USFD - SpartanNash Company Warrants Some Additional Patience To Play Out

2023-11-22 03:54:59 ET

Summary

- SpartanNash Company's financial performance has been mixed, leading to a decline in its stock while the broader market has risen.

- Revenue, profits, and cash flows have all been affected, but management's guidance suggests upside potential in the long run.

- Despite recent challenges, SpartanNash remains cheap compared to similar companies and is expected to benefit from the growing demand for food and related products.

In an ideal world, a stock that you buy would go up instantly after you purchase it. But we don't live in such a perfect place. When buying into the stock market, especially purchasing individual companies, you should be prepared to be wrong, sometimes for a while. Some of the best investments I have ever made end up costing me a lot in the near term. This can be especially true when the financial performance of the companies in question comes in mixed. A good example that has had a rough go as of late, but that I believe will ultimately appreciate, involves SpartanNash Company ( SPTN ), a food distribution company that also happens to have a chain of supermarkets and fuel centers under its belt. Revenue, profits, and cash flows have all been mixed in recent quarters. As a result, shares have fallen at a time when the broader market has risen. But with how cheap the stock is, and when factoring in management's own guidance, I do believe that upside exists in the long run.

A difficult time

The last article that I wrote about SpartanNash came out in early April of this year. At that time, the firm was exhibiting attractive growth on the top line. Cash flows were also doing nicely, but some of the other financial data reported by management was mixed. Management's emphasis had been on growing the business, as is usually the case. But one area that I felt was being ignored was the retail side of the business because of how robust its profits were prior to 2022. This opportunity, combined with how cheap the stock was as a whole, led me to reiterate the ‘buy’ rating that I had on the stock, which is a rating that denotes my belief that shares should outperform the broader market for the foreseeable future.

{kind=link}

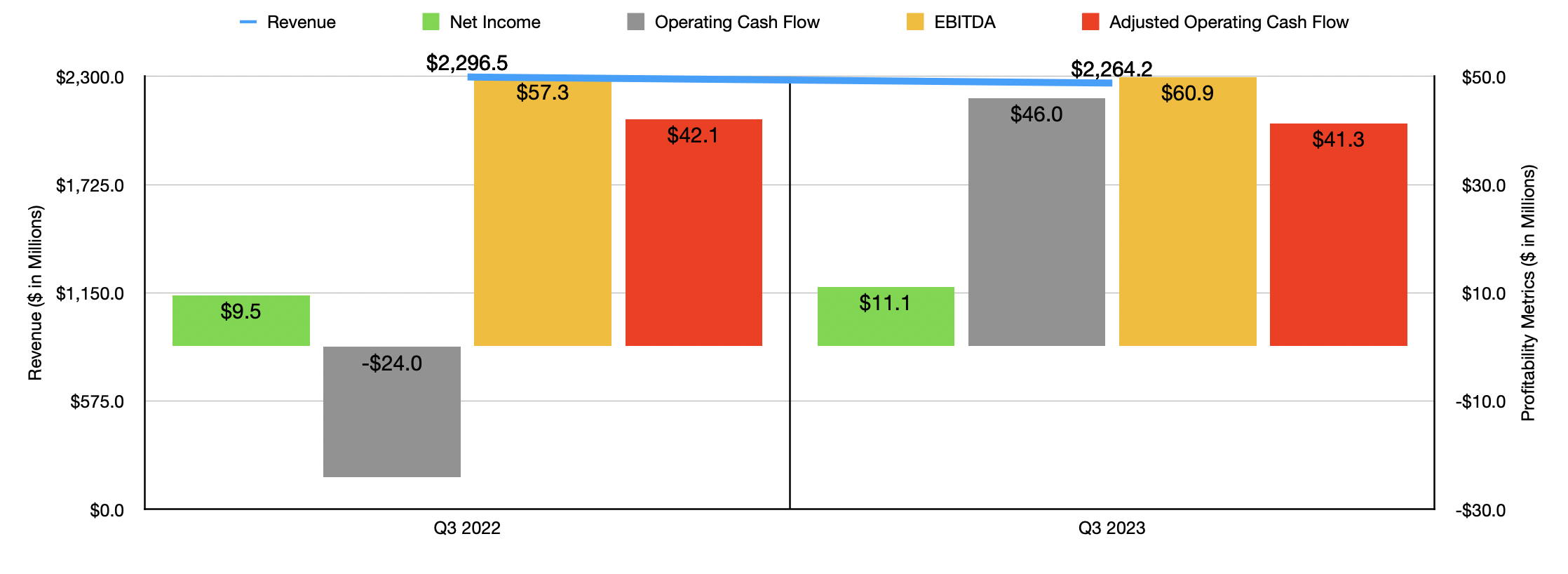

As sad as I am to say this, the fact of the matter is that the market has so far disagreed with my assessment. While the S&P 500 is up 11.2% since the publication of that article, shares of SpartanNash have seen downside of 8.8%. I would make the case that this is likely in response to some of the mixed financial data coming from the company. To see what I mean, we should touch on performance for the third quarter of the 2023 fiscal year . During that time, revenue came in at $2.26 billion. That's 1.4% lower than the nearly $2.30 billion reported one year earlier.

{kind=link}

Both of the company's operating segments suffered during this time. The Wholesale segment, for instance, reported a decline in revenue from $1.63 billion to $1.60 billion. Management attributed this weakness to marketplace demand changes associated with a specific national customer. This more than offset pricing changes, resulting in a reduction in volume of 5.4% year over year. The retail side of the business also took a hit, dropping from $666.6 million to $662.2 million. That decline, according to management, came about even as comparable store sales grew by 1.2%. But a 6% reduction in volumes hit the company, as did a 0.8% drop in fuel sales.

On the bottom line, the picture was more mixed. Net profits actually increased from $9.5 million in the third quarter of 2022 to $11.1 million the same time this year. This was largely the result of a decline in the selling, general, and administrative costs of the company from 14.5% of sales last year to 14.3% this year. But not every profitability metric came in strong. It is true that operating cash flow went from negative $24 million to positive $46 million. But if we adjust for changes in working capital, we would see a decline from $42.1 million to $41.3 million. On the other hand, EBITDA for the company improved from $57.3 million to $60.9 million.

{kind=link}

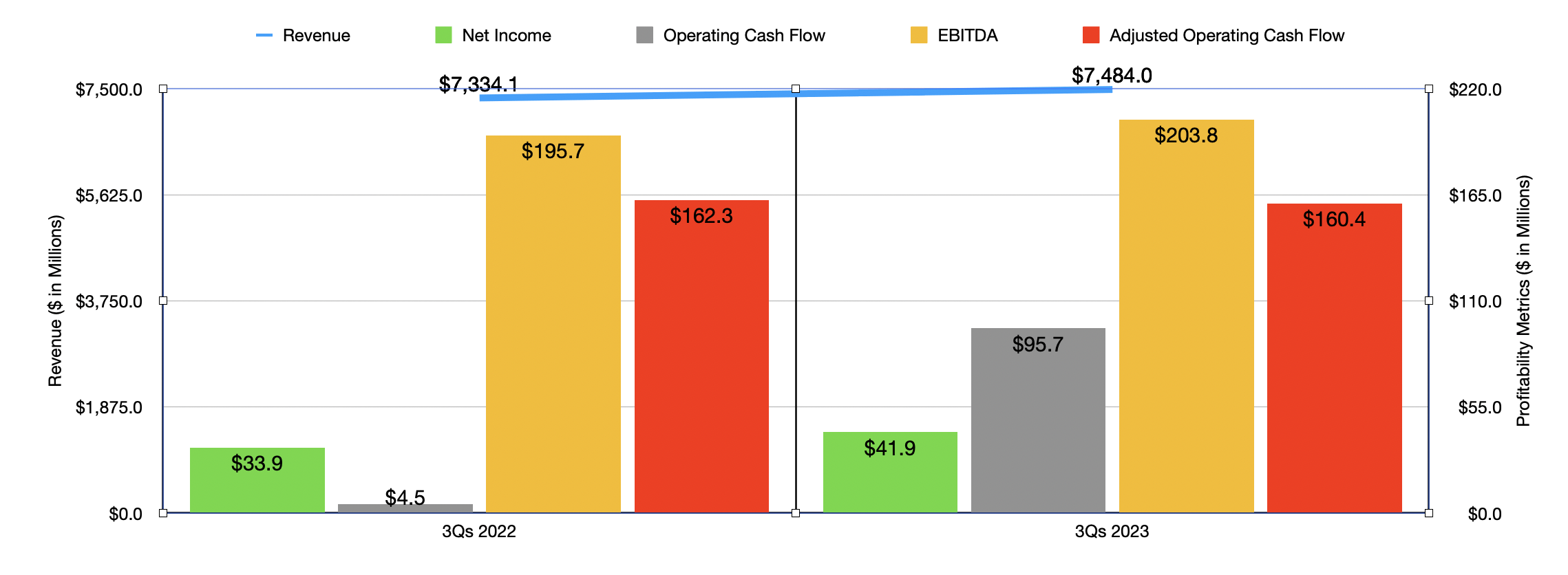

I think it's important to note that, in some respects, the third quarter was a bit unusual. If we look at the first nine months of 2023 as a whole, we would have seen revenue increase by 2% from $7.33 billion to $7.48 billion. Both segments improved during this time, with the Wholesale segment benefiting from a 4.2% increase in volumes and the Retail segment experiencing a 3.6% rise in comparable store sales even as fuel sales dropped by 1.3%. Net profits and operating cash flows, as well as EBITDA, all grew year over year. Only adjusted operating cash flow worsened during that time.

It is the performance for the first nine months in its entirety that has made management confident that revenue for all of 2023 will be stronger than it was last year. At the midpoint, revenue is expected to be $9.75 billion. That would be 1.1% above the $9.64 billion reported for 2022. At the midpoint, EBITDA is forecasted to be about $255.5 million. By comparison, in 2022, it came in at around $243 million. No guidance was given when it came to adjusted operating cash flow. But based on my own estimate, it should be around $193.7 million this year.

{kind=link}

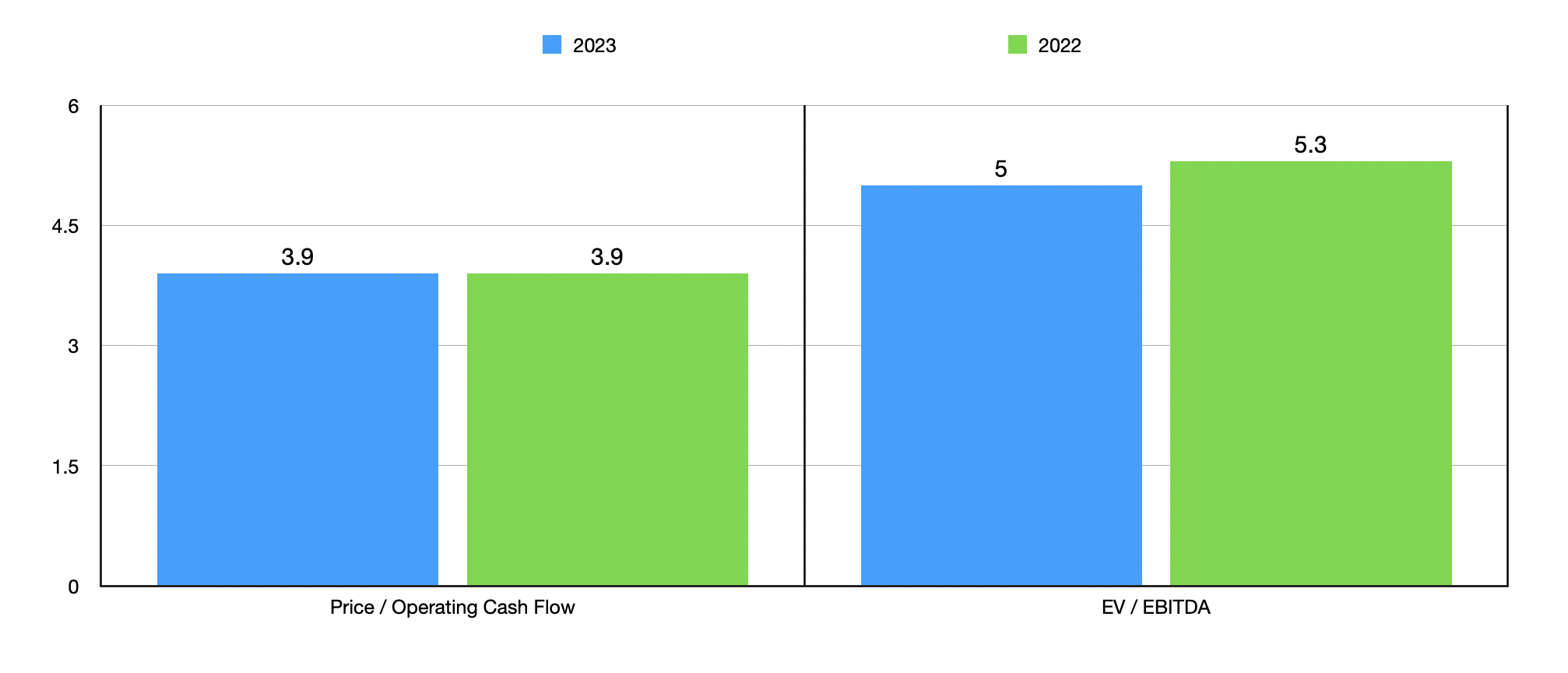

Using these figures, I was then able to create the chart above. As you can see, the stock is trading in the low- to mid-single digit range for both of the profitability metrics that I looked at. And pricing does not change significantly from 2022 to 2023. While the picture could always be better, this is positive in the grand scheme of things. I then, in the table below, compared the firm to five similar companies. On a price to operating cash flow basis, two of the five companies were cheaper than our prospect. Using the EV to EBITDA approach, however, SpartanNash ended up being the cheapest.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| SpartanNash Company |

| 3.9 |

| 5.0 |

| United Natural Foods ( UNFI ) |

| 1.5 |

| 6.3 |

| The Chefs' Warehouse ( CHEF ) |

| 94.7 |

| 11.6 |

| The Andersons ( ANDE ) |

| 1.5 |

| 7.3 |

| Performance Food Group Company ( PFGC ) |

| 16.3 |

| 10.2 |

| US Foods Holding Corp. ( USFD ) |

| 9.7 |

| 11.5 |

Takeaway

At this point in time, it is clear to me that SpartanNash is not doing excellent. But it is certainly not doing poorly either. Financial performance has been mixed, especially in the most recent quarter. But shares remain very cheap, both on an absolute basis and relative to similar companies. In the long run, this country will see an ever-growing population and that leads to more demand for food and products related to food. Ultimately, this will bode well for the firm. Because of these factors, I do still believe that the ‘buy’ rating I assigned the stock is appropriate at this time.

For further details see:

SpartanNash Company Warrants Some Additional Patience To Play Out