive regulatory environment. I have covered both SO and DUK in the past here on Seeking Alpha, but have not added to my positions in a long time due to valuation concerns.

As is well known, Southern Company is in the midst of an aggressive transformation towards becoming a net zero greenhouse gas emission energy supplier by 2050, and that comes at a huge cost. Given this, the notoriously high maintenance capex of utilities in general, and the significant leverage, it's worth asking whether there is still room for adequate shareholder returns. At the same time, knowing that it is usually risk-averse and income-oriented investors like myself who are attracted to utility stocks, I will explore the question of whether SO stock is now a better investment than long-term government and corporate bonds, given that the Fed Chair Powell pivot has become reality .

Still Room For Shareholder Returns Amid The Expensive Transformation And High Debt?

Starting with Southern's balance sheet , I've always been a bit concerned about its high leverage. Of course, this is by no means a company-specific phenomenon, but still - high leverage is one reason why utilities (see my bearish article on the Utilities Select Sector SPDR® Fund ETF, XLU , from February) have performed so poorly until the bond rally started in October. That said, Southern deserves special mention in connection with the high leverage stemming from the considerable maintenance capex and the investments in alternative forms of energy. The cost overruns at the Vogtle Units 3 and 4 nuclear power plants (see my last article ) are well known, and longer-term investors may remember the disaster at the Kemper natural gas combined cycle power plant . The Kemper project ended up with cost overruns of more than 150% of estimates , and the construction and financing costs for Vogtle exceeded $34 billion in 2023. That's $9 billion more than the 2018 estimate, and keep in mind that work on Units 3 and 4 began back in 2009. Originally, Vogtle Units 3 and 4 were expected to cost $14 billion .

Let's take a look at how Southern's financial situation has evolved over the years.

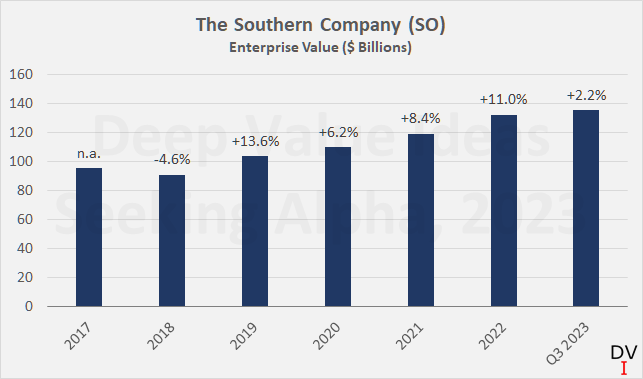

Southern's enterprise value (Figure 1) has increased significantly since 2017 with a CAGR of 6.2%, compared to a CAGR of 5.9% for SO's share price. Net debt increased at a CAGR of 4.7% (from $45 billion in 2017 to almost $60 billion at the end of the third quarter of 2023) and diluted shares outstanding increased at a CAGR of 1.5%. However, operating cash flow ((OCF)) remained practically flat between 2017 and 2022 - at around $6.3 billion. OCF for trailing twelve months period improved ($7.0 billion), but at the same time capital expenditures were also higher - $9.0 billion compared to $7.9 billion in 2022.

Figure 1: The Southern Company (SO): Enterprise value, based on the average share price over the period (own work, based on company filings and the closing price of SO)

{kind=link}

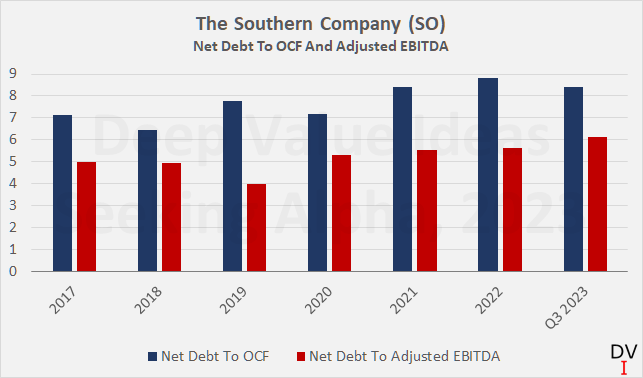

Putting earnings and cash flow in relation to net debt shows that leverage has increased over the years (Figure 2), leading to increasingly weak debt servicing capacity, especially against the backdrop of higher interest rates. No wonder Southern Company's stock performed poorly in 2023, but rebounded strongly when long-term bonds rallied in early October. Following Powell's dovish comments, the market is increasingly anticipating rate cuts in 2024. Keep in mind, however, that the main reason for rate cuts is to stimulate economic growth in the midst of a recession. In such times, companies with reliable earnings tend to outperform cyclical stocks, so this is likely to have also played a role in the recent bid for utility stocks. That said, I doubt that the Federal Reserve will squander its hard-earned firepower lightly and be wary to cut back at the first sign of a recession.

Figure 2: The Southern Company (SO): Leverage ratio – net debt to operating cash flow (OCF) and net debt to adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) (own work, based on company filings)

{kind=link}

But what if interest rates are not cut in 2024 and we find ourselves in a "new normal" - which is actually the old normal that many seem to have forgotten in the years following the Great Recession. Long-term interest rates of 4% are not really high from a long-term historical perspective. Therefore, I deem it necessary that every company in my portfolio can service its debt if long-term interest rates remain at 4% in perpetuity (and I don't think that's overly conservative).

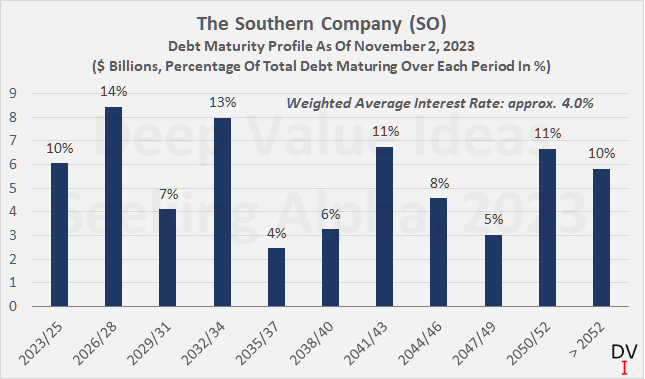

Southern's longer-term bonds are currently trading at a premium of around 130 basis points over the 10 year Treasury. According to Southern's current maturity profile (Figure 3), around 25% of its debt matures in the next six years. As the company does not disclose the interest rates on its bonds in its annual report, it is impossible to perform an accurate interest rate sensitivity analysis. However, assuming that all outstanding bonds have a coupon rate identical to Southern's weighted average interest rate of 4.0% (slide 13, 2023 Q3 presentation ), a (rough) back-of-the-envelope approximation can be made. It is also known that Southern's exposure to floating rate bonds (weighted average interest rate of 5.1%) is about 10% of long-term debt, so I have also accounted for this in the sensitivity analysis.

Figure 3: The Southern Company (SO): Debt maturity profile as of November 2, 2023; carrying amounts (own work, based on company filings)

{kind=link}

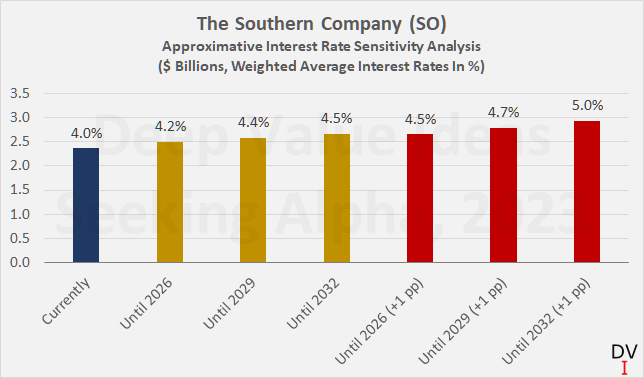

The results are shown in Figure 4 and should be read as follows. The blue bar shows Southern's estimated current gross interest expense, and the yellow bars show how interest expense (and the weighted average rate) would increase if long-term interest rates remain at current levels for another 3, 6 or 9 years. Similarly, the red bars show what happens if interest rates increase by 1 percentage point and remain at that level for the specified number of years.

Figure 4: The Southern Company (SO): Approximative interest rate sensitivity analysis (own work, based on company filings)

{kind=link}

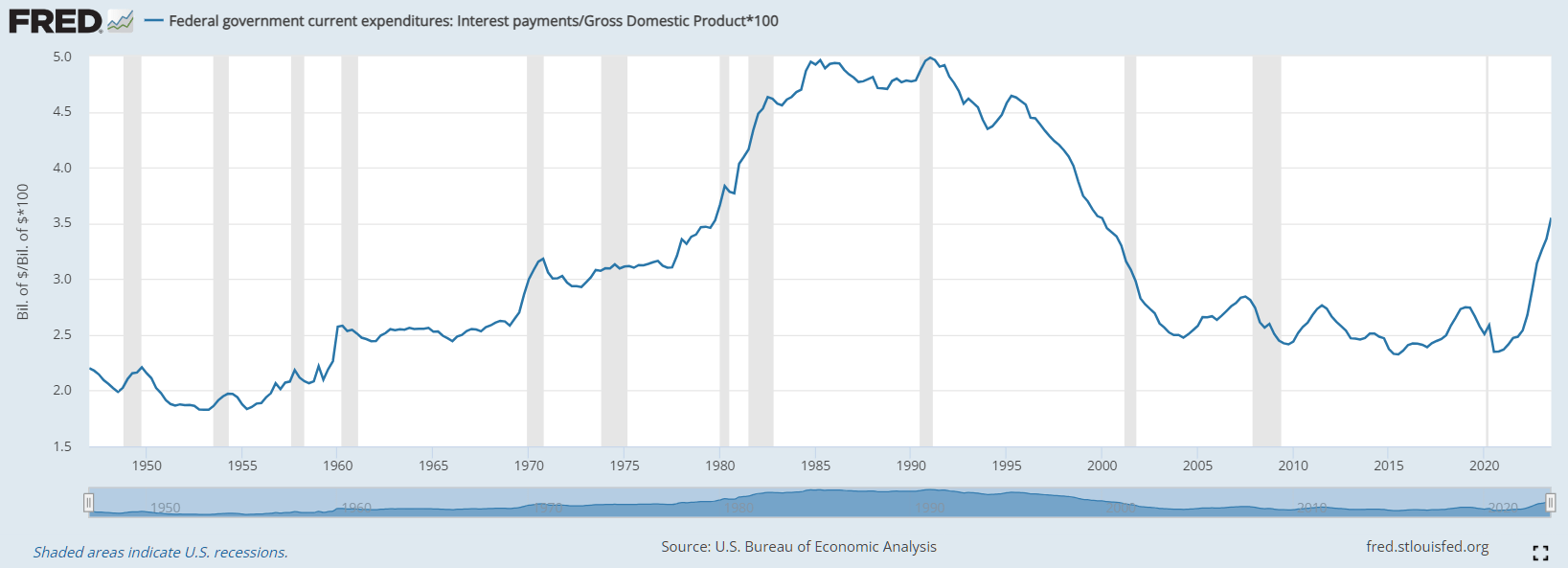

To put the results into perspective, Southern's interest coverage ratio - currently 4.5 and 4.8 times operating cash flow and adjusted EBITDA respectively - would fall by 5 to 20% in these scenarios. This decline in the interest coverage ratio would be manageable, in my view, and I would also like to emphasize that I consider the scenarios represented by the red bars in particular to be very unlikely. On the one hand, it can be assumed that the U.S. government will willingly accept a slightly higher average inflation rate due to the devaluation effect on debt; on the other hand, one should bear in mind the historically high level of government debt (Figure 4) and the resulting limited room for maneuver.

Figure 5: U.S. interest expense in percent of GDP, A091RC1Q027SBEA/GDP*100 (U.S. Bureau of Economic Analysis, retrieved from FRED, Federal Reserve Bank of St. Louis)

{kind=link}

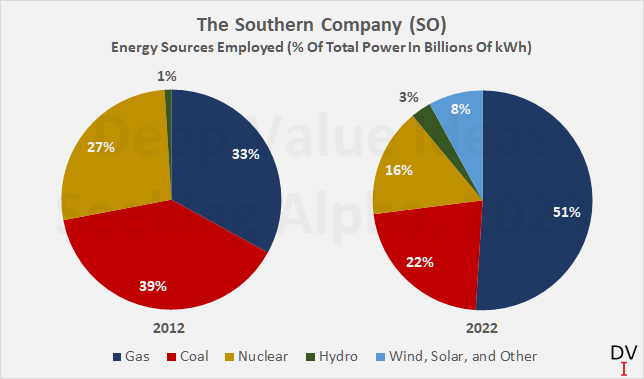

In addition to the headwinds arising from a potential "higher for longer" scenario, Southern's capital investment plan should also be noted (slide 15, 2022 Q4 presentation ). Management expects to invest around $43 billion in the period 2023-2027. Approximately $23 billion is earmarked for work to improve grid reliability and resilience, and to upgrade and replace pipelines. About $19 billion will go toward Southern's clean energy and renewable energy portfolio (e.g., wind, solar and renewable natural gas). I don't want to be misunderstood as an opponent of solar and wind, but I have concerns about their low EROI (energy return on energy invested), the risk of impairment charges (think of the $1.3 billion write-down at Duke ) and their service life and maintenance expenses. I think they make sense in a diversified portfolio, but I appreciate companies taking a balanced approach and adopting new technologies gradually and as they mature. Therefore, I continue to monitor Southern Company's energy mix and appreciate the fact that more than 50% of kilowatt-hours generated come from gas-fired plants, while the contribution from "renewable" forms of energy is still only 8% (Figure 5).

Figure 6: The Southern Company (SO): Energy sources employed for power generation - 2012 vs. 2022 (own work, based on company filings)

{kind=link}

Taken together, Southern Company, like most (if not all) utilities, finds itself in a difficult environment. The comparatively high interest rates are putting pressure on profitability as upcoming notes need to be refinanced and this aspect will be particularly relevant if interest rates remain elevated, contrary to current expectations. Combined with the ambitious investment plans, I do not see a clear path to high shareholder returns. However, with Unit 3 of Vogtle coming on stream earlier this year and Unit 4 scheduled for early 2024, it is reasonable to assume that earnings growth will improve at least somewhat going forward. Similarly, consider that Southern operates in states with a comparatively constructive regulatory environment, leading to rather good returns on equity (all else being equal), as I examined in my comparative analysis of several utilities .

My base case scenario is that investors will have to be content with a continuation of the $0.08 annual dividend increase for the foreseeable future. If long-term interest rates bottom out at around 3.0% and Southern doesn't suddenly start aggressively investing in low EROI energy assets, I can envision a slow and steady improvement in earnings growth and thus dividend growth.

Let us now look at how an investment in Southern Company stock compares to an investment in long-term bonds.

Southern Company Stock Versus Long-Term Bonds – Pro Versus Contra

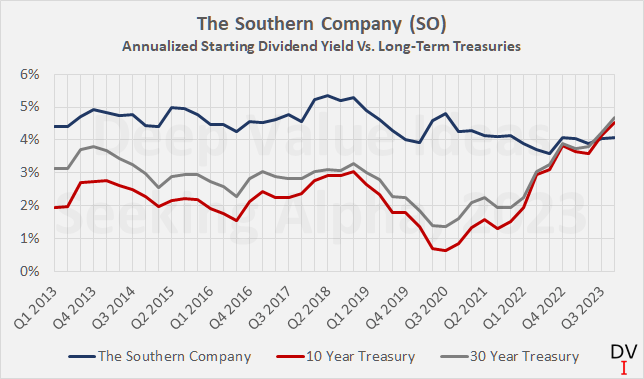

If we compare the starting yield on Southern Company stock with the current yield on long-term government bonds (Figure 7), we see that for the first time in over a decade, de facto risk-free bonds had a higher starting yield than SO shares. But does this automatically make them a better investment today?

Figure 7: The Southern Company (SO): Annualized starting dividend yield versus yield on 10 and 30 year Treasuries, based on quarterly average yields (own work, based on company filings, SO daily closing price, and Treasury data)

{kind=link}

Aside from the dividend/bond yield, it's worth noting that coupon payments from a (government) bond investment are typically taxed at a higher rate (assuming the investor is U.S.-based). As a foreign investor, this aspect is of no concern to me as the taxes on dividends and coupons are identical for me.

Then there is the reinvestment risk to consider. With bonds, the investor must reinvest the proceeds at maturity. What if we find ourselves in another period of zero interest rates in ten years' time? In contrast, equities do not mature and there is no contractual right to repayment, only a residual claim on the company's assets. So while equity investors do not need to consider reinvestment risk and can theoretically benefit from perpetual dividend payments (and of course capital gains) - assuming operating fundamentals remain intact - they do need to consider the (theoretical?) risk of a "higher for longer" scenario. If interest rates are significantly higher in ten years' time, investors in SO stock are likely to find their dividend yield somewhat disappointing. I explained the concept of bond duration in a separate article , in which I also applied it to equities.

From a yield perspective, and ignoring the tax aspect, a retired investor (or other investor who relies on the income) might take comfort in the fact that there is a contractual right to coupon payments. Dividends, on the other hand, are a discretionary payment by the company. The risk of a dividend cut should always be considered, even for companies with a decades-long track record of increasing dividends and a seemingly infallible business model.

Take the example of UGI Corporation ( UGI ). The company has paid dividends on its stock for 139 consecutive years (yes, the company started paying a dividend in 1885 ), and its most recent uninterrupted growth record spans 36 years . While the company has not yet announced a cut, the underlying fundamentals have deteriorated significantly, and with a current yield of 6.4% ( five-year average 3.6% ), the market is likely pricing in a cut. Also worth mentioning is the recent refinancing of the 5.625% 2024 notes issued by AmeriGas (a subsidiary of UGI) at an interest rate of 9.375% and a term of five years.

However, before going too much into the pros and cons of dividends, let me refer you to a separate article I wrote not too long ago explaining why I continue to focus on dividend (growth) stocks, despite the currently comparatively high bond yields.

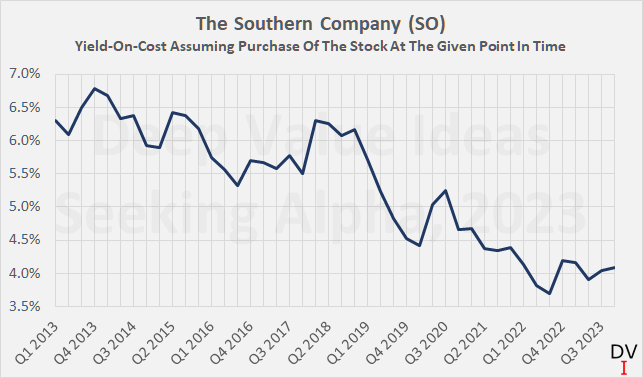

Turning back to Southern Company, Figure 7 only tells half the story, of course, because the dividend has grown over time (3.6% CAGR since 2013), resulting in a higher yield-on-cost for long-term investors. According to Figure 8, an investor who bought Southern Co. stock in 2013 currently benefits from a 6.2% to 6.7% yield-on-cost, but that is of course the gross yield, and inflation must be factored into the equation.

Figure 8: The Southern Company (SO): Yield-on-cost assuming purchase of the stock at the given point in time (own work, based on company filings, SO daily closing price, and Treasury data)

{kind=link}

I don't think the high single digit inflation rates we saw in 2022/23 should be considered the "new normal," but factors such as chronic underinvestment in fossil fuel supply post shale boom and a trend towards deglobalization are the key drivers of a "higher for longer" inflation scenario. Against this backdrop, consistently growing dividends (besides TIPS , but keep in mind the reinvestment risk) are the only way to protect one's income from inflation. Conventional bonds with a fixed coupon that matches the inflation rate during the holding period, on the other hand, serve only one purpose - preserving the purchasing power of the principal. I also discussed this aspect in the article linked above.

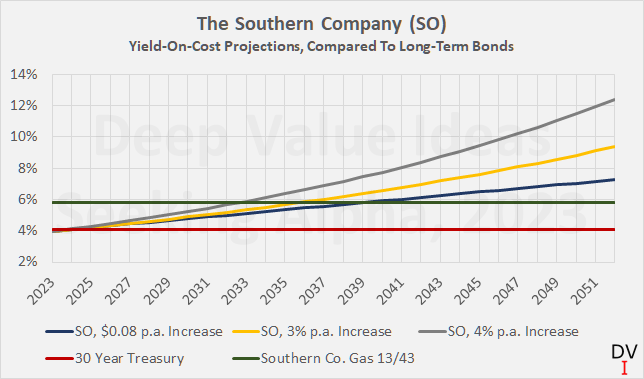

Figure 9 shows the yield-on-cost of Southern Co. stock purchased today after a given period and assuming that the company can increase its dividend by $0.08 each year (blue line), 3% per year (yellow line) or 4% per year (gray line). At current interest rates, the 30 year Treasury (red line) is a comparatively poor investment from an income investment, assuming Southern's operating fundamentals remain intact.

Of course, this does not take into account credit risk, and I acknowledge that it is more appropriate to compare the yield on SO stock to a corporate bond with a similar long-term rating (currently Baa2 with positive outlook ). Of course, a 1:1 comparison is not possible due to the bondholders' generally senior claim on the company's assets. So for example, the yield on Southern Company Gas Cap. Corp.'s 16/46 notes (rated Baa1 , green line in Figure 9) is 170 basis points higher than that of the 30 year Treasury, and investors in SO common stock would have to wait between 10 and 16 years for their yield-on-cost to exceed the fixed yield-to-maturity on the bond.

Figure 9: The Southern Company (SO): Yield-on-cost of the stock at a given dividend growth rate compared to bond yields (own work, based on company filings, SO daily closing price, Treasury data, and SCGC’s 13/43 yield)

{kind=link}

In addition, an investment in the bond would have generated significantly higher near-term cash flow. If Southern is only able to increase its dividend by $0.08 per year, an investor in SCGC's 16/46 notes would generate significantly higher cash flow ($13.9k vs. $12.7k) over the holding period with less risk (market- and credit risk wise). Southern would have to increase its dividend by more than 3% per year for the cumulative dividend income to exceed that of the bond over its remaining term. But of course it is the cash flows in later years that make the equity investment more lucrative - in 2046, the bond investor has to reinvest the proceeds at a potentially lower interest rate, while the equity investor benefits from a yield-on-cost of 6.6% to 9.8%, depending on the scenario.

That said, if I put myself in the shoes of a retired investor, I can see the appeal of a long-term bond like SCGC's 16/46 notes - strong cash flow, contractual right to coupon payments, lower volatility of principal and lower credit risk.

Conclusion

Southern Company is undoubtedly one of the better managed utilities and operates in comparatively favorable jurisdictions in terms of regulation. However, the massive cost overruns at Vogtle Units 3 and 4 (the latter of which has yet to be commissioned) are a stark reminder that utilities are not necessarily the low-risk investments they are often touted to be. Similarly, the constant need for investment - particularly in light of the push towards net zero by 2050 and the notoriously poor EROI of wind and solar - is a strong argument for critically questioning the shareholder return prospects of utilities. Moreover, should a "higher for longer" interest rate environment materialize, Southern Company's ability to service its debt will be significantly impacted. However, and assuming a balanced approach towards investments, I think the company will be able to continue to pay its dividend even in such a scenario.

Knowing that the Vogtle waiting game will come to an end very soon, it is reasonable to expect a return to a slightly more meaningful dividend growth rate. However, if I put myself in the shoes of a (retired) income-oriented investor, I can understand the attraction of the higher coupon payment on bonds with a similar credit rating to SO (yield difference of >170 bps). Over the next 20 years, the cumulative cash flows from such a bond investment are likely to be higher than the cumulative cash flows from SO dividend. Lower volatility of principal, a contractual right to coupon payments and to repayment of principal at maturity are further arguments to consider.

However, I think this line of thinking only applies to a hypothetical investor with immediate cash flow needs and a rather limited investment horizon. As long as Southern's operating fundamentals remain intact, I believe investing in the stock is the better choice for investors with a long-term horizon, such as myself. For this reason, and because the Vogtle Unit 4 commissioning is imminent, I will hold on to my modest position in SO stock, knowing that my dividend cash flows are (at least partially) protected from inflation-driven erosion of purchasing power.

Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

For further details see:

Southern Company: The Pros And Cons Of A Stock And Bond Investment