BRW - SPE And BRW: Investing With The Activists

2023-07-25 17:30:06 ET

Summary

- Closed-end funds offer opportunities for investors to exploit discounts and premiums, with Bulldog Investors and Saba Capital Management being major activists in this space.

- Both Bulldog and Saba offer publicly traded CEFs that can pool some of their targets into these funds, providing discounted exposure to discounted investments.

- Despite the added expenses of investing through a CEF into another pool of CEFs, both funds offer attractive discounts, with Special Opportunities Fund looking particularly attractive.

Written by Nick Ackerman, co-produced by Stanford Chemist.

One of the primary ways to exploit closed-end funds for opportunities is by taking advantage of discounts/premiums. This is a fairly unique characteristic of CEFs as all investments can be under or overvalued at any time; CEFs literally tell you what they are valued with their net asset value per share.

Despite being told exactly what the value should be, investors still allow significant discounts to open up. This can be for various reasons, higher expense ratios, active management that can underperform passive investments and future prospects of losses, or just being averse to leverage. The majority of CEFs are leveraged, but not all.

These discounts and premiums can run for significant periods of time; nearly perpetual discounts seem a permanent fixture for some funds. However, there are some ways to monetize these discounts. One of those ways is following activist investors in the CEF space. Two of the major players in the space are Bulldog Investors and Saba Capital Management.

Fortunately for investors, we don't have to just watch out for what these two management teams are up to. Instead, they offer publicly traded CEFs themselves that pool their targets into these funds - plus some other investments outside of CEFs alone. Perhaps most ironically, these funds offer some deep discounts themselves, with Special Opportunities Fund ( SPE ) at a discount of 17% and Saba Capital Income & Opportunities Fund ( BRW ) at a discount of around 7.3%.

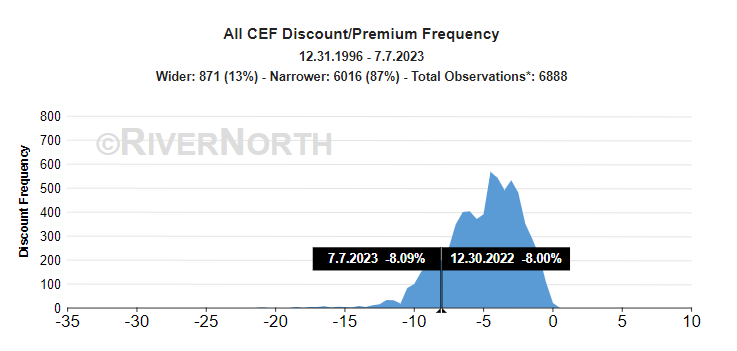

Overall, CEFs are close to historically high discounts . So these funds provide discounted exposure to discounted investments themselves. Of course, a downside of investing through a CEF into another pool of CEFs is that it also means expenses on expenses.

CEF Discount/Premium Average Relative to History (RiverNorth)

{kind=link}

Special Opportunities Fund

- 1-Year Z-score: -1.09.

- Discount: -16.92% (based on 7/21/2023 reported NAV).

- Distribution Yield: 9.28%.

- Expense Ratio: 1.89%.

- Leverage: 27.41%.

- Managed Assets: $212.976 million.

- Structure: Perpetual.

SPE " employs an opportunistic investment philosophy with a particular emphasis on investing in discounted closed-end funds, undervalued operating companies, and other attractive special situations including risk arbitrage and distressed securities."

The fund's NAV is reported weekly rather than daily, as is the case with most CEFs. However, weekly is still frequent enough to give us a good idea of what the current valuation and potential opportunity could be for this fund. This fund was actually a target of Bulldog itself, as it was formerly the Municipal Income Fund, that was taken over by Bulldog and renamed in 2009.

At the present time, the fund's discount is quite large, as we can see below. It is trading well below its historical average of the last decade. Remember, this is on already highly discounted CEFs historically.

YCharts

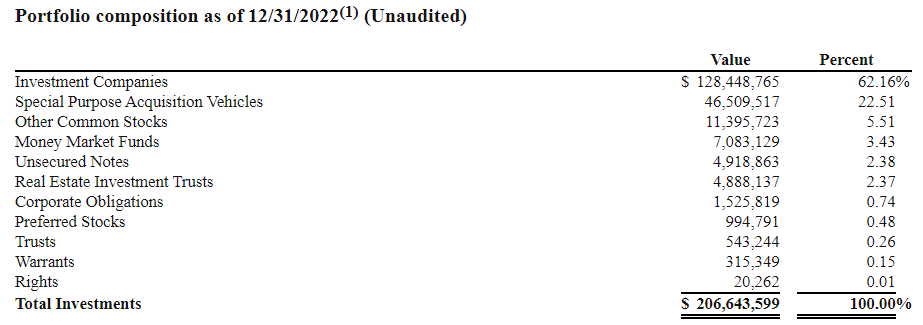

The fund carries significant exposure to other investment companies, around 62%, when they last reported their breakdown.

{kind=link}

However, we also see that special purpose acquisition vehicles or SPACs are another large exposure for the fund. This isn't actually that unique, as BRW also shares this characteristic of meaningful exposure to SPACs. These are SPACs before they merge with a company. Essentially, at this point, they are pooled T-Bill or other cash equivalent funds until they find a potential merger opportunity.

Since cash is paying something these days, it isn't necessarily a terrible idea to put cash aside in this area of the market until opportunities can come up. SPE was also able to leverage itself through a preferred Series C Convertible Preferred ( SPE.PC ) offering with a 2.75% fixed-rate dividend. Therefore, after its leverage costs and even its higher expense ratio, they could be making some positive spread on these SPACs, with T-Bills now paying 5%+.

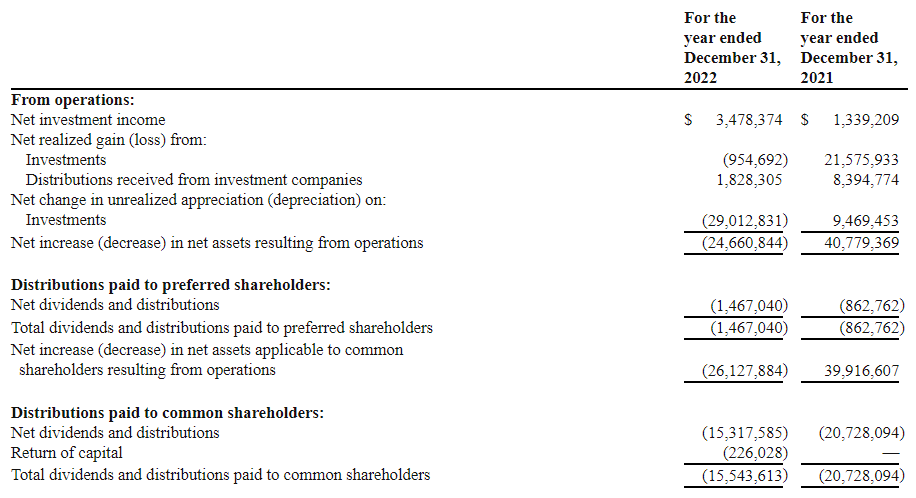

This is likely one of the reasons why we see net investment income climb quite materially in the last year for the fund. This was also before full rates have taken effect. In the next report, we should see NII increase further, all else being equal.

{kind=link}

Coverage of the distribution will improve with higher NII, but in the end, it ultimately doesn't matter. One of the other features of both of these funds is having a managed distribution plan. For SPE, it's based on 8% of NAV that gets reset annually.

When looking at the largest holdings, BRW is one of the funds that make its way into the top ten for SPE. While it's interesting to see, I guess the one reservation here would be that we would be getting triple expenses at this point - SPE's expenses on top of BRW's expenses on top of BRWs' holdings expenses. Even if strong results occurred, that ~3% of SPE's portfolio is unlikely to do anything for the fund in terms of providing positive results unless there was some overall discount contraction in all three components.

The rest of the portfolio is generally deep-discounted 'old school' CEFs that trade at perpetual discounts. It would be great to see them get a bit more active in trying to shake these funds up.

SPE Top Ten Holdings (Seeking Alpha)

Saba Capital Income & Opportunities Fund

- 1-Year Z-score: 0.91.

- Discount: -7.31%.

- Distribution Yield: 13.18%.

- Expense Ratio: 1.31%.

- Leverage: 18.39%.

- Managed Assets: $370 million.

- Structure: Perpetual.

BRW has an investment objective to "provide investors with a high level of current income, with a secondary goal of capital appreciation." Their website highlights that they will "invest in high yield credit." They will also "opportunistically invest in other products, such as, closed-end funds and special purpose acquisition companies." Then, finally, they will "also use derivatives where it believes it can achieve attractive risk-adjusted returns as a way to reduce portfolio risk."

BRW is also the product of a fund being taken over and completely transformed, just as SPE was. However, in this case, it was Saba taking over what was formerly the Voya Prime Rate Trust. After putting significant pressure on the fund, Voya essentially gave up and dropped the fund after Saba controlled the entire Board.

Saba has been on the move against several BlackRock funds in a fairly public manner, with Boaz Weinstein going to Twitter with several posts. Even more recently, they are taking on 16 different CEFs in a lawsuit over control share provisions.

The discount for BRW might not be as alluring as what we saw for SPE, but it's definitely looking pretty enticing nonetheless. Since the fund was more recently taken over and transformed only starting in 2021, going back further for a discount/premium doesn't make sense. The below chart shows from July 1st, 2021 to today. As we can see, the discount is above its average but still remains at a healthy discount.

YCharts

It should be noted that BRW is less active in terms of its CEF exposure relative to SPE. Instead, corporate bonds and SPACs make up the largest positions in the fund, then followed by CEF exposure.

BRW Portfolio Composition (Saba Capital)

The largest holdings here mirror the type of exposure we see above, with mostly corporate bonds as the fund's largest holdings.

BRW Top Ten Holdings (Saba Capital)

In fact, the only traditional CEF we see as the largest holding here is the BlackRock ESG Capital Allocation Term Trust ( ECAT ) - which is one of the funds that Saba is actively targeting to get Board members. Otherwise, there is the Grayscale Bitcoin Trust ( GBTC ) and Grayscale Ethereum Trust ( ETHE ). GBTC and ETHE are trying to convert to exchange-traded funds. That could immediately see their discounts erased and provide an instant bump to the NAV of BRW.

YCharts

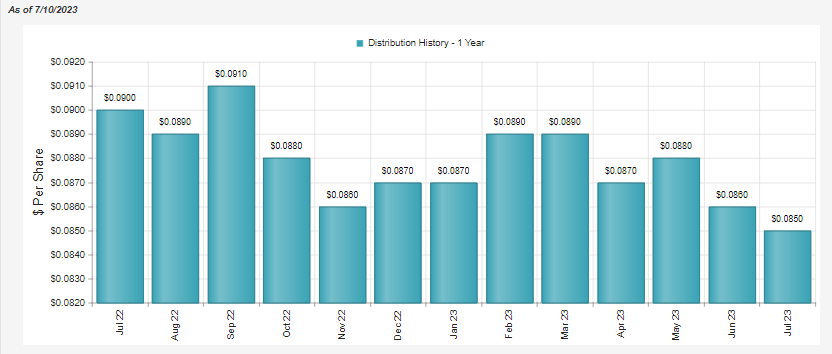

BRW's managed distribution plan is based on a 12% rate on its NAV. However, it's adjusted monthly, which causes a variable payout each month.

{kind=link}

Conclusion

Activists can often offer some opportunities to follow their trades. In the case of Bulldog and Saba, they offer publicly traded vehicles to make following their moves easier. Of course, that comes with added expenses. It also comes with additional discounts to help compensate for those additional costs. Both funds offer attractive discounts, with SPE looking particularly attractive.

For further details see:

SPE And BRW: Investing With The Activists