SPAB - SPAB: Fed's Comments Are Dovish But Bearish

2023-12-26 06:04:19 ET

Summary

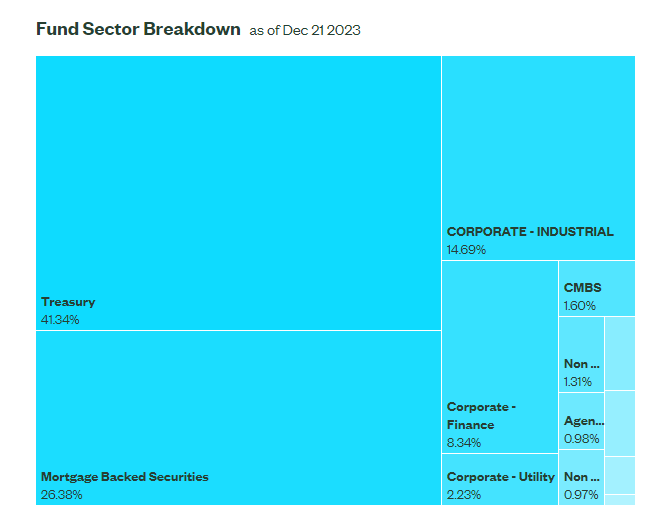

- The SPDR Portfolio Aggregate Bond ETF has a high duration and includes treasuries, MBS, and corporate bonds.

- The Fed is focused on labor market dynamics and improving supply-side data, indicating a shift in focus to the growth mandate.

- Powell acknowledges the stickiness of inflation and believes there are still supply-side issues that need to be resolved.

The SPDR® Portfolio Aggregate Bond ETF ( SPAB ) contains a quite high duration of substantially treasuries but also MBS' and corporate bonds. It appreciated a lot on the basis of the Fed's dovish pivot in the last Powell's remarks. We go over our meeting comments, and why we think that the dual-mandate is kicking in now, with the Fed policy reflective less about "success" in the inflation battle and more about economic concerns. While we still think inflation will be stickier, it's more reasonable to believe at this point that the Fed's ceiling on rates has come.

Comments on Powell's Remarks and Q&A

Having read the full Powell remarks transcript , it's worth sharing some comments on what has been said.

- The Fed is focused on the fact that labour market dynamics seem to be coming back to more normal pre-pandemic levels, with increases in participation matching jobs and payroll growth as well as low unemployment. Supply and demand for labour are strong and in balance, leading to a good outcome for the economy. Additionally, the Fed is focused on the fact that a lot of supply-side data has improved, which we expected over time.

- Another remarkable thing is that Powell acknowledges fully that there could be lags in the effects of the policy on the economy, and therefore just as things might get tighter without further rate hikes, they also need to start loosening before the inflation target of 2% is hit otherwise they'll overshoot. While this is fairly intuitive, it is quite bearish since they have demonstrated that they are taking the inflation mandate very seriously as well. Splitting fire means the economic concerns might be substantial.

- This may signal that they are more urgently considering the growth part of the dual mandate now. The economy is decelerating, and may continue to see mounting pressures even after the Fed starts reversing.

- Another really interesting point is Powell's comment on the stickiness of inflation. He actually states that he doesn't believe that inflation is in its last mile yet and that there are still supply side issues that need to be resolved. This is a bit surprising considering that supply side issues are in the rear-view in most of our coverage universe. In other words, the Fed believes there are still low hanging fruits to be achieved on the supply side, although he's not sure about how much more the labour supply can grow at this point. Honestly, we don't see much evidence that there is still a ways to go in supply loosening on the goods side at least. Possibly the end of the Ukraine war which still has some effect on ease of export of basic materials and grain.

- Another element on anchored expectations is that Powell feels that the expectations anchored into 2026 and so forth demonstrate a pretty good curve, and that expectations, at least those that matter are still anchored at 2% levels, but just not for a couple of years. We are still concerned about shorter term expectations and feel that they can become the new normal quite easily, and that those 2026 expectations and forecasts don't matter and are a weak argument that inflation is under control.

- Our outstanding concerns are around expectations and shorter term anchoring. We actually do think inflation will prove sticky and this might trounce expectations. However, we acknowledge that if the Fed sees that the data points to genuinely somewhat more restrictive conditions, and with more effects in the pipeline, they probably haven't jumped the gun or succumbed to pressure especially as there isn't much pressure on them in terms of the current economic data, even though this may be leading some pain.

Bottom Line

The key matter is that the growth mandate is kicking in. It does matter after all, the expectations are showing a pretty meaningful deceleration in US growth. There is also likely attention to the US public finances being paid, although that isn't strictly part of the mandate but related. All this indicates a ceiling is likely here.

SPAB is above 6 years in duration , meaning it's sensitive to these rate revisions. Credit quality is high thanks to meaningful Treasury exposures.

{kind=link}

The ETF has appreciated around 10% on the recent revisions to longer-term rates, which have come down quite quickly on account of Fed dovishness. The ETF's expense ratios are low, and we think that a higher duration bet makes some sense now. While there may be outstanding risks around inflation, which may cause speculation against the extent of the pivot, the fact that markets had priced in rate hikes substantially before the remarks and that markets have been a little inconsistent since does reflect a possible growing concern around economic fundamentals. Balancing the dual mandate means we are probably at that ceiling, and that the margin to get it high this far is owed to US hegemony and leverage to roll with the punches following the Ukraine war and associated supply shocks.

Whether what's in the pipeline in terms of rate effects actually causes a recession on its own is not something we're sure of, especially as money velocity and positive anticipation likely softens the effects of decreased availability of money.

While duration bets like SPAB may not have too much downside from these levels, if inflation is sticky high returns are going to be needed beyond what can be offered by non-opportunistic fixed income. We think the play continues to be Japanese equities where many opportunities still haven't re-rated, and try take an uncorrelated approach as uncertainties are still high. There is still the possibility of less rate cuts than expected, or even rate hikes, depending on whether continued progress on inflation is actually made, and whether expectations may limit the downstream benefits of a more balanced labour market.

For further details see:

SPAB: Fed's Comments Are Dovish But Bearish