DALXF - Spartan Delta: One Of The Best Growth Stories You Probably Have Not Heard Of

2023-12-18 01:44:01 ET

Summary

- Spartan Delta operates in the low cost Duvernay basin that is shallower than most other US basins.

- DALXF has acquired 130,000 acres that are located in a liquids-rich window of the Duvernay basin.

- Transitioning the company's production profile from predominantly natural gas to predominantly liquid stands to dramatically boost margins and earnings.

- I view Spartan Delta as a small-cap stock with extremely high growth potential.

Thesis

NOTE: DALXF or SDE:CA is a Canadian company traded on the Toronto Stock Exchange.

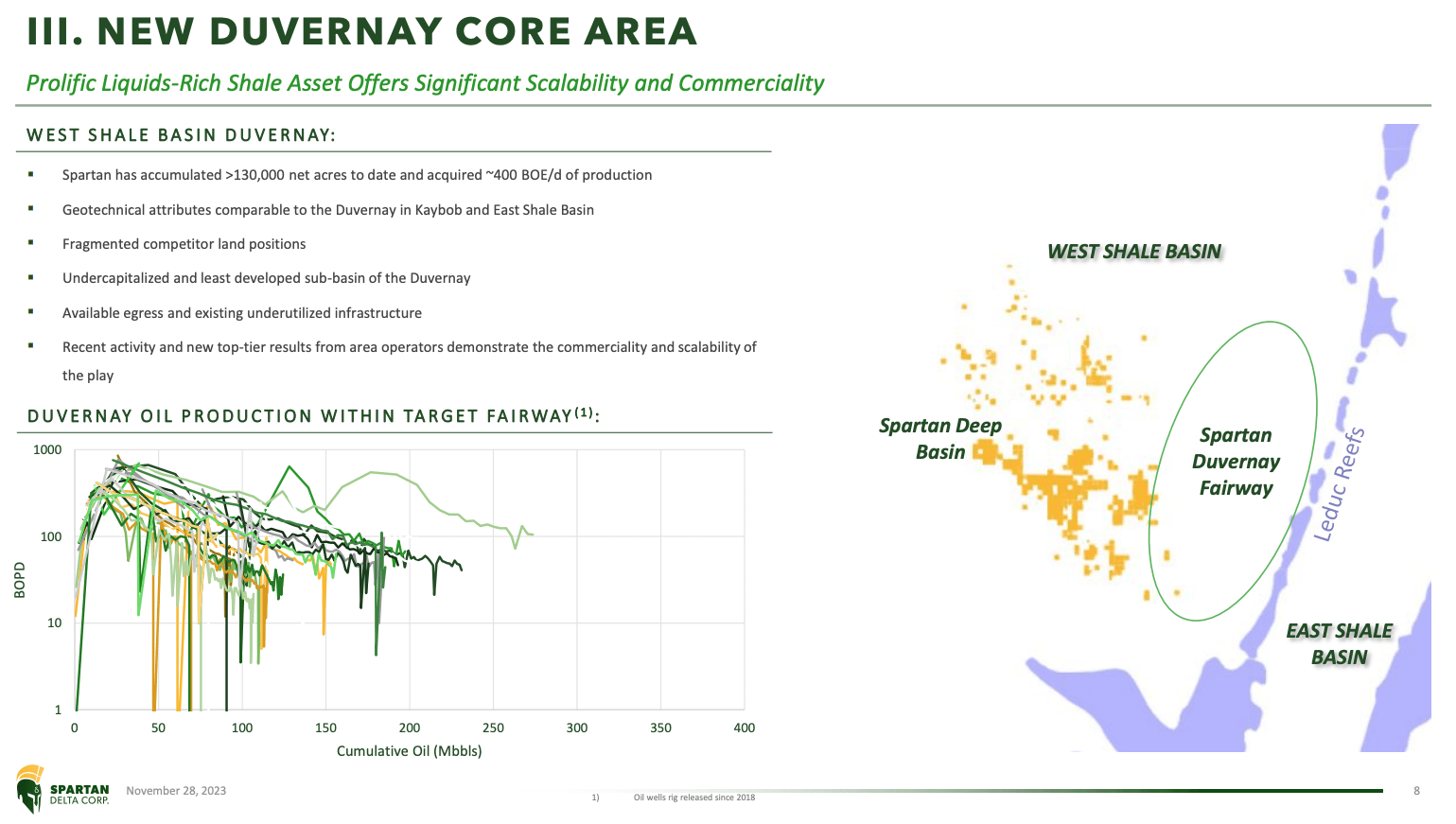

Spartan Delta ( DALXF ) ( SDE:CA ) is a Canadian energy company that is in the early stages of a transformation from mainly natural gas production to an operation focused on NGLs, condensate, and crude oil. This transformation is made possible due to the recent acquisition of 130,000 net acres in the Duvernay Fairway. The Fairway has seen levels as high as 89% liquids which exceeds even the well-known Permian Basin (approximately 75% liquid). The transition to higher-margin products will result in substantial free cash flow growth.

The Duvernay basin of Alberta, Canada has a rather shallow depth. The Duvernay basin is thousands of feet shallower than some of the most well-known basins in the United States. This shallowness requires less capital to drill and complete new wells, leading to higher returns for producers.

This provides SDE:CA with a competitive advantage. To capitalize on this advantage, SDE:CA plans to increase production by 7% in 2024 while also improving capital efficiency by 20% as it achieves greater economies of scale. This will allow the company to strengthen its already robust cash flows and balance sheet while it completes plans to best optimize the Fairway and transition into a high FCF business.

To fully evaluate the growth potential of this acquisition, I will evaluate SDE:CA using a slight variation to my three D's method: Depth, Deposits, and Dollars.

A Quick Look

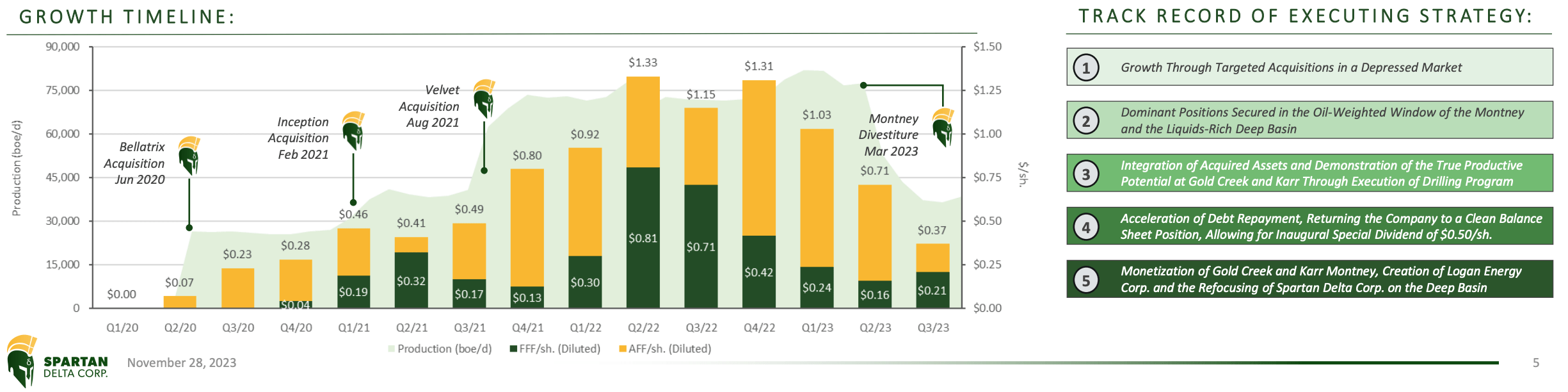

Spartan Delta is the surviving company following a combo asset sale and spin off event. The company sold its Gold Creek and Karr Montney assets for $1.7 billion to Crescent Point ( CPG ) while also spinning off its remaining Montney acreage into a newly formed company, Logan Energy ( LOECF ). The goal of the transaction was to maximize shareholder value through special dividends and shares in both Spartan Delta and Logan Energy.

SDE:CA can now fully focus on its Duvernay assets. Up until recently, SDE:CA solely operated in the Deep Basin of the Duvernay. This area has produced 70% of its volumes in the form of natural gas with the remaining 30% comprised of various liquids. On November 28th, SDE:CA announced it had acquired 130,000 net acres in the Duvernay Fairway which neighbors the Deep Basin.

The Fairway, is a game changer. The Fairway has a significantly different production mix than the Deep Basin, with competitor Baytex Energy registering up to 89% liquid volumes. SDE:CA has not yet included the Fairway into their 2024 capital plans as they continue to study and plan the execution of this high value asset.

{kind=link}

Basin Depth

For those unfamiliar with the Duvernay Basin let's start with our first key feature depth. The depth of a basin contributes to various geological properties but also directly influences drilling and completion costs. Deeper wells require more labor and materials to complete.

The liquids-rich window of the Duvernay is approximately 5,000 to 6,500 feet below the surface. Any well drilled here can be completed at a lower cost than most US basins. The table below compares the depth of this basin to some of the most notable basins in the United States.

| Basin |

| Depth |

| Duvernay |

| 5,000 - 6,500 ft |

| Delaware (Wolfcamp) |

| 8,000 - 10,000 ft |

| Midland (Wolfcamp) |

| 6,000 - 8,000 ft |

| Eagle Ford |

| 6,000 - 10,000 ft |

| Haynesville |

| 10,500 - 13,500 ft |

| Marcellus |

| 4,000 - 8,500 ft |

| Utica |

| 6,500 - 9,500 ft |

The low cost aspect of the shallow Duvernay has allowed SDE:CA to remain profitable in Q3 even with natural gas fluctuating mostly between $2.50 and $2.75 for the quarter. The achievement of remaining profitable for a small-cap company should not be understated.

SDE:CA is still a small producer that has not yet achieved the size to realize the benefits of economies of scale. As SDE:CA grows its production, it stands to benefit from lower operating costs per BOE. Management has guided to increase production 7% in 2024 while also targeting areas with higher liquid content. The net impact is expected to yield a 20% improvement in capital efficiency.

{kind=link}

Basin Deposits

For any energy company, the quality of the rock they drill into will ultimately determine its success. The Duvernay is no different and just like real estate, location matters.

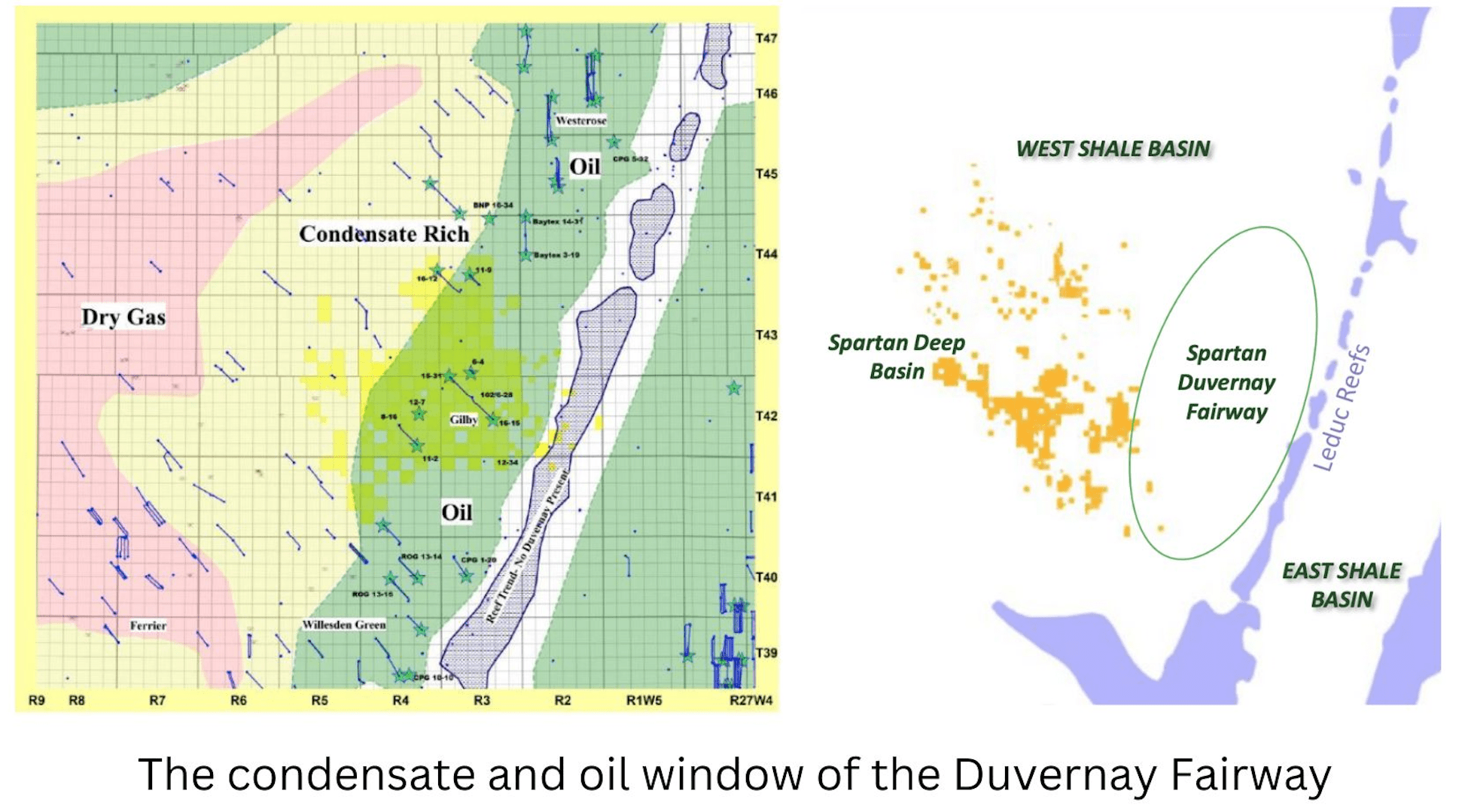

The acquired acreage lies in the T40-T50/R1W5-R5 grid zones using the image geological map below (left). This part of the play has a high concentration of oil and condensate. As one moves further from the heart of the play, the shale becomes deeper and more gaseous. You can see in the image below that the newly acquired acreage is located in a liquids-rich window.

Duvernay Oil Prospect Report - Provided by Journey Energy

{kind=link}

To get into the specifics, the Alberta Energy Commission has provided a very in-depth study of the Duvernay formation. Using these reports, I estimate the liquid portion of the play to be roughly a 50/50 split between NGLs and oil which creates tremendous value for SDE:CA. Transforming the company from 30% liquid to potentially 80% or higher, is a recipe for incredibly higher levels of free cash flow and share price growth.

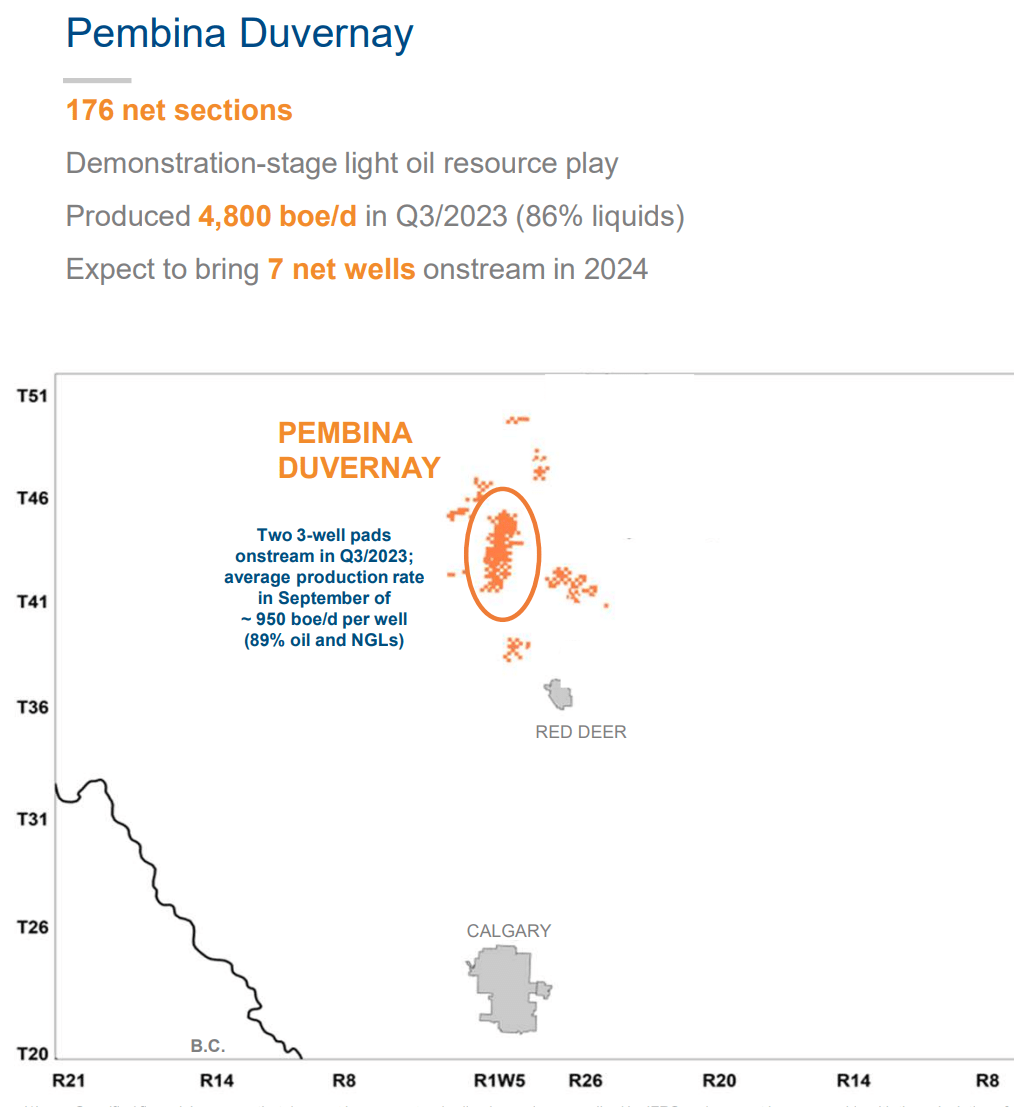

Operating neighbor Baytex Energy ( BTE ), also operates in this same window and has produced very promising results. These wells have produced at moderate rates but yielded extremely high liquid contents. BTE gave the following information in its earnings release.

The six wells generated average production rates of approximately 950 boe/d (89% oil and NGLs) in September (ranging from 790 boe/d to 1,080 boe/d) and continue to track to type curve expectations

This area is clearly in the early innings with relatively few wells drilled to date. Despite this, the initial results have been very promising. These results are also backed by multiple research studies , giving me high confidence that this window can be highly profitable.

This opportunity is magnified by the fact that SDE:CA is mainly a natural gas producer at this point. The Fairway of the Duvernay should easily reveal itself as the highest return on capital compared to the Deep Basin. Production will gradually shift to the Fairway, allowing SDE:CA to be a predominantly liquids producer over time. At the same production rate, SDE:CA stands to have 2x-3x revenue growth by selling a higher value product.

{kind=link}

Dollars - Part 1

To properly frame the potential transformation of this investment, we must first understand it in its original form. For 2024, SDE:CA plans to spend $130C million to drill and complete 19.2 wells. This spending plan projects to increase overall production by 7% up to 39,500 BOE/d with a slight uptick in liquids volumes up to 31% from 29% in Q3.

Using the assumption of $75 WTI and $2.75/GJ AECO natural gas, SDE:CA projects to generate $177C million of free cash flow in 2024. After CAPEX spending, that leaves $47C million remaining. The company plans to allocate the remaining funds to debt reductions. The net debt levels will be lowered to $19C million from the $64.5C million by the end of 2024. This translates into a net debt to FCF multiple of just 0.1x.

The table below summarizes the projected 2024 exit valuations using the current strip price of $2.22/share.

| Metric |

| Projected 2024 Multiple |

| Price to Free Cash Flow |

| 2.2x |

| Net debt to Free Cash Flow |

| 0.1x |

| Free Cash Flow per Share |

| $1.017/share |

All of these metrics indicate SDE:CA is incredibly undervalued even in its current form. For comparison, I plotted the price to FCF for some of the most notable Permian producers. The cheapest was Devon Energy ( DVN ) trading at nearly 10x FCF.

Dollars - Part 2

The second part of the financial analysis is an estimation of what could be the future of Spartan Delta. I began to wonder what the potential would be if SDE:CA fully transitioned from production in the Deep Basin to the Fairway. After all, in the long term, this acreage should command the bulk (if not all) of the capital budget going forward. The Deep Basin just doesn't compete on a ROI perspective.

To start down this road, we need to first look at the management team. The Spartan Delta management team was able to grow a brand new company with zero production in 2020 into two separate companies and a $1.7C billion asset sale. Therefore I believe they remain fully capable of developing this new play into a high value and high cash flow asset. This process may take 2 to 3 years since the Fairway has not yet been included in the 2024 capital plan. However, having an existing business that produces positive cash flow will make growth that much easier.

{kind=link}

The second step is to estimate the Fairway's potential. Using the estimated inventory projected by the AEC, a production profile of 40%/40%/20% (oil/NGL/natural gas) was estimated. Production in the Fairway was modeled as equivalent to the current production out of the Deep Basin (38,000 BOE/d) This projection assumed $75 WTI and $2.50 Henry Hub natural gas. The realized price would grow to $40.5/BOE compared to $17.48/BOE in Q3 of this year . This translates into 132% revenue growth from today's production.

To add conservatism to this estimate, I reduced the projected revenues by 10% and added a 25% increase in operating costs to transition into a new basin. The key data from this model is displayed in the table below

| 2026 Year End |

| $ (Canadian) |

| Revenue (Decreased by 10%) |

| $686 million |

| Royalty Expense (13%) |

| ($89.2 million) |

| Operating Expense (Increased by 25%) |

| ($298 million) |

| Tax Rate (23%) |

| ($69 million) |

| After Tax Net Income |

| $230 million |

| Earnings Per Share |

| $1.33C/share |

With earnings in Q3 registering $0.05C/share, this model implies there is a 6X annual earnings growth potential by transitioning production from the natural gas window to the liquid window of the Duvernay. This type of growth is not normally seen, but the ability to transition from a natural gas basin to liquids basin is not normal either. As mentioned above, a fair amount of "correction factors" were applied to ensure the estimate was not overly optimistic.

The only variable that cannot be accounted for in this model is time. How long will this transition take? My three-year estimate is based on two main factors. First, management isn't starting with nothing like they did in 2020. They have a cash flowing business to help support future growth. Secondly, they have minimal debt obligations. With a net debt position of only $64.5C under a credit facility, there is minimal risk of rising interest rates or maturities interfering with growth plans.

A conservative valuation for a small E&P company such as Spartan Delta would be 5 times earnings. This equates to $6.67C/share or roughly $5/share in USD. At today's price of $2.22, early investors stand to gain 2x to 2.5x on their investment over a 2 to 3 year investment period.

Risks

The most obvious risk to this thesis is if the geology studies don't bear fruit and the liquids-rich window is not as prosperous as indicated. While this would be disappointing, profitability is already proven in a low margin natural gas market. Growth expectations maybe tempered but still extremely robust compared to the general growth rate of the S&P 500. Given that LNG demand is to undergo extreme growth in the 2H of 2024, there is a secondary and backup bullish thesis to be had for Spartan Delta.

Spartan Delta is a home run style investment but given the low cost structure of the Duvernay basin, the risk to capital loss at these price levels appears low.

Summary

This article has laid out an extremely bullish growth story for Spartan Delta. The company has armed itself with what geologically, appears to be a high growth acquisition. The management team has done an excellent job at growing the current business from scratch since 2020. Thus I conclude that this is a capable team to lead the transition into the higher margin liquids window of the Duvernay basin.

You may be skeptical of the potential, I wouldn't blame you. Just to review, I have presented two different geological surveys that indicate a high presence of oil, condensate and natural gas. On top of that, a competitor is producing at rates of 89% liquid in the same operating area. Thus, where there is smoke there is fire.

The low cost profile of the Duvernay basin gives Spartan Delta another leg up on this journey. This clearly is a home run call on my part. If the geological report is too dreamy, the company can still remain cash flow positive giving some margin of safety while swinging for the fences. Spartan Delta is a Strong Buy based on very high potential and a limited downside if my thesis is proven incorrect.

Merry Christmas.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2024 Long/Short competition, which runs through December 31 . With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Spartan Delta: One Of The Best Growth Stories You Probably Have Not Heard Of