BRW - SPE: The Ironic Special Discount Greater Action Needed

2023-09-11 22:11:20 ET

Summary

- Special Opportunities Fund is a closed-end fund managed by Bulldog Investors known for using activist techniques to unlock value in rival funds.

- SPE currently trades at an 18% discount to NAV, and more action is needed from management to help reduce this discount.

- The fund aims to pay monthly distributions at a rate of 8% annually, but its small size may pose challenges in sustaining this distribution policy.

Special Opportunities Fund overview

The Special Opportunities Fund ( SPE ) is a closed end fund managed by Bulldog Investors. This manager is renowned for using activist techniques to unlock value in rival CEFs. The irony here now is that SPE exhibits many of the characteristics that this manager looks for in potential targets.

I first discussed SPE here in a 2019 article , so you can refer back there to the older history of this fund and that of Bulldog Investors. Back then I made the following point, “ One reason I don’t mind the idea of investing in an activist fund targeting other CEFs is because they need to seriously consider the discount they trade at themselves. It would be hypocritical for them to run campaigns against other CEFs if they are not being proactive with their own discount. ”

At the time of writing this article now, the discount to NAV for SPE is circa 18%. Back in 2019 I commented that a 12% discount was in the wider band of the 5-year average discount at that time. In recent years an 18% discount is not looking so much an aberration, but something to be expected.

Looking at some of the basic fund characteristics in terms of size and expense ratios, an outside activist might view these issues as problematic. They manage the fund using leverage (currently approximately 27%), with the management fees calculated on gross assets. This inflates the expense ratio as a percentage of net assets. Then the fund is arguably too small also (net assets approximately $160 million), resulting in an expense ratio of 1.89%.

The fund has plenty of flexibility and also invests in various other security types such as other common stocks, BDCs, REITs, Corporate Bonds and SPACs. In particular the SPACs exposure is often quite high, but is more of a lower risk arbitrage strategy as suggested in this article .

SPE sector exposures

Special Opportunities Fund Semi-Annual Report for the six months ended June 30, 2023.

SPE long term performance

Special Opportunities Fund Semi-Annual Report for the six months ended June 30, 2023.

In the past I have defended the performance of SPE in comparison to the S&P500. The decade leading up to 2022 was generally considered challenging for “value” based active investors. I also regard the SPE strategy as somewhat defensive, despite their use of leverage. For example, the SPACs exposure that I referred to as a low-risk arbitrage strategy, has often been a larger weight than the leverage used in the fund. In addition to that, often many of the discounted CEFs held are fixed income funds.

The flat market price returns for the 12 months leading into June 2023, is largely a result of the discount to NAV widening substantially.

Having said all the above, the patience of shareholders is being tested. The calendar year of 2022 did see an environment that should see a fund like SPE stand out. i.e., with the poor performance of many high profile growth stocks. The SPE NAV returns did suffer less of a decline than the S&P500 in 2022, but I regard the difference as modest and a little disappointing. The fund return was a decline of 13.81% that year, compared with the fall in the S&P500 of 18.11%.

Another way to form an opinion on the SPE performance is to cut them slack and view the fund as more of a high income generating defensive allocation to one’s portfolio. I shall discuss the income aspect shortly when I cover their distribution policy. In terms of the overall risk though, I would note SPE still also suffered quite a drawdown during the sharp market slump of early 2020.

Performance of similar funds

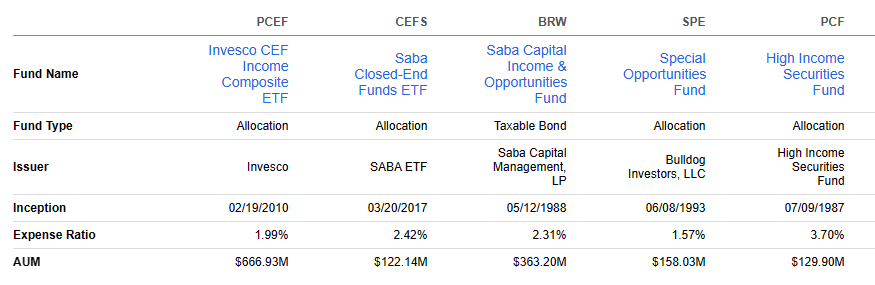

Comparing the performance of some of SPE’s peers can be a little problematic. In some cases, the funds in question have gone through some changes to the manager at points in time. For example, with Saba coming in to manage Saba Capital Income & Opportunities Fund (NYSE: BRW ). Then we have Bulldog Investors taking the reins over another CEF with High Income Securities Fund (NYSE: PCF ). Also analyzing various similar funds will see differences in use of leverage and overall risk amongst them.

Nonetheless I thought it was still worthwhile to take a look for some additional perspective. The above funds, as well as the Invesco CEF Income Composite ETF (NYSEARCA: PCEF ) & Saba Closed-End Funds ETF (BATS: CEFS ) are often sought after by many investors for comparison. It would take too long to go into detail regarding their similarities / differences in this article. It is fair to say they do all target achieving high distribution yields and use closed end funds to a large extent.

{kind=link}

Key Stats Comparison, Seeking Alpha.

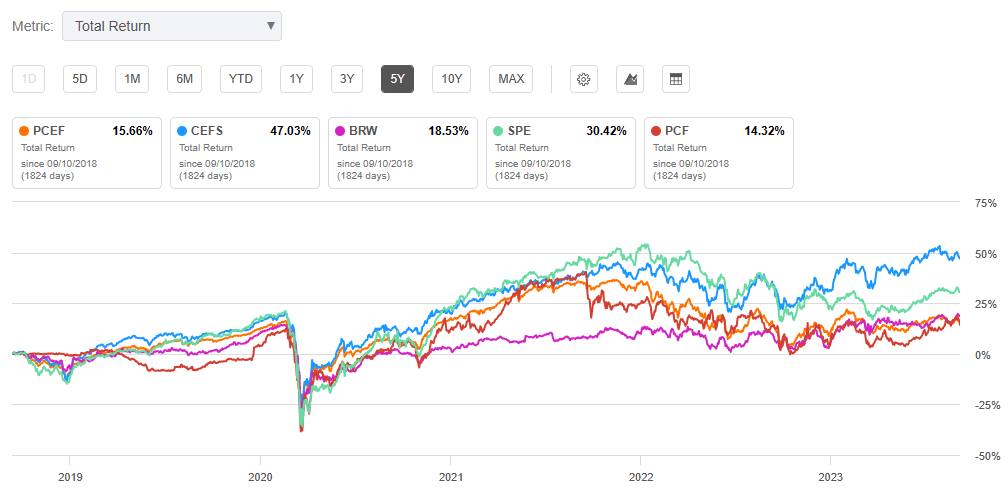

Notwithstanding some issues in performing such a performance comparison, I believe it is still useful to get some perspective regarding the volatility and overall returns. Some of this group I would regard the large drawdowns during market slumps of 2020 and 2022 a little disappointing, as I would the overall returns.

{kind=link}

Total Return, Seeking Alpha.

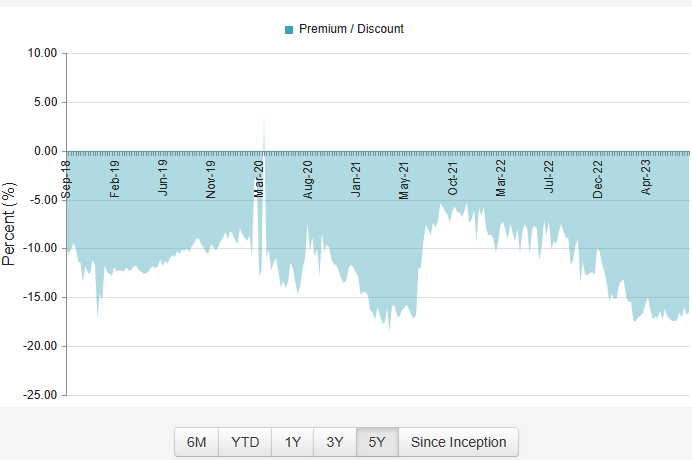

SPE discount to NAV

SPE currently is trading at a very large discount to NAV. I can see this might offset some of the disappointing history, and appeal to new investors at the current time.

{kind=link}

cefconnect, SPE discount to NAV over last 5 years

SPE distribution policy

The fund targets to pay monthly distributions at a rate of 8% annually for 2023. This is based off the NAV on December 31 st , 2022, of $13.01.

There is no guarantee necessarily that they will persist with such distribution policy. As I mentioned earlier, I regard the small size of this fund as less than ideal. Paying an 8% annual distribution may cause issue with the lack of scale for the fund if they cannot back it up with similar underlying returns or better.

In terms of the outlook in future years though, the movement in the NAV in 2023 YTD is encouraging so far anyway. It is the NAV movement rather than the share price movement that is important to consider here. Although some shareholders may be frustrated with the share price returns YTD being near flat, the NAV has gained approximately 5%.

If they navigate the rest of 2023 reasonably ok, then that augurs well for them to continue paying out an 8% annual distribution in 2024. Due to the large discount to NAV that SPE trades at now, effectively that is a yield above 9%. The combination of this, together with a share buyback plan in operation, should offer good support for the stock when at current discount to NAV levels.

SPE buyback

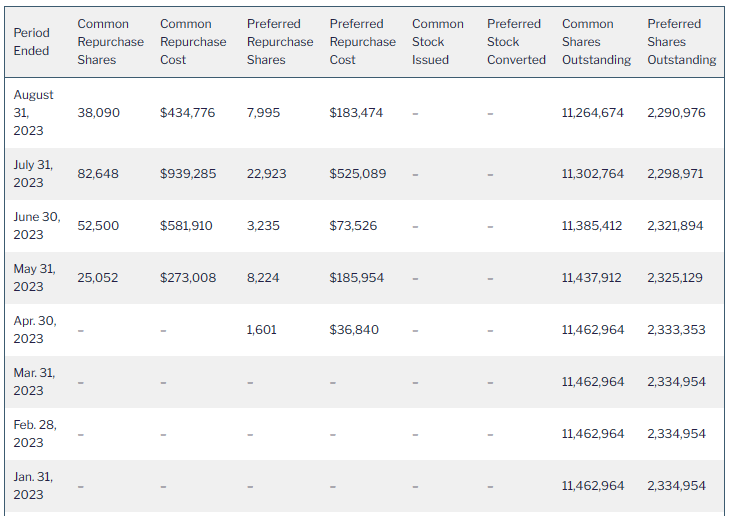

A development in recent months for SPE has been they have been more willing to buy back shares on market at this large discount to NAV.

Their initial bias with this was to action this more via the preferred shares outstanding, but lately have turned more to the common shares.

{kind=link}

specialopportunitiesfundinc.com/fund-shares-outstanding-repurchases-conversions

Either way this is very accretive to the NAV and can be tracked on their website here .

Shareholders might well question management though whether they could be more active here?

Should a tender or a merger be considered?

A tender offer made to SPE shareholders could allow many to be able to redeem shares a lot closer to the underlying NAV, but may start to make SPE a sub-scale fund. Due to this issue, I don’t consider it likely in the next year.

Another CEF managed by Bulldog Investors that I included in the performance comparison earlier was PCF. It has even less AUMs than SPE, but is not too dissimilar in strategy. Whilst some outsiders might look at these two CEFs and conclude a merger seems like a logical solution, it does not appear to be on the cards.

Reading the latest semi-annual report from PCF, the possible solution over there seems to be potentially adding leverage as a tool later in 2023. To quote from this report, “ In addition, we think the Fund should have the ability to prudently use leverage to enhance its returns. Later this year we expect to ask stockholders to vote on proposals to broaden the Fund’s investment parameters, authorize the use of leverage, and engage an investment advisor that has demonstrated success in using activist measures to enhance the value of its clients’ investments .”

My guess is PCF, like SPE, may then charge an investment management fee on gross assets. That might be something shareholders wish to query the investment manager on.

A merger on the other hand might reduce the fixed costs burdens for both sets of shareholders, food for thought.

Some recent activism progress from Bulldog

Investors

It is somewhat ironic that action from Bulldog Investors has assisted in the significant narrowing of discounts to NAV on two closed-end municipal bond funds in recent months.

In the case linked to just above, Bulldog Investors reached an agreement with the investment manager on some measures to close the persistent discounts. These CEFs responded with a tender offer up to 10% of all shares at 98% of the NAV. It is also proposed with these municipal bond CEFs that a liquidity event should be approved in 2025. That is, unless they achieve a sustained period of a discount to NAV of 7.5% or less before then.

SPE should want to remain credible with the boards and shareholders of other CEFs that they make activist campaigns towards. Ensuring its own shares don’t trade at almost a 20% discount to NAV would be a welcome start.

Conclusion

Greater action is needed to see SPE shares trade at a narrower discount to NAV. I can see that happening to some extent in the form of further active purchases of their own shares on market. This is very accretive to the NAV and can assist the NAV returns to hopefully finish with a solid positive number for 2023. This in turn should make the effective distribution yield of 9% continue to be attractive over the next year. I consider SPE therefore as a hold, and believe extra shareholder returns can come about from the discount slowly contracting back to circa 10-12%.

Also assisting SPE right now is the point in the CEF discount cycle more generally. This sees CEF Discount Stats indicating discounts are at historically wide levels. I could also see an environment heading into 2024 of more volatility in equity markets and rate cuts. That may assist in drawing investors back again to favor CEFs like SPE, that trade at wide discounts and use modest leverage.

In the event that the SPE discount reverts back to the mean of closer to 10% again, I would consider exiting SPE shares at that point. At that time, I would have to weigh up whether some better signs are appearing from Bulldog Investors. I would be hoping for better changes in terms of tackling their own discount to NAV problem, and performance in general.

For further details see:

SPE: The Ironic Special Discount, Greater Action Needed