STEW - SPE: A Discounted Opportunity

2023-04-10 11:45:58 ET

Summary

- SPE regularly trades at a discount, but that discount has been widening significantly.

- The fund suffered in 2022, as did most equities and bonds, but held up relatively better than the market.

- With a larger weighting to CEFs, the fund also had to contend with widening discounts in those positions across the board.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on March 27th, 2023.

One of the main opportunities, but also the frustration of investing in closed-end funds, is their discounts and premiums. They can trade at significant discounts for considerable periods of time - almost perpetually. However, that's generally where their largest opportunities are too. Special Opportunities Fund ( SPE ) is one such fund that is showing a potential opportunity as the fund's discount gets wider and wider more recently.

The timing of our last update was a fairly good one, right after a big drop. Since then, returns have been positive when figuring the distribution into the performance. That being said, more recently, the fund has been dropping, which has more to do with the discount widening than the actual performance of the underlying portfolio.

SPE Performance Since Prior Update (Seeking Alpha)

I think that this still represents a fund that is worth checking out for investors, but with realistic expectations. This fund isn't your usual fund and won't be for everyone. The S&P 500 reference above is the general guide to showing how the market performed. While that is fair if you want to use it as a benchmark, I don't believe it's very appropriate for comparing SPE. SPE is a much more unique fund with positions across all assets, including fixed-income assets that wouldn't be compared to equities.

The Basics

- 1-Year Z-score: -2.43

- Discount: 16.78% (based on 3/24/2023 reported NAV)

- Distribution Yield: 9.80%

- Expense Ratio: 1.89%

- Leverage: 28.35%

- Managed Assets: $205.902 million

- Structure: Perpetual

SPE "employs an opportunistic investment philosophy with a particular emphasis on investing in discounted closed-end funds, undervalued operating companies, and other attractive special situations including risk arbitrage and distressed securities."

The fund is fairly small; it would be even smaller if it weren't for the $58.4 million in preferred stock that it has outstanding. The fund's preferred stock is a convertible preferred with a dividend rate of 2.75% ( SPE.PC ). This is incredibly cheap, given the fact that interest rates have been rising. Most funds are now borrowing at ~5%+ rates.

Performance - Attractive Discount

On an absolute and relative basis, SPE's discount has become attractive. Keeping in mind that SPE only updates its NAV weekly. The latest NAV was reported on 3/24/2023 at $12.87. So it's more of an implied discount and not an absolute discount. This is similar to BDCs, except BDCs only report NAV quarterly.

Ycharts

However, SPE's discount isn't the only discount we are getting as the fund's underlying holdings also can go to significant discounts. SPE has a portion of its portfolio in other closed-end funds and business development companies. BDCs can also trade at significant discounts or premiums.

Of course, when you get 'double' discounts, it comes with the usual caveat of expenses on expenses. When looking at SPE's expense ratio of 1.89% in the latest annual report , we should keep in mind that the funds they are holding in a portion of their portfolio will generally also have expenses between 1% to 2% as well.

In the case of SPE, you also get leverage on leverage, which should be considered as it can be a more volatile fund. Which is another factor to consider when it comes to expenses. The total expense ratio for SPE is 2.03%. Considering they also hold some leveraged funds, a portion of their assets could be seeing expenses of ~4%+. That requires a lot of positive performance to be able to overcome such a cost.

That being said, the fund actually outperformed the market last year on a total NAV return basis. As I mentioned, the fund is a multi-asset approach, investing in a broad portfolio. Therefore, I've also included Vanguard Total Bond Market ETF ( BND ), another relevant ETF, along with ( SPY ) for some added color.

Ycharts

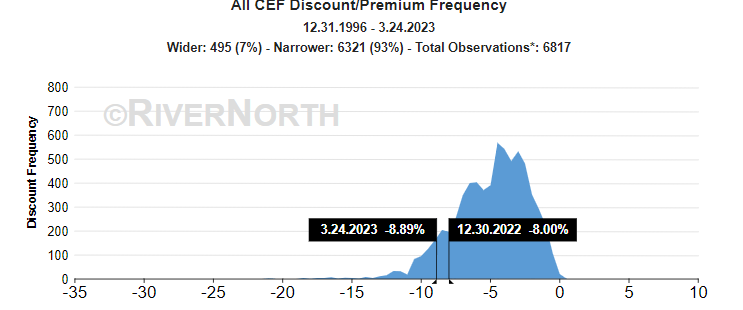

That's even despite widening discounts in the CEF space. CEFs started 2022 at historically narrow discounts across the board; on December 31st, 2021, the average discount was -2.51% for all CEFs. Since then, we've seen discounts widen to historically large levels. This means that not only is SPE's discount widening, but the actual underlying portfolio discount was also widening on a portion of their assets. If that hadn't occurred, the total NAV returns would likely have been down even less. We wouldn't know exactly unless it was provided by the fund showing what the fund's underlying CEF discounts had been on average.

{kind=link}

The outperformance relative to the equity market would seemingly be thanks to the fund's other unique characteristic of carrying a sizeable portion of its portfolio in special purpose acquisition companies or SPACs. These were hugely popular in 2020 and through 2021 for a period. However, since most of them have had sizeable losses since their de-SPACing, their popularity has largely faltered.

Of course, it isn't the SPACs' fault actually; it was the types of companies they were combining with. Growth-oriented companies that wanted to go public as fast and cheaply as possible, usually with limited profits or even limited products and services to sustain a business. That being said, SPACs are often given a negative connotation now.

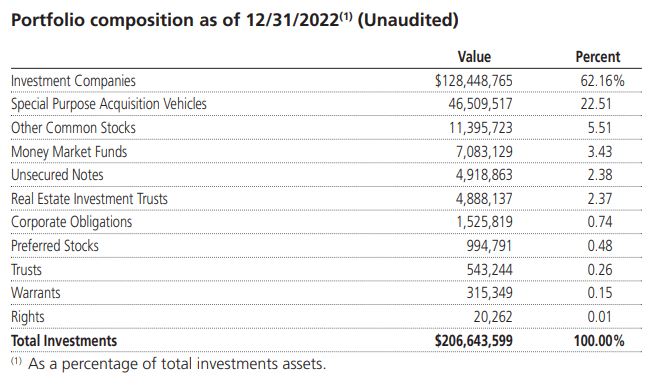

What SPE is investing in, though, are SPACs that are pre-merge, meaning they are essentially cash or cash-like investments. With short-term Treasuries and cash yielding something these days, even sitting in these should be earning the fund something. They listed 22.5% of the fund's assets as being in SPACs at the end of 2022.

With their leverage cost of only 2.75% locked in at a fixed rate. Thanks to a messed up (inverted) yield curve, the actual shorter-term 6-month and 3-month Treasuries appear to be yielding higher than the 1-year. Either way, SPACs can now earn around 4% in these cash-like instruments - above what SPE's leverage cost is.

Ycharts

So while I wasn't too excited about SPAC exposure, now it looks like at least a bit better of a deal. That being said, it once again highlights why we can't compare SPE solely to the S&P 500 Index. Making a spread around 1 to 2% above leverage costs isn't going to set your portfolio on fire, but it also doesn't hurt your portfolio now.

Distribution - 8% Managed Distribution

The fund's distribution plan is simple to understand. They have it based on an 8% NAV on the last day of the year that resets annually. If NAV is higher than the previous year, the distribution will increase. If not, as it wasn't in the previous year, then it goes down. Therefore, we don't get any big shock when they announce their distribution in either direction.

That being said, thanks to the fund's large discount, the distribution rate for investors comes to 9.80% currently. At the same time, the NAV rate is still around the 8% target at 8.08%, to be precise. That being said, some investors still like to see what the fund was earning in terms of income and realized or unrealized gains or losses.

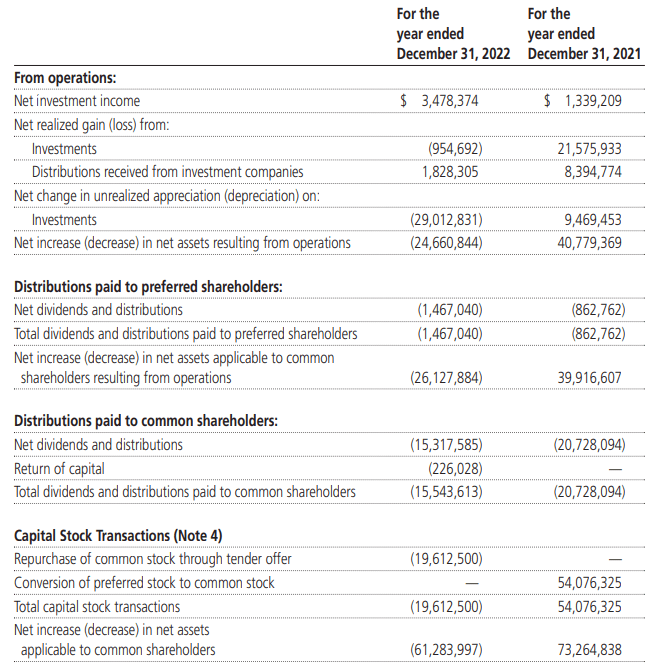

In the last year, the fund saw its NII rise significantly. That being said, it clearly still wasn't close to being able to cover the fund's distribution. After the preferred shareholders were paid, there was around $2 million left over for common shareholders against the $15.544 million paid in the year.

{kind=link}

After the fund's tender offer, reducing the number of outstanding shares and the reduction in the distribution back to their managed rate, the total distributions being paid out will be lower. Common shares outstanding at the end of 2022 were at 11,462,964. Based on that and the annualized distribution that is projected for this year (barring any alteration to the fund's managed plan) will see the fund distribute ~$11.926 million for the year.

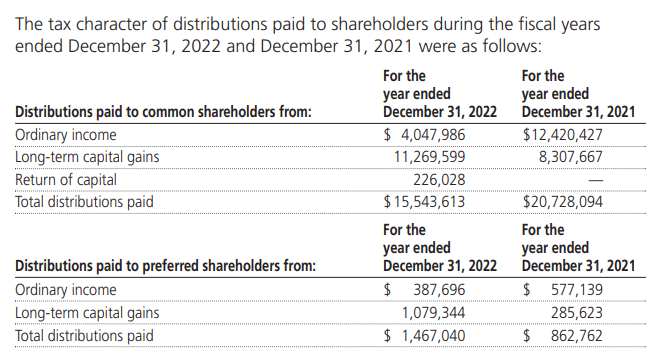

For tax purposes, despite not taking in any material amount of long-term capital gains for the 2022 year, the distribution was still largely classified as long-term capital gains. This was the case in the previous year too, but they had realized significant gains in the prior year. This a good reminder that what the fund earns in a given year doesn't always translate into how the distribution is classified at year-end.

{kind=link}

SPE's Portfolio

We already broke down the SPAC exposure in terms of its impact on SPE under the performance. That being said, SPACs make up the minority of their investments. Instead, the largest bucket in the fund is dedicated to investment companies. This represents both the CEFs and the BDCs in the underlying portfolio.

{kind=link}

One of the benefits of SPE that I've highlighted previously and continue to find an appealing part of the fund is it holds some of the "old school" CEFs. These are the SRH Total Return Fund ( STEW ) (formerly Boulder Growth & Income Fund (BIF)), General American Investors ( GAM ), Central Securities Corporation ( CET ) and Adams Diversified Equity Fund ( ADX ). These are generally the older equity funds that don't get a lot of attention. They trade at considerable discounts and have done so and are expected to continue to do so for the foreseeable future too.

Ycharts

Some of the problems with these funds are generally lower distributions on a quarterly or semi-annual basis. CEF investors tend to push up funds that pay out sizeable distribution rates - whether their earned or not. That being said, SPE takes the exposure to these funds and turns them into monthly distribution plays at much higher distribution rates too.

STEW and GAM were the first and second largest holdings in this fund at the end of 2022. In our prior update, these two positions were reversed in their order. CET was the third largest holding previously, but Texas Pacific Land Corp ( TPL ) and CION Investment Corp ( CION ) now come in as the third and fourth largest holdings. That's pushed CET down to number five.

TPL is one of their fairly rare individual common stock holdings in the fund. This is an oil and gas play. Naturally, as an activist team is managing this fund, there is more to the TPL play here than just investing in a company. This is outlined in the latest annual report.

One of our largest operating company investments is shares of Texas Pacific Land, a company that owns approximately 880,000 acres of land in West Texas, primarily in the Permian Basin, and has traditionally generated revenue through rental and royalty payments by oil and gas producers. Despite generally strong stock performance over the past few years, a number of shareholders, including us, believe that its potential is not being fully realized and that senior management has deployed capital generated by its traditional high margin business to other businesses with lower margins to justify the executives’ extremely high compensation. We think most of TPL’s profits should be used to repurchase its shares or be distributed to stockholders. The company has sued its largest shareholder for allegedly breaching a promise to vote its shares in accordance with the Board’s recommendation on a proposal that is arguably a prelude to an acquisition. We believe the shareholder will argue that the proposal in question is exempt from its voting agreement. While it is difficult to predict the outcome of this lawsuit, a ruling for the shareholders could be a catalyst for a higher stock price.

Conclusion

SPE remains an interesting investment choice, but I would maintain that it isn't for everyone. Some investors will enjoy investing alongside activists in a highly diversified portfolio, while others won't find it appealing. That being said, the fund's massive discount sparks my interest in this latest update. While the fund regularly trades at a deep discount, this goes even wider than usual. At the same time, the fund's underlying holdings are also experiencing wider than-usual discounts. Both of those factors contribute to the potential opportunity for adding at this time.

For further details see:

SPE: A Discounted Opportunity